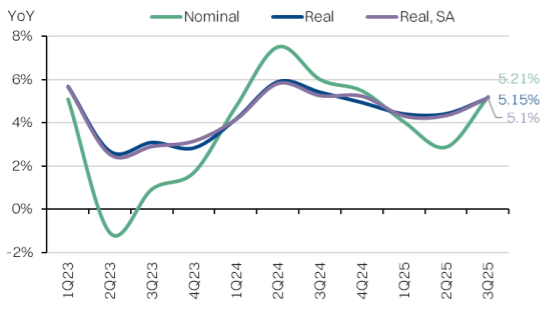

Solid Headline Growth

GDP is well on-track to hit the 4.5% target, following the robust 3Q print. However, the momentum in underlying growth is a little soft, especially for domestic consumption.

Disclaimer: By using this information, you hereby acknowledge that you are fully and solely responsible for evaluating the merits and risks of any investment decision and agree not to hold NewParadigm Research fully liable whatsoever for any actions, omissions and/or damages of any kind or matter arising from such decision.

Key takeaways

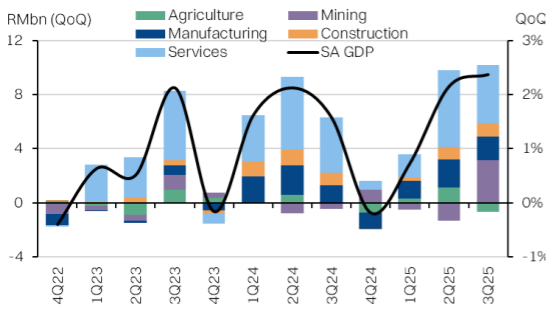

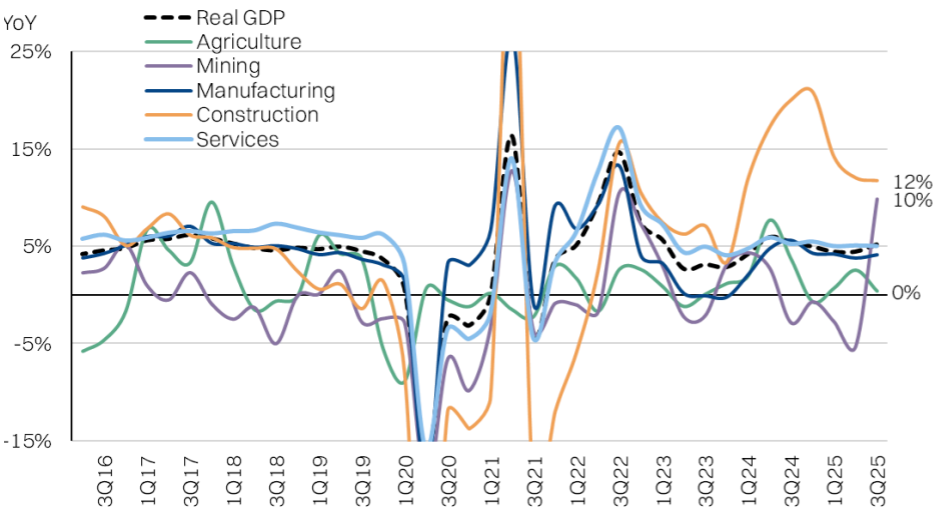

- 3Q25 Real GDP met expectations at +5.2% YoY growth. Sequential seasonally adjusted growth was +2.4% QoQ.

- The rebound was driven by a rebound in O&G production volumes as well as a bounce in net exports.

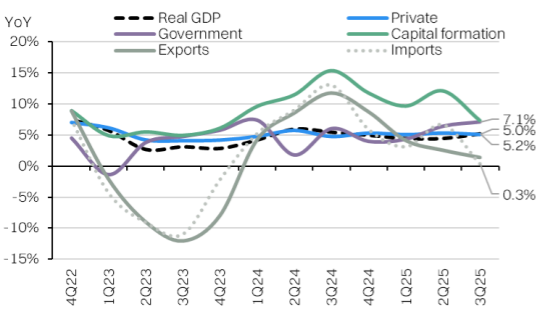

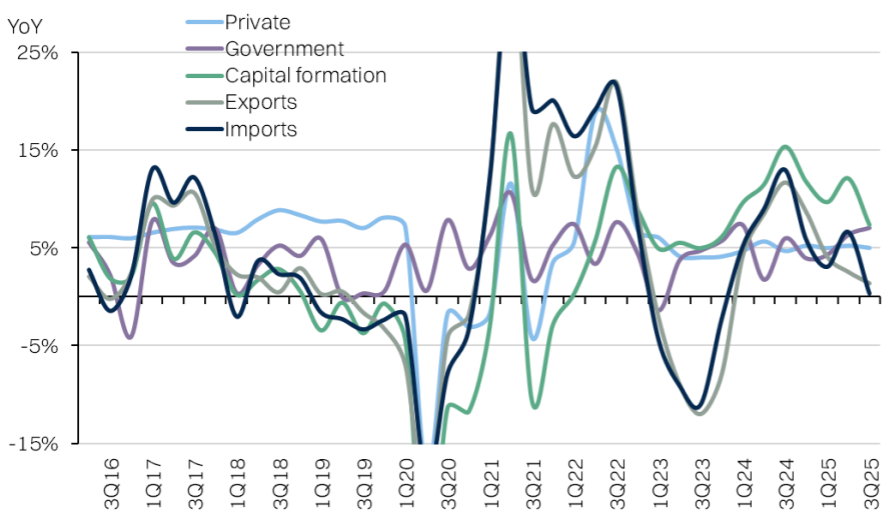

- Private consumption continued to hover around +5% YoY with support from tourism, while capital formation cooled to +7.3% YoY.

GDP (YoY) - Sequential rebound

Seasonally adj. GDP by sector (QoQ)

Real GDP by expenditure (YoY)

Sector specific tailwinds

- On the supply side, there was a +13% QoQ jump in natural gas, following planned maintenance in the previous period, which alone accounted for almost 10% of the sequential real GDP growth.

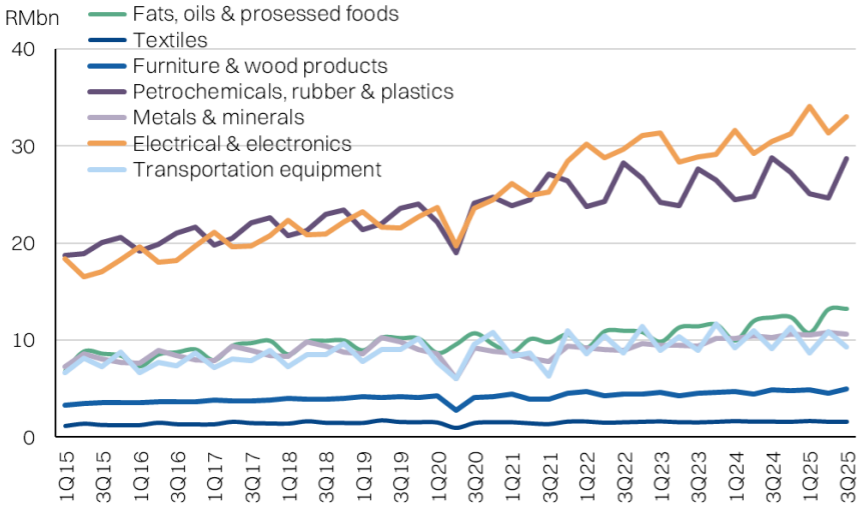

- Momentum in E&E manufacturing (+5% QoQ,+9% YoY) was sustained despite the US tariffs and concerns of a pullback from 1H volume front-loading.

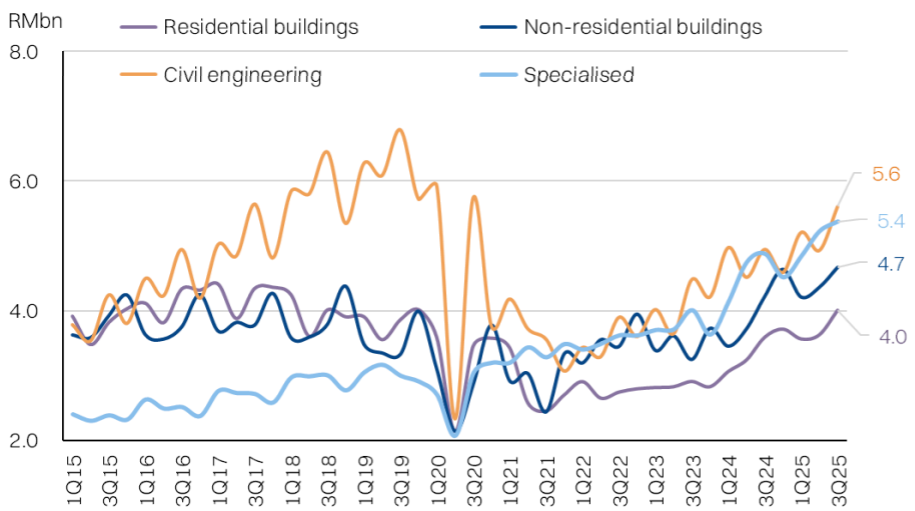

- Construction remains a bright spot (+8% QoQ,+12% YoY), even if headline growth is decelerating from the high of +21% in 2024 due to the high base effect. This was underpinned by strong demand for buildings as well as specialized construction works.

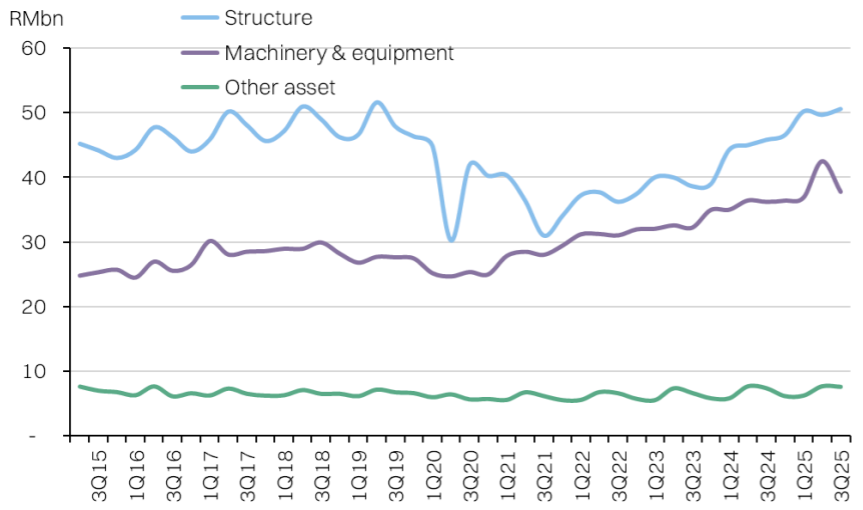

- On the demand side, fixed capital formation (+7% YoY) remains a key growth driver even if there was a sequential cooling (-4% QoQ). The growth in this segment was partially explained by a surge in datacenter investments over the past two years.

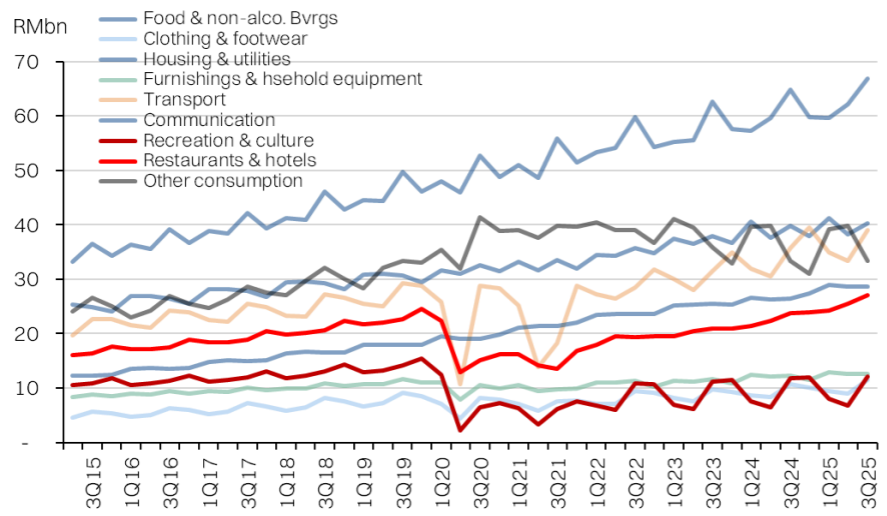

- Overall consumption remains stable at +5% YoY, but still below the pre-pandemic average of +7%. This is a little concerning, given that there was strong support from tourism, which is recovering from a low-base. Restaurants & hotels rose +6% QoQ while recreation and culture services jumped +78% QoQ. Both of these segments have only just recovered to pre-pandemic levels in gross real terms.

- The trade balance also bounced to RM50.3bn, due to a deceleration in retained imports in the quarter as well as the aforementioned bounce in O&G production.

Is the balance of risk shifting to growth?

- GDP is well on-track to hit the 4.5% target, following the robust 3Q print. However, adjusting for some of the tailwinds in the quarter, the momentum in underlying growth is a little soft, especially for domestic consumption. We note that credit to households only grew by +5.7% YoY (2Q25: +6.0% YoY), with disbursements actually flat at -0.4% YoY.

- Furthermore, much of the external shocks do not appear to have materialized in the numbers so far, with manufacturing exports still chugging along. Datacenter investments have also offered a nice boost to growth, but in our view will not translate to a lasting broad-based boost to domestic consumption.

- Against the backdrop of a stronger ringgit, we think the balance of risks is shifting away from inflation and over to growth.

Real GDP

Real GDP by sector - Mining bounced driven by O&G

Real GDP; Construction sector - cyclical boom, supported by DC's

Real GDP; Manufacturing sector - E&E still strong despite tariffs

Real GDP by expenditure - gross fixed capital formation is cooling from a high base

Real GDP, private consumption breakdown - tourism-linked segments laggard recovery

Real GDP, gross fixed capital formation - breather in machinery & equipment

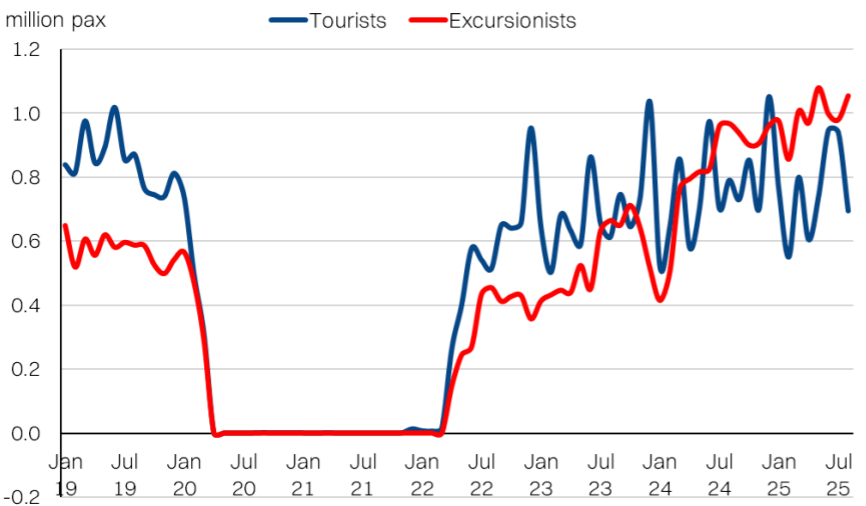

Tourism in focus

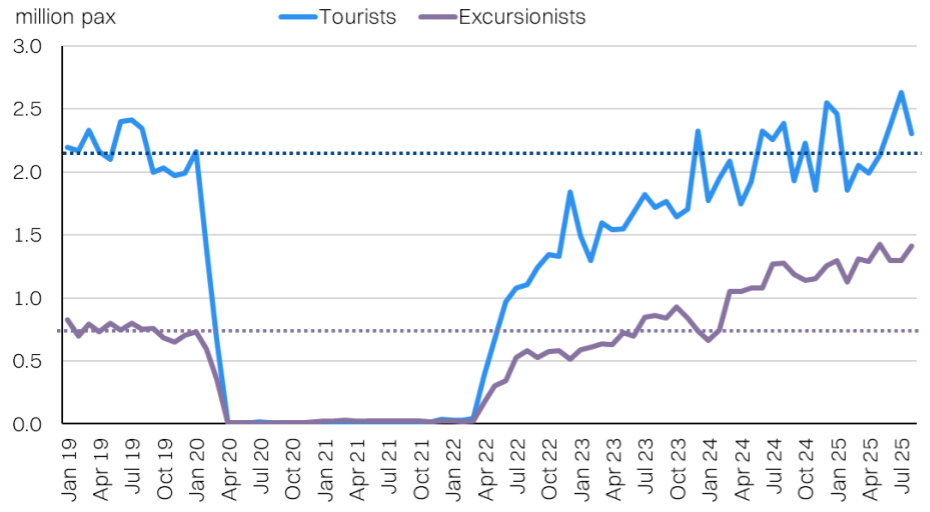

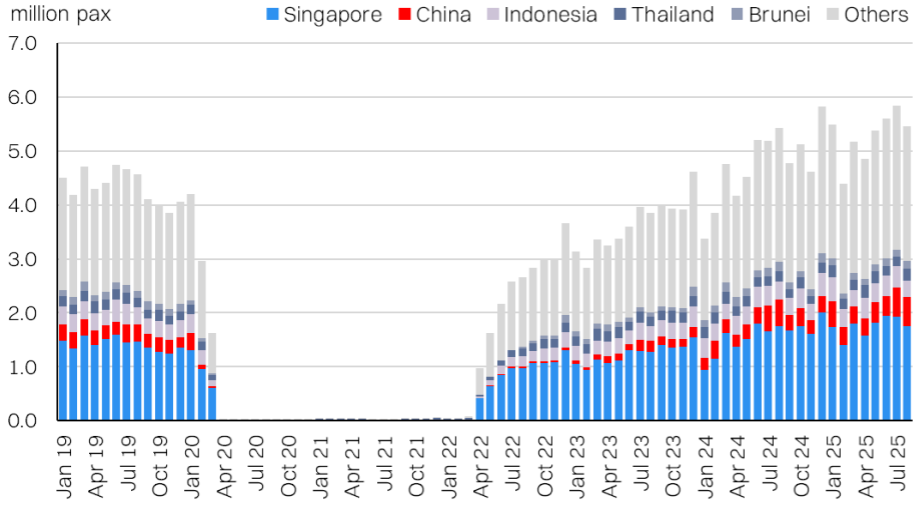

One of the tailwinds for the economy has been the recovery of tourist arrivals to pre-pandemic levels. The big driver of this has been the +47% jump in Chinese tourists to~407k/month on average this year. But with the strengthening of the ringgit, it could put pressure on further upside to tourist arrivals.

Another interesting dynamic has been the surge in day-trippers or excursionists. While tourist arrivals have barely recovered, excursionists are up +76% vs 2019. This is predominantly the result of more Singaporeans visiting JB, with a key driver being the rising cost of living in Singapore and the relative affordability of Malaysia. Compared with 2019, there are +73% more excursionists from Singapore visiting Malaysia in 2025, at almost 1million/month.

Most of this spending will have boosted domestic consumption indicators. The catalyst for further growth will be the completion of the RTS due in December 2026. However, in the short term, the removal of blanket fuel subsidies and the strengthening of the ringgit could also pose some headwinds to the trend.

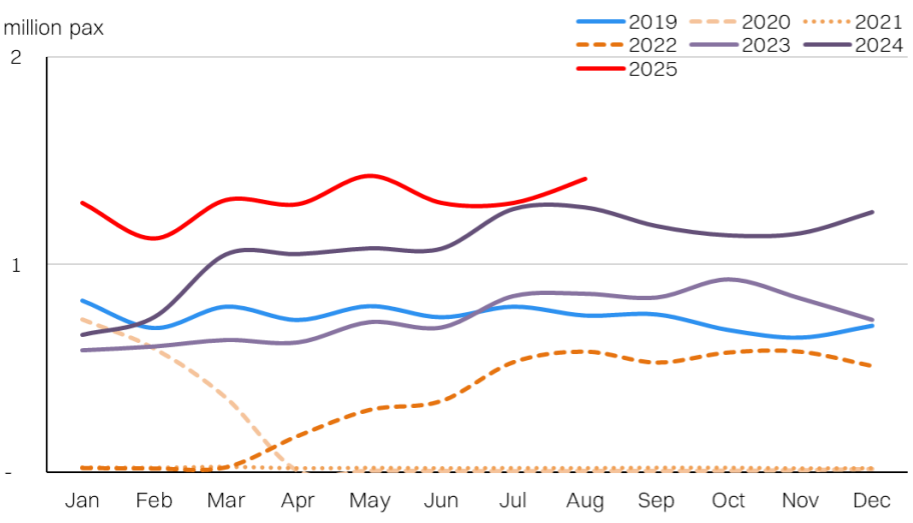

Tourist arrivals have finally recovered, but the upside has come from excursionists

Tourist arrivals - Just about matching 2019

Excursionists - 76% above pre-pandemic levels

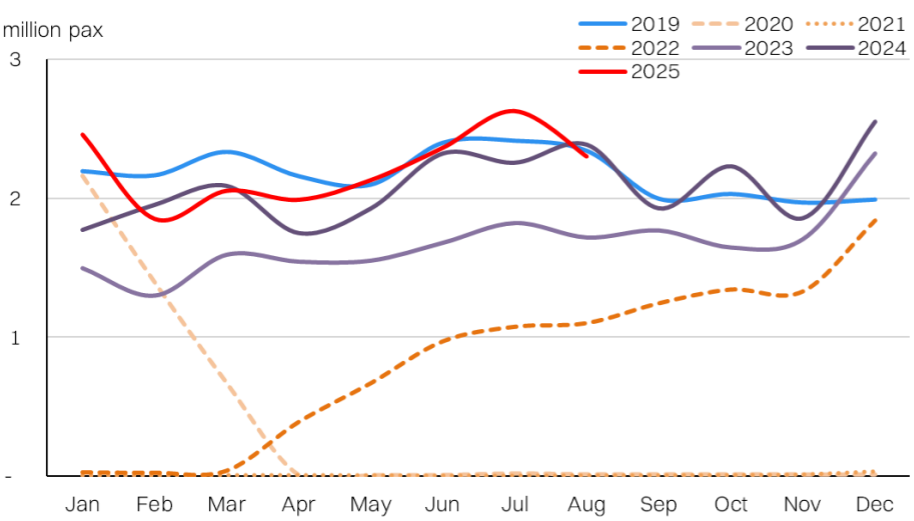

Visitors by country, Singapore remains the most important market

Singaporean visitors - tourist arrivals are lagging 2019, but excursionists have surged