4QFY25 - Meeting Expectations

LSH continues to build a track record of sustained high-margin construction earnings.

Stock information

LSH CAPITAL

LSH | 0351.KL

BUY

Target price: RM3.50

Last price: RM2.19

Market cap (RMm): RM1,836m

Shares out: 838m

52-week range: RM0.730 / RM2.56

3M ADV: RM5.36m

T12M returns: 164%

Disclaimer: By using this information, you hereby acknowledge that you are fully and solely responsible for evaluating the merits and risks of any investment decision and agree not to hold NewParadigm Research fully liable whatsoever for any actions, omissions and/or damages of any kind or matter arising from such decision.

Key takeaways

- 4QFY25 NP of RM34.6m (+32% QoQ,+5% YoY), was in-line with our expectations. Full year FY25 NP of RM101m was up +36% YoY.

- GP margins sustained at 41% for the quarter and 39% full year, driven by the construction segment as well as KL Tower concession.

- Maintain BUY with unchanged target price of RM3.50 on 13x FY27 PER.

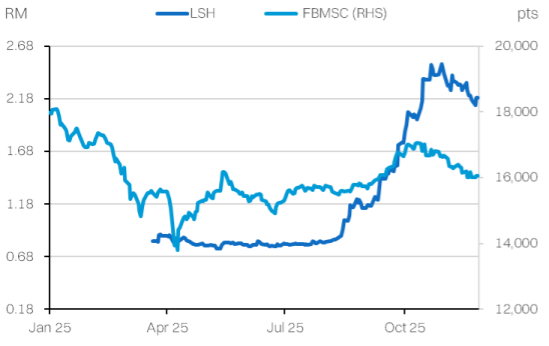

Share price performance

Investment fundamentals

| RMm | FY24A | FY25E | FY26E | FY27E |

|---|---|---|---|---|

| Revenue | 361 | 439 | 600 | 742 |

| Revenue Growth | 1% | 22% | 37% | 24% |

| EBITDA | 106 | 139 | 173 | 213 |

| EBITDA margin | 29% | 32% | 29% | 29% |

| Adj PATAMI | 74 | 103 | 140 | 225 |

| PATAMI margin | 21% | 23% | 23% | 30% |

| ROA | 12% | 12% | 14% | 17% |

| ROE | 16% | 19% | 22% | 28% |

| PER | 21.9 | 18.8 | 13.8 | 8.6 |

| P/BV | 3.4 | 3.6 | 3.0 | 2.4 |

| Yield | 1.0% | 1.0% | 2.0% | 3.0% |

Source: Company data, NewParadigm Research, November 2025

Margin expansion

- Construction segment revenues continued to accelerate at +53% QoQ and +24% YoY. Critically, gross margins for the segment also rebounded from 28% in 3QFY25 to 41%. Recall that the elevated margins relative to peers is one of the key drivers of our thesis.

- The strong performance in the construction segment helped offset a slight shortfall in the property development segment, which saw a sequential -39% QoQ deceleration (still +262% YoY from a low base). This is largely due to the lumpy nature of the segments sales and recognition.

- The KL Tower concession maintained its ~RM12m per quarter run-rate, but saw gross margins rise to 77% (from 63% in 3QFY25). We have modelled for a ~60% GP margin for this business going forward.

- On the back of robust cash flow growth (+RM57m operating cash flow) management declared a dividend of 1.55sen per share, which brings full year payout to 3.89sen per share for a 30.8% payout ratio, which is in-line with management’s 30% payout target.

- Overall, we are positive on the results. the group’s external construction orderbook remains at a healthy level of RM485m, with a substantial replenishment funnel.

Earnings delivery supports thesis

- LSH continues to build a track record of sustained high-margin construction earnings.

- We anticipate the RM3.2bn orderbook funnel over the next 24 months and RM1.8bn GDV in property launches will be the catalyst for valuations going forward.

- Maintain our BUY recommendation with an unchanged TP of RM3.50.