Constrained Populism

Considering fiscal limitations, we are overall positive on Budget 2026, even if market impact might be low.

Balanced but boring

- No major positive or negative surprises for the market. Key sectors include consumer, sin stocks, infrastructure and tourism.

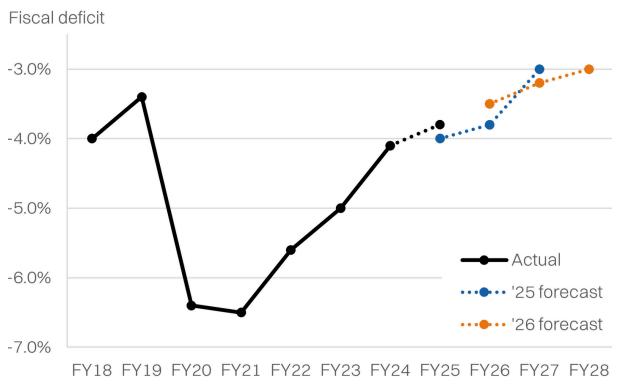

- Headline deficit to fall to 3.5%, but the MTFF target of 3% is pushed out another year. Still, subsidy reforms underwrite the trend.

- Elevated emphasis for spending on key states - Sabah & Sarawak - RM6.9bn and 6bn development expenditure allocated respectively.

Trimming expenditure growth

3% deficit target pushed out by another year

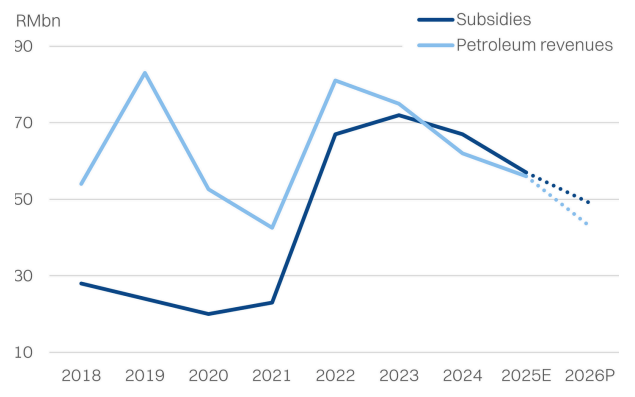

Subsidy cuts and lower petroleum dependence

Sectors in focus

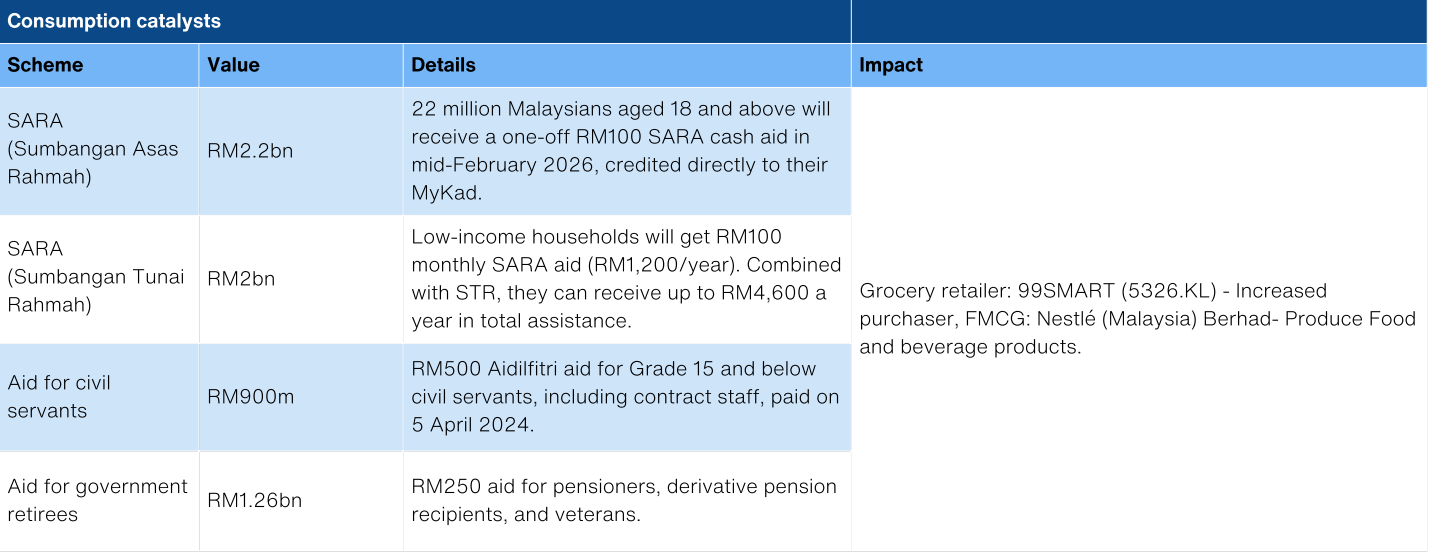

- Consumption stimulus: The biggest surprise is the repeat RM100 SARA handout that will benefit 22million Malaysians in Feb 2026. The relevant consumer stocks that have the most direct upside include 99SpeedMart and Nestle. Other consumption catalysts could include the proposed trade-in scheme for cars over 20 years old that could spur some demand for local marques, benefitting SIME (via Perodua) and DRB-Hicom (via Proton).

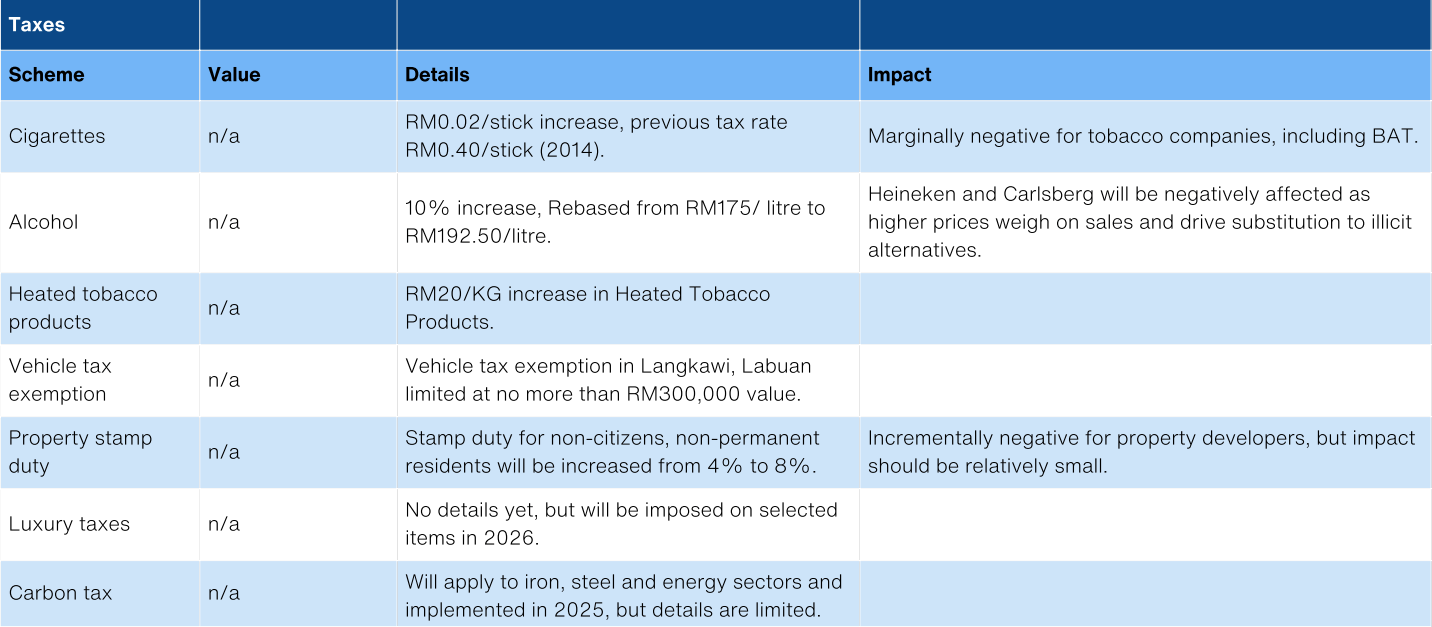

- Sin and luxury taxes: Corporates can breathe a sigh of relief, as there were no major tax hikes this year. The focus for revenue enhancement this year is skewed to plugging leakages, in part supported by e-invoicing. A carbon tax was mentioned but without any details. However, avoiding the gaze of the tax man for many years, tobacco and alcohol have now been hit with higher excise duties. Price impact should be roughly 5% for cigarettes and 10-20% for alcohol. The government also indicated luxury taxes will be implemented in 2026 but did not disclose details.

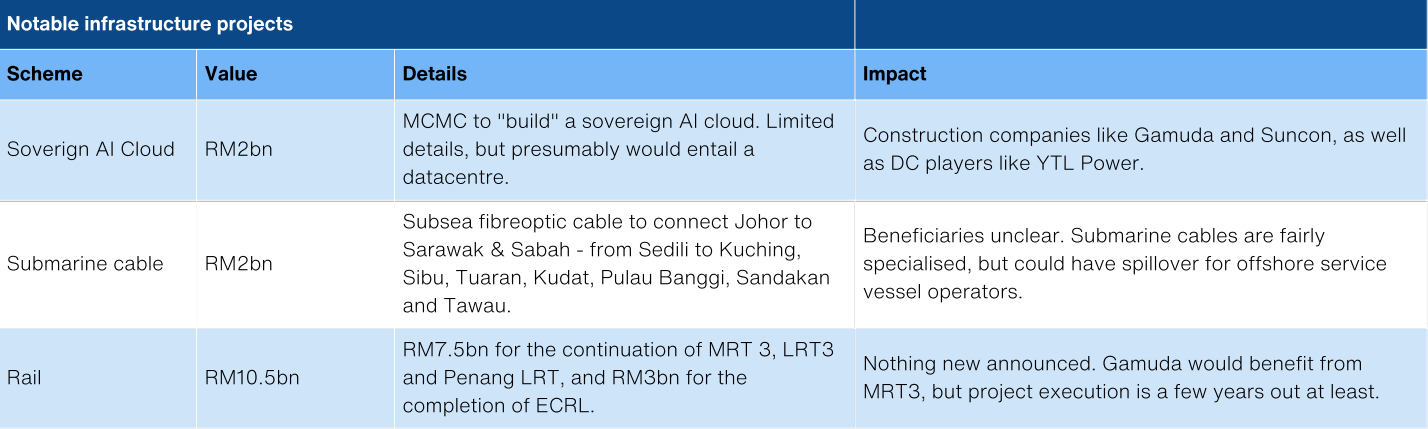

- Infrastructure: The government announced that MCMC will be investing RM2bn to build a Sovereign Cloud AI. Details are scant at this juncture, but this could be a catalyst for construction stocks like Gamuda and Suncon, as well as datacenter players like YTL Power. Additionally, the government also announced an RM2bn undersea submarine cable to connect Johor with Sabah and Sarawak (3,190km). Otherwise, the government is following through on existing rail transportation contracts - LRT3, Penang LRT, ECRL - with a total spend of RM10.5bn for FY26.

- Visit Malaysia 2026: The government also announced a broad package of stimulus to catalyze a targeted 47 million arrivals and RM165bn in receipts. In addition, there will be tax deductions to encourage more domestic tourism as well. The likely beneficiaries will be Genting Malaysia as well as AirAsiaX.

Weaning subsidies without losing votes

- Considering fiscal limitations, we are overall positive on Budget 2026, even if market impact might be low. Fiscal reform is gaining credibility, but populist tendencies remain entrenched based on the surprise handout.

Key budget impact sectors

Source: MOF, NPS Research, October 2025

Subsidy rationalization

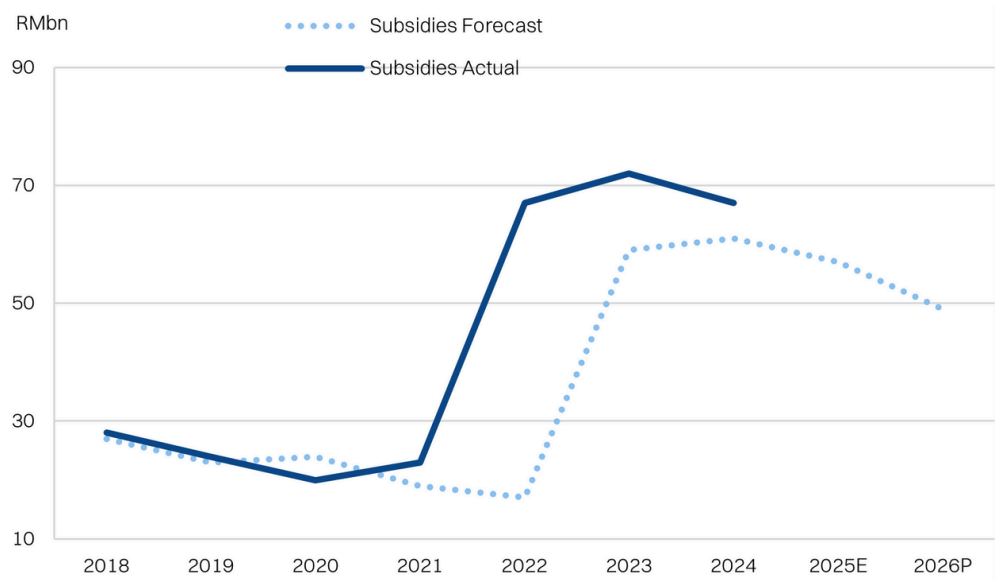

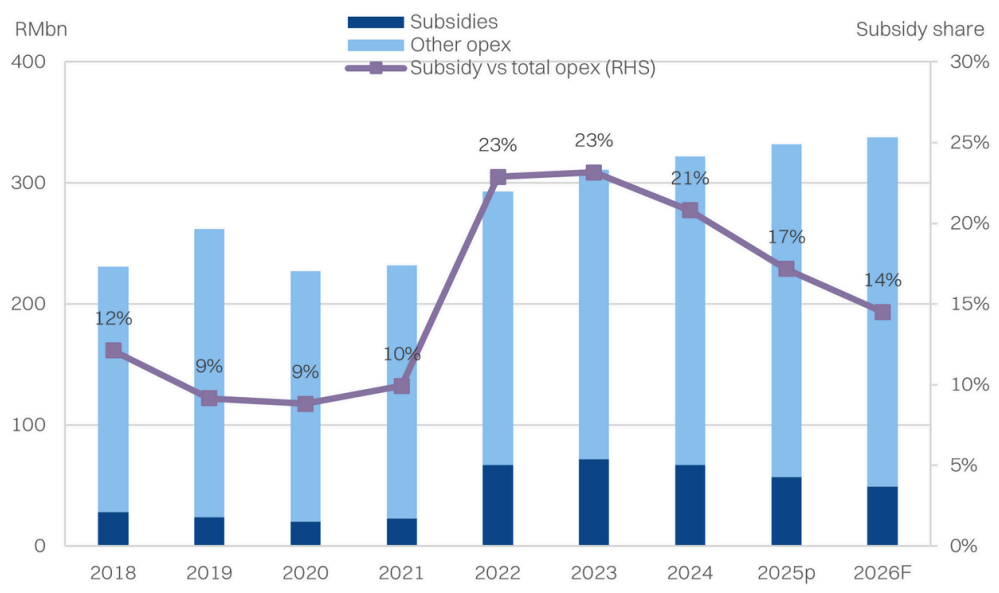

Subsidies have run above projections in previous years

Subsidy share of OPEX is easing towards 14%

Long-term fiscal trends

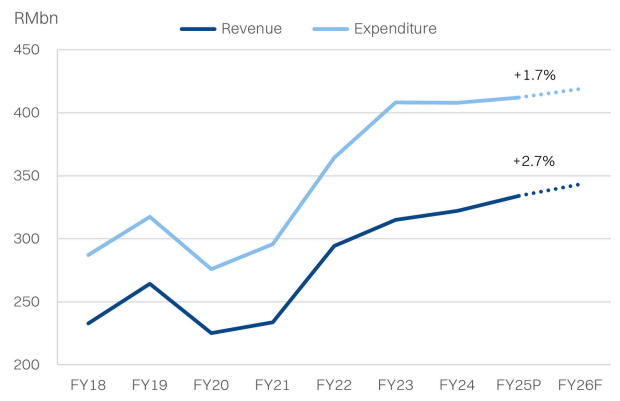

Over the past two years, the government has managed to reign in overall fiscal spend. This has been a function of cuts to development expenditure growth (-13.5%/-4.4% for FY24/FY25), as well as the fuel subsidy reforms (for diesel) in the past year.

Meanwhile, revenue is now back on an upward trend, driven by indirect taxes (+11.3%for FY25E), which has been the result of a broadening and deepening of SST. Looking ahead, it looks like the government intends to lean on more direct taxes to prop up revenue growth.

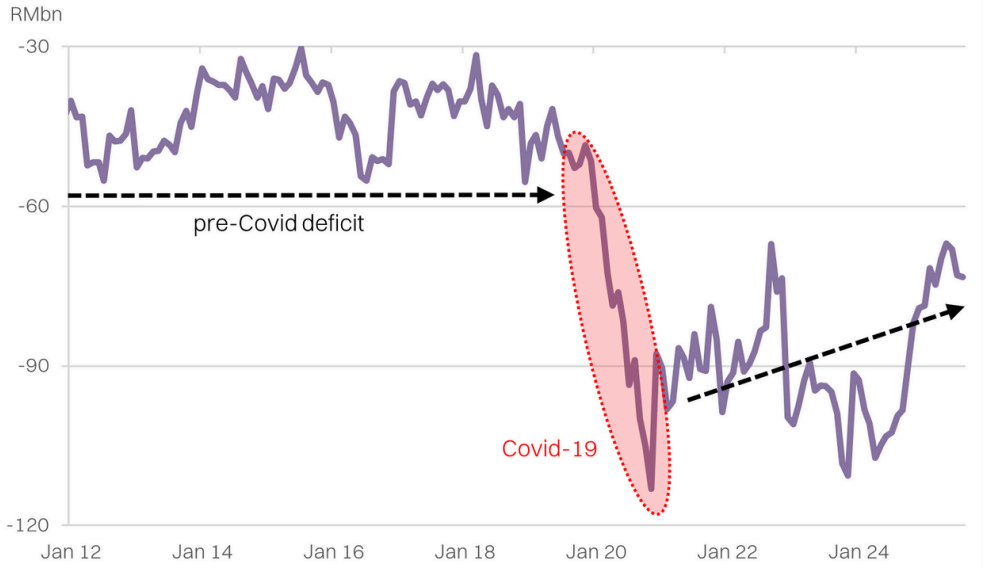

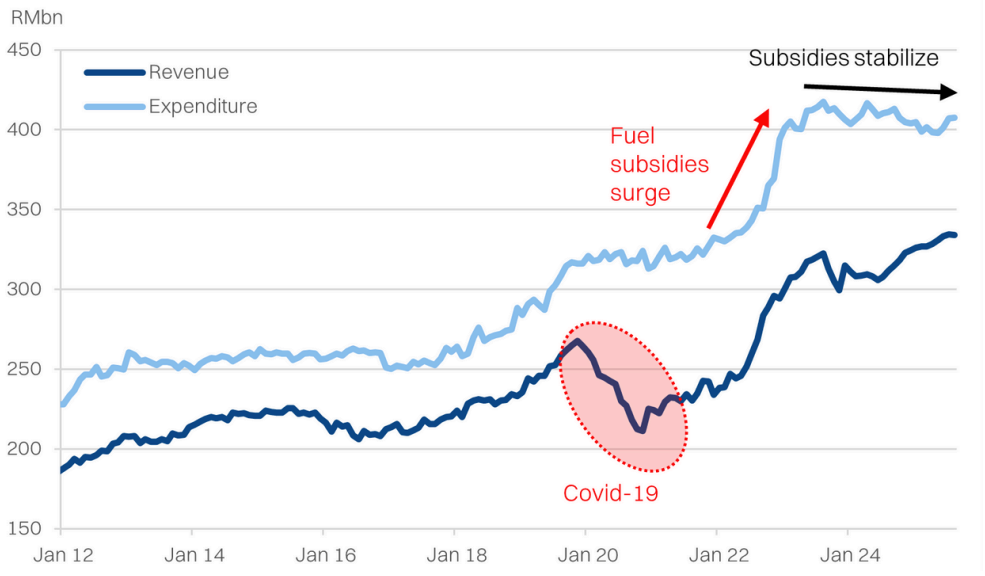

T12M fiscal revenue & expenditure -

In absolute terms, the Federal Government maintained a relatively disciplined fiscal balance pre-Covid with a deficit of around RM40-RM50bn. Following the pandemic however, the deficit has remained elevated at around RM90bn, exacerbated by the aforementioned surge in fuel subsidies. The deficit could have been narrowed further, but the government has trimmed its reliance on dividend income (particularly from Petronas) in the past few years. The deficit will need to narrow further by about RM20bn or so, for the fiscal balance to return to its pre-pandemic run-rate.

T12M fiscal balance - on a consolidation pathway