Improving collections, a dividend likely

Improving cash flows were a key signpost to continue rehabilitating market perception of Destini, on the back of a 4th quarter in the black.

Stock information

Destini Berhad

DESTINI - 7212.KL

BUY

Target price: RM0.65

Last price: RM0.47

Market cap: RM258m

Shares out: 549m

52w range: RM0.20 / RM0.51

3M ADV: RM0.5m

T12M returns: 77%

Disclaimer: By using this information, you hereby acknowledge that you are fully and solely responsible for evaluating the merits and risks of any investment decision and agree not to hold NewParadigm Research fully liable whatsoever for any actions, omissions and/or damages of any kind or matter arising from such decision.

Key points:

- Management held a well-attended post-results briefing, on the back of the full-year profits.

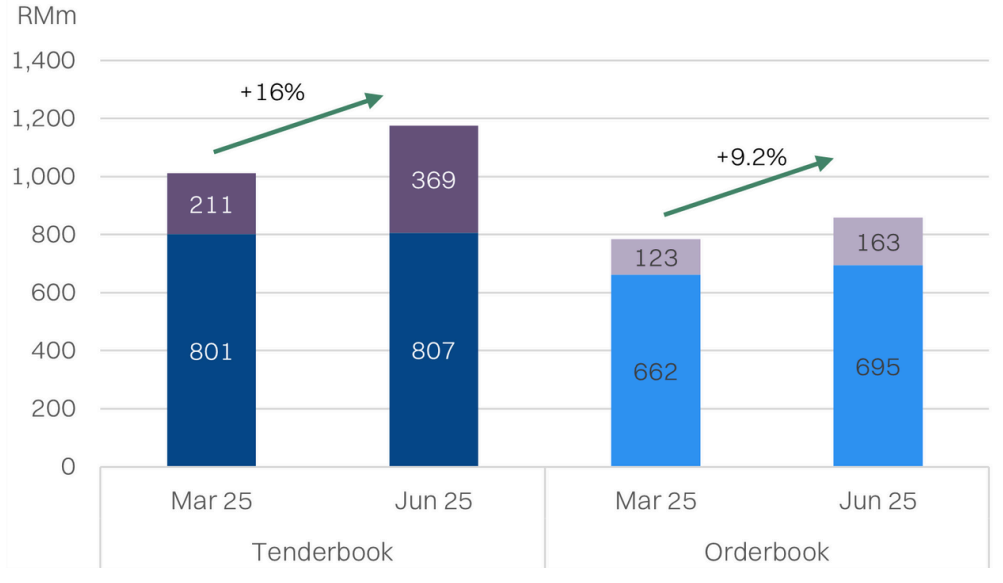

- Tenderbook funnel improves +16% to RM1.2bn; orderbook +9% to RM858m.

- Better collections, especially from MoT is easing working capital pressure. Board to mull a small dividend; positive for optics.

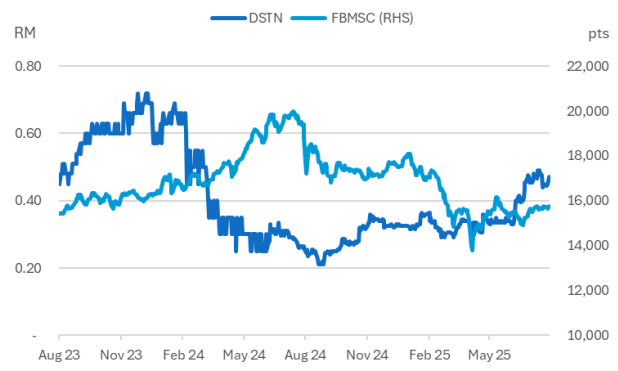

Share price performance

Investment fundamentals

| RMm | FY25A | FY26A | FY27A | FY28A |

|---|---|---|---|---|

| Revenue | 340.5 | 454.7 | 500.1 | 508.9 |

| Revenue growth | 114% | 34% | 10% | 2% |

| EBITDA | 50.7 | 67.4 | 78 | 78.4 |

| EBITDA margin | 15% | 15% | 16% | 15% |

| PATAMI | 28.2 | 40.7 | 49.9 | 49.9 |

| PATAMI margin | 8% | 9% | 10% | 10% |

| ROA | 7% | 7% | 8& | 7% |

| ROE | 17% | 19% | 19% | 16% |

| PER | 8.0 | 6.1 | 5.0 | 4.9 |

| P/BV | 1.5 | 1.1 | 0.9 | 0.8 |

| Yield | 0% | 0% | 5% | 6% |

Source: Company data, NewParadigm Research, August 2025

New orderbook wins remain key catalyst

Getting paid for the bird in hand

- Improving cash flows were a key signpost to continue rehabilitating market perception of Destini, on the back of a 4th quarter in the black. Payable days from MOT have improved from 150 days to 48 days, guides management, and should remain around this level going forward. This is a critical paymaster, since the level 4 MRO contracts make up 61% of Destini’s remaining orderbook.

- Another step to improving optics, would be paying a dividend - the first in roughly 15 years. Management indicated that a dividend, albeit a small one, would be put forward for board approval by late-October.

- Still, some balances due on the aviation and defense front remain a little slow, pending payment from the government. See Page 3 for our results recap.

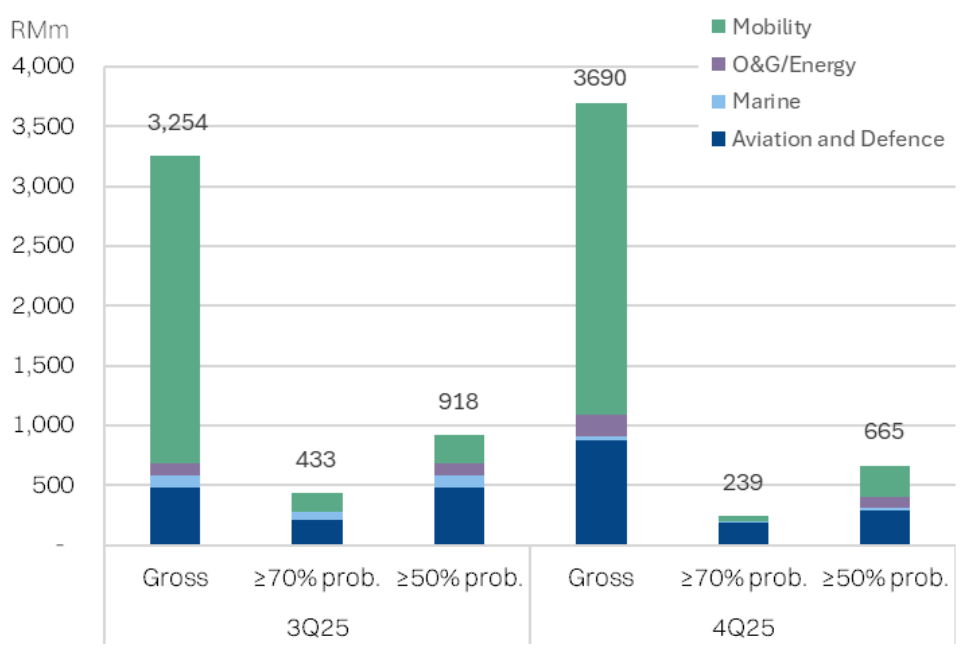

Birds in the bush - RM5bn leasing opportunity

- The key catalyst for Destini remains new contract wins. Since our initiation, Destini has secured a level 3 RM71m MRO contract for KTM trains as well as (we estimate) an RM25m contract for MRT HVAC and brake caliper overhauls, catalyzing a rally in the share price to a high of 50sen last month.

- Management indicated that the headline tenderbook has improved to RM1.2bn, but it appears to be driven by high-value, low-probability leasing contracts. We anticipate said leasing contracts will only see meaningful progress in 2026, but remains a key long-shot catalyst for Destini - we estimate the refurbishment and leaseback could be worth RM4-5bn for 18 train sets over 25 years.

- In the next 12 months however, we estimate a realistic orderbook (>50% chance of winning) to be RM665m.

The turnaround is rail, maintain buy

- We reiterate our BUY recommendation with an unchanged target price of 65 sen with no change to earnings. Destini is positioned as a potential beneficiary of the government’s move rail procurement off-balance sheet to leasing.

- Destini is trading at only 6.1x FY26 PER, cheap considering the orderbook in hand covers earnings for the next two years.

About the company

Destini Bhd offers engineering services in mobility (mostly rail), aviation and defence (primarily for the military), marine (for O&G) and energy (predominantly solar. The bulk of Destini’s operations are based in Malaysia, but it has a small footprint in Singapore, China. Australia and UAE. The bulk of Destini’s orderbook today relates to the maintenance, repair and overhaul (MRO) of KTMB rolling stock.

About the Stock

Destini Bhd’s controlling shareholder is Datuk Aziz with a 11.6% stake. The stock otherwise is mostly held by retailers with almost no institutional participation. This reflects the perceived political risk associated with the companies operations. Destini has seen two major corporate exercises in 2024 – a 2 for 1 rights issuance as well as a 1 for 10 stock split.

Investment thesis

Destini is a turnaround story, that is still building credibility. As the profitability track-record continues and the group continues to build its orderbook, the market should reward the company with a smaller discount on valuations. Critically, the stock has virtually no institutional ownership, for now. Destini’s profits for the next 2-3 years are underpinned by its Level 4 MRO contract with KTMB (RM695m), and new contract wins are supported by a sizable RM3.2bn bid book funnel.

Key risks

Political risk – Destini primarily contracts with the government or government linked entities. Changes to the political establishment can be disruptive to contract flows and payments, as seen in 2018.

Cash flow risk – Despite turning profitable, Destini’s bloating receivables has translated persisting cash flow drag and remains reliant on debt.

Cyclical risk – Destini has enjoyed lumpy level 4 MRO contracts, but such overhaul/refurbishment cycles are irregular and infrequent – likely more so as RAC moves towards a leasing model.

Orderbook outlook

- While headline tenderbook wins are rising, we note that the high and fair probability jobs have narrowed after the recent conversion to wins. Still, it remains a very healthy funnel on a 12-month outlook, with low concentration risk as the tenderbook is spread over 60 bids.

- Still, the big catalyst that the market will be looking for should be the leasing contracts - similar to what SMH rail secured earlier this year (link). However, we see this only likely to make progress in 2026. Destini is likely to bid for this contract via Railtec - which is a JV with KTM Bhd.

- In the meantime, Destini is focused on qualifying more EEM (equivalent equipment manufacturer) status for its supplies - especially local ones. This will give Destini an advantage in future bids as it will be able to lower the cost and reduce lead time. The acquisition of Trovon has been a key enabler of this and is bearing fruit with the recent MRT brake caliper contract win, according to management.

Tenderbook breakdown

Destini orderbook and tenderbook outlook

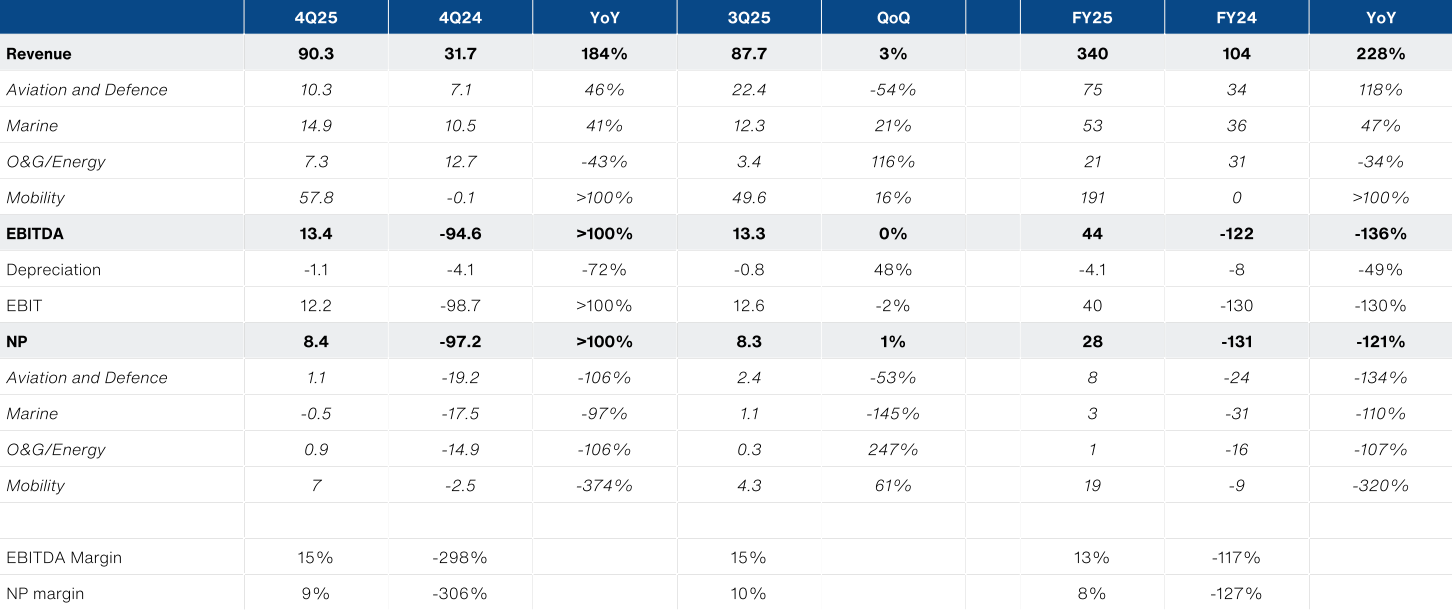

4Q25 results: Sustained trajectory

4Q25 (ended-June) net profit of RM8.4m (+8.3% QoQ) took full year net profits to RM28m. While this trailed our forecast of RM30m, the positive trajectory of operations – particularly for mobility – remains within our expectations. It also marks Destini’s 4th consecutive profitable quarter, following the kitchen sinking in FY24.

Revenue of RM90.3m (+3% QoQ) matched our forecasts, at RM340m. However, a

surge in admin costs (+28% QoQ) to RM19.9m trimmed the EBITDA performance to flat QoQ. The higher costs were pinned on the acquisition of Australia-based Trovon Group, but should be mitigated progressively as Destini restructures some cost centers over to Malaysia.

Mobility segment contributions for the quarter are up +16% QoQ to RM57.8m, taking the full year to RM191m – potential to accelerate further as additional VO’s come in FY26, driving up revenue per train.

Critically, we were happy to see working capital pressure stabilize with a QoQ improved collection of RM13m across receivables and contract assets – helping improve operating cash flows.

Note that the RM17m from the private placement in May was also captured in 4Q25.

Results snapshot