Exceptional Underlying Growth

We conclude from the post-results briefing that the combination of seasonal tailwinds, a step-up in leading-edge product mix, and sustainable margin dynamics, that the current momentum should be sustained.

Stock information

FRONTKEN

FRONTKEN - 0128.KL

BUY

Target price: RM4.80

Last price: RM4.35

Market cap: RM6,894m

Shares out: 1,585m

52w range: RM2.63 / RM4.59

3M ADV: RM13m

T12M returns: -5%

Disclaimer: By using this information, you hereby acknowledge that you are fully and solely responsible for evaluating the merits and risks of any investment decision and agree not to hold NewParadigm Research fully liable whatsoever for any actions, omissions and/or damages of any kind or matter arising from such decision.

Key points

- Underlying revenue and PATAMI rose $+21\%/+70\%$ YoY, adjusting for one-offs and forex translation. Beat vs ours/street expectations.

- Strong margin expansion on better product mix, higher volumes, and better operating leverage.

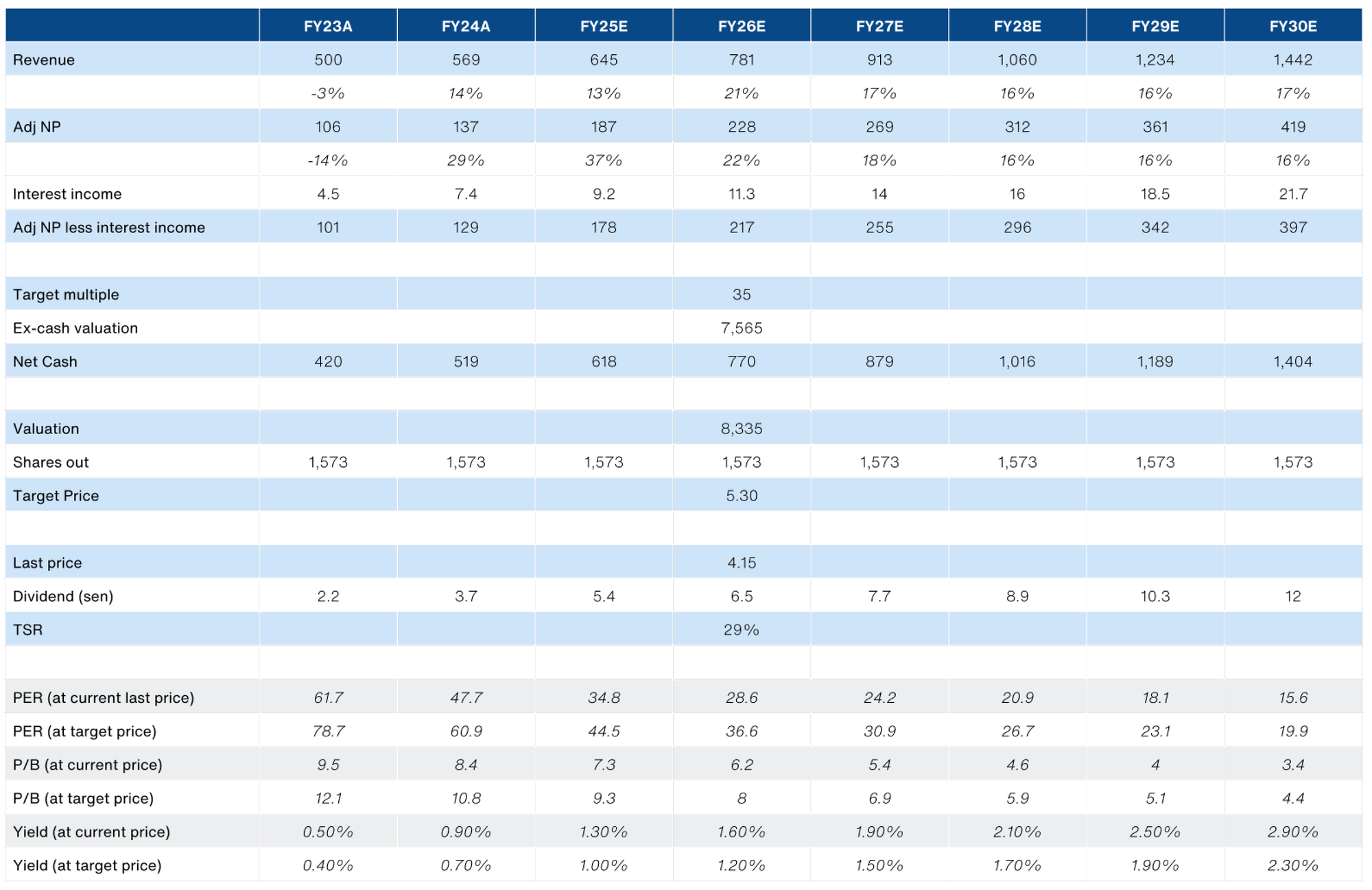

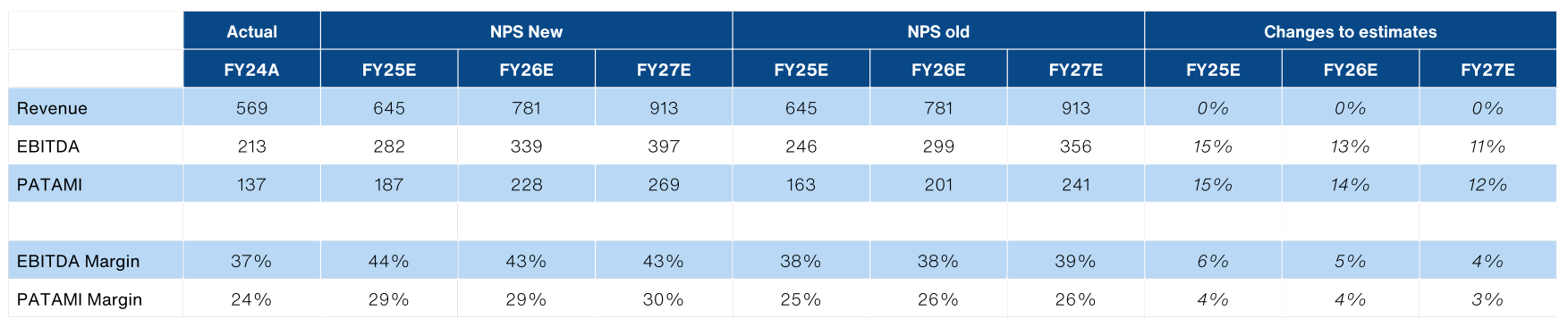

- Upgrade our FY25-27E PATAMI forecasts by $+15\%/+14\%/+12\%$ on higher margin assumptions. Upgrade TP to RM5.30 (from RM4.80).

Investment fundamentals

| RMm | FY24A | FY25E | FY26E | FY27E |

|---|---|---|---|---|

| Revenue | 569.2 | 644.9 | 780.5 | 913.1 |

| Revenue growth | 14% | 13% | 21% | 17% |

| EBITDA | 212.5 | 281.7 | 338.8 | 396.7 |

| EBITDA margin | 37% | 44% | 43% | 43% |

| PATAMI | 136.8 | 187.5 | 228 | 269.4 |

| PATAMI margin | 24% | 29% | 29% | 30% |

| ROA | 14% | 17% | 17% | 18% |

| ROE | 18% | 21% | 22% | 22% |

| PER | 47.7 | 34.8 | 28.6 | 24.2 |

| P/BV | 8.4 | 7.3 | 6.2 | 5.4 |

| Yield | 1% | 1% | 2% | 2% |

Source: Bloomberg, NewParadigm Research, 2025

Margin expansion drove the beat

- Frontken beat ours/street's expectations, with a healthy +9ppt expansion in net margins.

- 2Q25 Adj NP (Adjusted Net Profit) surged +62% YoY (+61% QoQ) to RM53m on the back of revenue growth of +16% YoY (+18% QoQ) to RM156m. This brings 1H25 Adj NP to RM85.7m (+32% YoY) which is 53%/51% of ours/consensus full-year expectations.

- Critically, we conclude from the post-results briefing that the combination of seasonal tailwinds, a step-up in leading-edge product mix, and sustainable margin dynamics, that the current momentum should be sustained.

- Interim dividend of 2sen/share is in-line with our expectations.

- Separately, management indicated that it had managed to acquire an additional 0.9% additional stake acquired in AGTC (the key Taiwanese subsidiary), bringing total shareholding to 93.4%. The acquisition was done at high-single digit PER multiples.

- Looking ahead, management indicated qualification for the Singapore fab remains on-track for 3Q25. Discussions with potential partners in the US to support the key customer in Arizona, are ongoing with multiple options being explored. Finally, expansion of the third plant in Taiwan is likely to be completed by early 2027.

Results beat expectations

| 1H25A | NPS forecast | vs NPS | Consensus forecasts | vs consensus | |

|---|---|---|---|---|---|

| Revenue | 289 | 645 | 45 | 690 | 42% |

| Adj EBITDA | 123 | 246 | 50% | 253 | 49% |

| Adj PATAMI | 86 | 163 | 53% | 169 | 51% |

Source: Bloomberg, NewParadigm Research, 2025

Upgrade TP to RM5.30

- We raise our earnings assumptions by +15-12% for FY25-27E, on high margin assumptions. There is headroom to upgrade topline growth as well, going forward.

- We upgrade our target price to RM5.30 on a slightly lower target multiple of 35x FY26 PER. Maintain BUY.

About the company

Providing precision cleaning services to leading-edge foundries in Taiwan, where it derives almost 70% of revenues and over 80% of operating profits. It is a relatively high margin business. FRCB’s key customers includes TSMC, and both stocks have historically enjoyed a reliable correlation in earnings. FRCB also runs a non-core O&G business which includes maintenance, repair and overhaul of industrial equipment. FRCB boasts a strong track-record in retaining market share with its customer as well as securing qualification for new nodes.

About the stock

Frontken is among the top 3 largest companies by market cap within the

semiconductor sector in Malaysia. It is seen as the best proxy to front-end

semiconductors (fabs), as most of its peers are back-end packaging OSAT’s

and/or equipment makers (capital goods) for the sector. The stock is well institutionalized with EPF holding almost 10% of the stock. On the other side of the coin, the stock is tightly held by institutions and is relatively illiquid. In turn, Frontken trades on premium valuations of >30x PER - even higher than TSMC's high teens PER.

Investment thesis

Frontken is the best domestic exposure to semiconductor front-end in Malaysia. It boasts more stable and persistent secular drivers, due to its leverage to leading edge processes and customer stickiness. It is also more defensive through the cycle compared with OSAT peers and not exposed to dollar weakness. Frontken's premium valuations is also further justified by the option to match TSMC's capacity expansion into new regions as well as potential to montize intellectual property.

Key risks

- High customer concentration risk. While the probability is very low, any

operational mistakes/lapses that result in the loss of confidence by the

customer poses steep financial risk to FRCB. - High expectations for earnings delivery - having been consistently profitable since 2016. We anticipate there could be strong negative share price reaction if there is a significant miss to earnings and/or steep downgrade in guidance.

- Geopolitical risk: Frontken is highly exposed to the broader Taiwanese front-end semiconductor ecosystem. Any structural shocks to the industry would pose significant downside risk to both profitability and valuations.

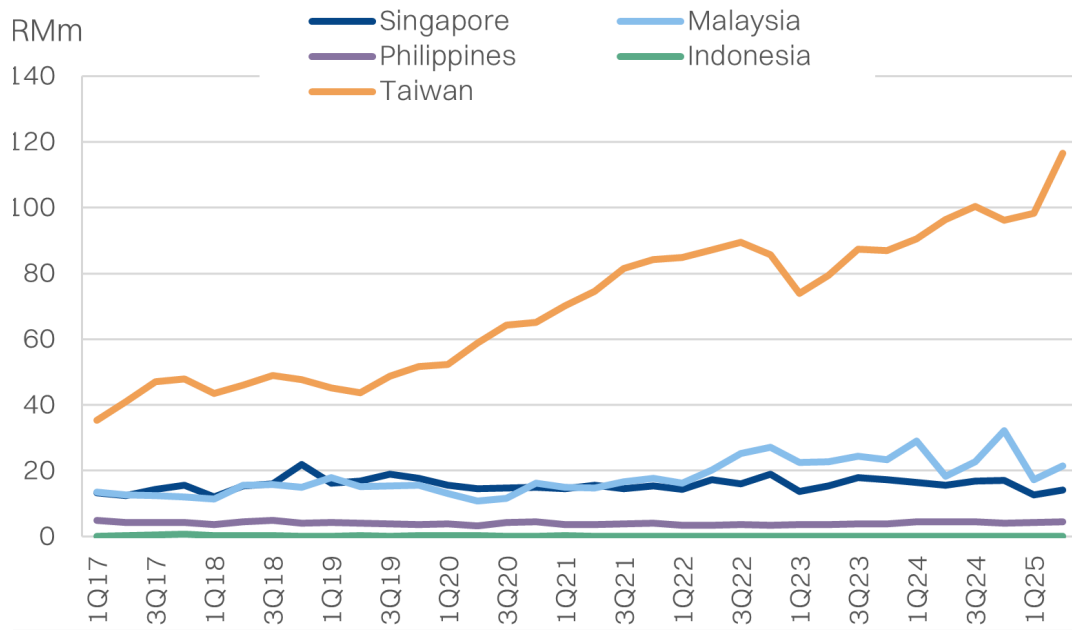

Revenue by segment

Underlying growth of +70% YoY

- Frontken’s underlying revenue and PATAMI growth was +21% and +70% YoY respectively for 2Q25, if the one-off forex losses as well as the forex translation impact of the stronger ringgit was stripped.

- The one-off forex losses of RM19.4m (RM19m unrealized) was due to the group converting a large sum of cash to US dollars in 2Q25, to attempt an acquisition in the US. However, the transaction fell through and the depreciation of the dollar during that period led to the losses. Some of the losses have been crystalized, but it is likely to result in some gains in 3Q25 due to the subsequent rebound in the dollar.

- The stronger performance was driven by the semiconductor segment in Taiwan, with management pointing to higher loadings from customers, especially for 2nm.

- The big surprise for the market was the 9ppt increase in net margins YoY, that drove net profits to a new record high of RM52.9m (adjusted) or +61% YoY.

Without the TWD-MYR deterioration in this period, the underlying momentum would have been even stronger at +70% YoY. - From the call with management, we distill that this new level of margins is likely sustainable, as long as the current mix from customers remains - i.e. a continued loading of leading-edge processes.

- On a separate note, Frontken has declared an interim dividend of 2sen per share, which is in-line with our expectation

2Q25 earnings snapshot

| 2Q25 | 1Q25 | QoQ | 2Q24 | YoY | 1H25 | 1H24 | YoY | |

|---|---|---|---|---|---|---|---|---|

| Revenue | 156.4 | 132.6 | 18% | 134. 9 | 16% | 289 | 275.4 | 5% |

| EBITDA | 50.4 | 51.6 | -2% | 50 | 1% | 102 | 104.2 | -2% |

| Adj EBITDA | 69.8 | 53.4 | 31% | 49.3 | 42% | 123.2 | 105.8 | 16% |

| PBT | 36.5 | 34.1 | 7% | 36.5 | 0% | 70.7 | 69.9 | 1% |

| PATAMI | 33.5 | 31.1 | 8% | 33.3 | 0% | 64.6 | 63.4 | 2% |

| Adj PATAMI | 52.9 | 32.8 | 61% | 32.6 | 62% | 85.7 | 65 | 32% |

Source: Company data, NewParadigm Research, August 2025

Core earnings

Upgrade earnings, upgrade target price

We upgrade our margin assumptions, raising our EBITDA margins to 44% (from 38%) for FY25, with a slight decline going forward. This is below the 45% level achieved in 2Q25. Furthermore, our net margin is upgraded to 29% (from 25%) but remains below the 34% achieved in 2Q25.

We raise our TP to RM5.30 (from RM4.80) on the back of the higher earnings but trim our target multiple to 35x (from 36x).

Changes to earnings

Valuations: Upgrade TP to RM5.30