2Q25 - Dividend upgrade

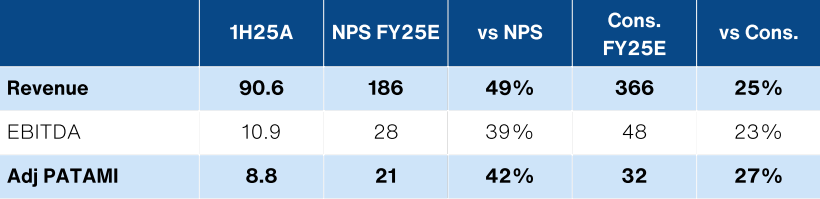

KJTS’ earnings continued to accelerate in the second quarter, bringing 2H25 Adj NP to RM8.8m (+23% YoY).

Stock information

KJTS

KJTS - 0293.KL

TRADING BUY

Target price: RM2.00

Last price: RM1.67

Market cap (RMm): RM1,150m

Shares out: 689m

52-week range: RM0.62 / RM1.76

3M ADV: RM1.8m

T12M returns: 149%

Disclaimer: By using this information, you hereby acknowledge that you are fully and solely responsible for evaluating the merits and risks of any investment decision and agree not to hold NewParadigm Research fully liable whatsoever for any actions, omissions and/or damages of any kind or matter arising from such decision.

Key takeaways:

- Net profits rose +8% QoQ and +23% YoY to RM4.6m, in line with our expectations.

- Dividend of 0.406 sen per share (62% payout) was up +77% from FY24.

- Maintain Trading Buy with target price of RM2.00. We foresee newsflow as the catalyst for the share price going forward.

Share price performance

Investment fundamentals

| RMm | FY24A | FY25E | FY26E | FY27E |

|---|---|---|---|---|

| Revenue | 138 | 186 | 222 | 280 |

| Revenue Growth | 15% | 35% | 20% | 26% |

| EBITDA | 12.2 | 27.9 | 35.3 | 44 |

| EBITDA margin | 9% | 15% | 16% | 16% |

| PATAMI | 8.1 | 21.2 | 29.6 | 41.9 |

| PATAMI margin | 11% | 11% | 13% | 15% |

| ROA | 10% | 12% | 13% | 15% |

| ROE | 13% | 16% | 19% | 23% |

| PER | 70 | 51.1 | 36.6 | 25.8 |

| P/BV | 9.3 | 8.2 | 7.1 | 5.9 |

| Yield | 0% | 1% | 1% | 2% |

Source: Company data, NewParadigm Research, August 2025

Margins offset cooling revenue

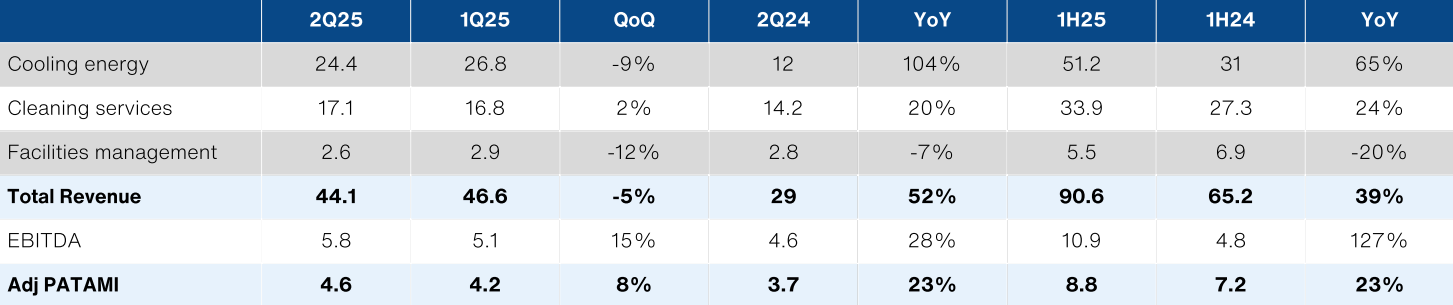

- KJTS’ earnings continued to accelerate in the second quarter, bringing 2H25 Adj NP to RM8.8m (+23% YoY). This was 42%/27% of ours/consensus full-year expectations. We deem this to be in-line as we expect the contribution from the Malakoff Utilities Sdn Bhd (MUSB) acquisition to kick in in 2H25.

- Revenue did cool off sequentially to RM44.1m (-5% QoQ), but on balance was still up +39% YoY to RM90.6m. Revenue for cooling energy dipped -9% QoQ, while facilities management fell -12% QoQ. This was offset by better cleaning services +2% QoQ.

- Nonetheless, margins improvement helped offset the weakness with EBITDA margins up to 13.3% for the quarter from 11% in 1Q25.

- We note that margins were supported by a 300% QoQ jump in other income to RM2.1m, as well as a moderation of admin expenses -9% QoQ to RM7m.

Earnings vs expectations

Maintain trading buy

- Management will be hosting the post-results briefing at 3pm, 28 August.

- Pending additional updates, we maintain our earnings expectations with unchanged target price of RM2.00 and a Trading Buy.

Earnings summary