Cooling is Heating Up

While valuations may appear stretched at first glance, we flag that the nature of KJTS’ business means the earnings delivery on a new project is not front-loaded.

Stock information

KJTS

KJTS - 0293.KL

TRADING BUY

Target price: RM2.00

Last price: RM1.57

Market cap (RMm): RM1,081m

Shares out: 689m

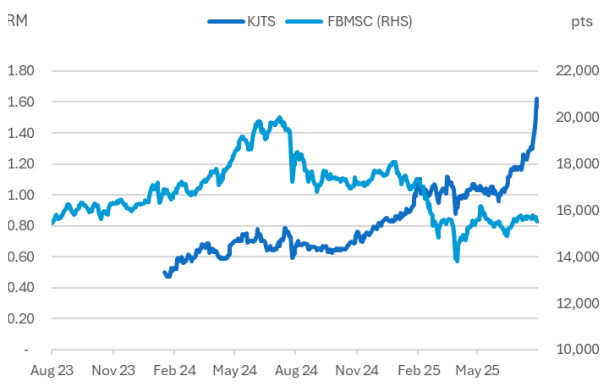

52-week range: RM0.62 / RM1.65

3M ADV: RM1.5m

T12M returns: 156%

Disclaimer: By using this information, you hereby acknowledge that you are fully and solely responsible for evaluating the merits and risks of any investment decision and agree not to hold NewParadigm Research fully liable whatsoever for any actions, omissions and/or damages of any kind or matter arising from such decision.

The pitch:

- Unique cooling energy efficiency company, positioned to benefit as energy prices rise.

- Joint venture with Stonepeak is a pivot in its capital funding strategy that will turbocharge growth, off-balance sheet.

- Initiate with a TRADING BUY and a target price of RM2.00, implied FY27E PER of 33x.

Share price performance

Investment fundamentals

| RMm | FY24A | FY25E | FY26E | FY27E |

|---|---|---|---|---|

| Revenue | 138 | 186 | 222 | 280 |

| Revenue Growth | 15% | 35% | 20% | 26% |

| EBITDA | 12 | 28 | 35 | 44 |

| EBITDA margin | 9% | 15% | 16% | 16% |

| PATAMI | 15 | 21 | 30 | 42 |

| PATAMI margin | 11% | 11% | 13% | 15% |

| ROA | 10% | 12% | 13% | 15% |

| ROE | 13% | 16% | 19% | 23% |

| PER | 70 | 51 | 36 | 26 |

| P/BV | 9.2 | 8.2 | 7.0 | 5.9 |

| Yield | 0.0% | 1.0% | 1.0% | 2.0% |

Source: Company data, Bloomberg, NewParadigm Research, August 2025

Good business, better capital structure

- The cooling energy efficiency space is both sizable (est.RM40bn market) as well as thematically relevant - as a play on rising energy prices as well as the growing need for cooling in a warming world. KJTS’ business model benefits directly from higher electricity prices and should enjoy an uplift in 2H25 earnings on the back of TNB’s +13.6% tariff hike.

- Additionally, KJTS enjoys exposure to the AI datacenter thematic - as these facilities have substantial cooling requirements.

- The x-factor that will turbo-charge growth is KJTS’ tie-up with Stonepeak (an infrastructure investment firm with US$72bn in real assets) into a JV called Lestari Cooling Energy (LCE). Previously, KJTS’ growth would have been limited by its ability to recycle capital into new acquisitions/capex. The JV structure with Stonepeak (est. capitalization of RM1.5bn) allows the growth to be funded by its partners, off-balance sheet, while still allowing KJTS to capture income from the EPCC and O&M segments.

- Looking ahead, we anticipate the stock will be news flow-driven, as the success of the JV hinges on the group executing on acquiring the potential pipeline of ~20 assets. Another key catalyst for the stock would also be the inclusion of a potential domestic strategic investor for LCE that management is seeking to support potential funnel of cooling energy asset acquisitions.

A trading buy

- While share price has already done well this year, we see this as a trading buy with room to improve to outperform on the back of news flow. Valuations are not cheap, but this is a stock that can get more overvalued as it taps into strong thematics that will be sheltered from external shocks - a good combination of defensiveness and growth.

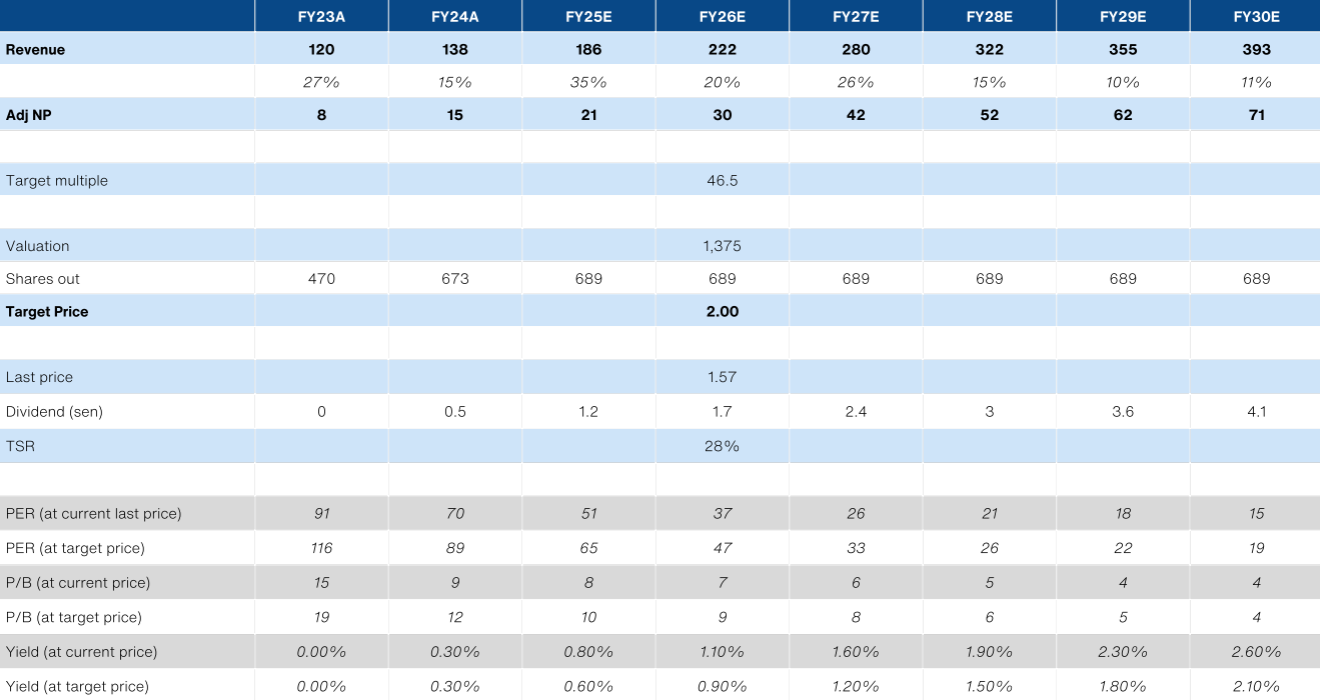

- Initiate with a Trading Buy and target price of RM2.00 on a FY26E PER of 46.5x. While steep, this is due to the deferred nature of earnings delivery. FY27/28E implied PER is 33x/26x at our target price. At the very least, this is a stock to accumulate on any pull-back from the recent highs.

- KJTS will report 2Q25 earnings on 27 August.

About the company

KJTS’ core business is providing cooling energy services via large-scale district cooling systems. The company bears the capex to upgrade existing cooling systems to improve energy efficiency, offering clients immediate savings with no capital outlay. KJTS books the EPCC revenues as well as enjoying the surplus energy savings and the facilities management over a long-term contract. In turn, KJTS’ secured business has direct leverage to energy prices and long-term growth is tied to securing new projects.

About the stock

KJTS is a Shariah compliant stock that was listed in 2024 in the ACE market. In our view, KJTS is misclassified as an industrial products and services company. It might be better to think of KJTS as a utility or energy stock.

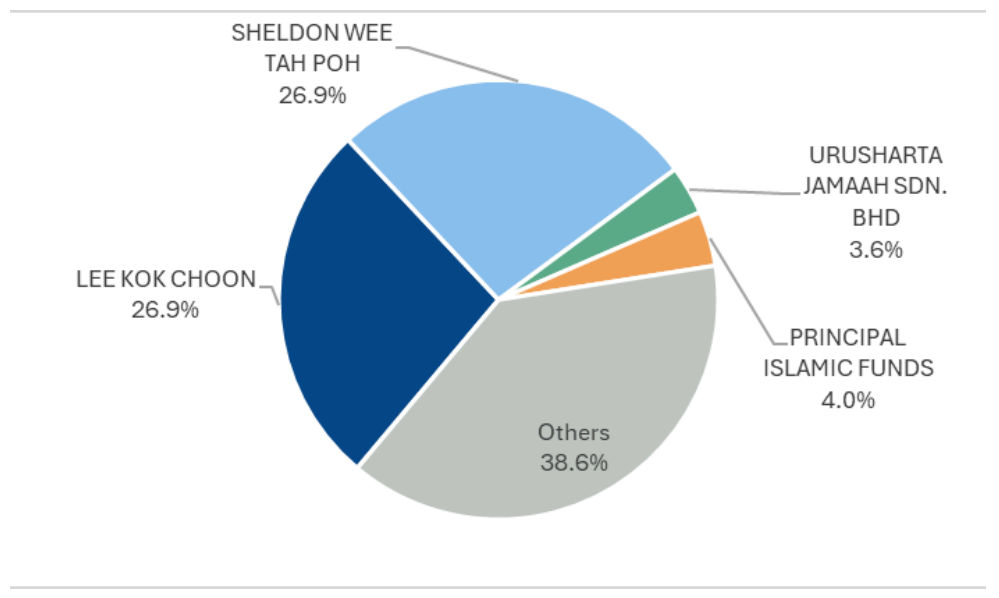

KJTS was originally the Asean arm of Dalkia Group, prior to a management buyout in 2014 by Lee Kok Choon and Sheldon Wee - both currently the key management and controlling shareholders (combined).

Investment thesis

KJTS offers a unique exposure to energy efficiency for large scale cooling

infrastructure, including datacenters. We see deep value in the group’s long-term growth potential, against a backdrop of global warming and energy price inflation. The recent kicker for the group is the change in its capital model - from purely self-funding to relying on strategic partners like Stonepeak to supply capital, without significant compromise on earnings accretion. At this juncture, we recommend KJTS as a Trading Buy.

Key risks

- Failure to secure new projects - will severely limit growth. Acquisitions could be lumpy and intermittent.

- Dependency on partners - the joint venture with Stonepeak is a lynchpin to our thesis. If the partner(s) choose to withdraw from the joint venture, it would hurt KJTS’ growth prospects.

- Execution risk - failure to meet expected energy efficiency targets could result in lower or even negative returns on a project.

Shareholding breakdown

Cool business, hot stock, Trading Buy

We initiate coverage on KJTS with Trading Buy and a target price of RM2.00, based on a FY26E target multiple of 46.5x PER. We foresee potential 26% further upside from current levels, on the back of news flow of new project wins as well as potential inclusion of strategic partners for its joint venture - Lestari Cooling Energy (LCE).

While valuations may appear stretched at first glance, we flag that the nature of KJTS’ business means the earnings delivery on a new project is not front-loaded. Furthermore, the group has yet to fully switch on the joint venture with Stonepeak that could see RM1.5bn of assets (acquisition + capex) injected into the JV over the next 3 years. In turn, forward multiples are substantially more reasonable at 33x/26x FY27/28E PER once earnings catch up.

Critically, we think KJTS strikes a good balance between quality defensive earnings and thematic driven growth, now turbo-charged with a new capital model.

- Quality defensive: The cooling energy contracts offer are long-term recurring cash flows and high customer stickiness. Contract structure also gives KJTS upside from energy price inflation.

- Thematic growth: Cooling infrastructure demand is likely to continue growing at a multiple above GDP growth - as global warming continues to pile on additional demand for cooling and for more importantly, efficient cooling. New secular drivers for cooling demand like datacenters further supplement the core demand coming from offices, malls, hospitals, among others.

- Capital efficiency: Prior to the JV with Stonepeak, KJTS’ growth would have been limited by its ability to raise and recycle capital. We see the venture as providing KJTS an expediated pathway to scale-up its earnings base. In turn, this should also pave the way for more investors to consider the stock. It is also a highly scalable approach that could be extended beyond Malaysia to KJTS’ other markets like Singapore and Thailand where the firm has a small toehold. KJTS could consider a transfer to the main board within the next 12 months.

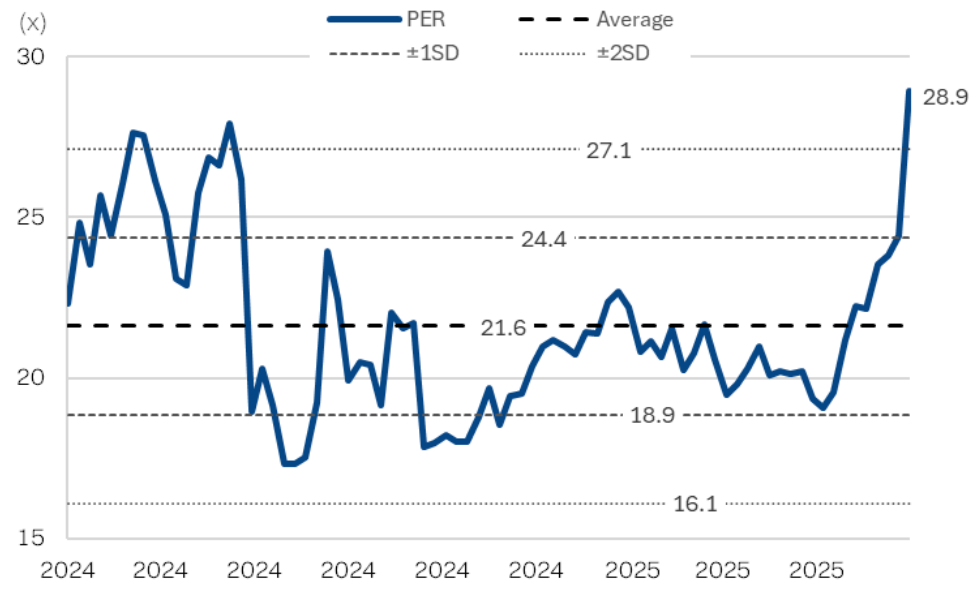

12M BF PER bands - KJTS breaking out

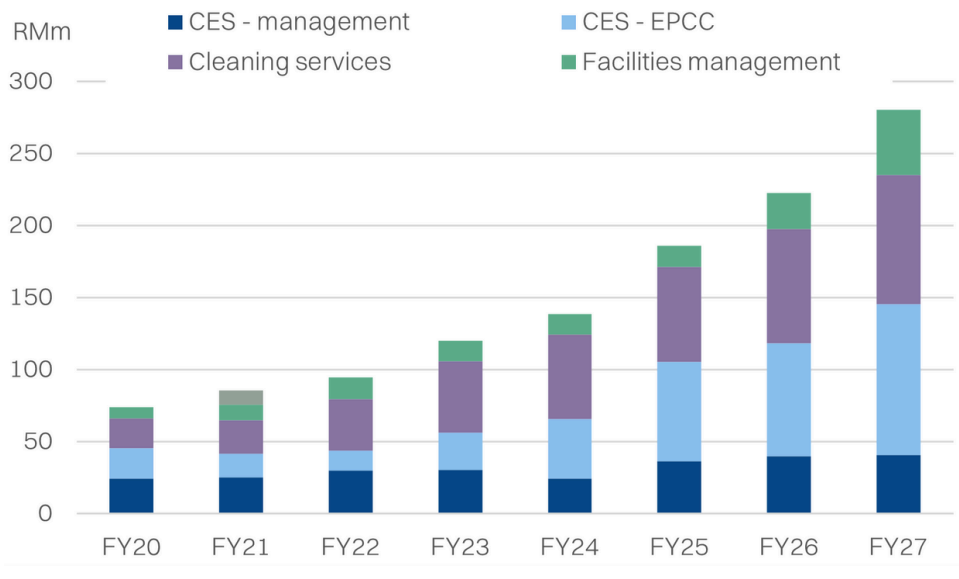

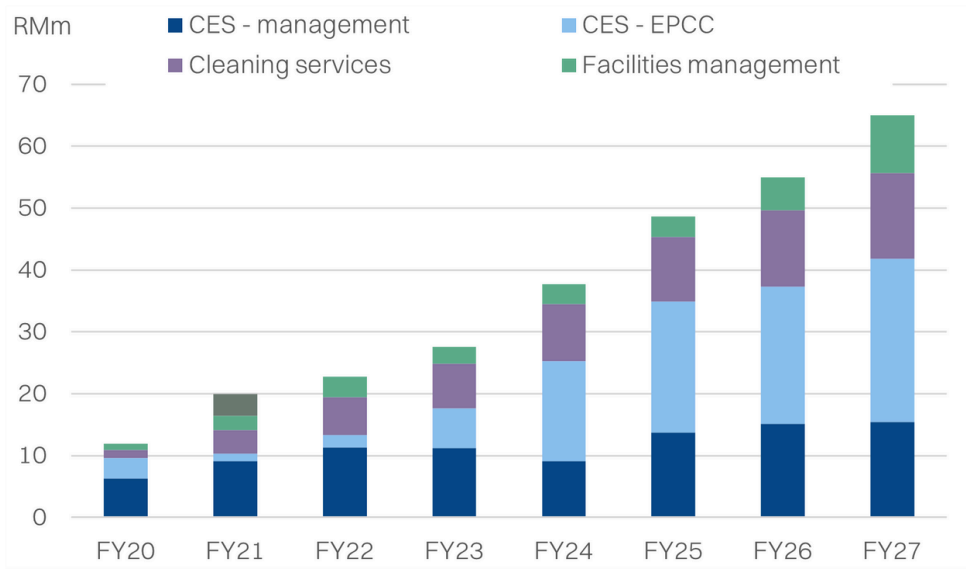

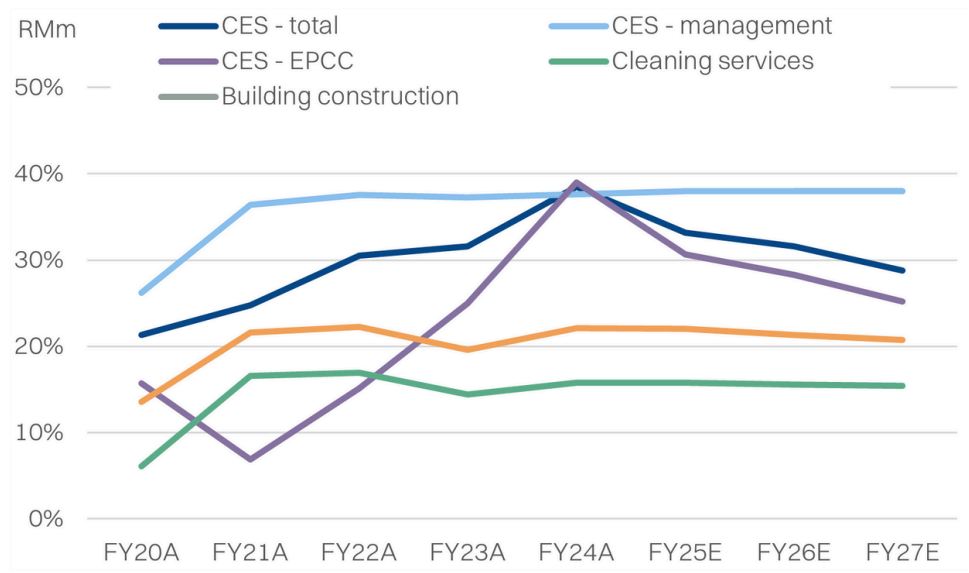

Segmental breakdown

Revenue breakdown

GP breakdown

GP breakdown

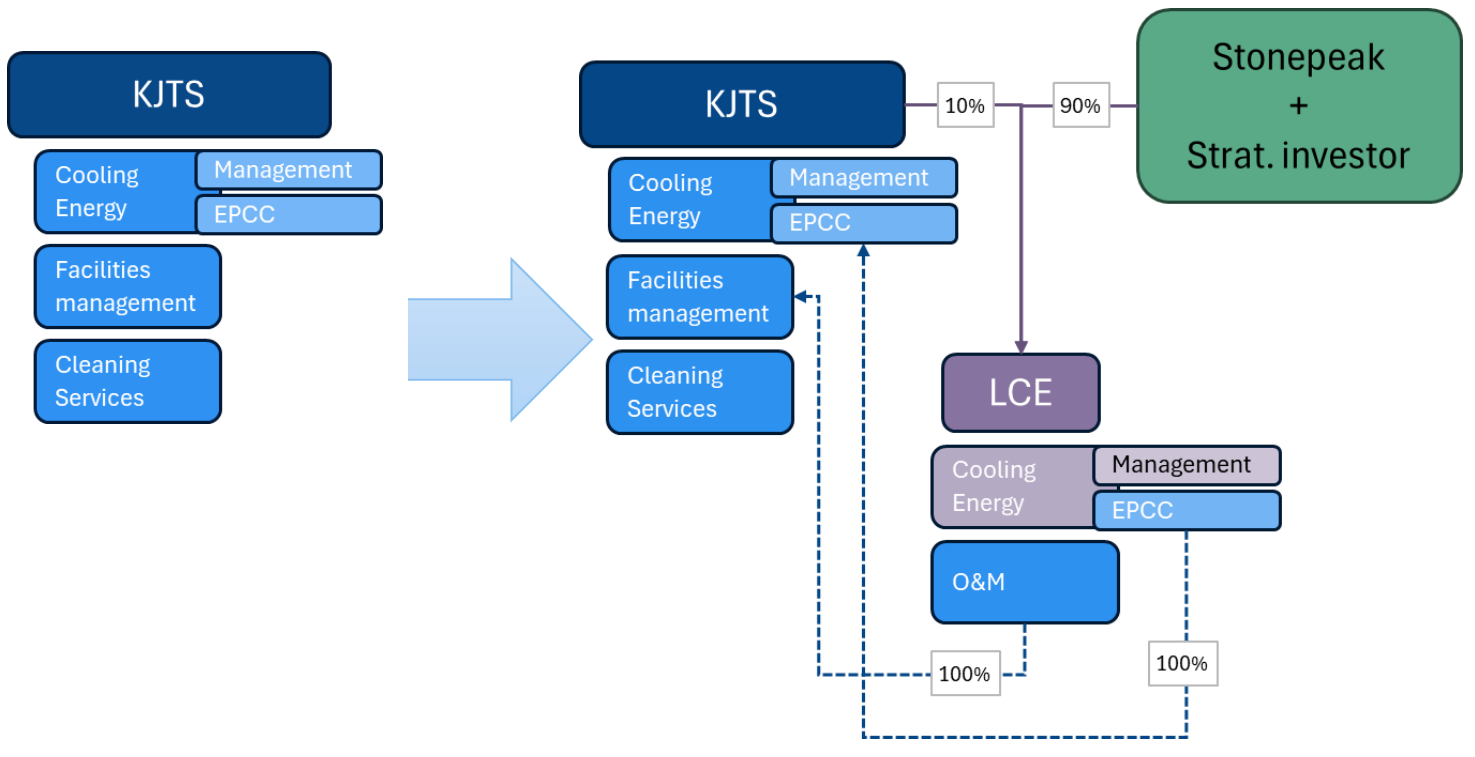

Lestari Cooling Energy - Sourcing capital for growth

KJTS has formed a joint venture with Stonepeak - Lestari Cooling Energy Sdn Bhd (LCE), with an expected capitalization of RM1.5bn. Management also indicates it is seeking another domestic strategic investor for this vehicle.

The objective is to inject CES assets into LCE, which will be a 10% associate for KJTS. While this will reduce the share of income from management of CES to 10% as well, KJTS will continue to enjoy full recognition of EPCC works undertaken for new capex. Additionally, KJTS will also charge its associate for O&M work. Of course, the related-party nature will impose limits on margins - management is guiding for 20% gross margin ceilings on both EPCC and O&M work.

The advantage of this structure is that it would allow for much faster growth as LCE’s other shareholders will take the burden of sourcing capital away from KJTS. This could be further complemented if KJTS is able to bring in a strong domestic strategic partner that can help source and secure more CES assets for injection.

Management has indicated a potential funnel of over 20 assets on its long list, that

should be able to hit the RM1.5bn enterprise value of the JV. Keep in mind that acquisitions only make up a portion of the investment required. Most of these acquisitions will require capex to enhance the assets in order to generate energy

savings that are accretive to overall returns. We estimate that for every RM2 of acquisitions, there could be roughly RM1 worth of capex.

Said capex is the underlying ST driver of value for KJTS, since it will translate into

EPCC revenues for the group. Critically, this set up allows for KJTS to potentially

monetize its existing portfolio of assets up-front, and poses an asset-light model for growth that is scalable - both onshore as well as regionally.

We note that the key factor that will enable success for this business model ultimately hinges on executing on the acquisitions. To this end, securing a domestic strategic partner into the JV will be critical.

Revised capital model

About Stonepeak

- Website: https://stonepeak.com/about

- Announcement: https://stonepeak.com/news/kjts-and-stonepeak-form-joint-venture-to-pursue-district-cooling-projects

Stonepeak Partners LP is a New York–based alternative investment manager specialising in infrastructure and real assets. Since its founding in 2011 by former Blackstone executives, Stonepeak has grown into one of the world's largest infrastructure-focused private equity firms. Stonepeak manages approximately US$76 billion in assets under management (AUM). Its investment philosophy blends the stable and utility-like cash flows of hard infrastructure with private equity-style value creation.

US$3.3 billion Stonebeak Asia Infrastructure Fund

In March 2024, Stonepeak closed its inaugural Asia Infrastructure Fund with US$3.3 billion in committed capital which exceed its US$3 billion target. The fund is dedicated to high-growth Asia Pacific infrastructure themes.

Notably, the fund has earmarked a portion of its dry powder for investments in

Malaysia. Culminating in a landmark joint venture with KJTS Group Berhad.

Strategic JV: Stonepeak x KJTS Group

On 14 March 2025, KJTS announced a strategic joint venture with Stonepeak Kelvin Holdings, an affiliate of Stonepeak, marking the US$3.3 billion Asia Fund’s first entry into Malaysia. Under the agreement:

- Stonepeak holds 90% of the JV while KJTS owns 10% via its wholly owned KJ

Technical Services subsidiary. - KJTS acts as the EPC contractor and O&M provider, leveraging its technical

expertise. - The JV is structured to raise up to RM1.5 billion (~US$340 million) in equity and debt to finance cooling and electricity distribution projects.

The venture provides Stonepeak with access to Southeast Asia’s growing district

energy infrastructure. District cooling aligns closely with Stonepeak’s thematic focus on long-term, inflation-linked cash flows and energy transition infrastructure. In Malaysia alone, demand for centralized cooling is being driven by:

- Datacentre expansion

- REITs and commercial buildings seeking ESG-compliant energy solutions

- Supportive government policy under the National Energy Transition Roadmap

(NETR)

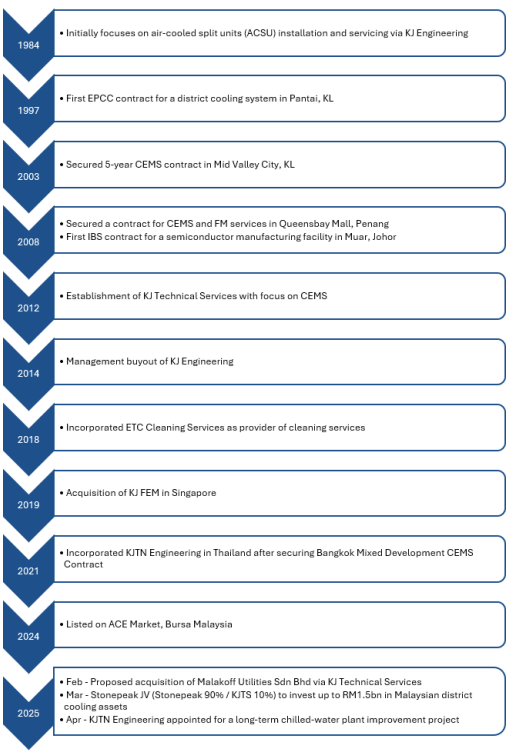

Company history

Key management:

Azura Binti Azman - Independent non-executive chairman

Azura Binti Azman was appointed as independent non-executive chairman of KJTS Group in November 2022. She brings with her over 30 years of diverse experience in capital markets and banking which cover corporate banking, institutional sales, equity broking, private equity and business development.

She is best known for her regional leadership in equities at RHB Investment Bank

Berhad where she served as Head of Group Wholesale Equities until her retirement in 2022. Her earlier career saw her take on key roles at Southern Bank, Ke-Zan Securities, Crosby Securities (UK) and HLG Securities.

Azura holds a Bachelor of Arts (Hons) in Economics and Linguistics from Victoria

University of Wellington, New Zealand. She is also a former Capital Markets Services Representative Licence holder for dealing in securities and derivatives.

In addition to her role at KJTS, she currently sits on the boards of Titijaya Land Berhad, RCE Capital Berhad and AmanahRaya Investment Management Sdn Bhd. She is also a member of Bursa Malaysia Securities’ Market Participant Committee where she contributes to regulatory development and industry standards.

Lee Kok Choon - Group managing director & substantial shareholder

Lee Kok Choon was appointed to the Board of KJTS Group as Managing Director in June 2022 and was redesignated as Group Managing Director in April 2024. He is also a substantial shareholder (~20%). With over 22 years of experience in the building support services and cooling energy industry, Lee has played a pivotal role in the Group’s strategic expansion and operational leadership.

He began his career with KJ Engineering in 2002 and rose through the ranks from

Project Engineer to COO, before becoming Managing Director of KJ Technical Services in 2013. He is best known for co-founding and growing KJ Technical Services and spearheading the management buyout of KJ Engineering in 2014. Under his leadership, KJTS has expanded its regional footprint into Singapore and Thailand.

Lee graduated with First Class Honours in Bachelor of Engineering (Mechanical) from Monash University, Australia in 1999.

He is also a director of several private limited companies. Lee does not hold any

directorship in public listed companies and maintains no conflict of interest with the Group.

Sheldon Wee Tah Poh - Executive director & substantial shareholder

Sheldon Wee Tah Poh was appointed to the Board of KJTS Group as Executive

Director in June 2022 and was redesignated as Group Executive Director in 2024. He is also a substantial shareholder (~21%). He is equipped with approximately 25 years of experience in the building support services industry.

He began his career in 1999 at PWB (M) Sdn. Bhd. and rose to the position of Managing Director before selling a majority stake to OCS Group International Limited in 2012. He later served as Managing Director and then Non-Executive Chairman of OCS Group Singapore Pte Ltd until 2018.

He professionalized his family-founded business, PWB (M) Sdn. Bhd. before

transitioning into regional leadership roles in integrated facilities management. His entrepreneurial drive led him to co-found KJ Technical Services and play a key role in the management buyout of KJ Engineering in 2014. His strategic acumen and cross-border experience were instrumental in the Group’s expansion into Singapore and Thailand.

Sheldon holds a Bachelor of Business majoring in Marketing and Information

Technology from the University of Technology, Sydney, Australia. He does not hold directorships in other public companies or listed corporations but is a director of several private limited companies. Sheldon maintains no conflict of interest with the Group.

Sector overview

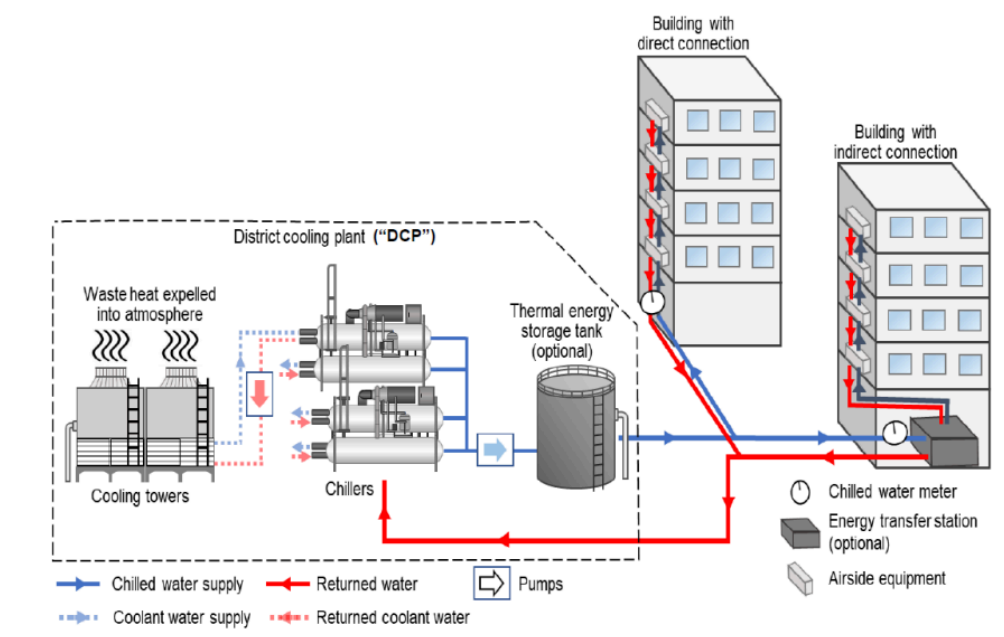

KJTS Group Berhad’s cooling energy business revolves around the delivery of energy-efficient and centralised air-conditioning solutions through chilled water systems. The company can play a dual role in this segment. First, as an EPCC contractor responsible for the full lifecycle of system construction. From engineering design to procurement, construction and commissioning. Second, as a long-term service provider managing the ongoing operations and maintenance of the completed cooling energy infrastructure. This integrated approach not only diversifies its revenue streams but also positions KJTS as a long-term partner to its clients by offering both capital works and utility-like chilled water supply services.

Illustration of a district cooling system

At the heart of its operations are centralised cooling energy systems particularly

district cooling systems (DCS) and chiller plants. DCS are large-scale centralised

facilities designed to supply chilled water to a network of buildings while chiller plants typically serve single buildings. These systems generate chilled water which is circulated via insulated piping to the buildings’ airside equipment (air handling units (AHUs) and fan coil units (FCUs)) where the chilled water absorbs indoor heat before returning to be cooled again in a closed-loop cycle. The systems are equipped with cooling towers, thermal energy storage tanks, control panels, pumps and sensors which are all orchestrated by a plant control system and supported by KJTS’s in-house energy management platform. This energy management system optimises performance by regulating chiller operation timing, managing thermal storage usage during off-peak electricity tariff hours and detecting system faults in real time.

What distinguishes KJTS’s approach is its ability to design systems that reduce long-term electricity consumption which is typically the largest operating cost in a building’s cooling infrastructure. Whether upgrading legacy systems or constructing new installations, KJTS tailors each solution based on the building’s design, location, usage profile and energy goals. For retrofitting jobs, the process typically begins with an energy audit to benchmark existing system inefficiencies. From there, KJTS proposes a solution that meets or exceeds the cooling requirements at a lower electricity cost, making the case for the upgrade compelling. In new developments, it typically works as a subcontractor under the project’s main contractor and deliver a complete optimised cooling solution that becomes a long-term revenue stream once commissioned.

The company’s involvement doesn’t end once the system is up and running. KJTS also manages ongoing cooling energy services through long-term contracts. Some of which extend up to 20 years. Under these arrangements, KJTS supplies chilled water and maintains the associated infrastructure. Ensuring system uptime and performance in line with service-level agreements. Each control room, either for a DCS or a standalone chiller plant is manned by KJTS personnel or remotely monitored from its 24/7 command centre in Kuala Lumpur. The company conducts real-time performance monitoring, preventive maintenance, corrective repair work and major overhauls. All aimed at ensuring uninterrupted cooling services for clients ranging from hospitals and malls to mixed-use commercial complexes.

Financially, the cooling energy segment has been a major contributor to the group’s performance. This revenue is derived from both EPCC contracts and recurring management fees for chilled water supply and system upkeep. Beyond Malaysia, KJTS has extended its reach to Thailand, supporting large-scale developments and reinforcing its regional presence.

Overall, KJTS’s cooling energy segment reflects a business model built on technical depth, operational integration and long-term client alignment. By combining EPCC execution with utility-style service provision, KJTS transforms cooling from a one-off construction job into a steady sustainable revenue stream backed by long-dated contracts and operational resilience.

Valuation: RM2.00 target price

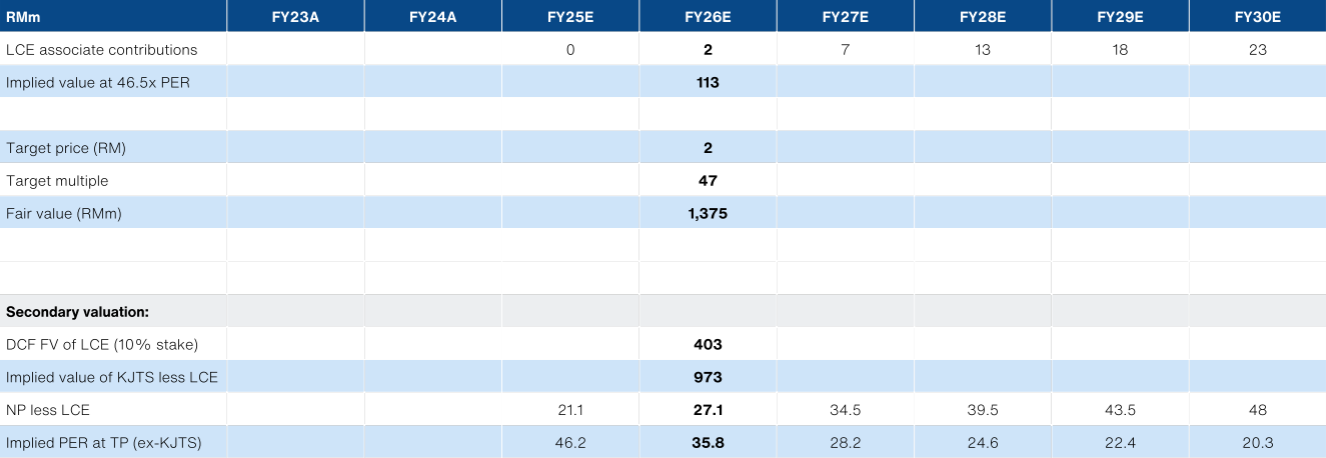

Our primary valuation methodology is PER - applying a 46.5x target multiple on FY26E earnings. This is well above the historical average PER of 21.6x. However, we flag that the earnings potential from LCE is not front loaded to FY26. Thus, while FY26 multiples look stretched at face value, we forecast multiples easing to a more digestible 33x/26x for FY27/28E.

Even then, this approach has shortcomings - even applying the elevated 46.5x PER

multiple to the associate earnings contribution from LCE (RM2.4m for FY26) - it only values the joint venture at RM113m.

However, our secondary valuation approach estimates a value of RM403m NPV for LCE. In turn, if we were to strip out the value of the JV alone (leaving the consolidated O&M and EPCC revenue streams in valuations), at RM2.00, the implied value of the KJTS is only 36x FY26E PER and 28x FY27E PER.

The key to supporting valuations going forward will be the news flow, in our view. After all, earnings delivery is spread out over several years (not front-loaded) and highly dependent on KJTS delivering a steady stream of acquisitions into LCE to support growth outlook.

Primary valuation methodology

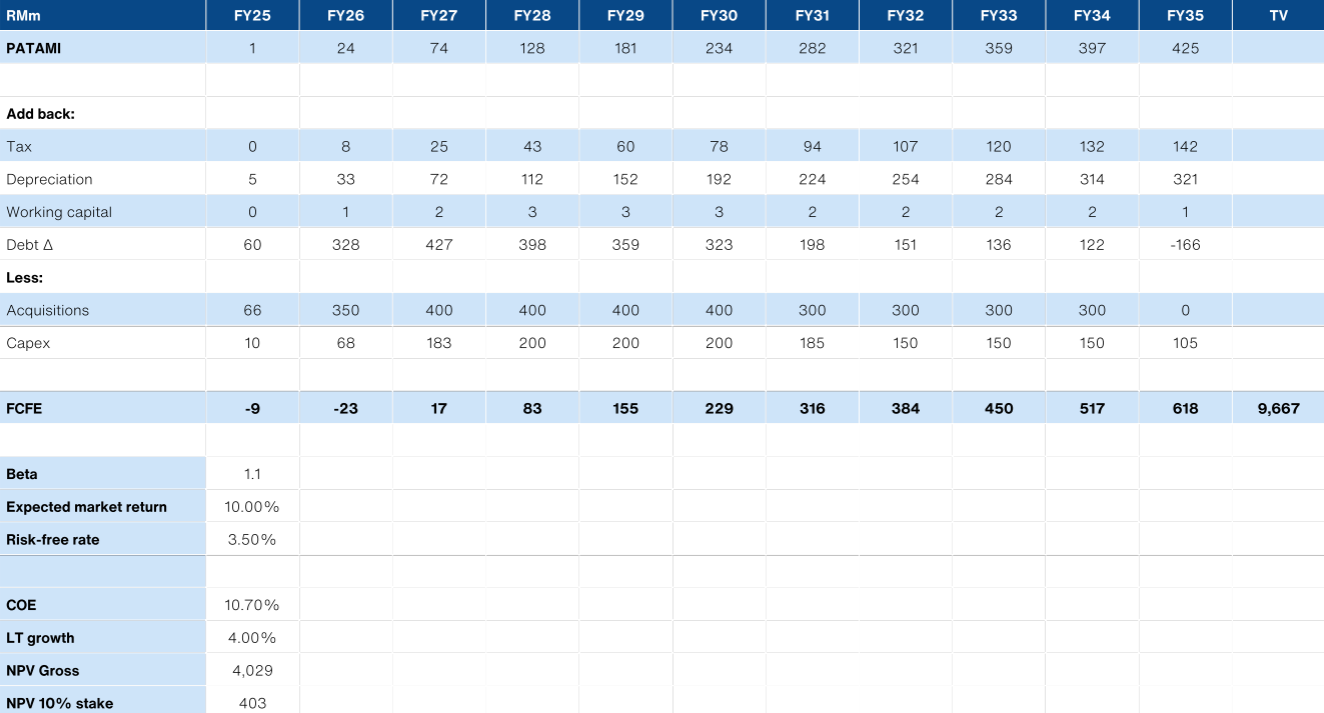

LCE valuation:

We also ran a secondary valuation on LCE. We assumed roughly RM1.5bn in total acquisitions and capex by FY28. Post-FY28, we assumed an expansion in fund size above RM 1.5bn, with continued acquisitions/capex totaling RM300-400m/per year till FY35 for our DCF stage 1.

DCF of LCE

Secondary valuation methodology

Key risks:

Failure to secure new contracts / acquisitions

Management flags that the EPCC cooling-energy business is project-driven; failure to secure new awards on commercially favourable terms or to replenish recurring

contracts in cooling energy, cleaning and FM would negatively affect financial

performance and growth. The Group’s strategy to mitigate this is to deepen Malaysia while expanding in Singapore and Thailand and to focus on larger-scale projects. This underscores that forward momentum depends on conversion of a visible pipeline into signed work.

We see this as the primary risk to the business as well as valuations, since we expect the market to react to newsflow of new acquisitions.

Reliance on strategic partners

KJTS’ strategy hinges on partners to provide capital and strategic access to cooling

assets/contracts. If Stonepeak or its prospective domestic strategic partner were to

scale back involvement or depart entirely, it would introduce substantial risk to future growth prospects.

Decrease in electricity tariff

KJTS’ cooling energy contracts include chilled-water charges (or fixed monthly charges components) which are indexed to electricity tariffs (i.e., priced as a mark-up over prevailing electricity rates). A decrease in electricity tariffs directly lowers the chilled-water tariff/charges and may compress margins if the cost reduction is smaller than the tariff reduction. (Conversely, tariff increases are passed through.)

For illustration, a 10% fall in electricity tariff would reduce chilled-water tariff and

revenue by 10% (volume constant), for the segment.

Chilled-water tariff lower than cost (cost overrun / efficiency risk)

Under cooling-energy contracts KJTS bears operating costs (power, water, manpower, maintenance). If actual costs exceed estimates due to system inefficiency, calculation errors or higher maintenance/spares, the contract can run at reduced margins or losses over its life where costs outstrip the tariff/fixed charge. KJTS highlights ongoing investments in advanced tech, 24/7 monitoring and staff training to contain this risk.

Dependence on executive directors (Key-person risk)

The Group’s overall growth, strategy and operations rely significantly on the experience and contributions of Group MD Lee Kok Coon and Group Executive Director Sheldon Wee Tah Poh. Loss of one or more could strategy delivery and day-to-day performance. The Board states it reviews succession for senior management and ensures training/appointment/performance policies. This provides a governance mitigant, but reliance remains material given the roles described.

Early contract termination

Recurrent contracts (cooling energy management/FM/cleaning) and project contracts may be ended before expiry through formal notice, performance issues, customer financial distress, legal directives or mutual agreement. This may result in lost revenue and profit relative to original contract value. We see low risk of this occurring, since customers have limited alternatives.

Cooling energy contracts where KJTS has funded construction/retrofits face an added risk: termination before full capital recovery. The Group also has several long-dated contracts (some expiring through 2038) which raises exposure to unforeseen events over time. KJTS notes it incorporates compensation clauses to mitigate early-termination impact, but collection/recovery is not guaranteed.