Placement incoming

KJTS will be offering up to 14.82% new shares to comply with Bumiputera Equity Conditions; up to 102m new shares.

Stock information

KJTS

KJTS - 0293.KL

TRADING BUY

Target price: RM2.00

Last price: RM1.67

Market cap (RMm): RM1,150m

Shares out: 689m

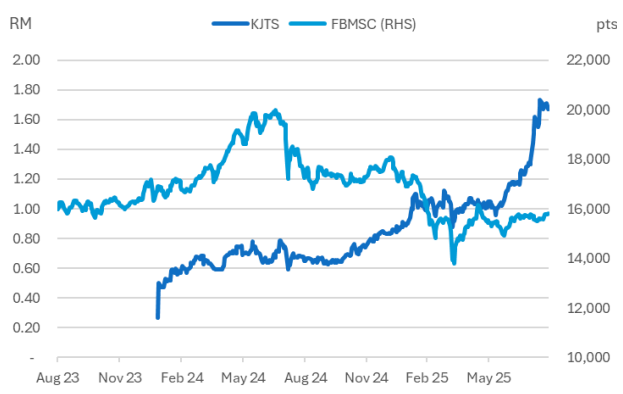

52-week range: RM0.62 / RM1.76

3M ADV: RM1.8m

T12M returns: 152%

Disclaimer: By using this information, you hereby acknowledge that you are fully and solely responsible for evaluating the merits and risks of any investment decision and agree not to hold NewParadigm Research fully liable whatsoever for any actions, omissions and/or damages of any kind or matter arising from such decision.

Key takeaways

- KJTS will be offering up to 14.82% new shares to comply with Bumiputera Equity Conditions; up to 102m new shares.

- Total proceeds raised will potentially as much as ~RM153m, assuming full take up at 5% discount.

- While dilutive for existing shareholders, relatively high valuation on the potential issuance is positive.

Share price performance

Investment fundamentals

| RMm | FY24A | FY25E | FY26E | FY27E |

|---|---|---|---|---|

| Revenue | 138 | 186 | 222 | 280 |

| Revenue Growth | 15% | 35% | 20% | 26% |

| EBITDA | 12 | 28 | 35 | 44 |

| EBITDA margin | 9% | 15% | 16% | 16% |

| PATAMI | 15 | 21 | 30 | 42 |

| PATAMI margin | 11% | 11% | 13% | 15% |

| ROA | 10% | 12% | 13% | 15% |

| ROE | 13% | 16% | 19% | 23% |

| PER | 70 | 51 | 36 | 26 |

| P/BV | 9.2 | 8.2 | 7.0 | 5.9 |

| Yield | 0.0% | 1.0% | 1.0% | 2.0% |

Source: Company data, Bloomberg, NewParadigm Research, August 2025

Dilutive, but at a good price

- The offering is in order to comply with the Bumiputera Equity Condition - ACE listed companies have to allocate at least 12.5% of its enlarged shares to Bumiputera investors to be approved by MITI within one year of achieving profit requirements for companies seeking listing on the Main Market.

- The 14.8% reflects the maximum scenario with the enlarged share capital including the exercise of all employee share option scheme shares.

- Assuming ESOS is not exercised, the amount of shares issued will be lower at 98.4m shares KJTS will offer the new shares at no more than a 10% discount to the 5-day VWAP, the latter is currently RM1.58. A 5% discount would be

~RM1.50. - Assuming full take-up this would translate to RM153m in the capital raised for KJTS in the maximum scenario. The maximum take-up in the minimum scenario would be RM148m (ESOS not exercised)

- However, given strong share price performance over the past 3 months, and the relatively high valuations, we anticipate that the placement is unlikely to achieve full take-up.

- Broadly, the utilization of proceeds will be primarily allocated to expansion of the cooling energy segments as well as general working capital.

- Management has no minimum take-up or claw back for this offering. Thus, ultimate subscription levels could be very low.

High take-up is unlikely

- Overall, the downside from the dilution to existing shareholders is substantially offset by the relatively high valuations at the time of issuance. This is likely to be further mitigated by (we expect) relatively low take-up.

- The additional funds would be helpful as well. KJTS has a substantial funnel of acquisition/capex opportunities over the next 12-18 months.

- Maintain Trading Buy with RM2.00 TP.