Second half tailwinds

2H25 enjoys multiple earnings drivers - higher electricity tariffs, improving margins, MUSB acquisition, and overseas projects.

Stock information

KJTS

KJTS - 0293.KL

TRADING BUY

Target price: RM2.00

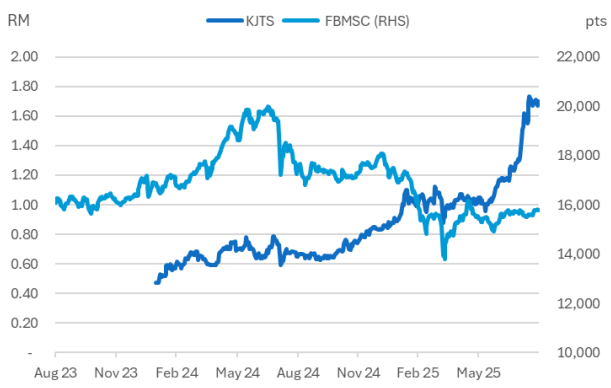

Last price: RM1.70

Market cap (RMm): RM1,171m

Shares out: 689m

52-week range: RM0.62 / RM1.76

3M ADV: RM1.8m

T12M returns: 151%

Disclaimer: By using this information, you hereby acknowledge that you are fully and solely responsible for evaluating the merits and risks of any investment decision and agree not to hold NewParadigm Research fully liable whatsoever for any actions, omissions and/or damages of any kind or matter arising from such decision.

Key takeaways

- Post-results briefing was well-attended and management’s tone was constructive overall.

- 2H25 enjoys multiple earnings drivers - higher electricity tariffs, improving margins, MUSB acquisition, and overseas projects.

- Still, primary catalyst for share price remains the onboarding of a GLIC investor into LCE in the next 3-6months.

Share price performance

Investment fundamentals

| RMm | FY24A | FY25E | FY26E | FY27E |

|---|---|---|---|---|

| Revenue | 138 | 186 | 222 | 280 |

| Revenue Growth | 15% | 35% | 20% | 26% |

| EBITDA | 12 | 28 | 35 | 44 |

| EBITDA margin | 9% | 15% | 16% | 16% |

| PATAMI | 15 | 21 | 30 | 42 |

| PATAMI margin | 11% | 11% | 13% | 15% |

| ROA | 10% | 12% | 13% | 15% |

| ROE | 13% | 16% | 19% | 23% |

| PER | 70 | 51 | 36 | 26 |

| P/BV | 9.2 | 8.2 | 7.0 | 5.9 |

| Yield | 0.0% | 1.0% | 1.0% | 2.0% |

Source: Company data, Bloomberg, NewParadigm Research, August 2025

2H25 drivers

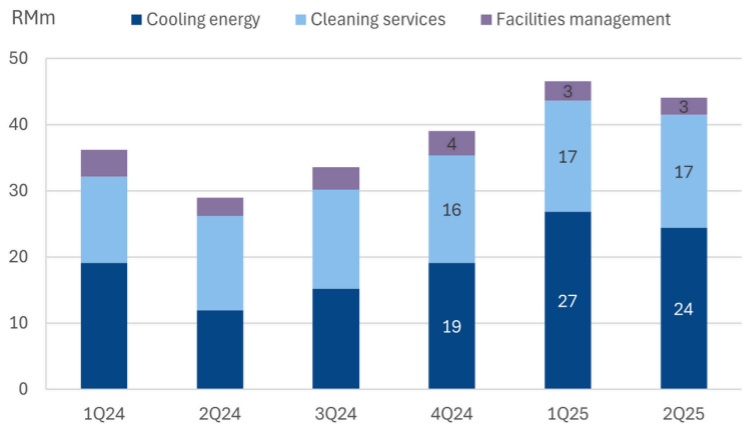

- Electricity base tariff hike of +13.6% (in July) will directly translate into stronger revenues for the cooling energy services segment in 2H25 - we estimate roughly +RM1.5m upside to 2H revenues.

- Critically, the higher tariffs is also driving more interest from potential clients seeking to mitigate the higher energy costs with more efficient cooling operations.

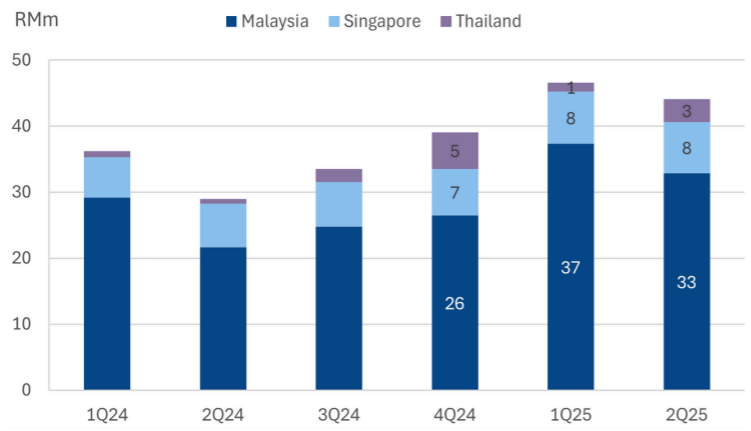

- EPCC -2Q25 was actually a little softer for EPCC recognition due to timing differences. Management is guiding for more projects to start in 2H25. Overseas funnel also appears to be improving, especially for Thailand with a focus on hotels.

- While management could not comment on the project values, current

orderbook (including LT concession projects) now stands at RM482m roughly 2x our FY25 revenue projections. - Malakoff Utilities Sdn Bhd acquisition should be finalized within 2H25,

pending several final conditions that need to be met, guides management. This should drive an immediate contribution to earnings. - KJTS is booking about RM1.5m per quarter from “consultancy fees” charged to the Lestari Cooling Energy joint venture with Stonepeak. This should be a recurring contribution going forward.

- Margin recovery: Management explained that the GP margin decline from 16.5% to 14.9% for the cleaning services segment was due to clients opting not to absorb the higher labor costs. But with all foreign worker allocation fully utilized, management is looking to terminate underpriced contracts to redeploy worker headcount to new clients at market pricing. This should normalize segment gross margins to ~16.5%.

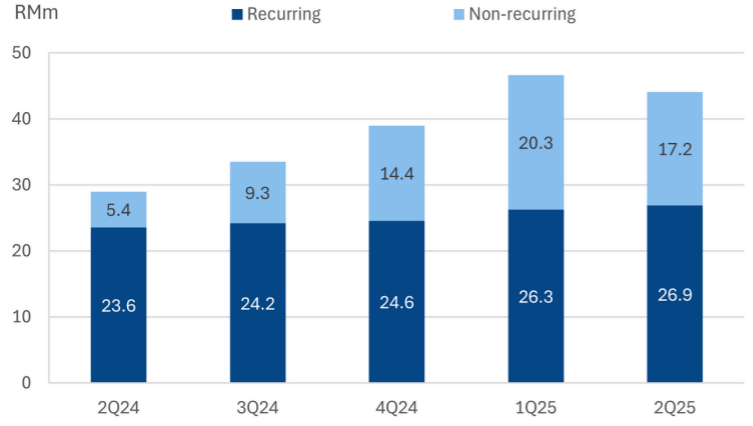

- Looking ahead, we expect to see the group’s recurring income base

accelerate in 2H25, supported by the aforementioned catalysts.

Maintain trading buy

- KJTS’s share price outlook over the next 3-6 months should be driven by newsflow - either on new project wins or the inclusion of new partners into the Lestari Cooling Energy consortium.

- Maintain our target price of RM2.00 and our Trading Buy call. Our target price implies a PER of 33x FY27 PER.

About the company

KJTS’ core business is providing cooling energy services via large-scale district cooling systems. The company bears the capex to upgrade existing cooling systems to improve energy efficiency, offering clients immediate savings with no capital outlay. KJTS books the EPCC revenues as well as enjoying the surplus energy savings and the facilities management over a long-term contract. In turn, KJTS’ secured business has direct leverage to energy prices and long-term growth is tied to securing new projects.

About the stock

KJTS is a Shariah compliant stock that was listed in 2024 in the ACE market. In our view, KJTS is misclassified as an industrial products and services company. It might be better to think of KJTS as a utility or energy stock.

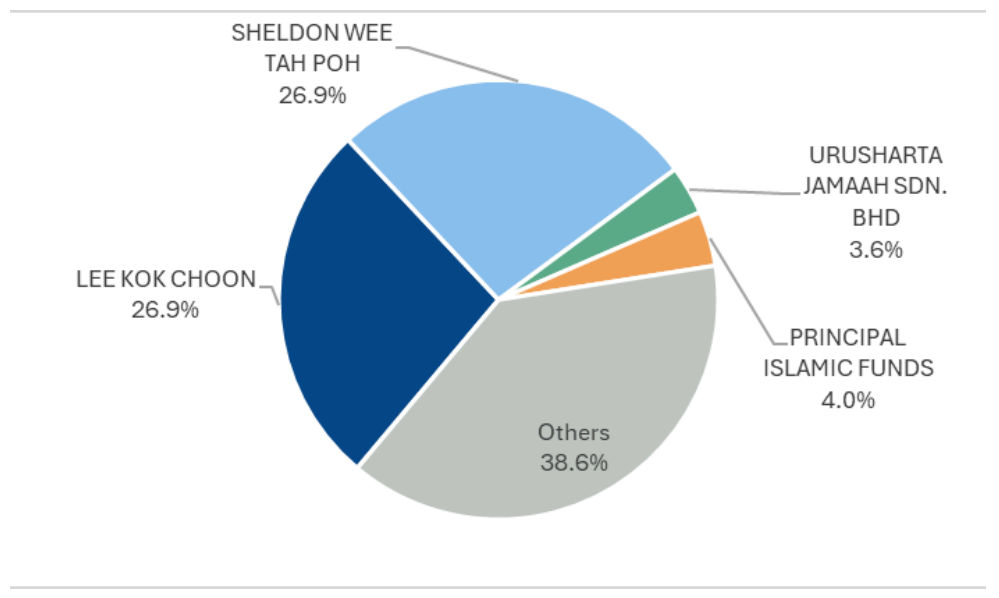

KJTS was originally the Asean arm of Dalkia Group, prior to a management buyout in 2014 by Lee Kok Choon and Sheldon Wee - both currently the key management and controlling shareholders (combined).

Investment thesis

KJTS offers a unique exposure to energy efficiency for large scale cooling

infrastructure, including datacenters. We see deep value in the group’s long-term growth potential, against a backdrop of global warming and energy price inflation. The recent kicker for the group is the change in its capital model - from purely self-funding to relying on strategic partners like Stonepeak to supply capital, without significant compromise on earnings accretion. At this juncture, we recommend KJTS as a Trading Buy.

Key risks

- Failure to secure new projects - will severely limit growth. Acquisitions could be lumpy and intermittent.

- Dependency on partners - the joint venture with Stonepeak is a lynchpin to our thesis. If the partner(s) choose to withdraw from the joint venture, it would hurt KJTS’ growth prospects.

- Execution risk - failure to meet expected energy efficiency targets could result in lower or even negative returns on a project.

Shareholding breakdown

Revenue by geography

Revenue by segment

Revenue - recurring vs non-recurring