Rapid Scale-Up on High Margins

In a sector with arguably elevated valuations, we foresee LSH distinguishing itself with a combination of robust orderbook growth and sector-leading margins.

Stock information

LSH Capital

LSH - 0351.KL

BUY

Target price: RM3.50

Last price: RM2.31

Market cap (RMm): RM1,937m

Shares out: 838m

52-week range: RM0.730 / RM2.56

3M ADV: RM5.05m

T12M returns: 189%

Disclaimer: By using this information, you hereby acknowledge that you are fully and solely responsible for evaluating the merits and risks of any investment decision and agree not to hold NewParadigm Research fully liable whatsoever for any actions, omissions and/or damages of any kind or matter arising from such decision.

Key takeaways

- RM3.2bn orderbook funnel over next 24 months and RM1.8bn GDV of property launches.

- Sector leading ~19% NP margins (FY25-27E) translates to +45% NP CAGR by FY27E.

- Initiate coverage with a BUY and target price of RM3.50, which implies only 11x FY27E PER.

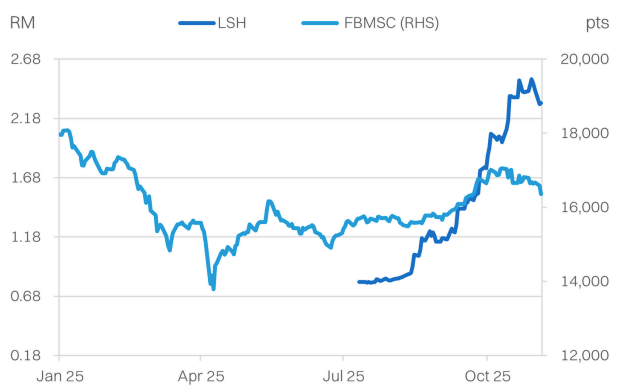

Share price performance

Investment fundamentals

| RMm | FY24A | FY25E | FY26E | FY27E |

|---|---|---|---|---|

| Revenue | 361 | 439 | 600 | 742 |

| Revenue Growth | 1% | 22% | 37% | 24% |

| EBITDA | 106 | 139 | 173 | 213 |

| EBITDA margin | 29% | 32% | 29% | 29% |

| Adj PATAMI | 74 | 103 | 140 | 225 |

| PATAMI margin | 21% | 23% | 23% | 30% |

| ROA | 12% | 12% | 14% | 17% |

| ROE | 16% | 19% | 22% | 28% |

| PER | 21.9 | 18.8 | 13.8 | 8.6 |

| P/BV | 3.4 | 3.6 | 3.0 | 2.4 |

| Yield | 1.0% | 1.0% | 2.0% | 3.0% |

Source: Company data, NewParadigm Research, November 2025

Orderbook surge + quality margins

- Between the RM3.2bn in potential orderbook wins and the RM1.8bn GDV in new property launches, LSH Capital has a solid funnel to drive revenue growth over the next 24 months. But the major differentiator will be the group’s sector leading margins, which we forecast will drive +45% PATAMI CAGR.

- LSH Capital averages a GP margin around 30% and NP margin around 20%. While there should be some dilution as the group scales up and takes on larger projects with lower margins, if it can keep core NP margins in the high-teens, it would remain one of the best in the sector. We contrast this with other construction stocks that have seen steep revenue growth on bloating orderbooks, but diluted by a sharp fall in margins.

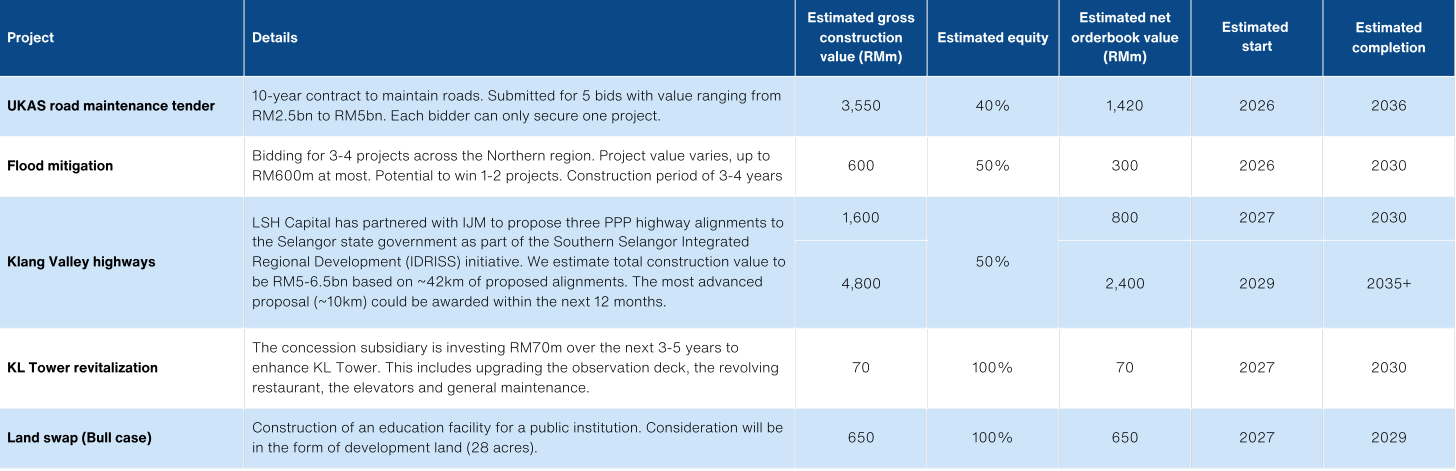

- Key construction projects include a UKAS road maintenance contract (RM2.5-5bn potential) and an RM1.7bn highway concession in the Klang Valley that should be awarded within the next 12 months. On a 40% & 50% stake respectively, this translates to an estimated net orderbook win of RM2.2bn.

- Property development’s key project will be Lake Side Homes that launches later this year with a GDV of RM1.15bn. For contrast, the group’s unbilled sales is only ~RM120m.

- Meanwhile, the 20-year KL Tower concession provides a stable recurring income to the tune of ~RM70m revenue/annum.

- Beyond the 2-year funnel, LSH Capital is also pursuing another RM2.4bn bids for construction and >RM7bn GDV developments.

Earnings delivery will be key

- We initiate coverage on LSH Capital with a BUY and a target price of RM3.50 based on 13x FY27E PER. This is in-line with the KL Construction Index’ long-run average PER, which is relatively conservative.

- At the last close of RM2.31, LSH Capital is only trading at an implied 14x FY26E and 9x FY27E, which is well below the current KLCON trailing 3yr average PER of 15x.

- Our bull case fair value is RM3.75, on the basis of a further RM650m orderbook boost from a land-swap project that will add +8% NP in FY27E.

About the company

Lim Seong Hai Capital Bhd (LSH Capital) is a construction company with a secondary focus on property development and facilities management. The group differentiates itself from peers by its sector leading margins, low gearing and low reliance on subcontractors (~10%). Within construction, LSH Capital’s primary focus is infrastructure jobs. The group also has a 20-year concession to maintain and operate KL Tower and is pursuing highway concession opportunities as well.

About the stock

LSH Capital is named after the late Lim Seong Hai and is now co-owned and run by his four children. It is also seen as a breakaway from the Tan Sri Lim Kang Ho’s group of companies (including Ekovest), which have similar operating segments. LSH Capital was initially listed on the LEAP market in 2021 but has since been promoted to the ACE market in March 2025.

Investment thesis

LSH Capital has a relatively large funnel of construction orderbook and property development launches, compared with its current low-base. Additionally, the group’s peer-leading margins allows for meaningful translation of orderbook wins to earnings. We forecast earnings growth to +45% CAGR (FY27E). Looking ahead, this implies LSH Capital is trading at single-digit PER multiples on FY27E, which is well below sector average.

Key risks

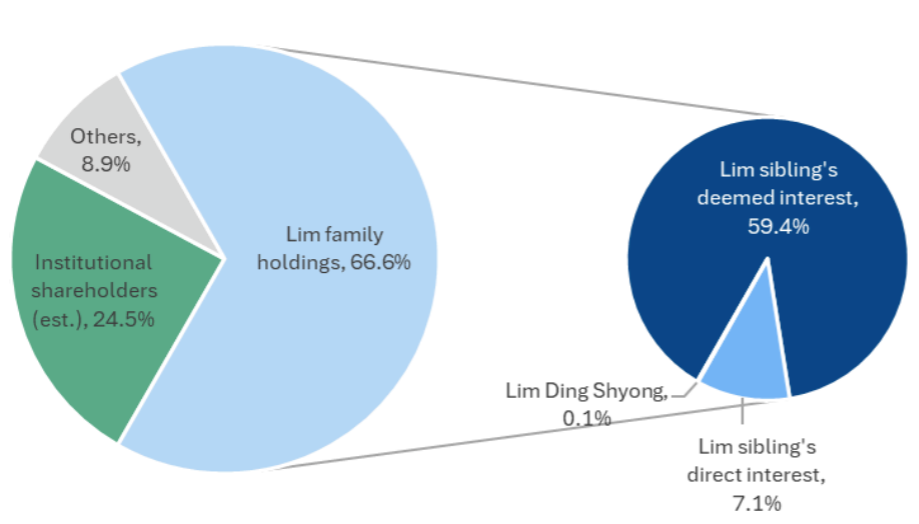

- Family business - The four Lim siblings collectively control 61% of the company and have full management control. Only 50% of the board is independent.

- Related party transactions - The group has a history of RPT transactions, and injection of related businesses. As LSH Capital transitions to non-RPT work, it remains to be seen if margins will continue to hold up.

- Small balance sheet - Net tangible assets total only RM400m (excluding RM149 goodwill on consolidation. We anticipate risk of additional fund-raising if capital intensive projects are secured.

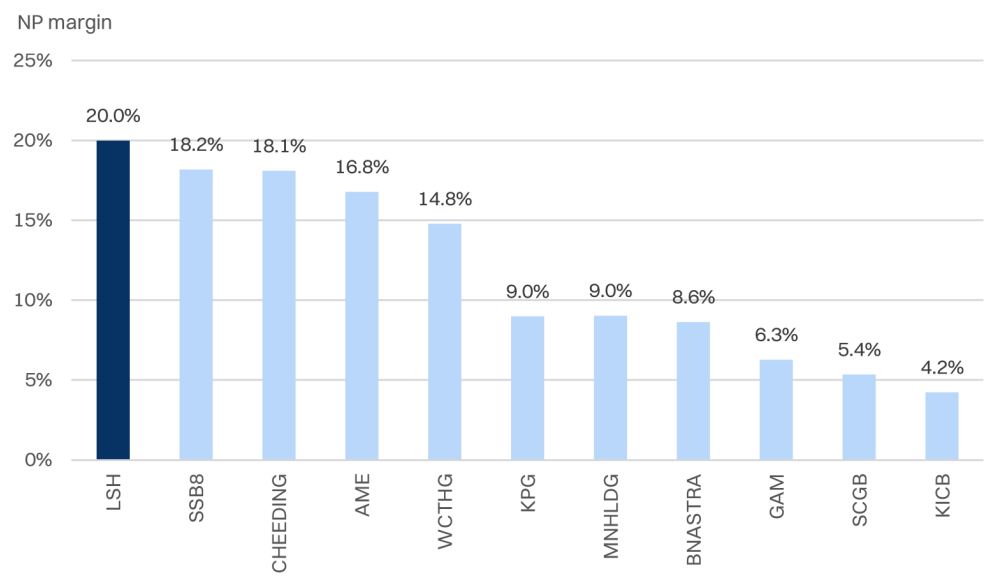

T12M NNP margins - LSH Capital is peer-leading

Orderbook surge + quality margins

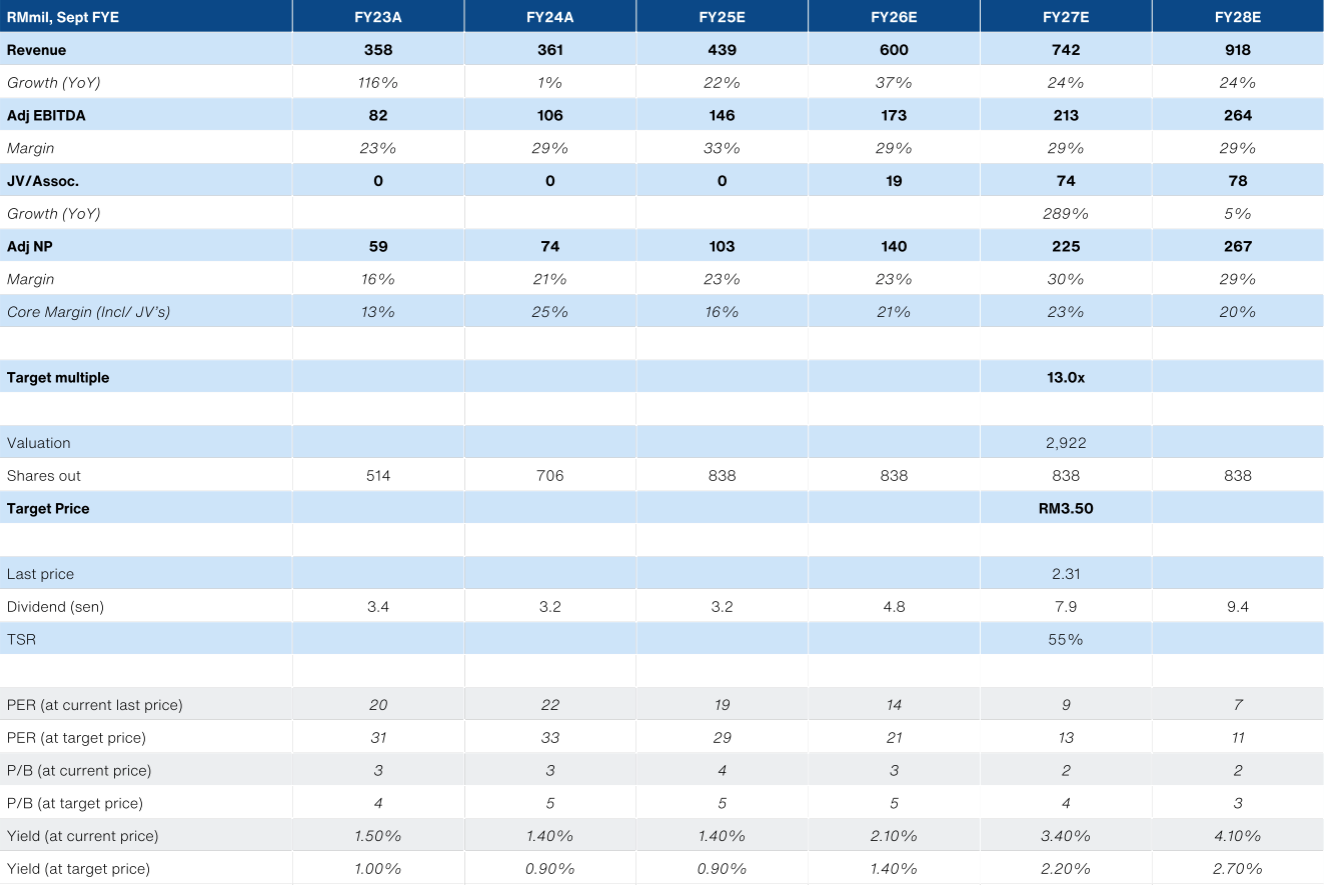

We initiate coverage on Lim Seong Hai Capital (LSH Capital) with a BUY and a target price of RM3.50 on 13x FY27E PER.

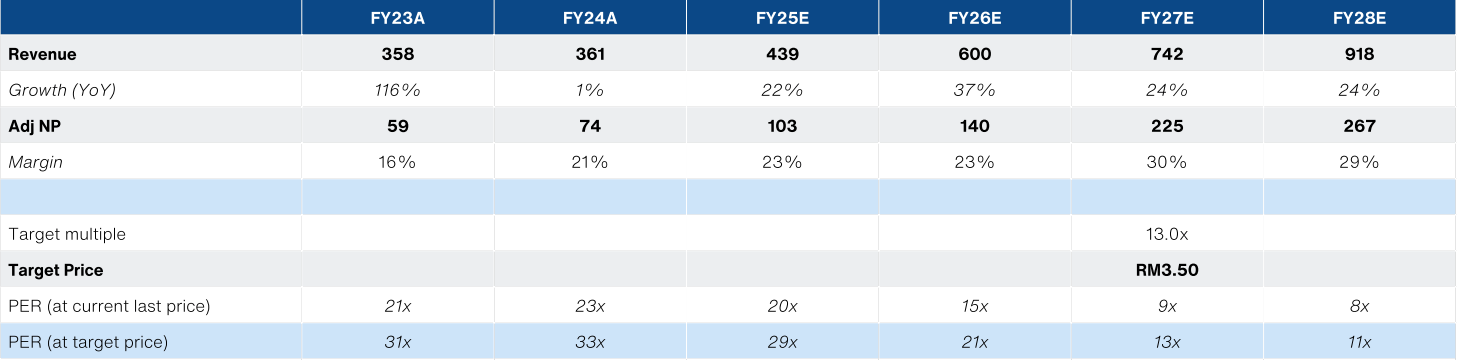

In a sector with arguably elevated valuations, we foresee LSH distinguishing itself with a combination of robust orderbook growth and sector-leading margins. We forecast the combination driving FY27E Adj NP to RM225m (+45% 3yr CAGR). This implies the stock is currently trading at a reasonable ~9x FY27E PER and orderbook wins should catalyze further re-rating.

High-level summary of forecasts

- Construction (60% of revenue): LSH has high potential to bag ~RM2.6bn of new orderbook wins over the next 12 months with a further ~RM3.1bn funnel beyond 12 months.

- Property development (30% of revenue): RM1.8bn GDV of launches over next two years, with a further funnel of >RM7b beyond. Unbilled sales are currently only RM120m.

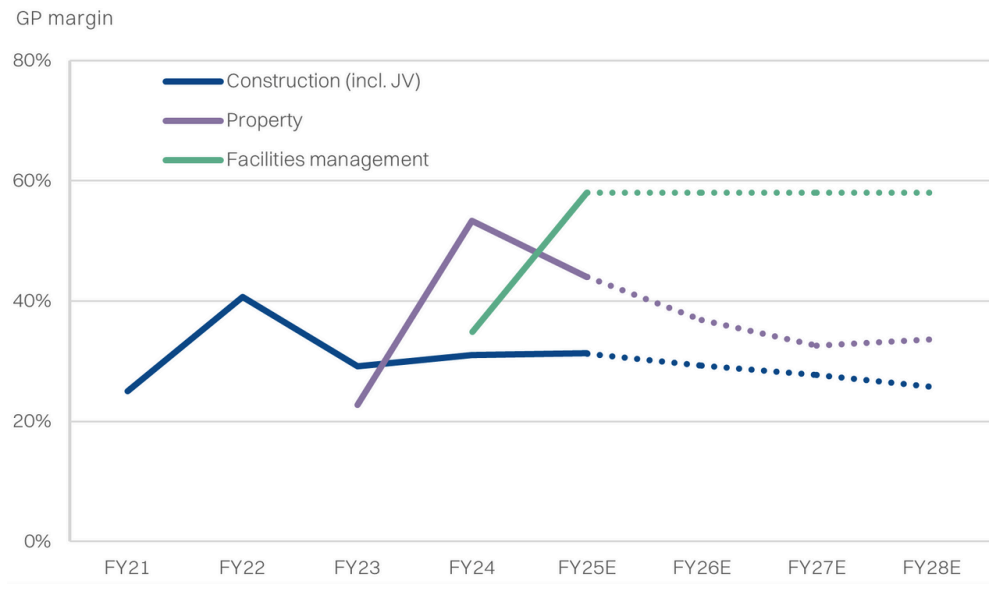

- Margins are sector-leading at ~21% net historically. We’ve assumed some margin dilution to ~19% (core, adjusting for JV revenues).

Where LSH Capital differentiates itself:

- Focus on projects with control of design to maximize margins with ~90% of works are undertaken in-house, only ~10% outsourced to subcontractors.

- Lower reliance on federally funded infrastructure projects, instead leaning on public-private partnership for build-operate-transfer highways.

- Low leverage, with focus on partnering with landowners for property development. However, this will change going forward with highway concessions (off-balance sheet debt) and potential land-swap deal (for property development).

- Building a track-record of successfully tendering for state and federal jobs, with the recent award of the KL Tower concession.

Bull case FV: RM3.75

- Our key bull case assumption is an additional ~RM650m orderbook win. This is for the construction of education-related buildings for a public agency, that LSH Capital is tendering for.

- We estimate it will add 7.7% upside to FY27E earnings. On the same 13x PER target multiple, the bull case fair value is RM3.75.

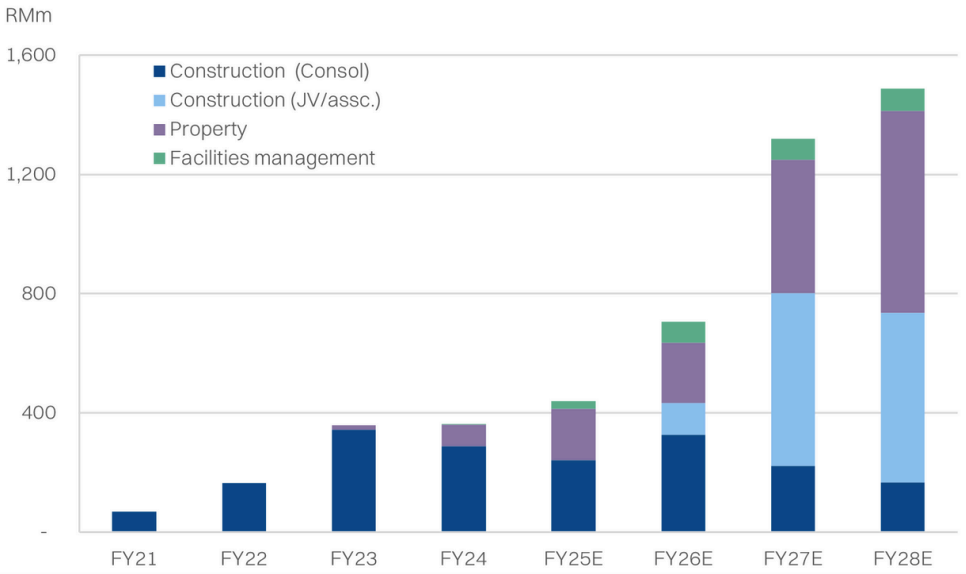

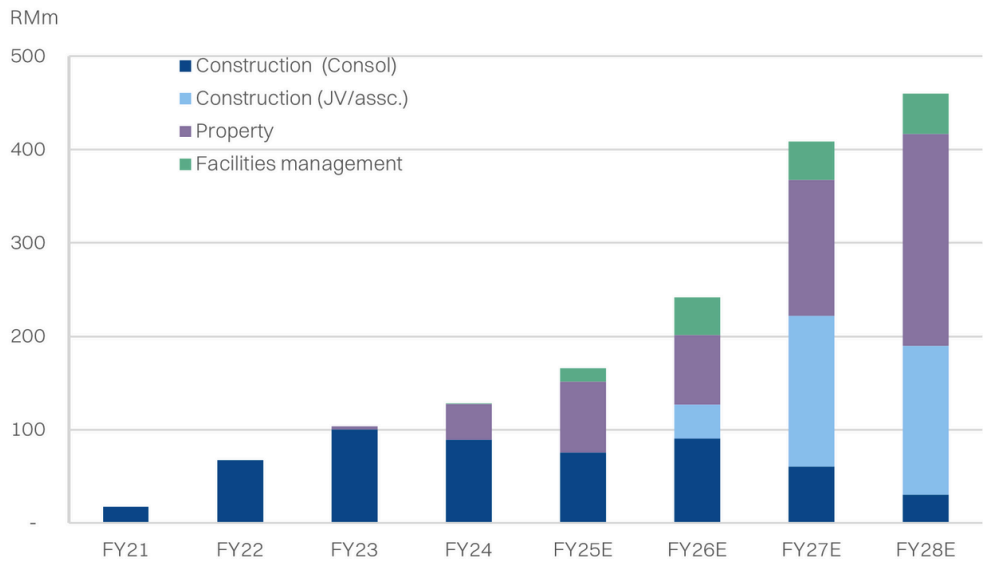

Revenue breakdown

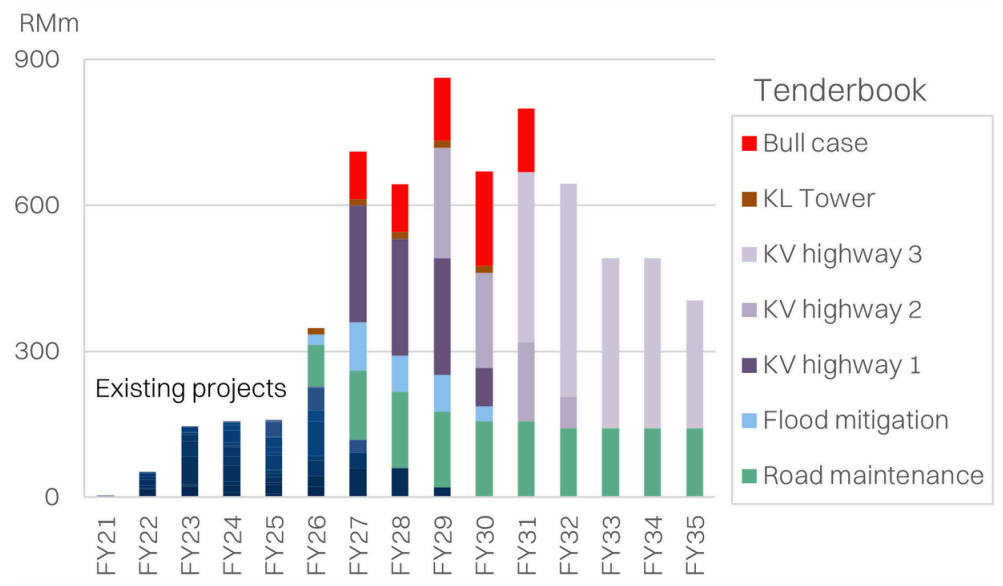

Orderbook assumptions

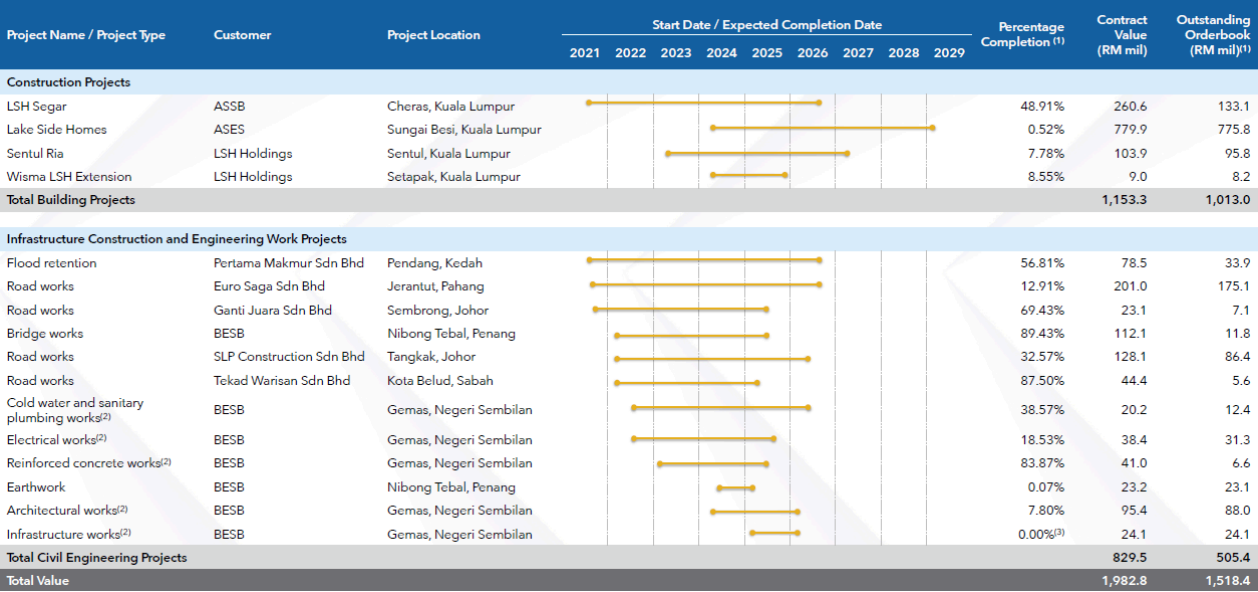

LSH Capital is currently sitting on an orderbook of RM586m with an estimated burn rate of RM150-200m per year that will cover the group will FY28.

Against this backdrop, we estimate that the group has a funnel of RM2.6bn of jobs with high probability of success, as well as a further RM800m for a highway concession. These bids are likely to crystalize in the next 12 months, driving further re-rating in the share price.

Furthermore, we foresee another RM650m bull-case upside from a potential land-swap project and a long-term funnel of RM2.4bn from the remaining highway alignments.

- Current orderbook: RM586m

- Non-highway projects: RM2.6bn

- Highway concession (alignment 1): RM800m

- Land swap (Bull case): RM650m

- Highway concession (alignment 2&3): RM2.4bn

Orderbook outlook

These additional orderbook wins will drive ~RM500m in additional revenue for the segment (including proportional JV share or revenues) in FY27E, compared with the current run rate of ~RM160m for FY25E.

Even if we assume net margins for the segment cools to 18% (FY25E: 20%), this will make up ~RM90m or 40% of FY27E net profits (including JV contribution) and strongly underpins our RM225m PATAMI forecast.

Simplified PER valuation table

Gross profit by segment

Construction segment GP margins

Detailed group revenue breakdown - consolidated

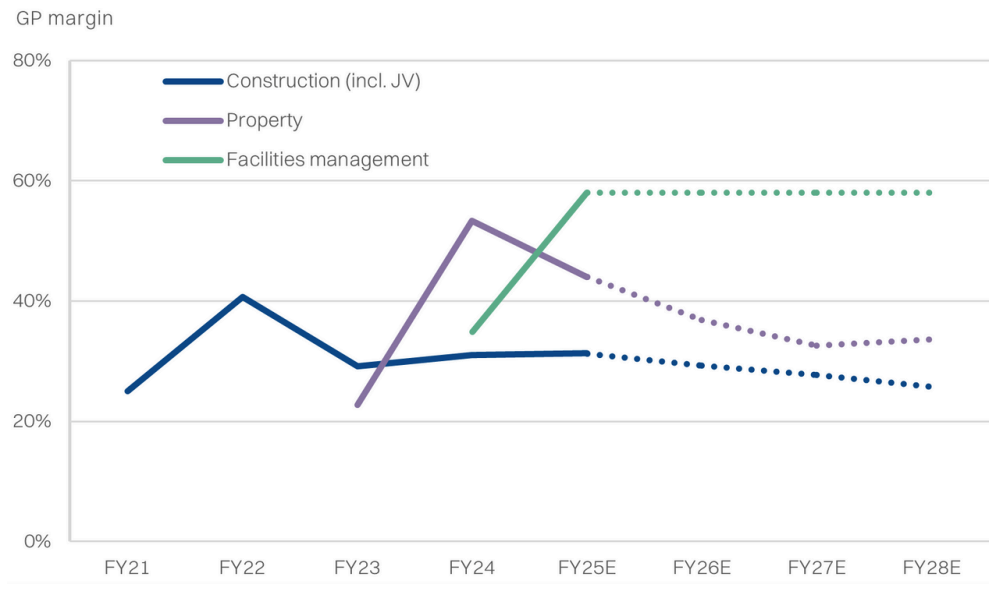

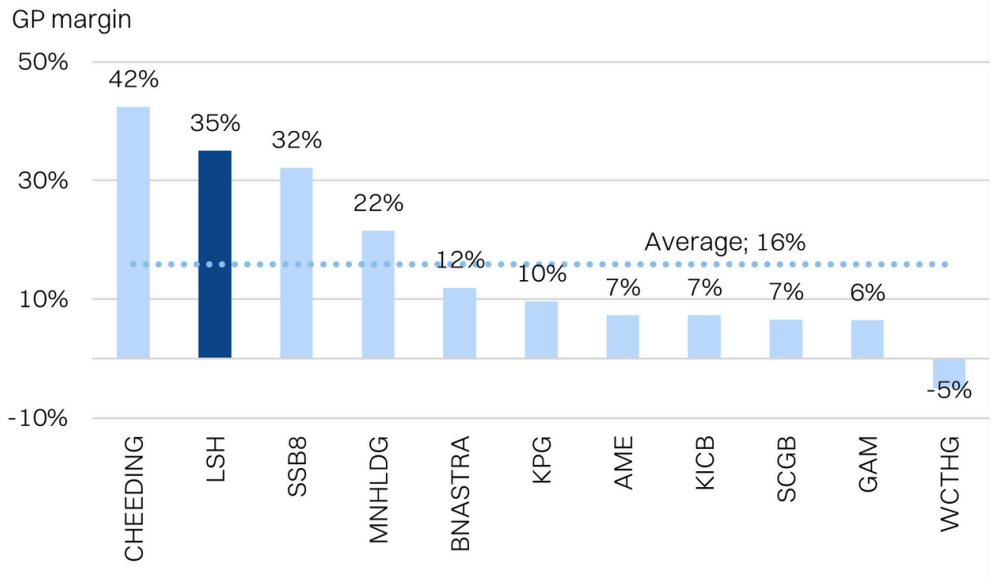

Construction, a margin outlier

LSH Capital’s construction GP margins of 35% is exceptional among its peers, roughly double the sector average that languishes in the mid-teens. In fact, LSH Capital’s GP margins are more comparable to specialist construction players like Cheeding, Southern Score Builders and MN Holdings. Civil works contractors typically deliver GP margins in the high single digits.

However, the critical eye will notice that a large proportion of LSH Capital’s existing orderbook stems from related-party work - roughly half is coming from Besteel Engtech S/B, which is controlled by Datuk Lim Keng Guan (one of the four siblings).

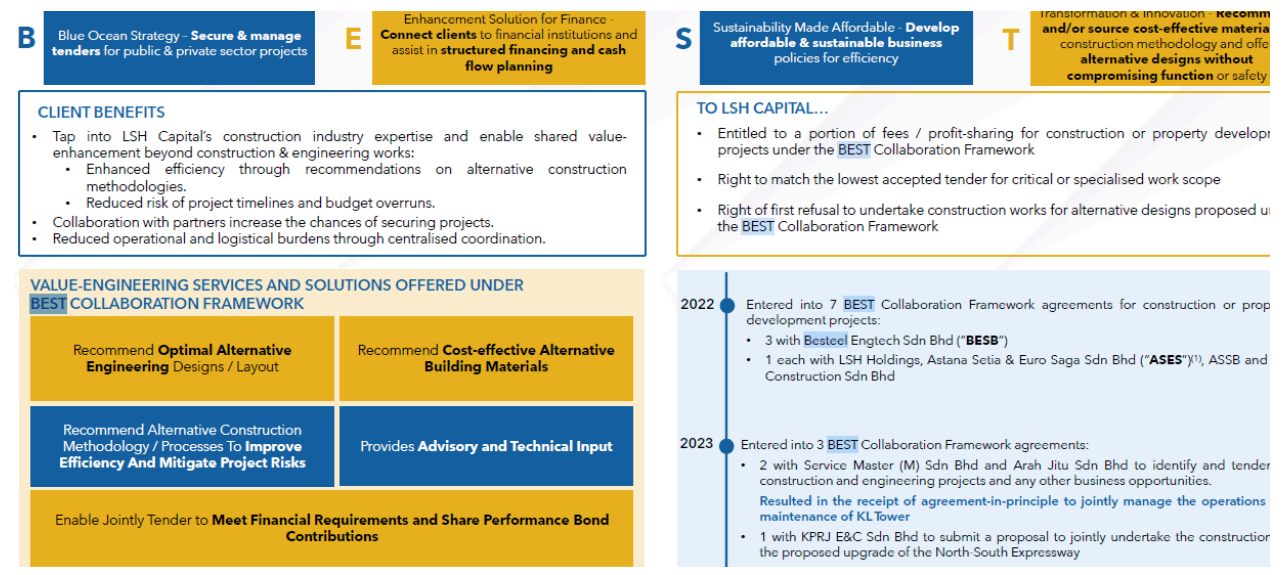

Management attributes the high margins to its BEST Collaboration Framework (see below). In summary, it requires control of a project’s design, collaboration with project owners, as well as aggressive opportunism to boost margins. We think the control of design as a critical component of the BEST framework, since it allows LSH Capital to conform the delivery of a given project to the capability of its existing assets.

Another interesting dynamic of the group is the relatively low share of sub-contracted work - roughly 10% only, and primarily for manpower requirements. This allows for better operational and financial control of any given project. It also gives the construction products segment better economies of scale to support the external revenues for the segment.

Construction segment GP margins (T12M)

The big question will be - are the margins sustainable?

We have baked in some compression in GP margins. In particular, we have assumed infrastructure works (like highways) will have GP margins in the low-20's. However, this won’t be visible in the consolidated accounts since it will fall under JV accounting. Note that the bulk of the construction revenues will not be consolidated going forward, as LSH Capital has strategic partners on the bulk of its tenders.

In turn, an artificial expansion of the headline net profit margin should be expected in the coming years.

BEST practices

The BEST Collaboration Framework (Blue Ocean, Enhancement, Sustainability and Transformation) is an in-house delivery model introduced by LSH Capital to enhance cooperation with project owners. Under this framework, the group works with clients from the design and tender stages through to completion, providing value-engineering input, financing support, and sustainability solutions. This model allows LSH to participate early in project planning, improve technical coordination, and build long-term client partnerships. Although the commercial structure of each collaboration is not publicly disclosed, the framework has helped the group strengthen project visibility and differentiate itself from conventional contractors.

BEST collaboration framework

Existing orderbook - remaining value: RM586m

Orderbook funnel

Within our forecast period (up to FY27E), we have assumed that LSH Capital will

able to secure roughly RM2.6bn in contracts in our base case. This includes one of the highway alignments. In addition to this, there is a bull case land-swap project, within the forecast period.

In turn, the key spike in revenues will take place in 2027 (note that the bulk of construction revenues will not be consolidated, but accounted for in JV/associates).

But beyond 2027, one of the reasons we like LSH is the potential visibility that is underpinned by two additional highway concession projects that is worth (we estimate) a further RM2.4bn.

Gross construction tenderbook value (including JV / associate share)

Key segment risks:

As with most construction projects, the big risk lies with securing the project at all, but here are some of the more nuanced risks for the key projects.

With regards to the UKAS road maintenance projects, the project values range from RM2.5bn to RM5bn over 5 packages. On paper, LSH Capital is bidding for roughly RM10bn of projects here, but can only be awarded one. These bids are tied to the expiry of Protasco’s (the currently incumbent) concessions for these projects in February 2026. Protasco has managed to book PBT margins of 8-11% for its maintenance segment over the years. We are optimistic that LSH Capital will be able to extract better margins, but falling below would be a risk.

The three Klang valley highway proposals are build-operate-transfer concessions under a public-private partnership framework. Drawing from experience with building the DUKE highways under Ekovest, LSH Capital’s strategy for these new alignments is to focus on connecting existing highways. This should reduce the traffic volume risk. The highways are relatively short.. 10-15 km (we estimate) each, but generally either elevated or at a high cost per km. We estimate the alignments will be around RM150m/km, excluding any land acquisition costs. While the intention is to fund these highways off-balance sheet (not consolidated), raising debt funding for highways can prove challenging and/or expensive in a post-pandemic paradigm.

Property development

While construction is poised to hold the spotlight, the group’s property segment is an integral part of our thesis. We forecast a 55% GP CAGR (FY24-27) on the back of RM1.8bn GDV of launches over the next 2 years. For context, LSH Capital is currently only sitting on unbilled sales of RM120m only.

The property development segment also boasts fairly healthy margins of 38% on average over the past two years and management is guiding for >30% margins going forward. This can be achieved because the construction is undertaken in-house (no revenue on construction recognized here for the group) with an emphasis on deploying surplus construction assets and minimizing requirement for new assets.

Additionally, the group has historically taken an asset-light approach for property

development, with a preference to develop land that is owned by a partner.

LSH Capital is also focused on mass-market segments, typically launching at around RM450-750k per unit. In turn take-up rates have generally been able to hit ~90% with the final portion typically limited to the Bumiputera units.

Property development launch pipeline

Looking ahead

LSH Capital will pivot to a relatively more capital-intensive approach going potential injection of LSH Bund land as well as acquisition of land in Southern Selangor. Additionally, the aforementioned bull case construction project will also provide some ~28 acres of development land (debt-funded) that will weigh on the group’s balance sheet. All in, this should result in lower margins for the segment going forward, and we have assumed it will ease to ~35% going forward.

However, it is worth noting that management is not positioning the property development segment as a high compounding growth segment. Rather, the strategy is to launch about one project a year and maintain a more digestible scale that will preserve margins. In short, LSH Capital isn’t chasing scale or volumes for this segment at the expense of profitability. Instead, the property development segment is positioned as strategically complimentary to the construction segment.

Next up, Lake Side Homes

Lake Side Homes is the next project slated for launch (end-2025) with a GDV of RM1.15b and a projected gross margin of 32.2%. Preliminary construction work is already underway.

It will be a combination of a condominium and an affordable housing project. The condominium portion will have 1,183 units while there will be 1,186 units of affordable housing.

Condominium pricing will range from RM400k-RM2mil, for 956-1,834sqft units. Affordable housing units will be priced around RM300k and range from 869- 1,012sqft in size.

Lake Side Homes - to launch by end-2025

Facilities management

LSH Capital earlier this year on 1 April bagged a 20-year concession to operate and

manage the iconic Kuala Lumpur landmark, KL Tower.

The 70%-controlled concession gives LSH Capital all ticketing sales, less a 15% concession payment off the top to the government. It comes with an obligation to rejuvenate and enhance the tower as well as the surrounding 10acres, to elevate the tower as a tourist destination.

LSH Capital is proposing enhancements not only to the tower, but to the surrounding land, which include new ancillary buildings and retail spaces.

Overall, this segment offers a relatively high margin recurring income stream for LSH Capital.

Key details:

- Management is estimating a total capex of RM70m over the next 3-5 years for KL tower, primarily to upgrade the tower’s four lifts which are currently imposing a limitation of capacity. Once all lifts are upgraded, it would boost capacity by +25% in ~2029. This capex can also be booked as external revenue by the construction segment.

- Management is projecting ticketing sales of ~RM70m annually. For 3QFY25 (ended-June) the group already booked RM12.1m in revenue before major enhancements.

- Gross margins (including government’s 15% take) was 63% in 3QFY25, and management is guiding that it will sustain around the 60% level going forward. In turn, we model this could generate ~RM40m gross profit for the group annually, within the forecast period before the elevator enhancements are completed.

Artists' impression - proposed new ancillary buildings

Valuation methodology - PER

Given the rapid change in the group’s revenue composition, as well as the potential

variability to prospective projects (both construction and property), we opted for a PER valuation methodology over an SOP that includes long-run discounted cash flow modelling for the facilities management segment and revised net asset value (RNAV) for the property development segment.

We also opted to apply a two-year forward PER with FY27E (September 2027) as the base year for our valuation. Note that with the September financial year end, the stock is already in FY26. Additionally, construction projects secured in the coming 12 months will only begin to contribute to earnings in FY27; in turn, FY26E would have under-represented the groups profitability.

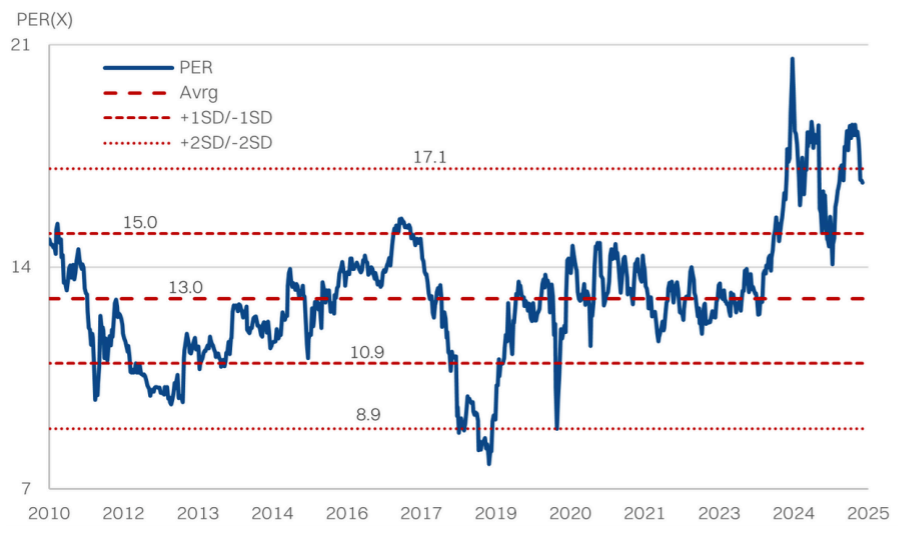

For the target PER multiple, we opted for 13x. This is the average long-run PER for the benchmark FBM KL Construction Index (KLCON). We opted to apply the KLCON as LSH itself only having been listed on the ACE market earlier this year does not have a sufficient historic PER range as a reference.

For context, the trailing 3-year and 5-year average PER for the KLCON is 15.1x and

14.4x, as the sector is currently trading above the historic average. Thus, the 13x target multiple we have applied is relatively conservative, which balances against our punchy earnings expectations.

Valuation methodology - PER

PER Bands

KL Construction Index - long-run PER bands

KL Construction Index - 3yr bands

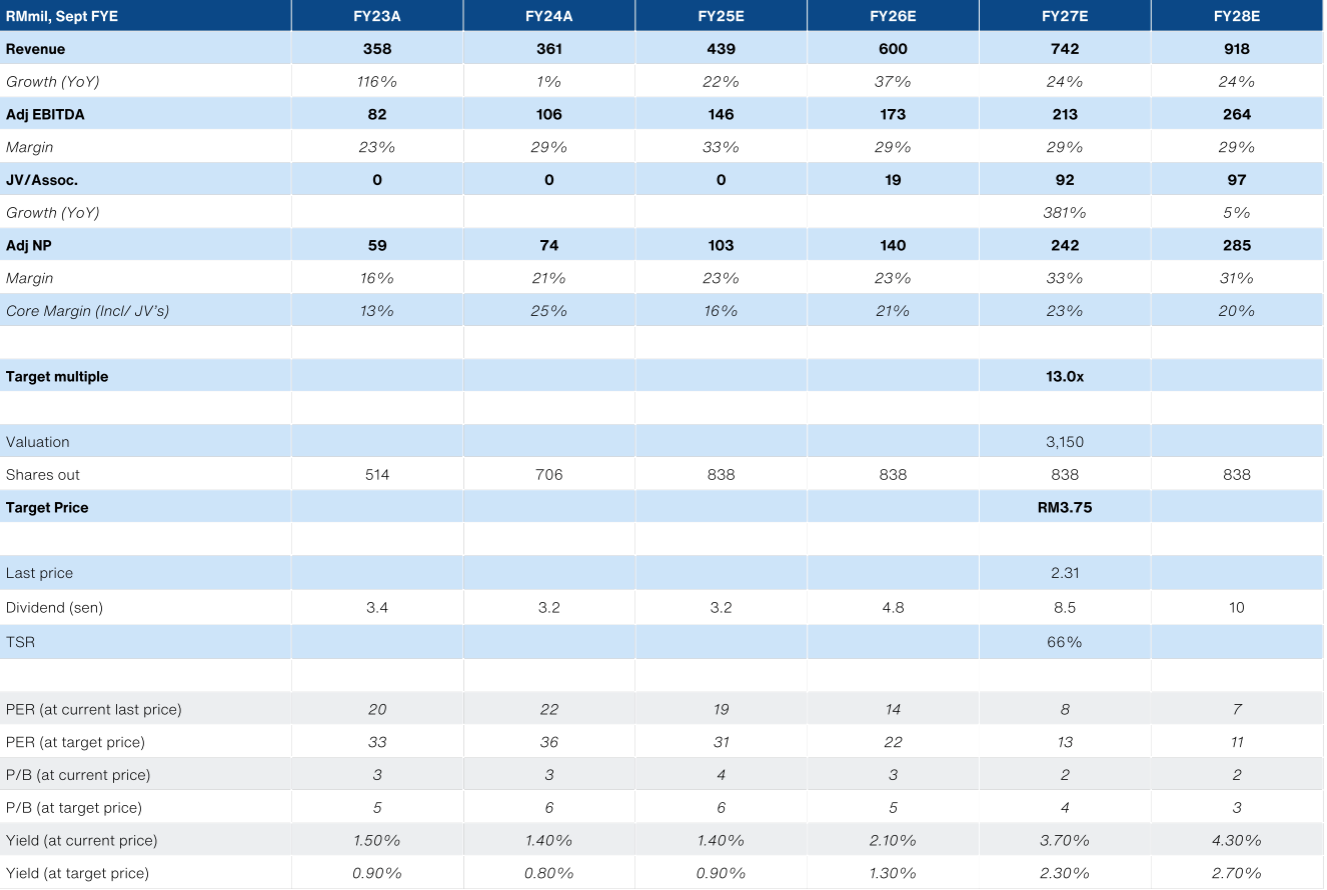

Bull case fair value - RM3.75

Our bull case fair value stems from a potential land swap construction project that is worth potentially RM600m. This relates to a proposed construction of a university campus related to the healthcare sector. The consideration for the construction will be a piece of land, that the group will deploy for development.

We estimate at 8% lift to FY27E earnings from the bull case scenario, which translates to a higher fair value of RM3.75 on an unchanged target multiple of 13x. This is still relatively conservative as it overlooks the further LT value from the development of the land.

Bull case FV

Company background

The story of Lim Seong Hai Capital Berhad (LSH Capital) began in 1966, when the late Lim Seong Hai founded Lim Seong Hai Construction and Companies, a small Class D contractor specialising in building and civil works. Over the next five decades, the Lim family gradually expanded the business into related sectors, building a strong presence in Malaysia’s construction and building-materials supply chain.

In 1995, the group established LSH Lighting Sdn Bhd, focusing on lighting and

mechanical and electrical (M&E) products. Four years later, in 1999, it founded Knight Auto Sdn Bhd, which has since become a well-known distributor of tools, machinery, and construction equipment nationwide. These two businesses formed the foundation of the group’s early success and reputation for reliability within the industry.

To consolidate its growing operations, the family incorporated Lim Seong Hai Capital Sdn Bhd on 11 November 2020, serving as the holding company for its expanding portfolio of construction-related businesses. The company was later converted into a public limited company and renamed Lim Seong Hai Capital Berhad on 21 May 2021.

LSH Capital achieved a major milestone when it listed on the LEAP Market of Bursa Malaysia on 30 July 2021, marking its first step into the capital markets. At the time, the company’s focus was primarily on building materials, lighting, and machinery trading through subsidiaries LSH Lighting and Knight Auto. The listing allowed the group to formalise its structure, improve transparency, and prepare for future growth.

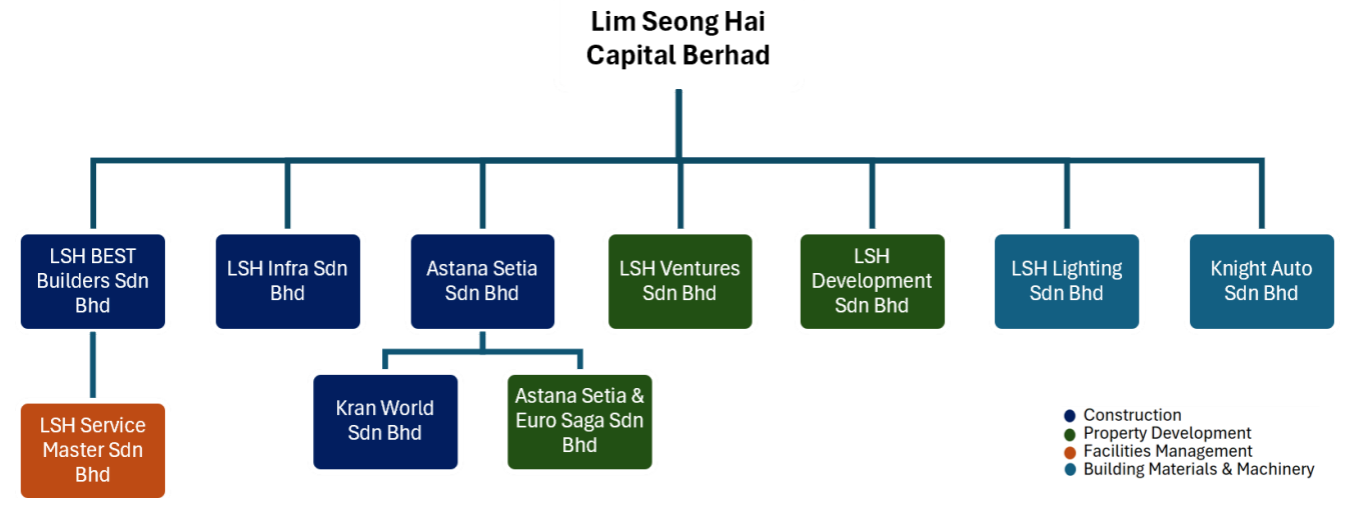

Between 2022 and 2024, the group began an active diversification phase, acquiring LSH Best Builders Sdn Bhd, Astana Setia Sdn Bhd, and LSH Ventures Sdn Bhd. These acquisitions expanded LSH Capital’s reach into construction, engineering, and property development, transforming the company from a trading-based business into a fully integrated construction group with end-to-end project capabilities.

On 21 March 2025, LSH Capital successfully transferred its listing from the LEAP

Market to the ACE Market of Bursa Malaysia.

LSH Capital's corporate structure

Key management

Tan Sri Datuk Seri Lim Keng Cheng

Non-Independent Non-Executive Chairman

Tan Sri Datuk Seri Lim Keng Cheng (age 62) was appointed as Non-Independent Non-Executive Chairman of LSH Capital on 11 November 2020. He brings more than 40 years of experience in construction, property development, and civil-engineering projects in Malaysia. He previously served as Managing Director of Ekovest Berhad, where he spearheaded large-scale projects including the Duta–Ulu Klang Expressway (DUKE) and the Kuala Lumpur River City development. Tan Sri Lim has also been involved in numerous public-private partnerships and major infrastructure concessions. He currently provides strategic leadership and governance oversight to the LSH Capital Group, drawing upon his deep industry experience to guide business direction and policy. He is the elder brother of Datuk Lim Keng Guan and Lim Keng Hun, and Lim Pak Lian, as well as the father to Lim Ding Shyong.

Datuk Seri Lim Keng Guan

Executive Vice Chairman

Datuk Lim Keng Guan (aged 60) was appointed as Executive Vice Chairman on 11

November 2020. He has more than 30 years of experience in property development and construction, spanning civil-engineering works, design-and-build projects, and project management. He previously held senior roles at Iskandar Waterfront Holdings Sdn Bhd and Iskandar Waterfront City Berhad, and co-founded ASSB Sdn Bhd, which has grown into one of LSH Capital’s key subsidiaries specializing in engineering and property development. Datuk Lim Keng Guan oversees the group’s overall operations and construction delivery functions, ensuring quality and efficiency across its projects. He is the brother of Keng Cheng, Keng Hun, and Pak Lian, as well as the uncle to Ding Shyong.

Lim Pak Lian (Jaclyn)

Group Managing Director

Lim Pak Lian (aged 59) was appointed as Group Managing Director on 11 November 2020. She possesses over 25 years of experience in the building-materials and construction-related industries, including distribution and retail of lighting, electrical, and hardware products. She founded LSH Lighting Sdn Bhd in 1995 and co-founded Knight Auto Sdn Bhd in 1999, which together form the foundation of the group’s Construction Products Division. Her leadership has been key to expanding LSH Capital’s business into property development and engineering solutions. She currently oversees the group’s strategic planning, diversification initiatives, and business development activities. She is the sister of Keng Cheng, Keng Guan and Keng Hun, as well as the aunt of Ding Shyong. Additionally, the group’s chief legal officer, Lor Kar Mun is the daughter of Pak Lian.

Lim Keng Hun

Director - Machinery, Hardware & Tools Division

Lim Keng Hun (aged 57) was appointed as Managing Director of the Machinery,

Hardware & Tools Division on 11 November 2020. He has more than 30 years of experience in the trading and rental of construction machinery, hardware, and tools. He co-founded Knight Auto Sdn Bhd in 1999 and oversees its nationwide retail operations, which supply industrial equipment, hardware, and engineering tools across Malaysia. Lim Keng Hun manages the group’s logistics and machinery-rental operations, supporting internal construction projects and external clients. He is the brother of Keng Cheng, Keng Guan and brother of Pak Lian, as well as the uncle of Ding Shyong.

Lim Ding Shyong

Executive Director

Lim Ding Shyong (aged 36) was appointed as Executive Director on 6 March 2024. He oversees the group’s construction, engineering, and development operations, focusing on execution and project management. He holds a Bachelor of Engineering and a Master of Science in Construction Management from King’s College London. Before joining LSH Capital, he accumulated over 12 years of experience in construction and property development, including involvement in large-scale infrastructure projects. At LSH Capital, Lim Ding Shyong plays a key role in advancing the group’s technical capabilities and operational efficiency. He is the son of Keng Cheng, and the nephew of Keng Guan, Keng Hun and Pak Lian.

Shareholding breakdown