Pan Merchant

PMI specializes in manufacturing filter presses for liquid-solid separation. The primary application for the presses is in edible oils, and mainly for crude palm oil processing.

PMI specializes in manufacturing filter presses for liquid-solid separation. The primary application for the presses is in edible oils, and mainly for crude palm oil processing. The secondary application is within waste management, including water treatment as well as mining. This gives PMI potential as an ESG play. PMI is primarily an exporter, with over 85% sales coming from abroad, including countries like Indonesia, Europe, and US.

About the stock

PMI was listed on the ACE market in June 2025, with the retail portion undersubscribed at only 37% taken up. It remains controlled by the founders'

family - which also control the board and management. PMI is a Syariah-compliant stock.

Investment thesis

PMI is well positioned to capitalize on the development of domestic water

treatment projects in Selangor and other states - supplying press filters for waste management. Each phase (there are two) will require ~RM50 worth of filter press (based on projects of similar scale), or ~20% upside to baseline revenue run-rate. Placement of underwritten shares from IPO will also provide a liquidity event.

Key risks

- PMI has some customer concentration risk, with over almost 70% of revenues coming from its top 4 customers. PMI is mitigating this risk via diversification into other customers and segments.

- PMI could face competition from Chinese firms in the future. It is reliant on long-standing relationships with customers in the edible oils segment, and proven track-record to fend-off competition.

- Founders/shareholders control most key management positions via family members. This could pose governance, succession planning, and talent development risks.

Stock information

Pan Merchant

PMIBHD - 0361.KL

BUY

Target price: RM0.30

Last price: RM0.215

Market cap (RMm): RM1,97m

Shares out: 916m

52-week range: RM0.185 / RM0.26

3M ADV: RM0.02m

T12M returns: -20%

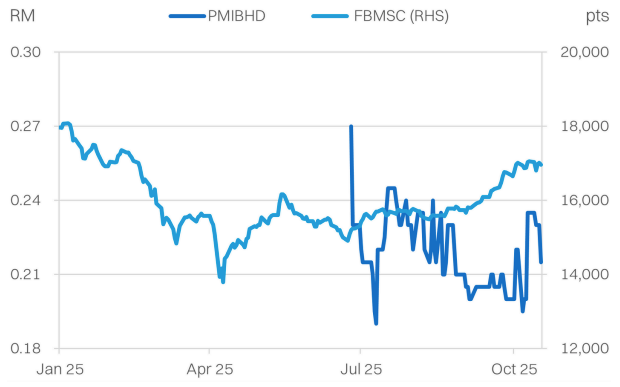

Share price performance

Investment fundamentals

| RMm | FY24A | FY25E | FY26E | FY27E |

|---|---|---|---|---|

| Revenue | 142 | 140 | 183 | 176 |

| Revenue YoY | 2% | -1% | 31% | -4% |

| Adj PATAMI | 10.2 | 8.1 | 15.3 | 12 |

| Adj PATAMI margin | 7% | 6% | 8% | 7% |

| DPS (sen) | - | 0.2 | 0.7 | 0.5 |

| ROA | 7% | 6% | 9% | 7% |

| ROE | 14% | 10% | 16% | 12% |

| PER | 18 | 22.7 | 12 | 15.3 |

| P/BV | 2.5 | 2.3 | 1.9 | 1.8 |

| Yield | 0% | 1% | 3% | 3% |

| Net debt/equity | -13% | 0% | -13% | -9% |

Source: Company data, NPS Research, October 2025

Disclaimer: By using this information, you hereby acknowledge that you are fully and solely responsible for evaluating the merits and risks of any investment decision and agree not to hold NewParadigm Research fully liable whatsoever for any actions, omissions and/or damages of any kind or matter arising from such decision.