Water project wins can reverse soft debut

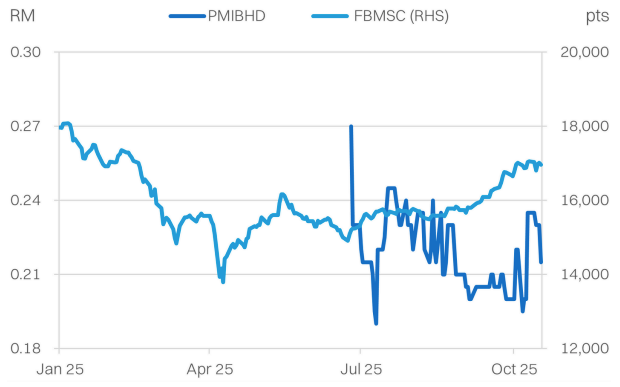

PMI has not put its best foot forward post-listing, touching a low of -33% vs IPO price and posting sluggish 1H25 earnings.

Stock information

Pan Merchant

PMIBHD - 0361.KL

BUY

Target price: RM0.30

Last price: RM0.215

Market cap (RMm): RM1,97m

Shares out: 916m

52-week range: RM0.185 / RM0.26

3M ADV: RM0.02m

T12M returns: -20%

Disclaimer: By using this information, you hereby acknowledge that you are fully and solely responsible for evaluating the merits and risks of any investment decision and agree not to hold NewParadigm Research fully liable whatsoever for any actions, omissions and/or damages of any kind or matter arising from such decision.

Key points

- RM400m tenderbook, including RM200m in water projects will be catalyst for rerating. 2H25 earnings to bounce back as well.

- We estimate 32m in shares underwritten from the IPO, could offer a liquidity event for investors to accumulate a position.

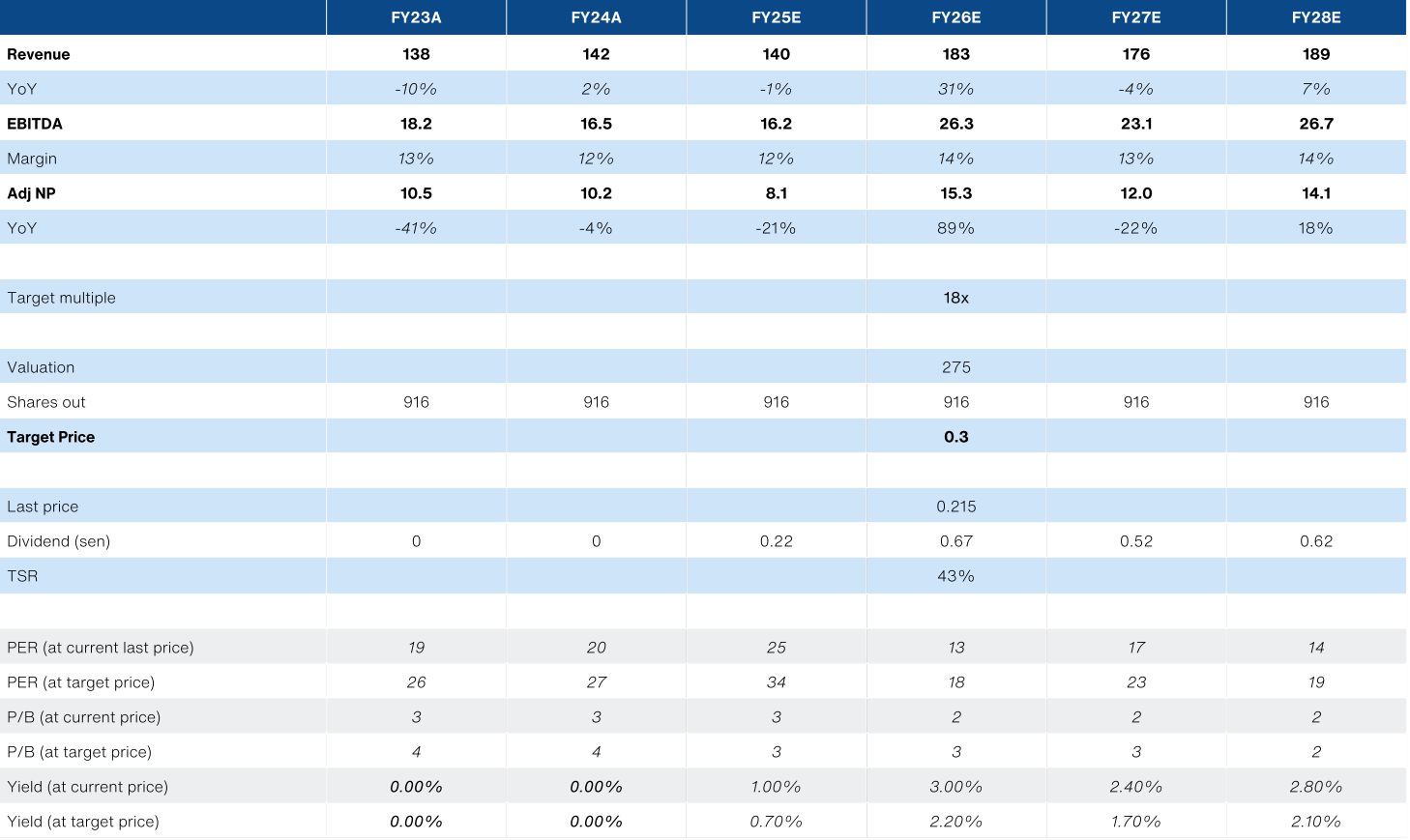

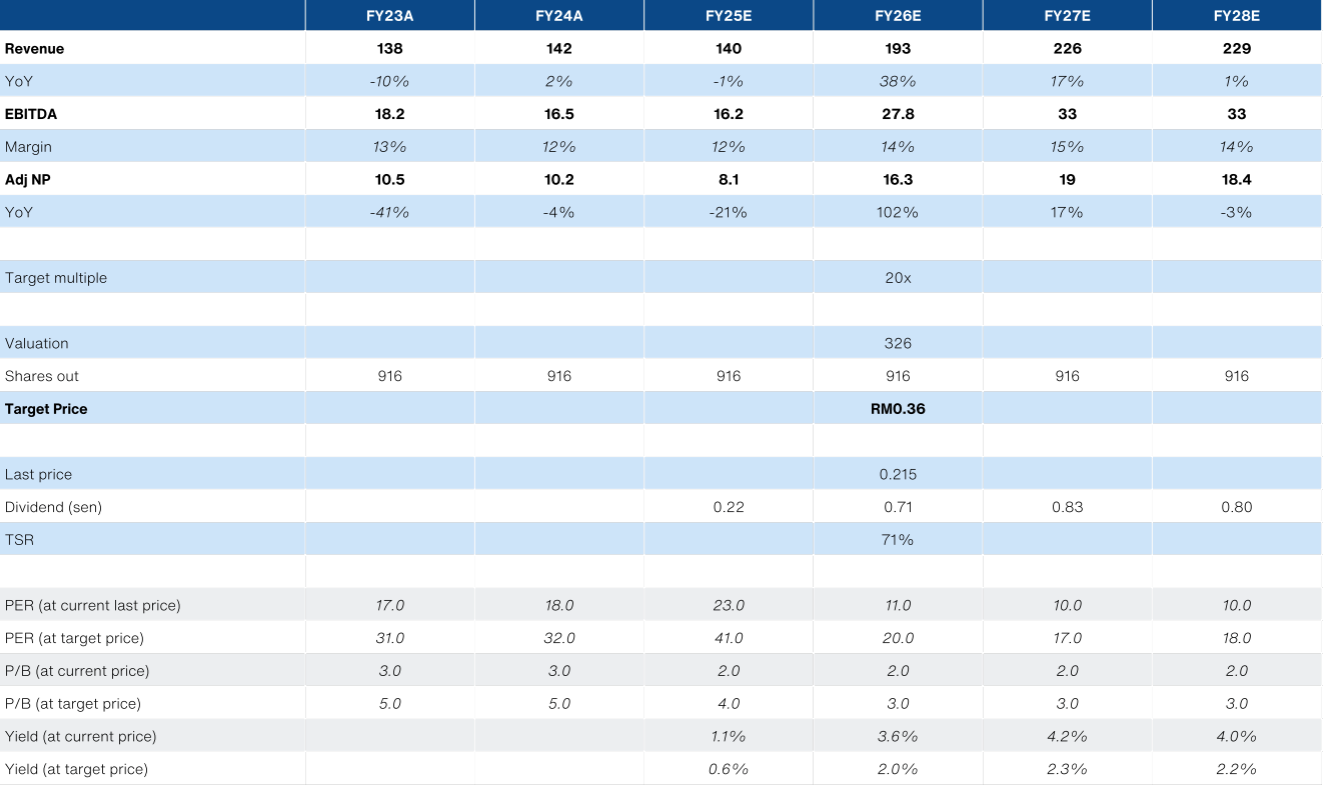

- Initiate with a BUY. Our RM0.30 TP is pegged to 16x FY26 earnings. Our RM0.36 bull case FV assumes a RM100m HK water project win.

Share price performance

Investment fundamentals

| RMm | FY24A | FY25E | FY26E | FY27E |

|---|---|---|---|---|

| Revenue | 142 | 140 | 183 | 176 |

| Revenue YoY | 2% | -1% | 31% | -4% |

| Adj PATAMI | 10.2 | 8.1 | 15.3 | 12 |

| Adj PATAMI margin | 7% | 6% | 8% | 7% |

| DPS (sen) | - | 0.2 | 0.7 | 0.5 |

| ROA | 7% | 6% | 9% | 7% |

| ROE | 14% | 10% | 16% | 12% |

| PER | 18 | 22.7 | 12 | 15.3 |

| P/BV | 2.5 | 2.3 | 1.9 | 1.8 |

| Yield | 0% | 1% | 3% | 3% |

| Net debt/equity | -13% | 0% | -13% | -9% |

Source: Company data, NPS Research, October 2025

Expanding beyond edible oil filtration

- PMI has not put its best foot forward post-listing, touching a low of -33% vs IPO price and posting sluggish 1H25 earnings. However, the low expectations set the stage for substantial +43% upside to our initiation target price of RM0.30

- The primary catalyst for our thesis is the potential award of up to RM100m of domestic water treatment related filtration works in Malaysia. We believe the project in question is Rasau Water Treatment plant in Selangor, that is now slated for completion by end-2026. We forecast a +31% revenue growth and an +89% growth for PATAMI for FY26E, if phase 1 of this project is secured. We expect the project to be awarded within the next 3-6 months.

- This breakout win in water projects will justify a re-rating in our view for the stock, to at least 18x FY26E PER. Currently, it could be argued that PMI’s valuations are dragged down to a lower benchmark of other palm oil-related industrial peers that tend to be in low at ~9x PER. However, global filtration peers trade at ~18x.

- The aforementioned contract win will lend credibility to PMI’s growth plans that are predicated on expanding non-palm oil related revenues across water, mining, sustainable fuels and waste management.

- Keep in mind, that PMI boasts a nearly 3-decade track record with key customers, primarily as an exporter, and has previously won similar water project works in Singapore.

- Meanwhile, the bull case scenario for the stock hinges on bagging a further RM100m water contract in Hong Kong (6-12 months award horizon), that would translate to a fair value of RM0.36 per share.

- Liquidity event: We estimate ~3% of the IPO shares that were underwritten have yet to be sold down by the underwriter. This could present a buying opportunity when said block comes to market.

Filter out the disappointing start

- Contract wins are the primary catalyst for the stock. Potential water infrastructure investment thematic beneficiary, longer term.

- 2H25 earnings will see rebound, but high earnings growth due in FY26E.

- Initiate PMI with a Buy recommendation and a target price of RM0.30.

About the company

PMI specializes in manufacturing filter presses for liquid-solid separation. The primary application for the presses is in edible oils, and mainly for crude palm oil processing. The secondary application is within waste management, including water treatment as well as mining. This gives PMI potential as an ESG play. PMI is primarily an exporter, with over 85% sales coming from abroad, including countries like Indonesia, Europe, and US.

About the stock

PMI was listed on the ACE market in June 2025, with the retail portion undersubscribed at only 37% taken up. It remains controlled by the founders'

family - which also control the board and management. PMI is a Syariah-compliant stock.

Investment thesis

PMI is well positioned to capitalize on the development of domestic water

treatment projects in Selangor and other states - supplying press filters for waste management. Each phase (there are two) will require ~RM50 worth of filter press (based on projects of similar scale), or ~20% upside to baseline revenue run-rate. Placement of underwritten shares from IPO will also provide a liquidity event.

Key risks

- PMI has some customer concentration risk, with over almost 70% of revenues coming from its top 4 customers. PMI is mitigating this risk via diversification into other customers and segments.

- PMI could face competition from Chinese firms in the future. It is reliant on long-standing relationships with customers in the edible oils segment, and proven track-record to fend-off competition.

- Founders/shareholders control most key management positions via family members. This could pose governance, succession planning, and talent development risks.

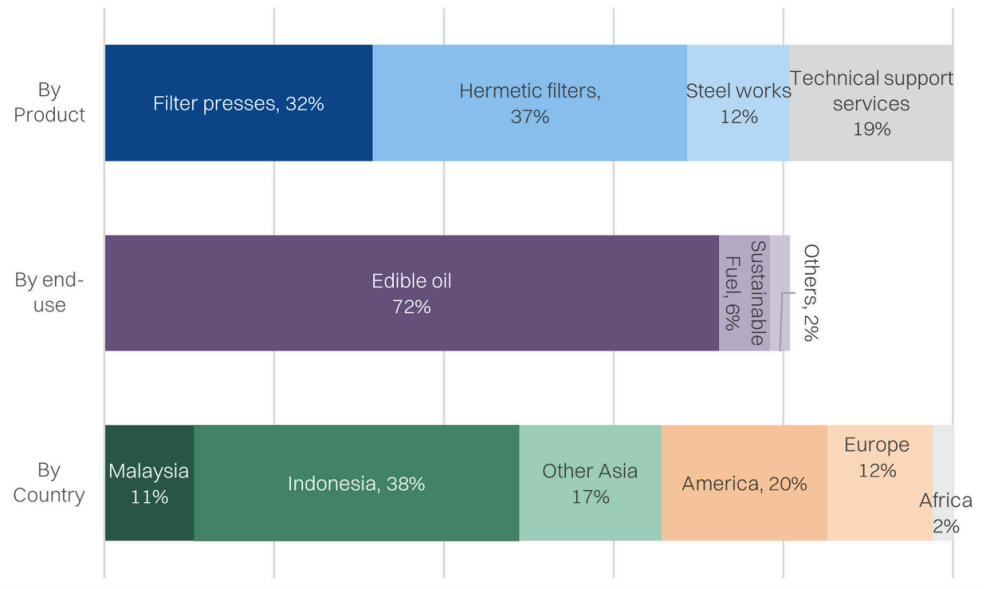

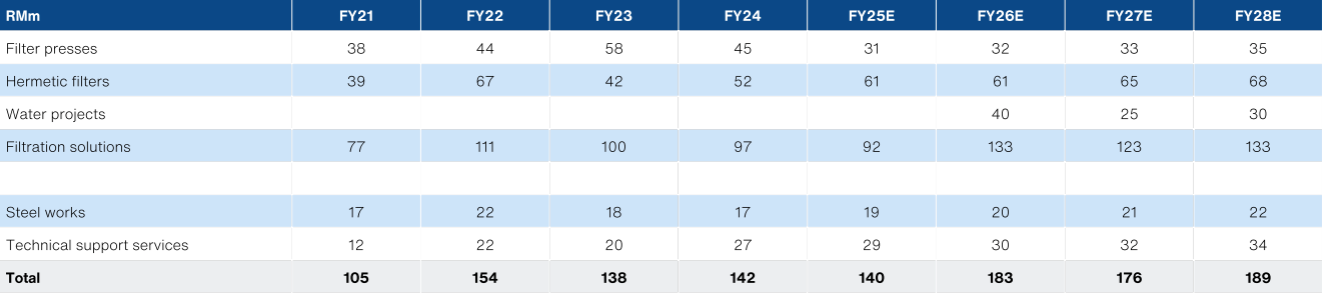

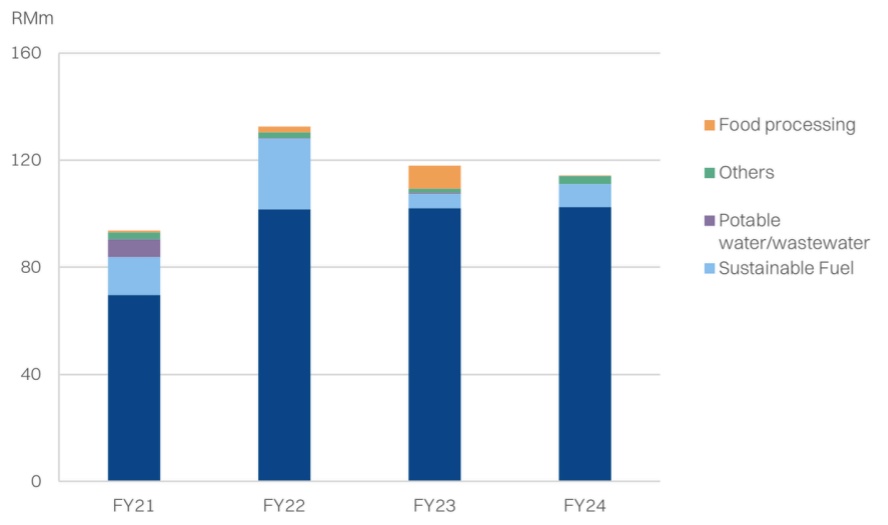

Revenue composition

Investment thesis: Water project wins to drive earnings and re-rating

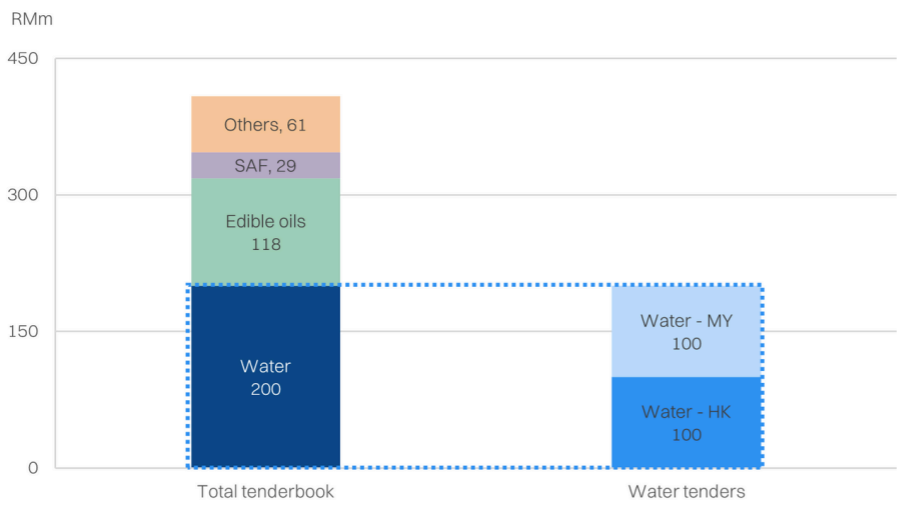

PMI has a tenderbook of over RM400m, but the current share price and valuations

suggest that market is overlooking meaningful project wins. For comparison, PMI has an underlying revenue run-rate of ~RM140m and an orderbook of ~RM70m.

Roughly half the tenderbook (RM200m) pertains to water projects, of which half is

based in Malaysia and half overseas. We believe some of the key projects that PMI is bidding for onshore are related to the Rasau Water Treatment Plant in Selangor. Given the two phases, we anticipate each project award could be ~RM50m, based on projects of similar scale and complexity.

Rasau’s construction was halted in September 2024, due to the collapse of an

embankment. However, works have resumed as of October 2025 and the project’s

slated completion date has been announced as end-2026. Assuming PMI needs 9-12 months for production of the filter presses for its portion of the project, we estimate contracts will need to be awarded in the coming months.

The filter presses that PMI is looking to supply are designed to help dewater sludge

waste, a by-product of water treatment. In short, this should be seen as a waste

management project.

Critically, PMI enjoys relatively high operating leverage to incremental sales. We

estimate that marginal sales above the current RM140m run rate should translate to a high-teens net margin (on incremental sales) compared with the current rate of ~6-7%. In turn, we forecast FY26E revenue growth of +31% YoY but a PATAMI growth of +89% YoY.

Additionally, we see this as a re-rating catalyst. The market should shift its perception of PMI as relatively stable edible oils play towards a waste-management proxy that has more explosive project-based growth.

Secondary to the water project wins, we also expect a 2H25 rebound in earnings from the low-base 1H25 slump. We peg PMI’s valuation at 18x FY25E Adj NP of RM15.3m (+89% YoY) for a target price of RM0.30/share. this implies 43% TSR.

Bull case fair value: RM0.36

Looking beyond Rasau, PMI is also bidding for a similar RM100m project in Hong Kong. We have excluded this in our base-case valuation. If secured, we estimate a fair value of RM0.38 on 20x FY26E. However, note that the bulk of the earnings accretion from this project should only materialize in FY27E, against which our bull case FV would have an implied valuation of 14x.

Valuation

We applied a PER target of 18x on FY26E earnings to derive our target price of

RM0.30. This implies a +29% TSR. We think this multiple is reasonable given the

~77% PATAMI jump in FY26, from the water project in Malaysia. Additionally, we think this maiden win will also improve expectations of future contract wins as well.

Against relative peer comparison, 18x PER is in-line with global filter press peers. While this runs above the domestic palm oil equipment supplier peers (~9x T12M PER), it is broadly in-line with other metal fabricators (18x T12m).

Thus, we anticipate the water project award will help PMI shed the low multiple

associated with edible oils and be re-rated as a fabricator of waste management related equipment.

Valuation

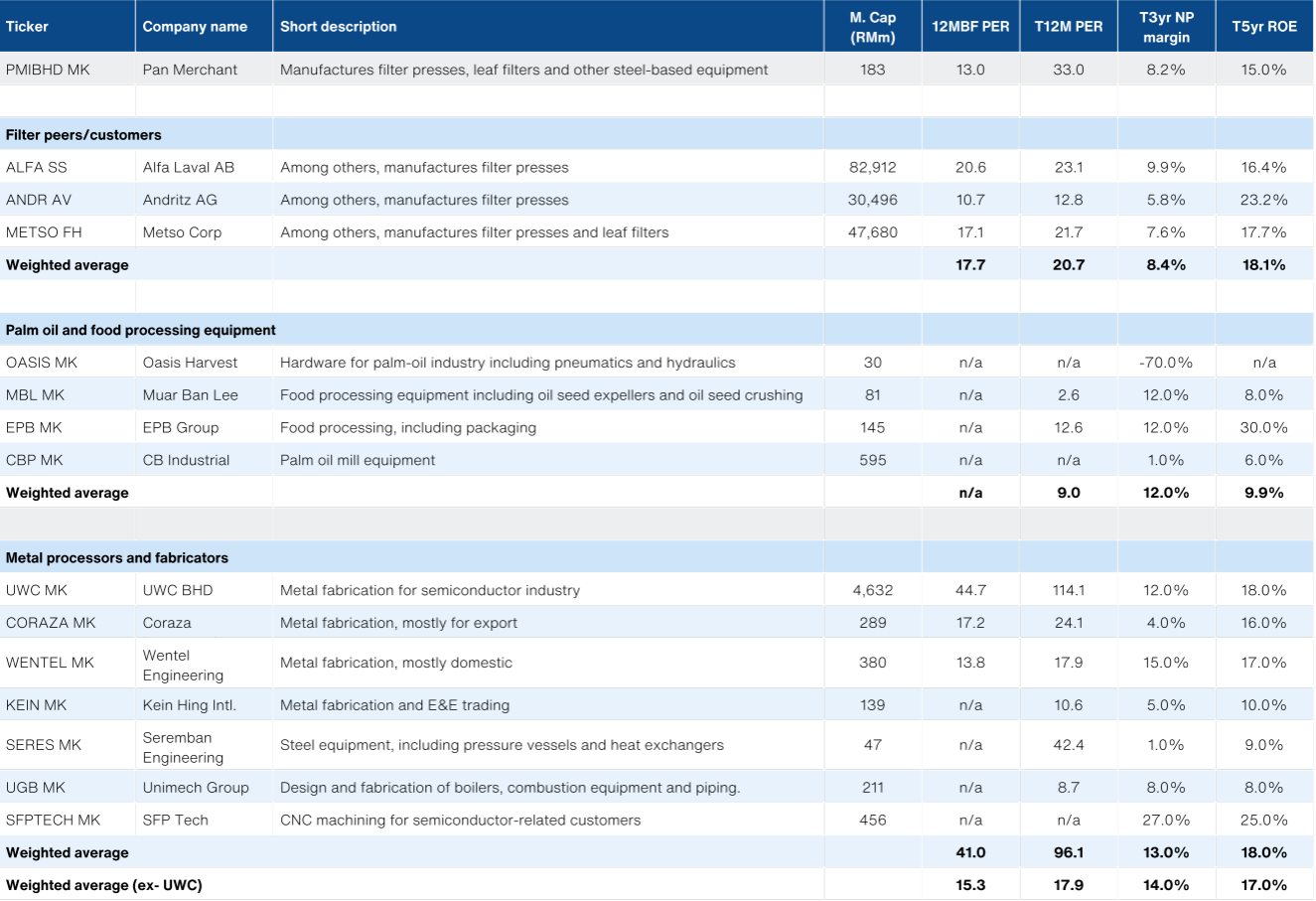

Peer comparison

With limited listed track record, PMI has little valuation information to benchmark against. Instead, we look to peer valuations. There are no meaningful direct comps in Malaysia. Companies that are directly in the filter segments include Alfa Laval, Andritz and Metso - which double as both customers and suppliers. Valuations for this group are around 18x forward PER

Domestic peers that could be comparable would be those that supply equipment to the palm oil industry. The average PER multiple for this group is about 9x trailing.

Lastly, the broader metal fabricators in Malaysia have an average forward PER of 41x, but excluding outliers like UWC, the average is 15x forward. However, given limited forward forecasts for this group, the T12M 18x PER is a better benchmark.

Peer comparison

Bull case fair value

Our bull case scenario for PMI is for the award of a RM100m water project in Hong Kong. The bulk of the earnings should materialize in FY27, with an estimated 2-year recognition window.

This project win should add +7%/+59%/+30% respectively to FY26/27/28E

earnings, with PATAMI slated to double by FY26E. We have assumed an s-curve

revenue recognition

In turn, we have also assumed a higher target multiple of 20x on FY26E, given that the bulk of the earnings upside is loaded to FY27. For reference, in our bull case earnings scenario, PMI’s current implied PER is only 10x FY27.

Visibility on the award of this project is limited, but we believe a timeline of 6-12 months for the award.

PER valuation methodology

Water projects driving growth

The key driver for growth in our assumptions arises from the diversification into water projects - roughly RM100m worth over the next 3-4 years, from Malaysia. The application for filters in a water treatment plant is for solid-liquid separation of the sludge waste that is a by-product of the primary water treatment process. In short, it is a waste management application.

We believe PMI is bidding for Rasau Water Treatment Plant in Selangor, which is broken into two phases. We estimate each phase will have a contract value of ~RM50m. The project has been delayed by over one year, after an embankment collapsed in 2024 (link). However, Phase 1 is slated for completion by end-26. Working backwards, assuming a 9-12month lead time to build and install the filters, the award needs to be done within the next 3-6 months. Meanwhile, we expect Rasau Stage 2 to be awarded between 2027 and 2028.

Separately, we have assumed the core revenue from edible oils end-segment will

continue to support a ~RM140m underlying run rate, with low single digit growth. These revenue streams primarily come via a few major customers, including Desmet and Lipico. While project-based in nature they have demonstrably stable replenishment rates over the past few years. Our assumptions are supported by the orderbook of RM70m in hand and the non-water tenderbook of RM200m.

Revenue forecasts

Tenderbook composition

Earnings

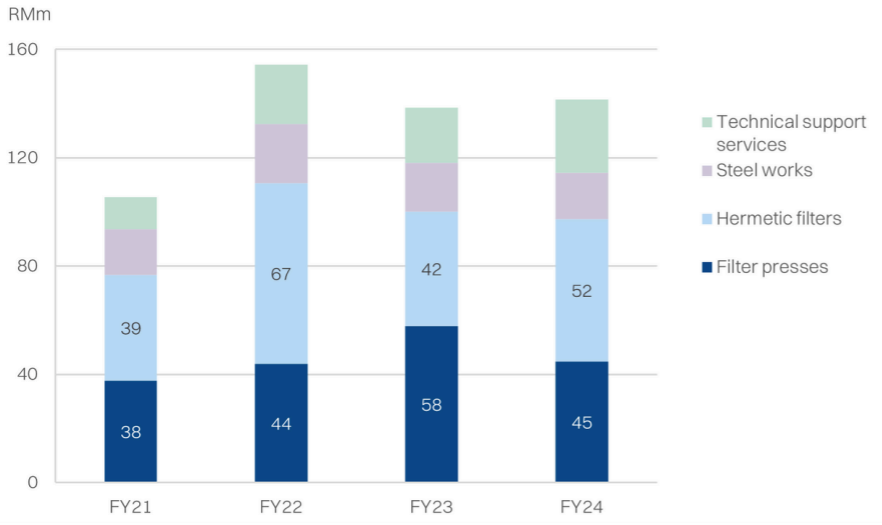

PMI’s revenue can be broken into 4 major segments, by product:

- Filter presses (32%) - low temperature, higher solid content, higher volume

- Hermetic filters (37%) - higher temperature, lower solid content, lower volume

- Steel works (12%) - pressure vessels, heat exchangers, etc.

- Technical support services (19%) - After sales and spare parts.

However, we foresee it may be more useful to think about PMI in terms of the end-markets that it serves:

- Edible oils (90%) - Primarily palm oil but also other seed oils in US.

- Sustainable fuels - Sustainable aviation fuels, biodiesel production.

- Potable water/waste water - Municipal water and filtered industrial waste.

- Food processing - Sugar and cassava starch.

Revenue by segment

Revenue by end-use (excludes technical support services)

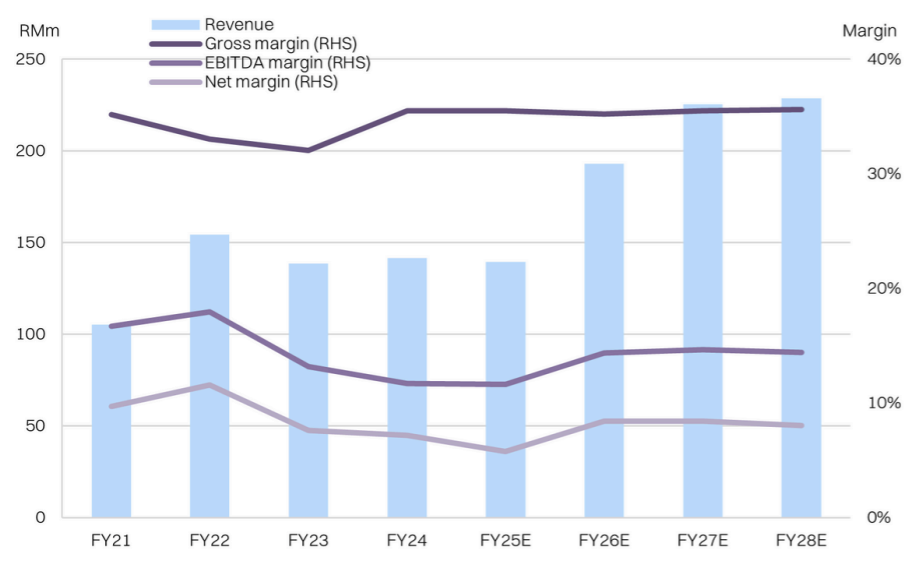

Margins

PMI’s gross margins have historically hovered between 32% and 33.5%. Even in the recent 1H25 underperformance, gross margins held up at 36%, supported by a higher mix of the technical support services segment.

As a gross profit level, the margins appear to be supported by the long-running relationship with customers and the customized nature of PMI’s solutions. This results is less pricing pressure. In fact, most of PMI’s domestic competitors boast lower margins.

However, net margins have softened over the past two years, now headed towards

~6% for FY25, compared with >7% from FY23/24. The margin pressure is arising

from higher staff costs and other start-up costs as the group gears up to expand into new markets and new end-segments.

Nonetheless, with the step up in revenue from the aforementioned RM100m in domestic water segment, we anticipate that margins will be able to recover to ~7% going forward, with further upside if the Hong Kong projects materialize as well.

Looking ahead, PMI has expressed interest to move upstream and venture into R&D and manufacturing of its own filter elements. Currently, it has to purchase said filters from European suppliers, which is a substantial component of COGS. The group is currently prototyping new filter and filter element designs, but will not reach commercial volumes without additional capex investment. If this scales up, it should be accretive to margins.

Margin trends

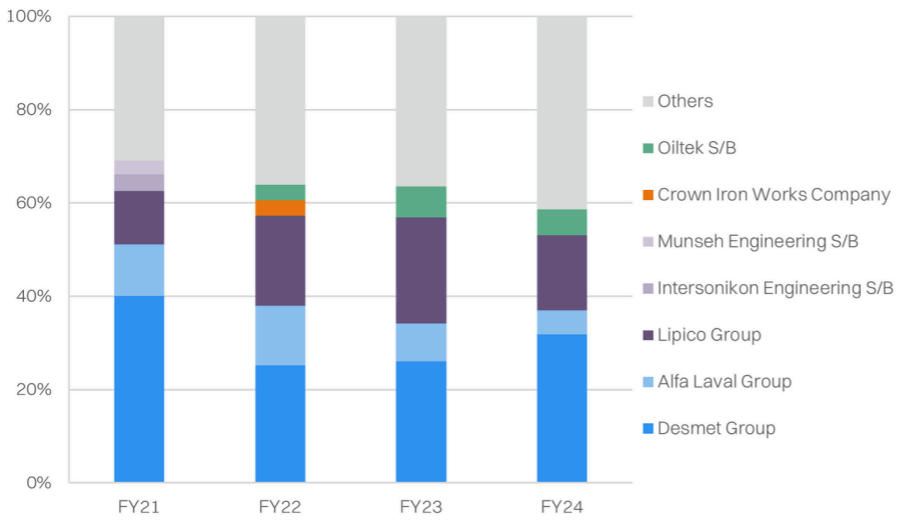

Key customers:

PMI has some customer concentration risk. Its top 3 customers make up >60% of

revenues on average, historically. While the concentration is high, it is worth noting that these are long-standing relationships that go back almost 30 years.

- Desmet Group: 28% of sales (FPE24)

- Headquartered in Belgium, founded in 1946.

- Acquired by Alfa Laval Group in 2022.

- Engineering company that specializes custom-designed plants and equipment for the food, feed, and biofuel industries.

- Procurement from PMI: Edible oil and sustainable fuel industries - filter press, agitators, hermetic filter, vessels, tanks and replacement parts.

- Desmet has a 27year relationship as a customer with PMI.

- Alfa Laval Group: 7.4% of sales (FPE24)

- Swedish engineering company, founded in 1883.

- Listed on Nasdaq Stockholm (ALFA SS).

- Specializes in heat transfer, separation processes (liquid, solids, gasses), and fluid handling. Applications include food, O&G and pharmaceuticals.

- Procurement from PMI: Edible oil and sustainable fuel industries - Filter press, agitators, hermetic filter and replacement parts

- Alfa Laval has a 29 year relationship as a customer with PMI.

- Lipico Group: 26% of sales (FPE24)

- Singapore based engineering firm, founded in 1996

- Focuses on oils and fats processing, oleo chemicals and renewable fuels.

- Procurement from PMI: Edible oil, sustainable fuels and oleochemical industries - filter press, agitators, hermetic filter, vessels, tanks and replacement parts.

- Lipico has a 28-year relationship with PMI.

Revenue breakdown by customer

Sector overview

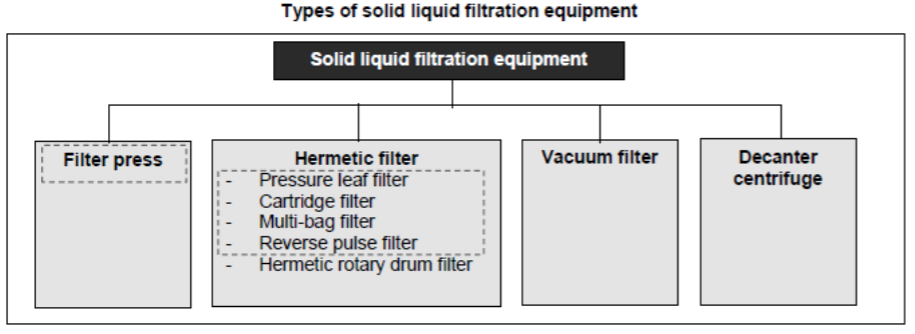

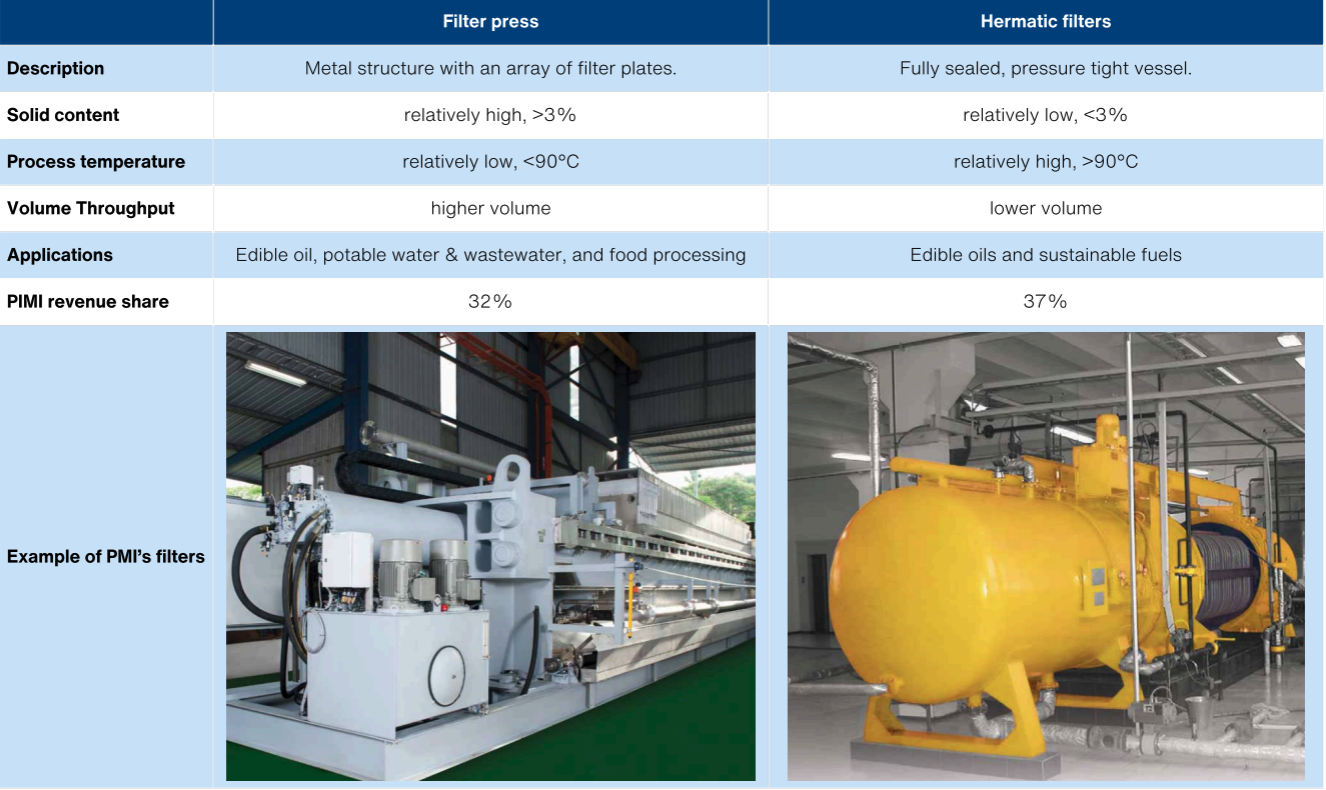

In brief, PMI specializes in filtration equipment for the purpose of separating solids from liquids by applying pressure. This takes the form in either filter presses or hermetic filters. Other filtration types include vacuum and decanter filters.

From the prospectus disclosure, the filter press and hermetic filter industry has an estimated size of US$6.4bn (RM29.3bn) in 2025 and will grow by 10.8% CAGR to US$7.9bn (RM36.1bn by 2027 - based on an independent market research report by PROVIDENCE.

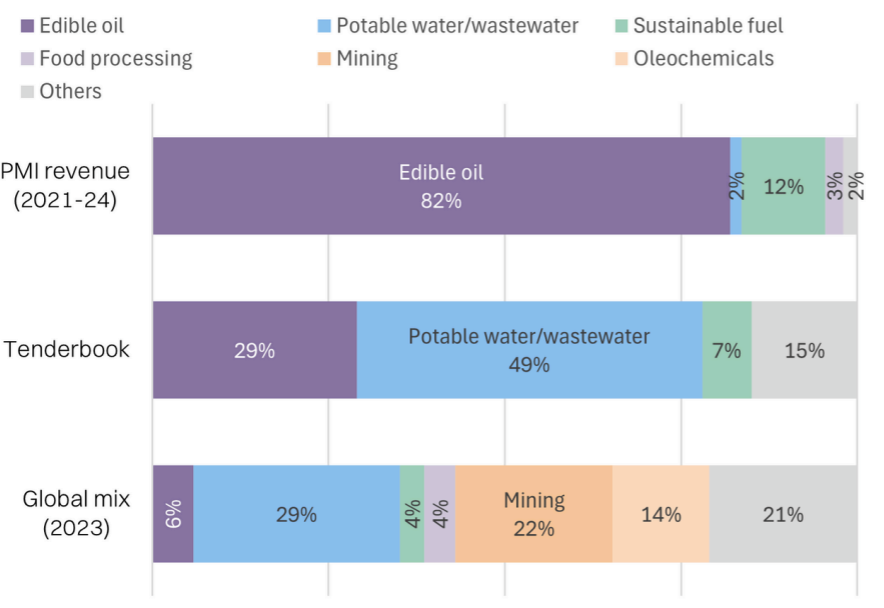

PMI’s segmental focus on edible oils is also not reflective of the broader market demand for said filters, given it is only ~6% of total filter applications (2023) but 82% of PMI’s historic revenue mix. This further underscores the importance of PMI’s diversification into other end-segments.

For context, we estimate that PMI could have high single-digit market share in global edible oil-related filter requirements, but virtually unrepresented in other end-segments. In fact, applications in potable water/wastewater is the single largest end-segment for said filters. And that is the primary growth driver segment for PMI.

Press and hermetic filters - PMI vs global mix

About the filters

PMI supplies both filter presses and hermetic filters to the edible oils industry. However, it is the application of the two technologies is quite different. Filter presses that have the most immediate upside for PMI due to its potential application in waste management for water treatment.

These filters are customized to their specific application and customer requirements. On one hand, this has underpinned PMI’s ability to retain its major key customers over the years - the group has deep understanding of customers’ requirements as well as the proven track-record.

This moat has also hindered PMI’s ability to venture into other applications. However, PMI will not be a complete newcomer. PMI in 2021 delivered filter presses for a water treatment plant in Johor for a Singapore end-user. While a small sample, successful implementation for the Singapore project has been the launchpad for PMI to bid for similar projects in Malaysia - Rasau.

Press filters vs hermetic filters

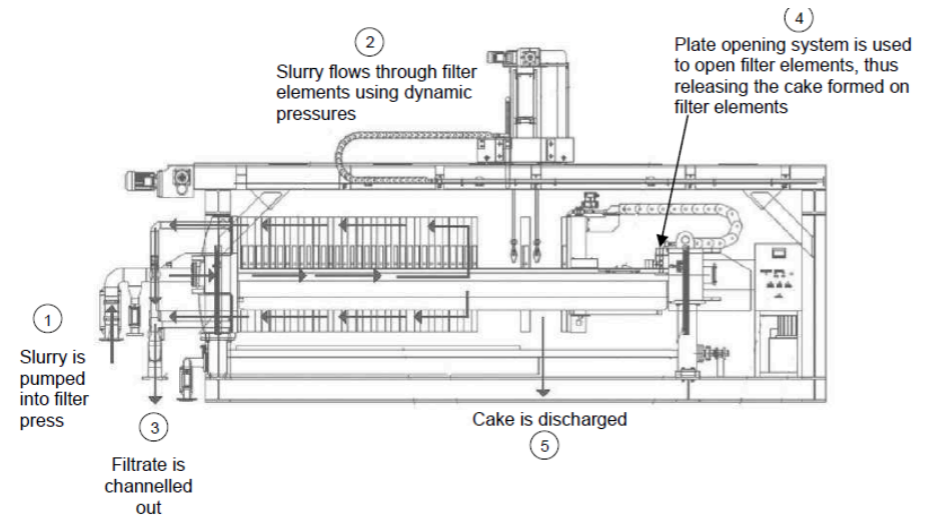

Filter press

A filter press works by pumping slurry in and applying dynamic pressure. This allows an even distribution of slurry over the filter elements. This will allow the trapping and accumulation of solid particles (also known as cake) on the filter elements. The liquid portion or filtrate is channeled out of the press.

The filter elements consist of filter plates - typically cast iron, silumin/aluminum or polypropylene - as well as a filter cloth. The filter cloth is typically made out of

polypropylene, polyester and nylon. The filter cloth will need to be cleaned to maintain filtration performance.

Filter press process:

Waste sludge is a by-product of the water treatment process. The sludge needs to be dewatered to a safe level before it can be disposed in a landfill. A low-cost approach that has been historically adopted in Malaysia is the use of sedimentation ponds. The waste sludge is simply pumped into open ponds and the solids will settle at the bottom over time. While boasting lower up-front capex costs, this approach is slow, inefficient, and susceptible to disruption from heavy rainfall.

Modern water treatment plants cannot rely on sedimentation due to the aforementioned inefficiencies and unpredictability, but also due to rising environmental requirements. Filter presses offer a good value proposition for dewatering sludge at reasonable cost and able to achieve solid content of up to 35%.

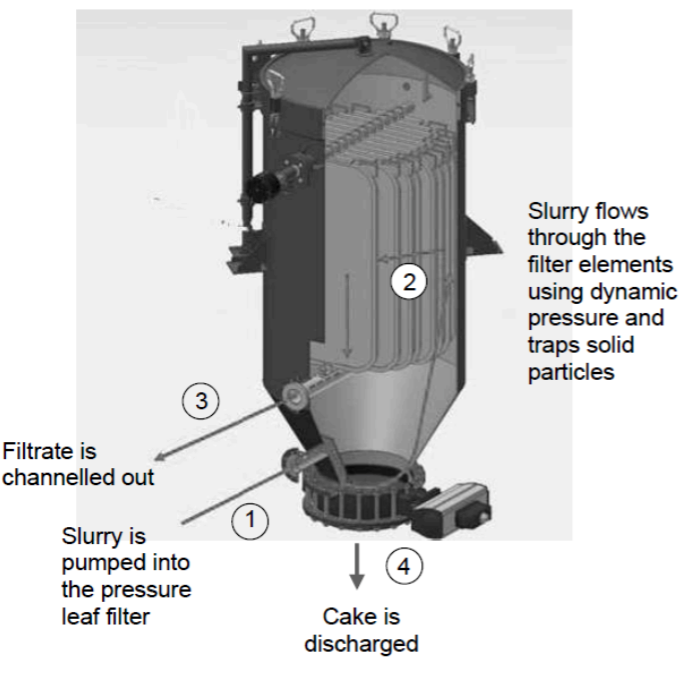

Hermetic filters

As the name suggests, hermetic filters are fully sealed, pressure-tight vessels. It comes in several variations, based on the filters (leaves, candles, bags or cartridges) as well as vertical or horizontal designs.

- Vertical pressure leaf filters: upright cylindrical vessels that allow optimization of floor space. Typically used in bleaching clay filtration in the edible oil industry.

- Horizontal pressure leaf filter: As the name suggests, lies horizontal. Also a cylindrical presure vessel. typically used in winterization of edible oils.

High pressure is applied via a pump - either liquid or compressed gas - within the

pressure vessel to force the slurry to pass through the filter elements. Solid particles are then trapped on the surface of the filter elements, forming a cake while the liquid filtrate passes through.

A vibrator is used to mechanically loosen the cake that accumulates on the filter

elements and the cake is then discharged through discharge valves.

The higher pressure translates to higher operating temperatures for these types of

filters, requiring more robust materials for the filters.

Hermetic filters - vertical pressure leaf filters

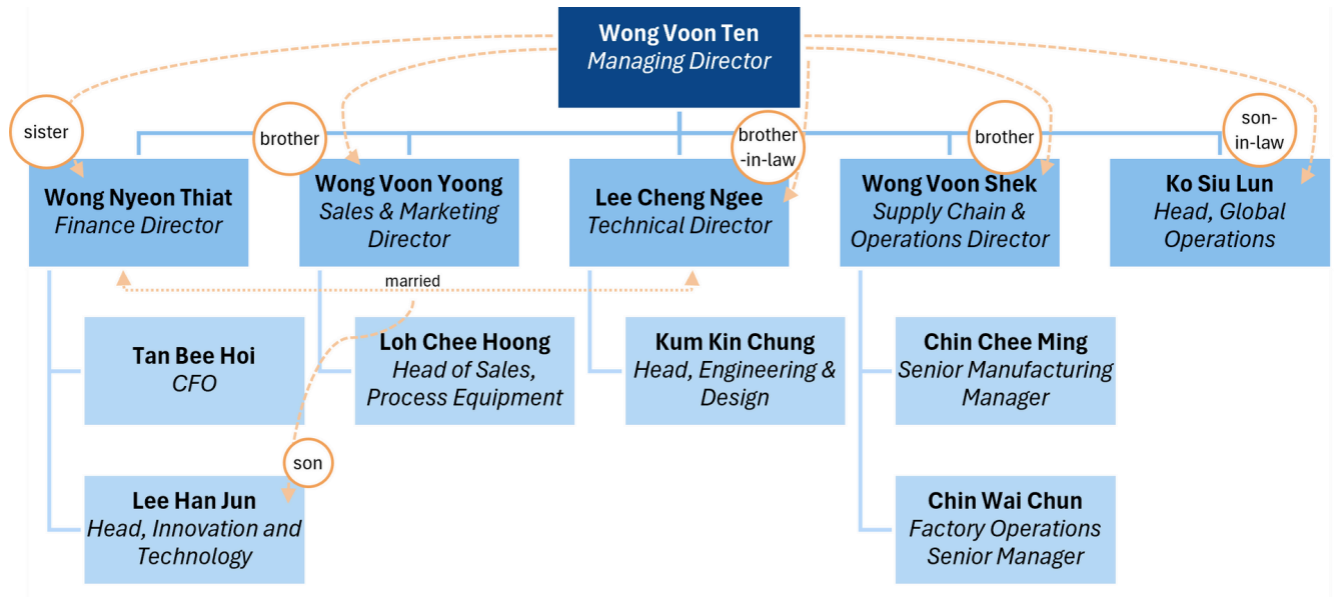

Key management:

PMI is founder managed and owned, with the related family members controlling ~60% of the outstanding shares and holding all the key management positions. On one hand, there appears to be some succession planning in place with second-generation family members involved in the company. Building a track-record will be key to convincing the market that the usual risks associated with a family-packed management team will not be a problem long-term.

Management structure

Wong Voon Ten - Managing Director

Together with Wong Nyeon Thiat (sister), Wong Voon Yoong (brother), Lee Cheng Ngee (Brother-in-law) , and Budhi Sentoso Rachmat, he the co-founded PMI Group, steering strategy, growth and future direction with both vision and elbow grease. At 65 he is the MD of the Group and brings with him the experience he accumulated in his family business, Folin & Brothers Sdn Bhd, as assistant to the Managing Director in October 1984, where he supported administrative and business development activities in engineering products.

Beginning in 2012, he led the transfer of the Group’s filtration solutions business into PMIT Malaysia and has since spearheaded the company’s development of customized filtration solutions, particularly for the edible oil sector which enhanced its manufacturing capabilities. In short, he oversaw PMI’s transition from being a distributor to becoming a full-fledged manufacturer of advanced filtration systems.

Wong Voon Ten’s son-in-law, Ko Siu Lun is the Head of Global Operations along with nephew Lee Han Jun (son of Lee Cheng Ngee & Wong Nyeon Thiat) is the Head of Innovation & Technology.

Wong Voon Ten is the brother of Wong Nyeon Thiat, Wong Voon Yoong, and Wong Voon Shek, brother-in-law to Lee Cheng Ngee. Father-in-law to Ko Siu Lun and uncle to Lee Han Jun. Wong Voon Ten has a ‘post-IPO’ direct stake of 14.93% in PMI.

Wong Nyeon Thiat - Executive director, finance

Wong Nyeon Thiat, 64, plays a key role in formulating financial plans and strategies, strengthening internal control systems, and overseeing human resource management to support the group’s growth. She was appointed to the board on 23 August 2024.

Armed with a BSc (Hons) in Accounting & Financial Management from Loughborough University, she was responsible for managing the accounts for Folin Engineering & Construction Sdn Bhd and later was appointed Finance & Administration Manager in April 1987 for Pan-Merchant Industries. Besides co-founding an industrial focused company Wong Nyeon Thiat was instrumental in establishing systems to support the company’s financial governance and operational efficiency.

She is the spouse of Lee Cheng Ngee, sister to Wong Voon Ten, Wong Voon Yoong, and Wong Voon Shek and mother to Lee Han Jun. She has a ‘post-IPO’ direct stake of 5.6% along with an indirect stake of 14.93%.

Wong Voon Yoong - Executive director, sales & marketing

Think of Wong Voon Yoong as the Group’s global deal-hunter and frontier pusher:

always looking for the next market, new sectors, and overseas challenges. Aged 61, he is the Promoter, substantial shareholder, and Executive Director of PMI. Started with modest beginnings: fixing air-conditioning units, supervising sites, checking tender prices; the kind of stuff that builds grit. In 1986, co-founded Pan-Merchant Industries with his siblings and by 1987, he became Sales Director. He didn’t just sell filters; he sold the idea that Malaysian-made filtration equipment could compete globally. He oversaw PMI’s sales of filters into markets like Africa, Australia and Netherlands.

As PMIT Malaysia grew from 2002 onward, he took on the role of Sales & Marketing Director, laying the groundwork for offices in Singapore, USA, Netherlands. Under his (and the team’s) watch, the IPO proceeds (RM67.6 million) are being used not only for expansion and new markets, but also specifically for upgrading manufacturing plants, adding machinery and tools, improving efficiency, renovating facilities.

He is the brother of Wong Voon Ten, Wong Nyeon Thiat, and Wong Voon Shek, and brother-in-law of Lee Cheng Ngee and Uncle to Lee Han Jun. Similar to his eldest sibling, Wong Voon Ten has a direct stake of 14.93% in PMI.

Wong Voon Shek - Executive director, supply chain & operations

At 59, Voon Shek drives operations in PMI, managing everything from manufacturing and assembly to installation, all while squeezing out inefficiencies.

After graduating with an Engineering bachelor's degree, he joined Wah Seong

Engineering Sdn Bhd as a Project Engineer and consequently joined Gadelius Sdn Bhd as a project sales engineer. In 1992, he joined Pan-Merchant Industries, taking charge of manufacturing, assembly, and the installation side of filter equipment. When PMIT Malaysia was formed and the filtration business was migrated over, he became Supply Chain & Operations Director of the Group.

He has overseen the group’s improvement in manufacturing and installation operations for filtration systems. Under his guidance PMI witnessed strengthening in supply chain systems to support the Group’s domestic and international projects.

He is the brother of Wong Voon Ten, Wong Nyeon Thiat, and Wong Voon Yoong, and brother-in-law of Lee Cheng Ngee and Uncle to Lee Han Jun. Wong Voon Shek has 85.5 mil shares of PMI Group which is equivalent to 9.33% (directly-owned).

Lee Cheng Ngee - Executive director, technical

At 66, Lee Cheng Ngee leads the technical arm of PMI, and holds a Bachelor of

Science (Hons) in Production Engineering and Management.

Lee Cheng co-founded Pan-Merchant Industries with Wong Voon Ten (Brother-in-law), Wong Nyeon Thiat (Spouse), Wong Voon Yoong (Brother-in-law), and Budhi Sentoso Rachmat. By April 1987, he was made Director, leading the After-Sales Department: dealing with technical support, installation & commissioning of filtration equipment, product design. When PMIT Malaysia was set up and filtration operations moved over, he became Technical Director. He’s been leading efforts to customise filtration machinery (higher pressure, bigger capacity, specific industry specs).

Under his watch, the Group now supports clients in industries beyond edible oils things like sustainable fuel, water treatment, food processing. His son, Lee Han Jun, is serving as Head of Innovation & Technology.

He is the spouse of Wong Nyeon Thiat and brother-in-law to Wong Voon Ten, Wong Voon Yoong, and Wong Voon Shek and father to Lee Han Jun. Lee Cheng Ngee has a 14.93% direct ownership along with 5.6% indirect ownership (excluding his wife’s stake in the company).