Coal as a source of resilience

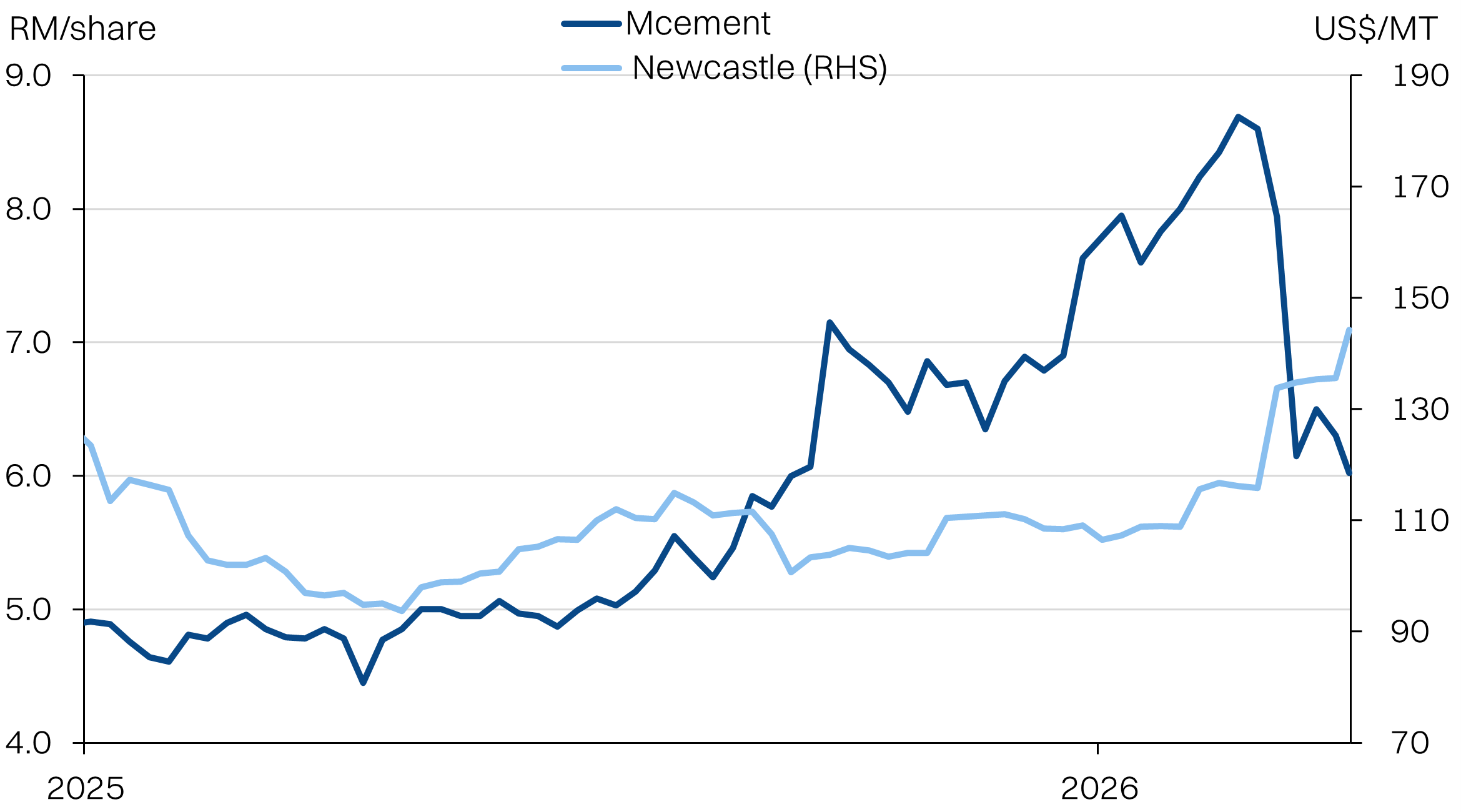

MCement is oversold on fears of higher coal prices.

Key Takeaways:

- National energy mix dependency on coal, particularly from Indonesia should cushion electricity inflation pressure.

- Indonesian coal has abundant supply due to falling China demand. Price increase has been relatively modest compared with other energy commodities.

- MCement is oversold on coal price fears. We place a FV of RM8.15/share (NR).

Fuel mix | Coal prices | MCement Valuations

Sources: Source: Bloomberg, NewParadigm Research, April 2026

Macro: Electricity tariffs shielded by Indonesian coal

- We focus on Malaysia’s coal exposure in this report, which looks to be a source of resilience against a backdrop of global energy inflationary shocks.

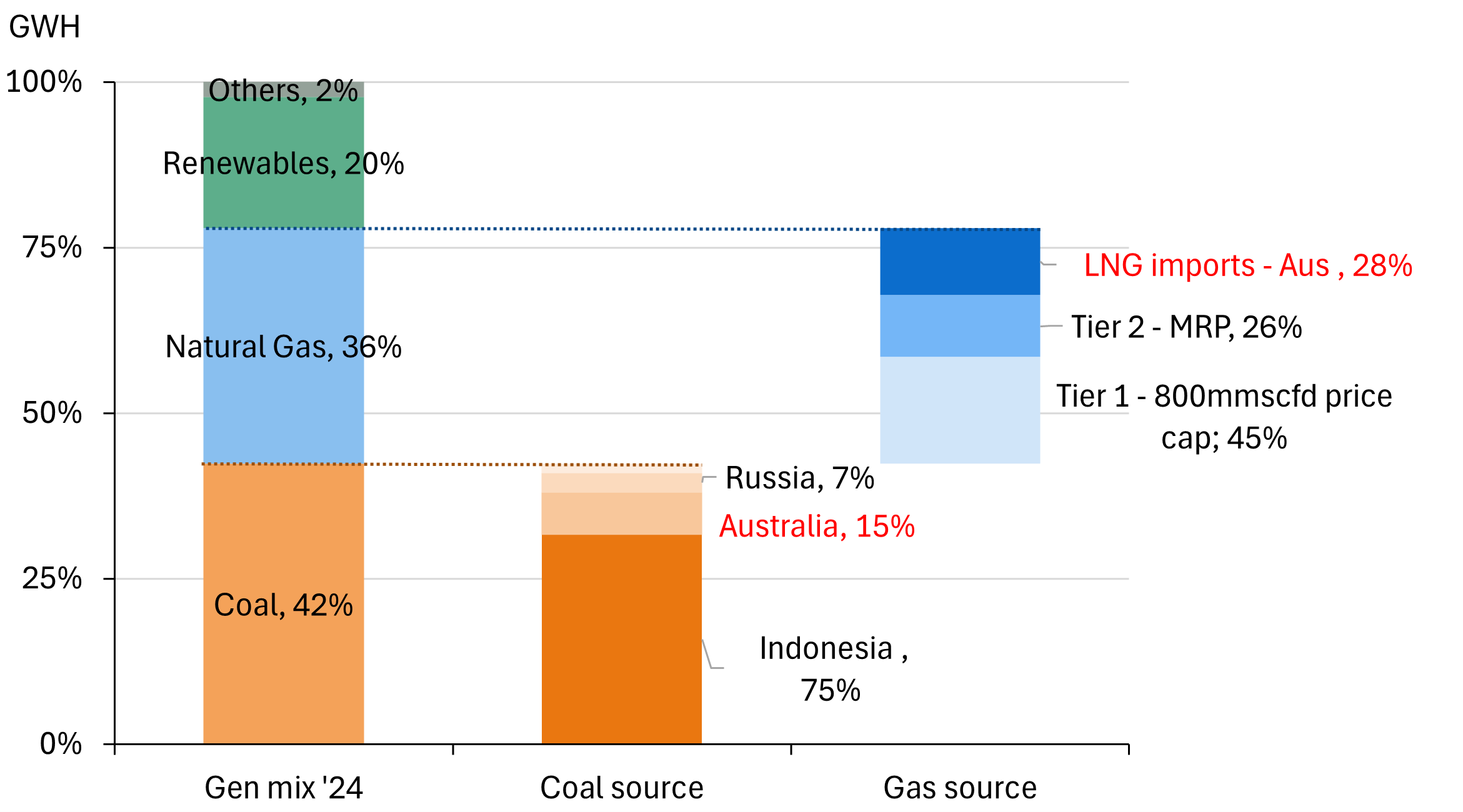

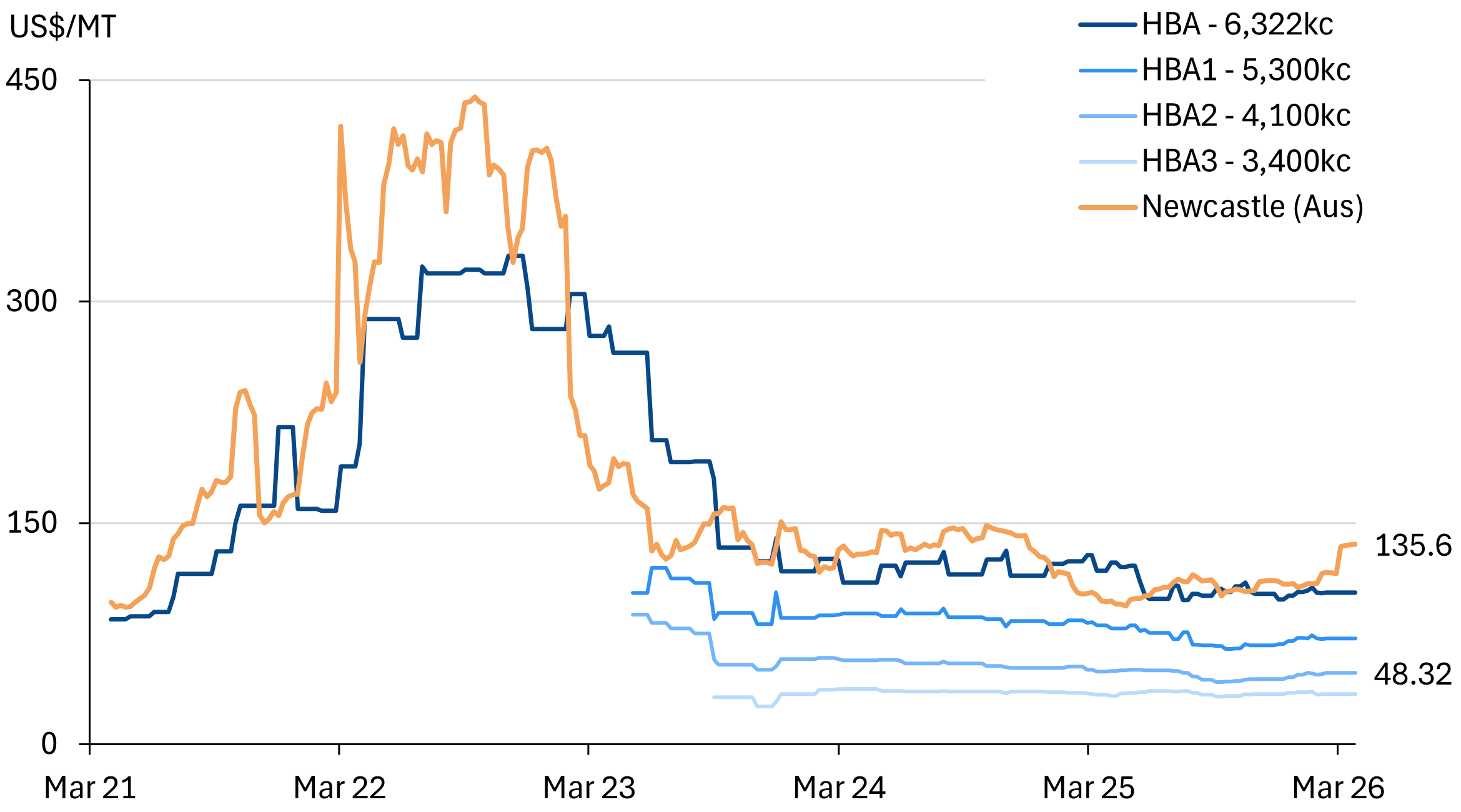

- Malaysia is highly dependent on Indonesian coal, with roughly 75% of coal sourced from Indonesia - particularly low-grade spec of around 4,200kc. Another ~15% comes from Australia and ~7% from Russia.

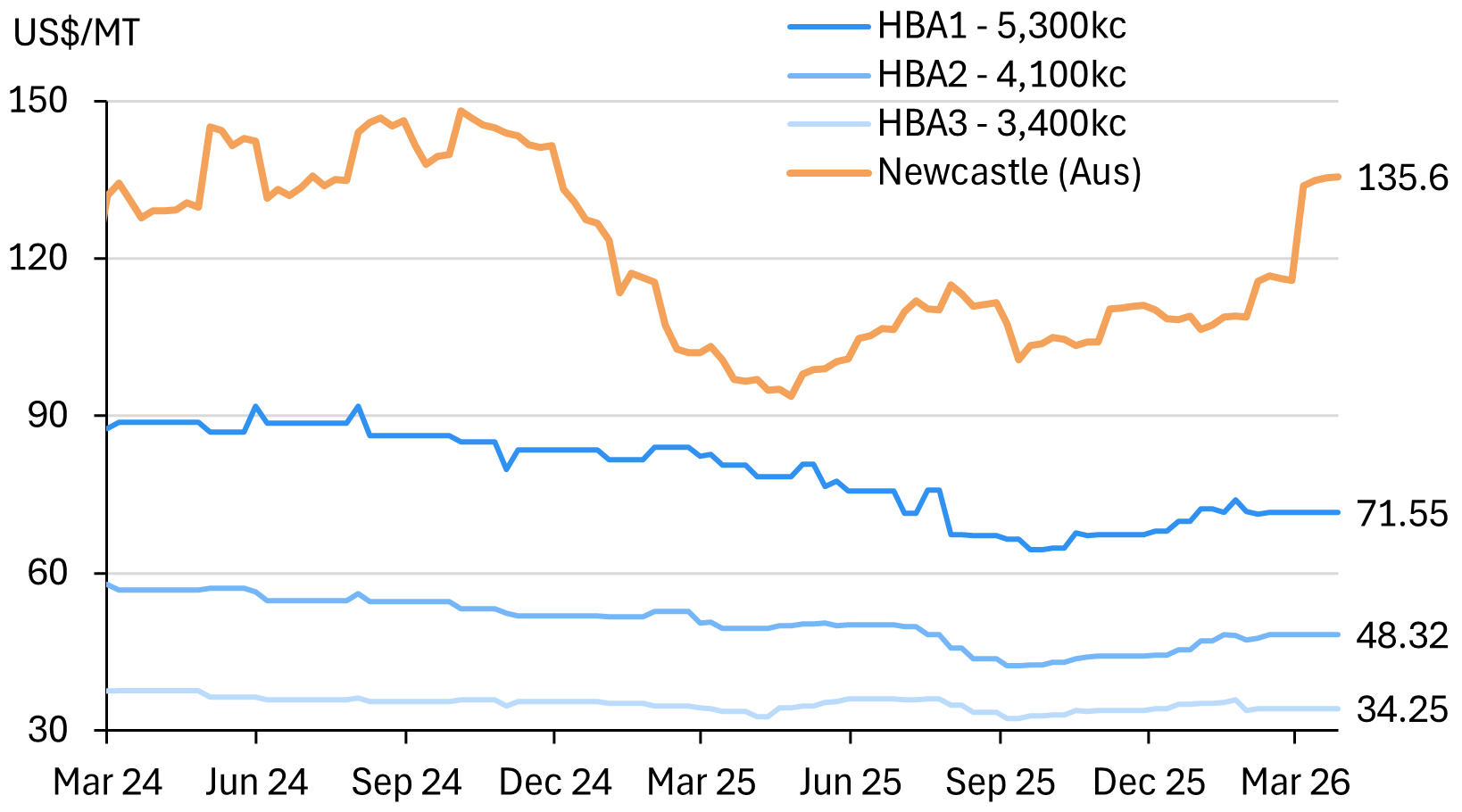

- Compared with the benchmark Newcastle coal benchmark (+25%), Indonesia’s HBA-priced benchmarks have been almost flat since the war broke out, especially for lower-grades.

- This is due to domestic overproduction and structural decline in demand from China. Even with the risk of windfall export taxes (now deferred), this relative price shock is modest in comparison.

- Outside of coal, we estimate less than 10% of total generation mix comes from imported LNG, which in turn is primarily sourced from Australia, ensuring at least supply security if not pricing stability. Of course, the balance of the gas is sourced domestically with 800mmscfd under a price cap.

- Overall generation fuel mix at risk of inflationary pressure works out to only ~16% of total mix. While there will almost certainly be some electricity tariff hikes (likely around May/June) it should not be as drastic as petrol and diesel.

MCement - oversold on coal fears

- One industry that benefits from the relative price stability of Indonesian coal are the cement makers, with coal making up about 40% of COGS.

- MCement solely sources its coal from Indonesia, and will be relatively shielded from the impact of the rising coal prices. Furthermore, the recent reduction in price rebates to distributors, raising effective ASP’s.

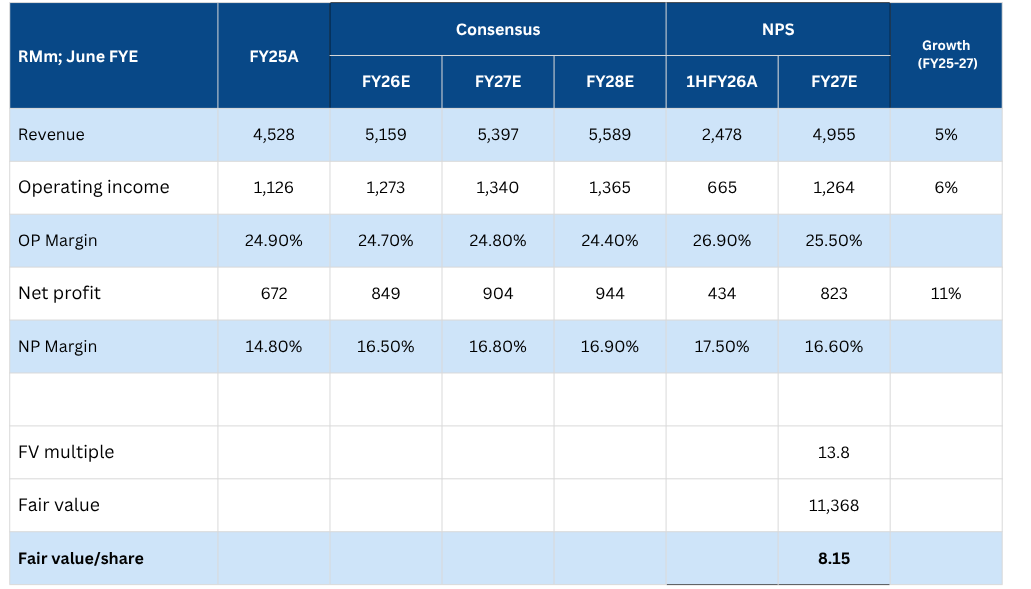

- Even if we assume revenue remains flattish at 1HFY26 (ended Dec) levels and margins revert to ~16.6% (2QFY26: 18.5%) to account for modest coal cost inflation, MCement would still deliver ~RM823m in NP (+11% CAGR vs FY25). Applying a 2yr average multiple of 13.8x (BF12M), our FV for MCement is RM8.15/share (non-rated).

Coal will anchor electricity price inflation

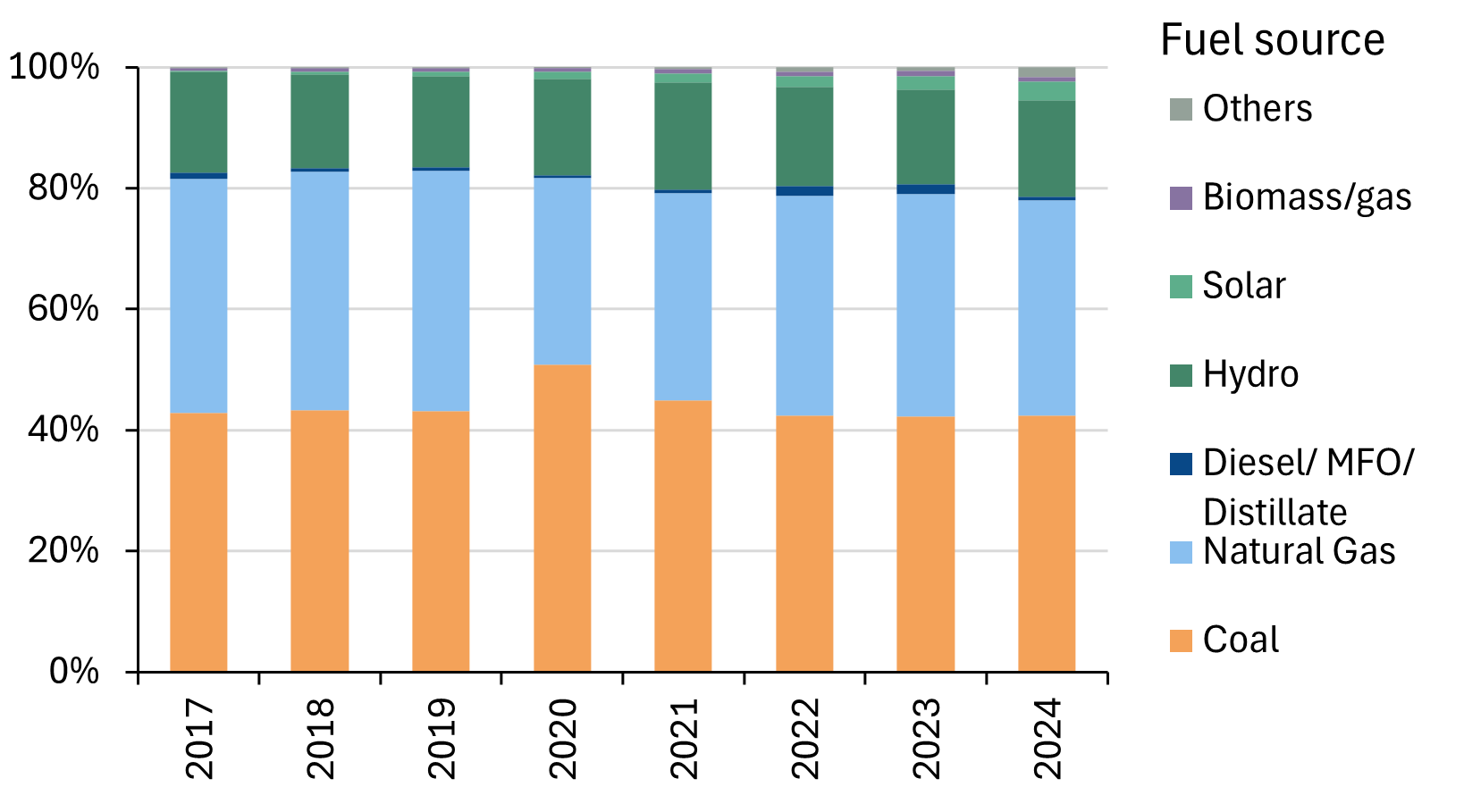

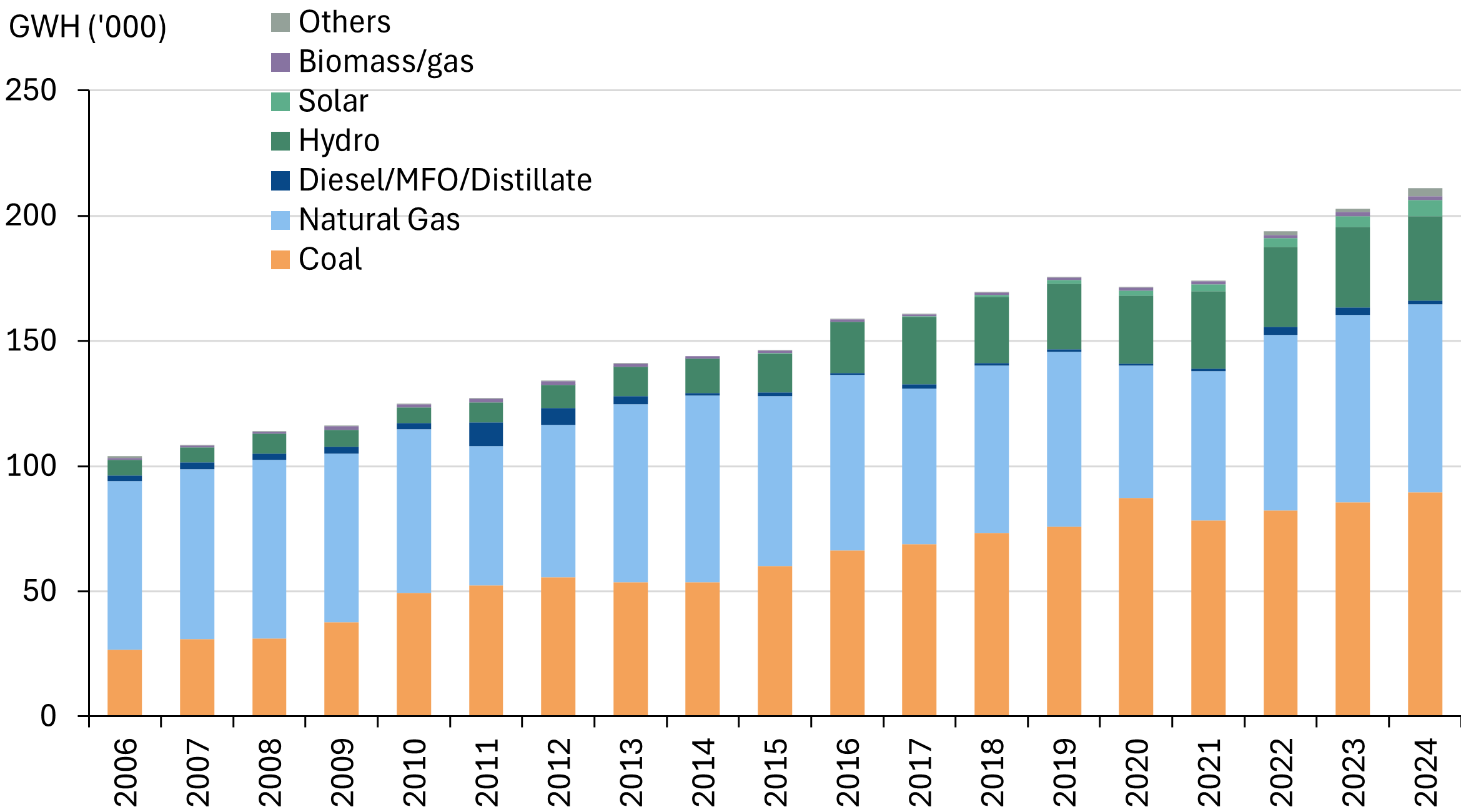

Malaysia’s electricity generation mix will be substantially shielded from the energy commodity price inflation triggered by the war in the Middle East. Nationwide, 42% of the generation mix comes from coal. But for Peninsula Malaysia alone, coal is 58.8% of the generation mix (FY25).

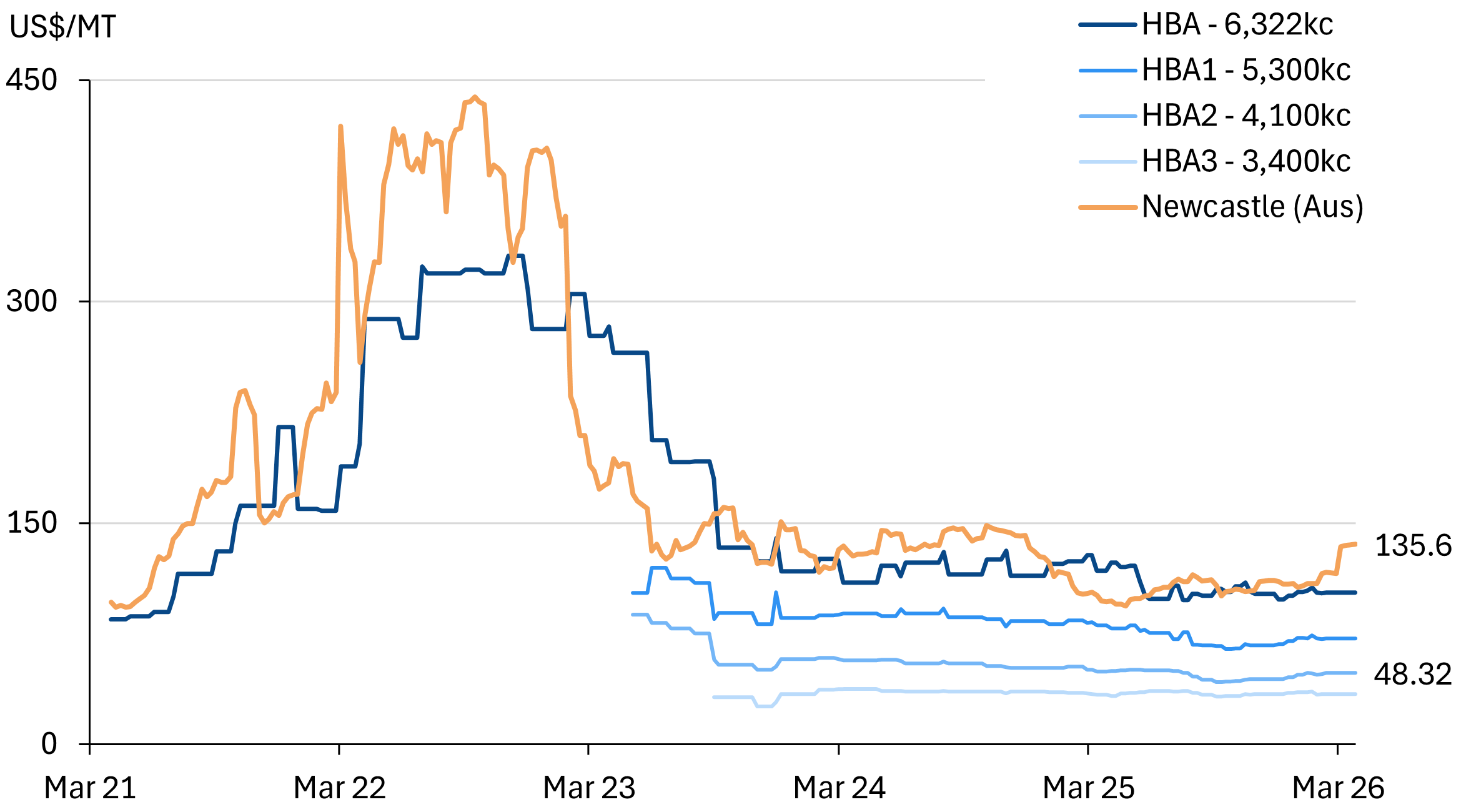

Critically, Malaysia sources 75% of its coal from Indonesia and only 15% from Australia. Another 7-8% comes from Russia. Thus, while the Newcastle Coal Futures (Australia) is up by +25% since the war began, the Indonesian benchmark - Harga Batubara Acuan (HBA) - has remained relatively flat. This is because Indonesia was facing a structural oversupply of coal prior to the war that has kept prices low (more in the next section).

And as far as natural gas goes, Malaysia at least has supply security with LNG, which is entirely sourced from Australia. This only makes up <10% of the total energy mix. Lastly, another ~20% of electricity comes from various renewable sources - hydro, solar and biomass & biogas.

Malaysia’s utilities fuel mix - 42% comes from coal

Malaysia’s utilities fuel mix over time

Why Indonesia’s coal prices are stable

Since the start of the war, Indonesia’s coal benchmark, HBA, has remained flat. This is in stark contrast to the Newcastle benchmark that is up +25%. This is because Indonesian coal was already struggling with structural oversupply before the war.

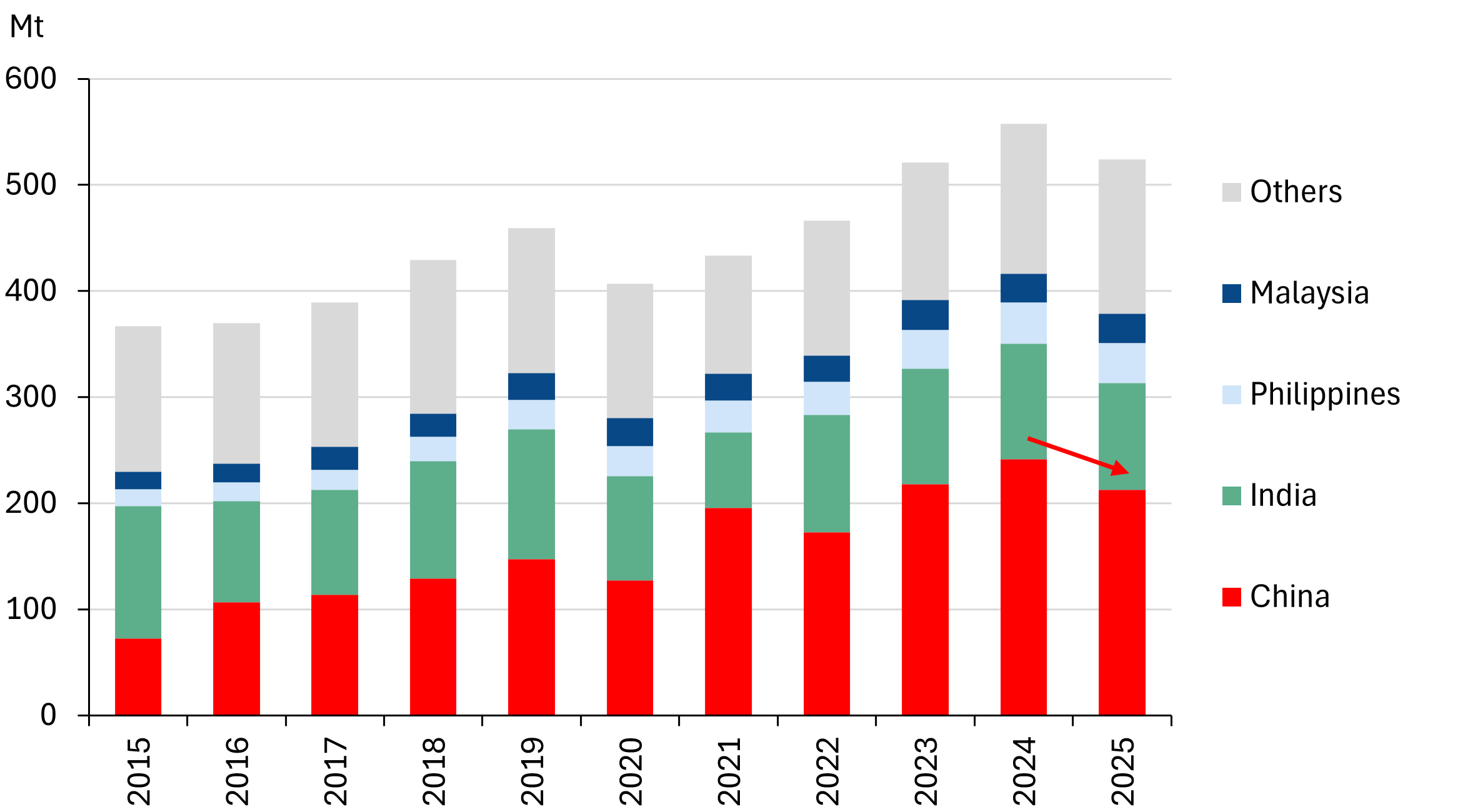

One of the key reasons is that Indonesia’s largest export market, China, which makes up 41% of export share has had a gradual decline in demand for imported coal - a combination of domestic supply availability as well as a growing share of renewables in the generation mix.

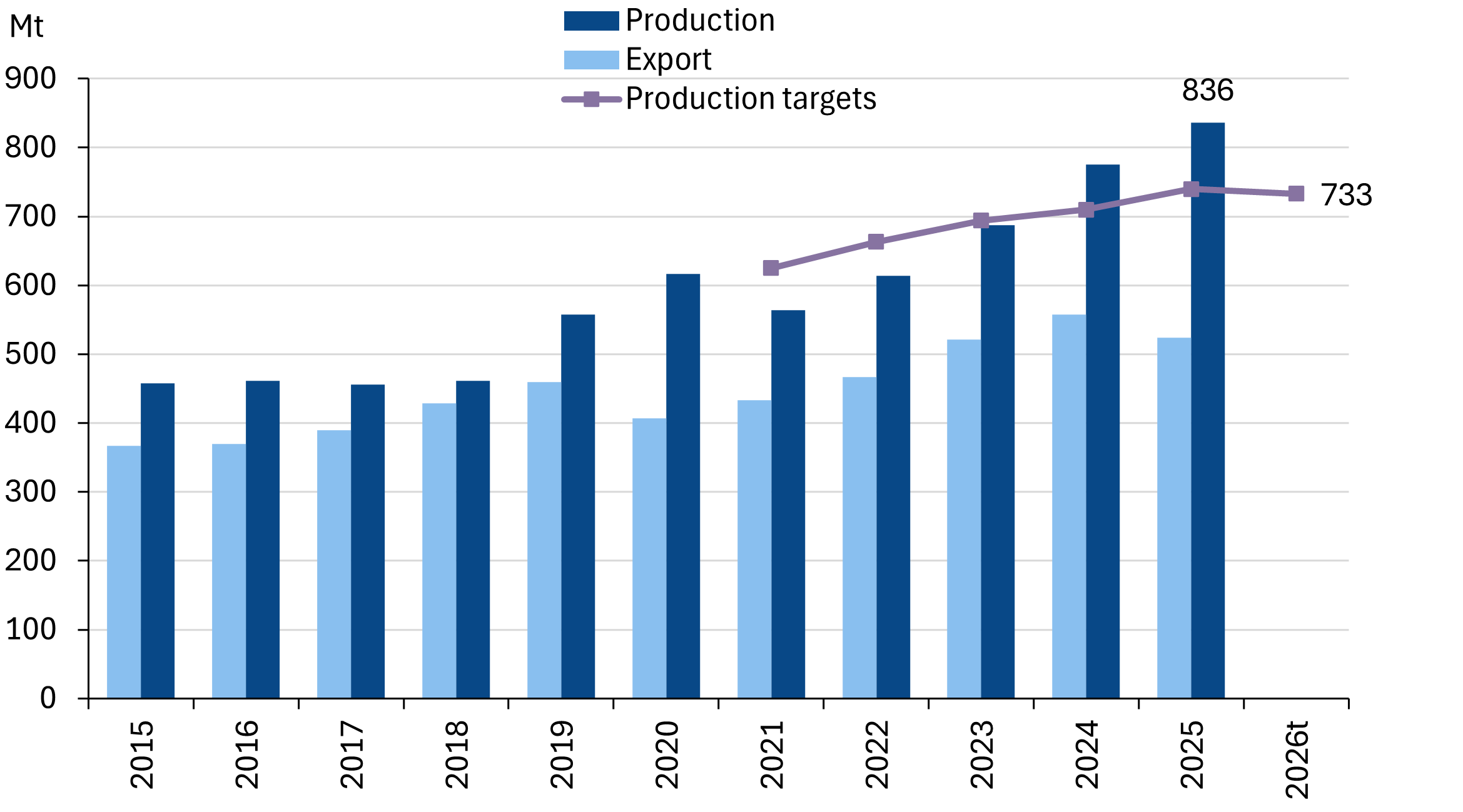

In fact, Indonesia prior to the war had lowered the coal production target to 600Mt for 2026, in an attempt to manage the glut that was hurting prices. That target has since been increased to 733Mt following the war, but still remains below the 740Mt target and the 836Mt actually produced last year. One reason for the overshoot (vs targets) is the previously approved 3-year Rencana Kerja dan Anggaran Biaya (RKAB) approval of 900Mt/yr for 2024-2026.

Unlike 2022, Indonesia coal prices remain stable compared with Newcastle benchmark

Indonesia coal - Production targets meant to curtail overproduction

Structural demand headwinds

Against rising coal production, many of Indonesia’s main export destinations are pursuing long-term decarbonization roadmaps. China is the largest importer of Indonesian coal, making up 43% share in 2024, but falling to 40% in 2025. China’s imports of Indonesian coal fell by -12% YoY in 2025, driving an overall -6% YoY drop in Indonesia’s coal exports.

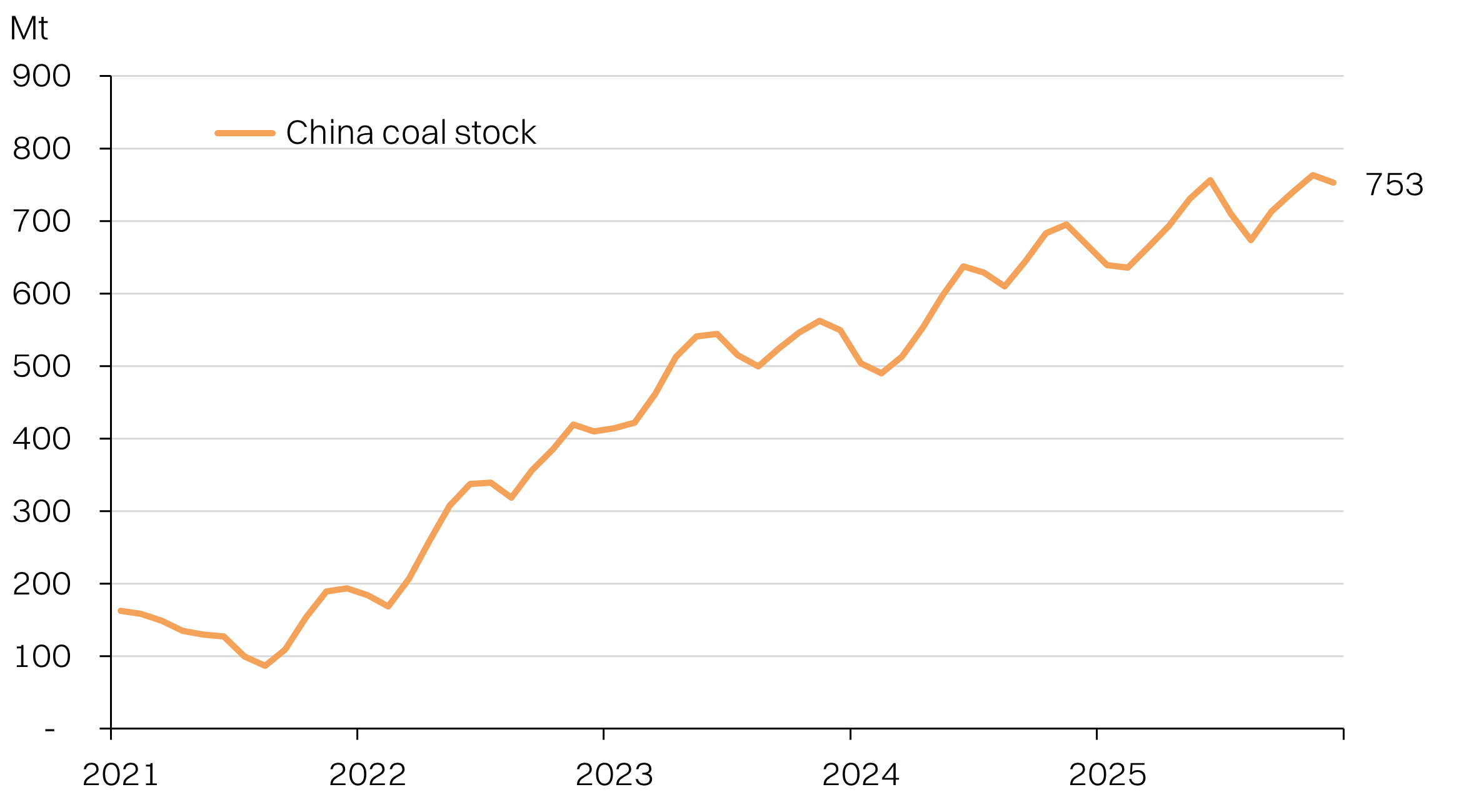

China’s coal consumption began to plateau in 2024, as the share of coal power in the generation mix fell to a low of 54.8%. This is down from 57% in 2020 - a trend that is expected to persist. Additionally, China has domestic coal production. The rising bunker fuel prices will drive up the cost of shipping the coal to China this year, improving the relative competitiveness of domestic coal. Finally, China’s coal stocks are also at a historically high level. As of December 2025, it stood at 753Mt.

Indonesia has been pivoting its exports towards Asean neighbours, but with the underlying overproduction and a ceiling on demand, prices should remain capped.

Indonesia coal exports - >40% exposure to China

Indonesia coal - Production targets meant to curtail overproduction

MCement - fears on input costs overblown

Against this backdrop, one of the big losers from the war has been the share price of Malayan Cement (MCement), down -30% peak to trough. We think a key catalyst for the sell-off has been fear of rising coal prices as well as softer demand. After all, coal makes up 40% of cement manufacturing costs.

Firstly, MCement solely sources its coal from Indonesia. The Newcastle benchmark references Australian coal export prices. And as we have pointed out - prices of Indonesia coal remain modest with a relatively subdued outlook as well. It is also worth mentioning that MCement also procures its coal about two months forward.

The concerns on the demand front are more reasonable. Inflationary pressure could dampen end-demand. However, the construction industry has high inertia and slowing ongoing projects is not a viable option.

MCement’s share price has corrected -30% peak-to-trough

Indonesia’s HBA coal benchmarks remain stable despite the war

Room for some margin pressure

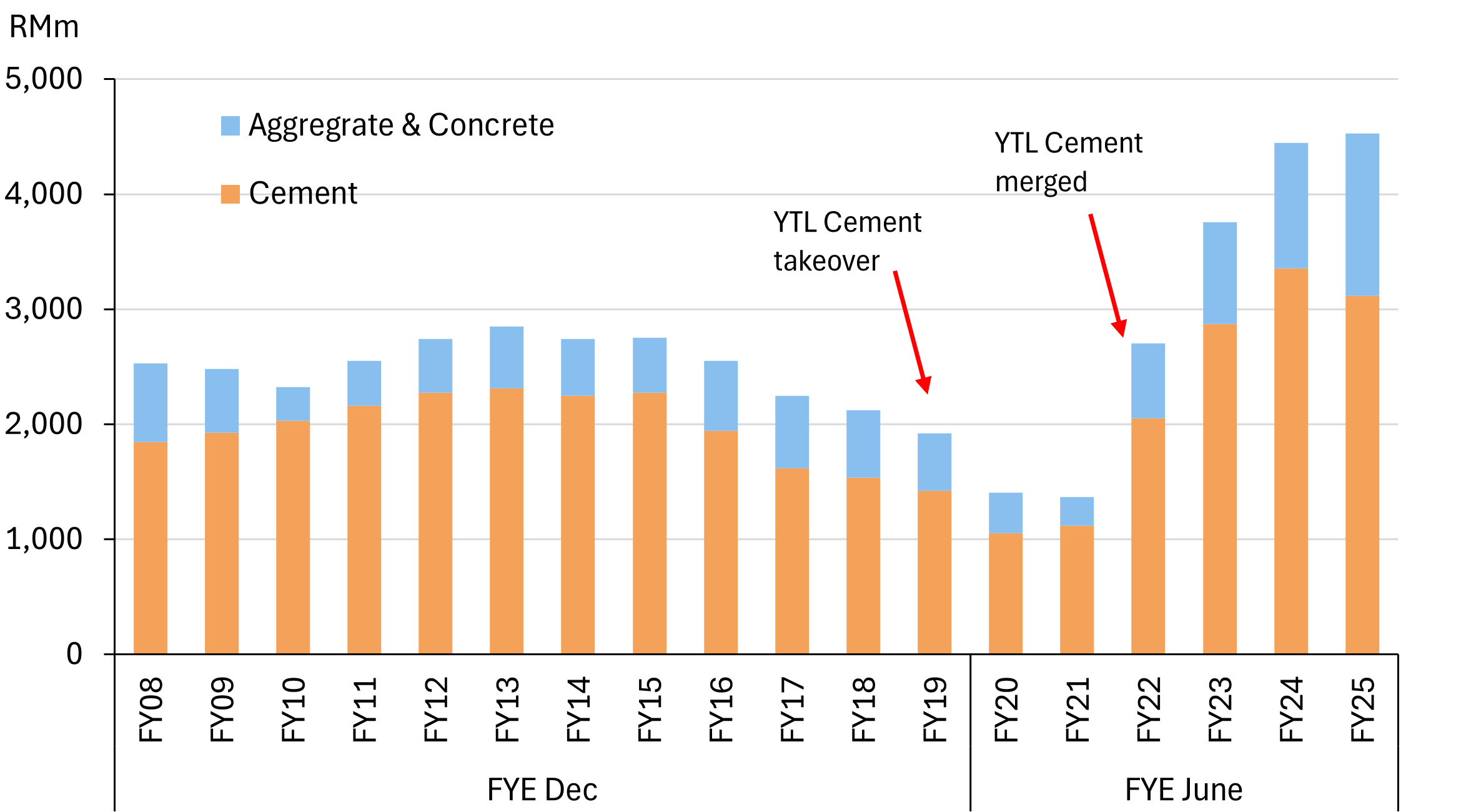

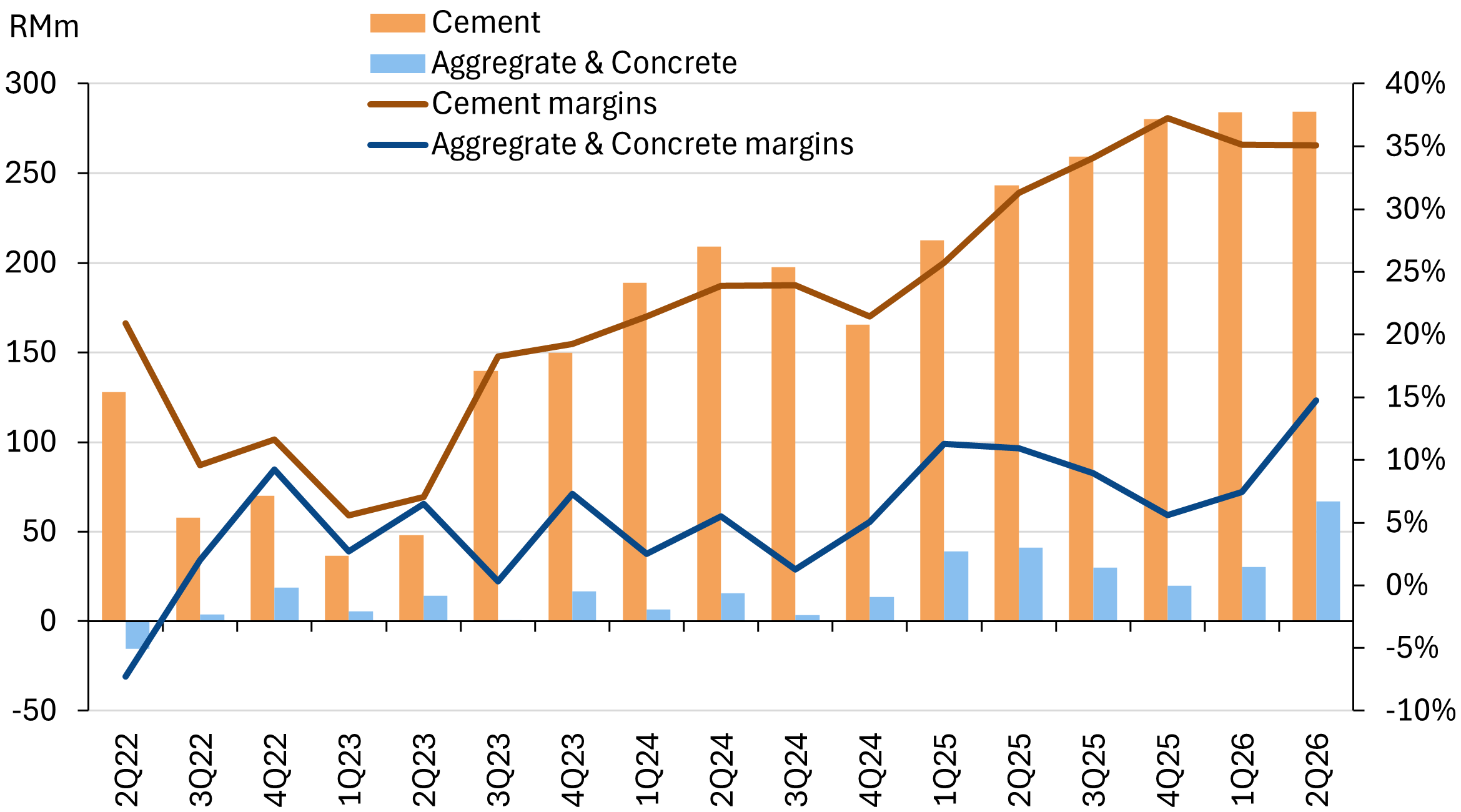

MCement’s earnings expansion has been driven by +10% YoY revenue growth in 2QFY26 (ended Dec), as well as a 3ppt YoY increase in operating margins to 27.8%. This came on the back of a reduction in rebates given to distributors that led to a +23% YoY jump in operating profits in 2QFY26 and a +26% YoY jump in NP.

For context, consensus is assuming +13%/+5% revenue growth for FY26/27 as well as +26%/+6% NP growth on margins expanding to 16.5%/16.8% compared with the 14.8% in FY25.

MCement’s 1HFY26 performance is on track to meet consensus’ high-growth assumptions, with revenue and NP at 48%/51% of forecasts. Furthermore, NP margins in 1H26 were at a historic high of 17.5% in 1HFY26.

MCement’s revenue has been enjoyed robust growth post-pandemic & merger

MCement’s operating profits and operating margins have been improving

Oversold even with some earnings downgrades

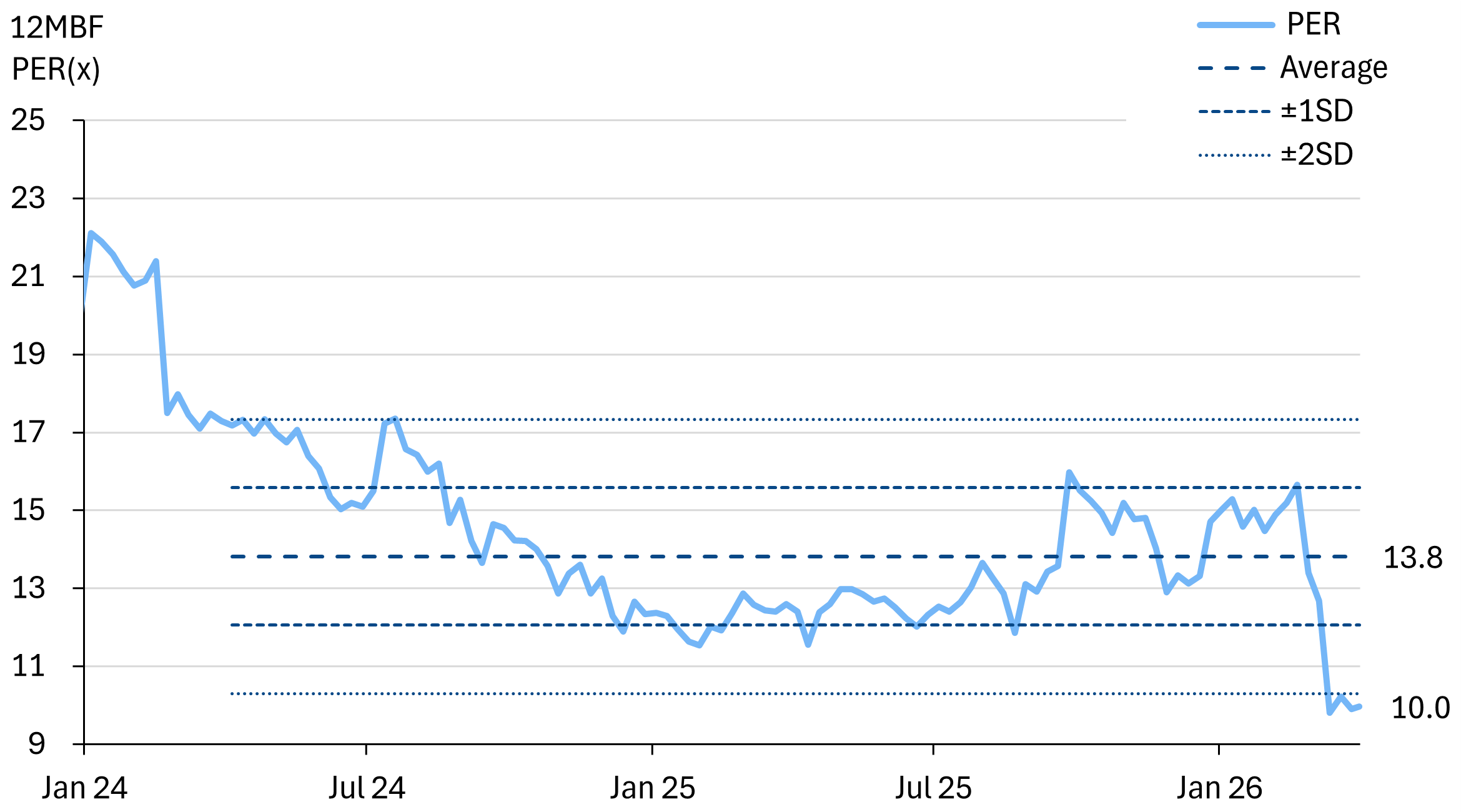

We estimate a fair value of RM8.15 (non-rated) for MCement, based on a conservative multiple of 13.8x - the average of the 2yr average PER (12MBF) against FY27E NP of RM823m.

For our earnings assumptions, we have trimmed revenue growth to 5% CAGR for FY25-27E, or RM4.955bn. This is very reasonable considering 1HFY26 is already annualizing towards RM5bn. Additionally, we assume margins hold at 16.6% - marginally lower than consensus’ expectations of 16.8%. This leaves plenty of headroom to surprise on the upside.

Additionally, our multiple could be higher. Using a 3-yr average PER would give a multiple of 17.3x and a bull case fair value of RM10.20.

The primary risk to our view would be physical supply disruption to coal from Indonesia, perhaps stemming from diesel shortages that are necessary for coal production and transportation.

MCement earnings expectations and FV

MCement is trading at -2SD vs the 2yr historic average PER