Crossing RM1bn orderbook

LSH is leveraging collaboration agreements to add RM600m to its order book.

Stock information

LSH CAPITAL

LSH | 0351.KL

BUY

Target price: RM3.00

Last price: RM1.88

Market cap (RMm): RM1,576m

Shares out: 838m

52-week range: RM0.730 / RM2.56

3M ADV: RM2.11m

T12M returns: 126%

Disclaimer: By using this information, you acknowledge that you are solely responsible for evaluating the merits and risks of any investment decision and agree not to hold NewParadigm Research liable for any damages arising from such decisions.

Key takeaways

- Between the two new “BEST Collaboration” projects, LSH will add ~RM600m construction orderbook with another ~RM230m profit share. Total orderbook will rise to ~RM1bn.

- We maintain our FY26E earnings at RM139m, but raise revenues by +9%.

- Maintain BUY but with lower TP of RM3.00 on 12x FY27 PER target. Still below sector average of 13x 24MBF PER.

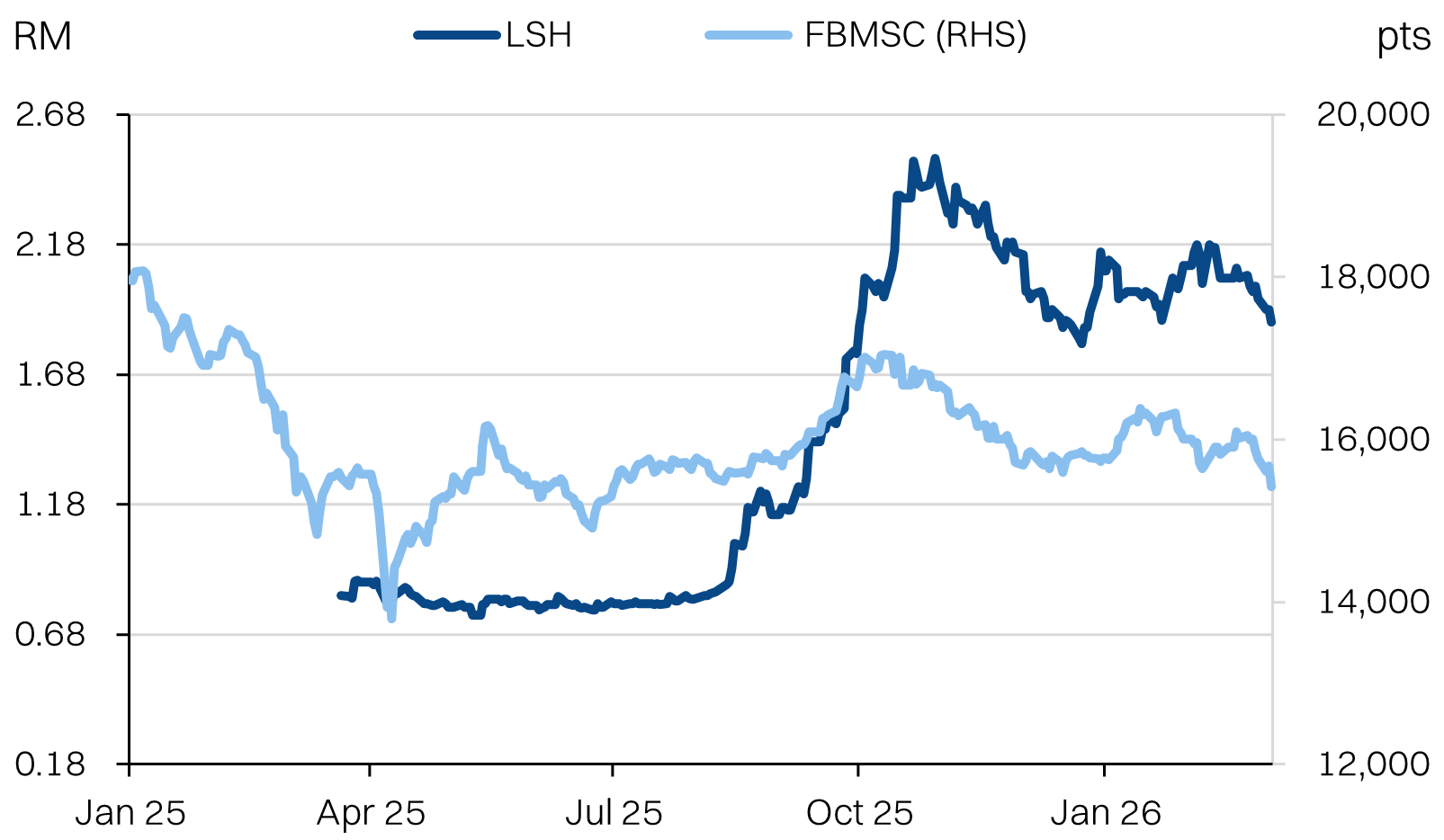

Share price performance

Investment fundamentals

| RMm | FY25E | FY26E | FY27E | FY28E |

|---|---|---|---|---|

| Revenue | 461 | 656 | 807 | 906 |

| Revenue Growth | 27% | 42% | 23% | 12% |

| EBITDA | 148 | 199 | 238 | 241 |

| EBITDA margin | 32% | 30% | 29% | 27% |

| Adj PATAMI | 108 | 140 | 225 | 226 |

| Adj NP margin | 23% | 21% | 26% | 26% |

| ROA | 12% | 12% | 14% | 15% |

| ROE | 16% | 18% | 23% | 22% |

| PER | 14.6 | 11.3 | 7.6 | 6.6 |

| P/BV | 2.4 | 2.1 | 1.7 | 1.5 |

| Yield | 2% | 3% | 4% | 4% |

Source: Company data, NewParadigm Research, March 2026

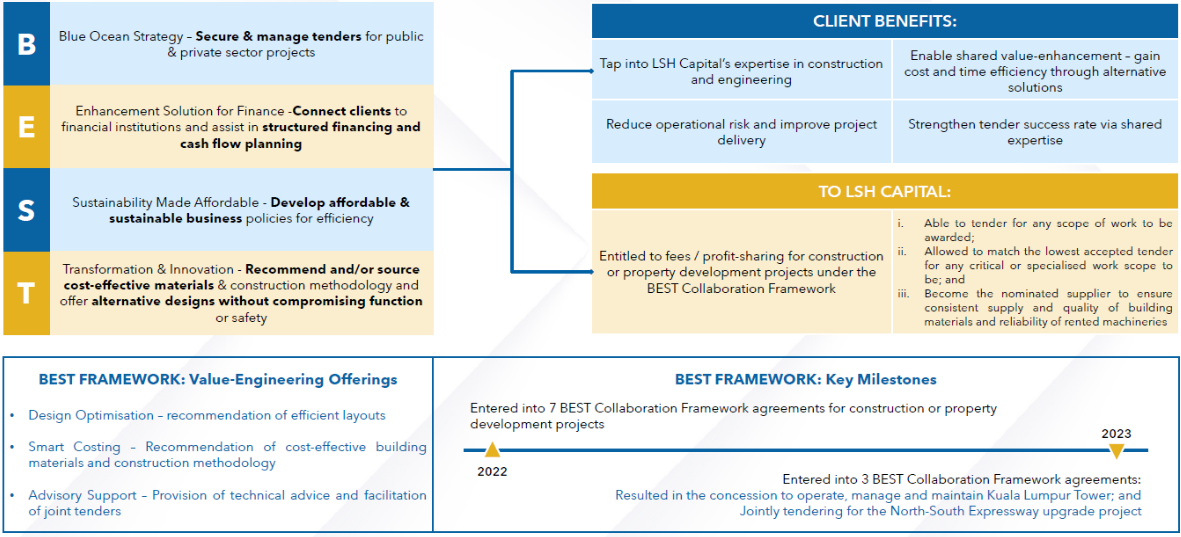

Unpacking the “BEST Collaboration”

- LSH announced two projects under the “BEST Collaboration” framework - LSH BUND as well as “Lot 2072 Gombak”. The respective GDV of the projects are RM500m and RM404m with GDC of RM350m and RM244m.

- The framework is unorthodox. Typically, companies will set up a JV structure to undertake such projects with the underlying developer. One benefit of this structure is it is quicker and lower cost to execute, minimising transaction fees. On the other hand, it is less transparent, especially if it involves a related party.

- LSH BUND is via a related party - Airman S/B, which is controlled by the Lim family. However, it is worth noting that the Gombak project is not an RPT.

- The headline economics of the projects are such -

- The combined GDC of ~RM600m will be booked as construction revenues with a targeted gross margin of 30%.

- LSH will also have a 75% cut of the ~RM310m development profits (GDV less GDC), for its own share of ~RM230m. We expect this contribution to be relatively high margin.

- While LSH Bund was previously in our property segment assumptions, the Gombak project is incremental to our assumptions. Against the orderbook burn rate of ~RM300m, LSH’ underlying orderbook would rise to ~RM1bn, or ~3x construction revenue. Note that both Bund/Gombak have not been formally awarded, but these should be high certainty wins.

Maintain Buy with lower TP

- Following the broader de-rating of the construction sector, we lower our target multiple to 12x FY27E from 13x. We think our target multiple remains reasonable, considering our forecasts peg LSH at +29% YoY earnings growth.

- We have also trimmed our FY27 NP assumption by -8% to RM206m, to reflect a more conservative assumption on the timeline for the infrastructure project awards - the highways, and UKAS projects.

- We maintain a BUY on LSH with a lower target price of RM3.00. The key catalyst for the stock will be a rebound in margins in 2QFY26 as well as newsflow on the aforementioned infrastructure projects.

About the Company

Lim Seong Hai Capital Bhd (LSH Capital) is a construction company with a secondary focus on property development and facilities management. The group differentiates itself from peers by its sector leading margins, low gearing and low reliance on subcontractors (~10%). Within construction, LSH Capital’s primary focus is infrastructure jobs. The group also has a 20-year concession to maintain and operate KL Tower and is pursuing highway concession opportunities as well.

About the Stock

LSH Capital is named after the late Lim Seong Hai and is now co-owned and run by his four children. It is also seen as a breakaway from the Tan Sri Lim Kang Ho’s group of companies (including Ekovest), which have similar operating segments. LSH Capital was initially listed on the LEAP market in 2021 but has since been promoted to the ACE market in March 2025.

Investment Thesis

LSH Capital has a relatively large funnel of construction orderbook and property development launches, compared with its current low-base. Additionally, the group’s peer-leading margins allows for meaningful translation of orderbook wins to earnings. We forecast earnings growth to +45% CAGR (FY27E). Looking ahead, this implies LSH Capital is trading at single-digit PER multiples on FY27E, which is well below sector average.

Key Risks

- Family business - The four Lim siblings collectively control 61% of the company and have full management control. Only 50% of the board is independent.

- Related party transactions - The group has a history of RPT transactions, and injection of related businesses. As LSH Capital transitions to non-RPT work, it remains to be seen if margins will continue to hold up.

- Small balance sheet - Net tangible assets total only RM509m (excluding RM149 goodwill on consolidation). We anticipate risk of additional fund-raising if capital intensive projects are secured.

Project Summary: LSH Bund & “Lot 2072 Gombak”

LSH Capital Bhd has entered into two mixed-development deals in Kuala Lumpur and Selangor with a combined estimated GDV of RM903.9m. Through its subsidiary ASSB, the group is collaborating with Airman S/B on LSH Bund, a 52-storey development in Setapak with a GDV of RM500m and a principal approval plot ratio of 6.4. Separately, subsidiary LSHBB has partnered with Bakti Jaya Impian S/B for the Lot 2072 Gombak project, a residential and commercial development with an estimated GDV of RM403.9m.

Both collaborations fall under the BEST Framework, where LSH provides construction services, value-engineering, and the supply of building materials and machinery. Under these agreements, the subsidiaries earn a 75% share of the pre-tax project profits.

LSH Bund & Lot 2072 Gombak / BEST Collaboration Framework

Source: Company Data, NewParadigm Research, March 2026

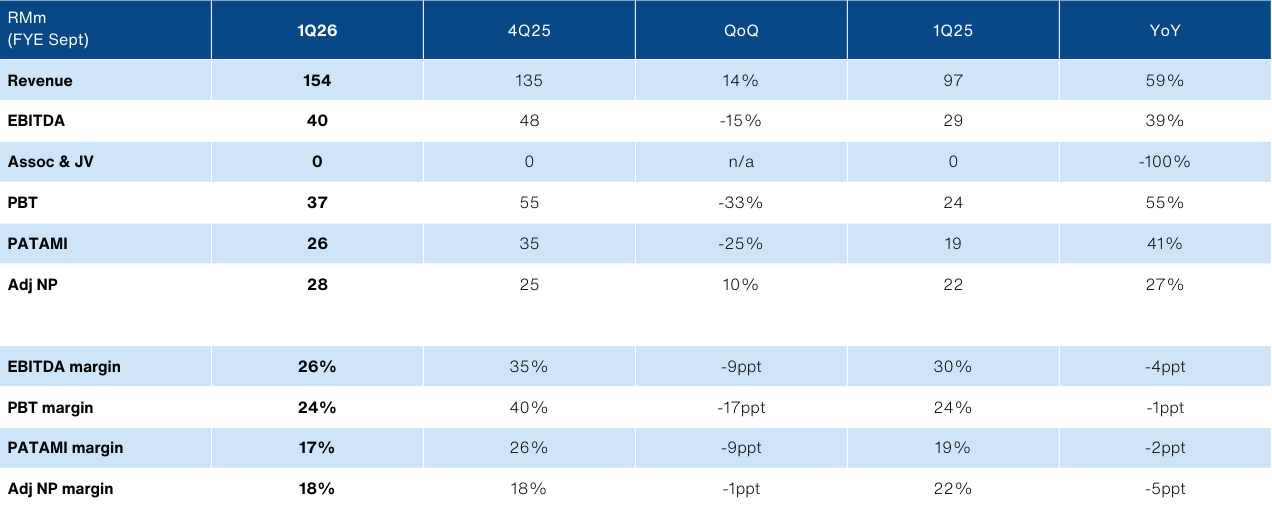

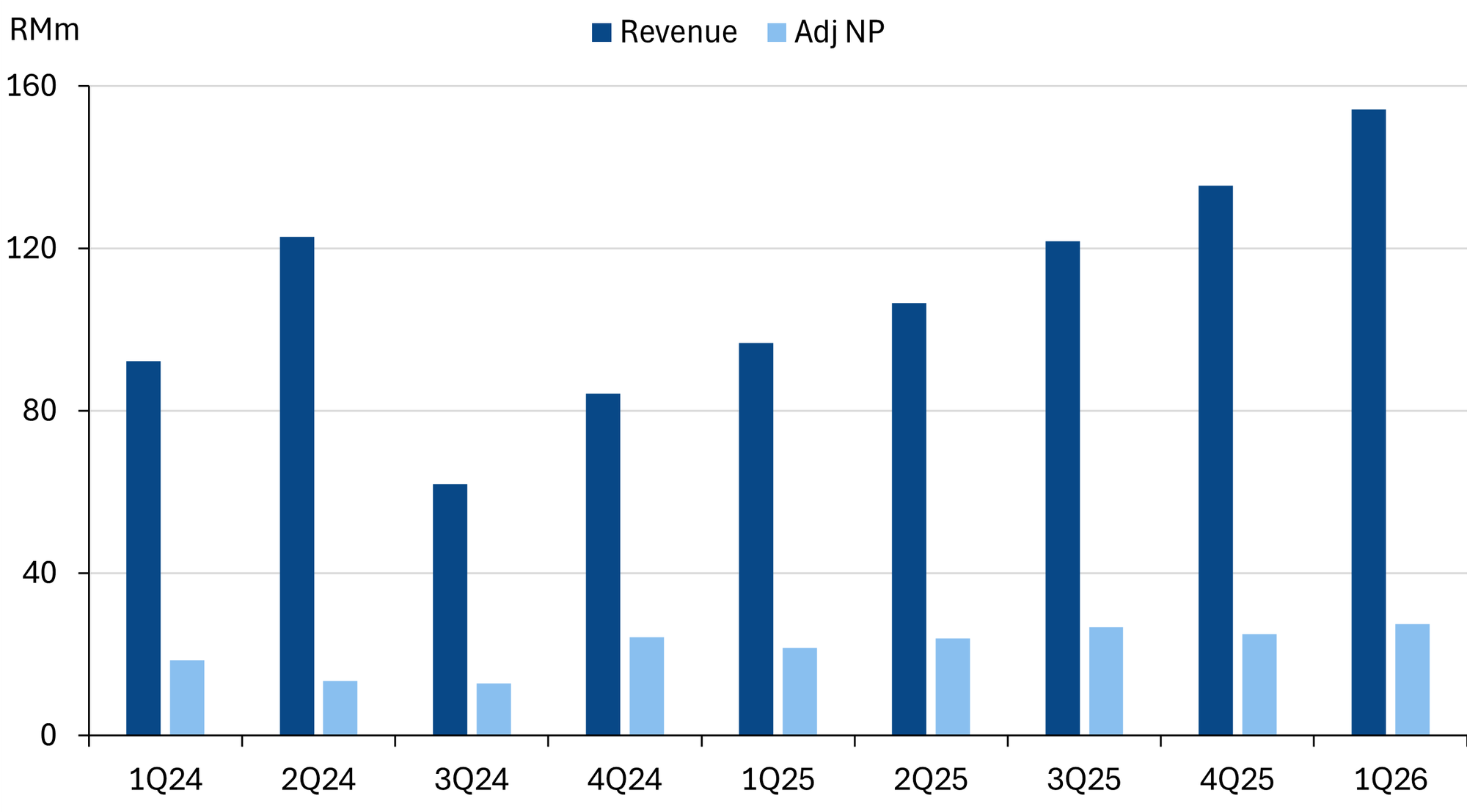

1QFY26 results recap

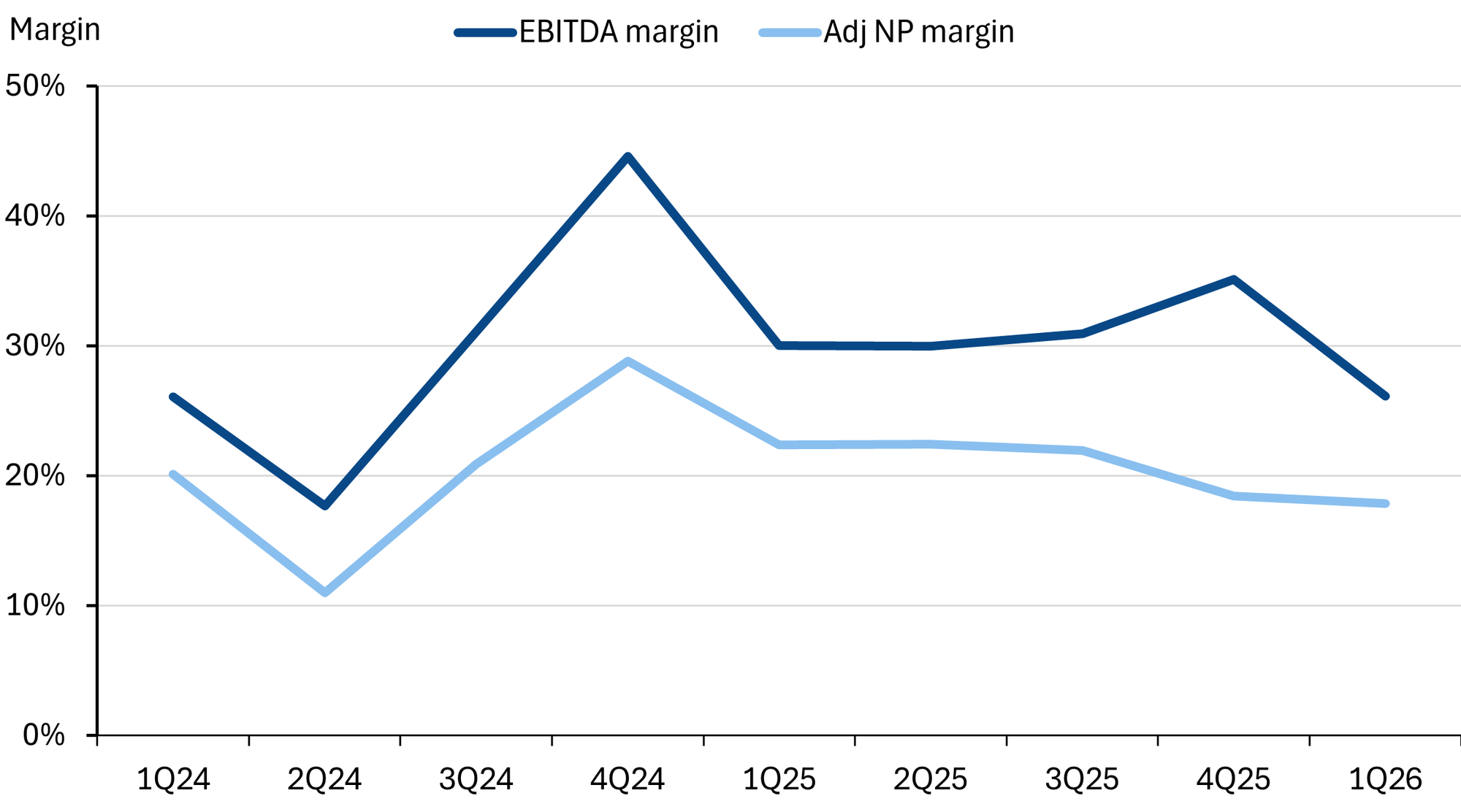

1QFY26 (ended-Dec) revenue of RM154m (+59% YoY, +14% QoQ) was in line with our expectations, but the Adj NP of RM28m (+27% YoY, +10% QoQ) was behind our forecasts. Net margins cooled to 18% (-5ppt YoY), driving the miss.

Management pinned this on project mix for the quarter that led to a -11% QoQ decline in gross profits that resulted in GP margins falling from 41% to 32% sequentially. However, management is guiding for margins to rebound in coming quarters, as 4QFY25 saw some abnormally high margin recognition.

Note: we have stripped out allowances for receivables from our core numbers, as most of the amounts are reversed at the end of the financial year.

LSH 1QFY26 results snapshot

Revenue and NP trend

Margins eased in 1Q26

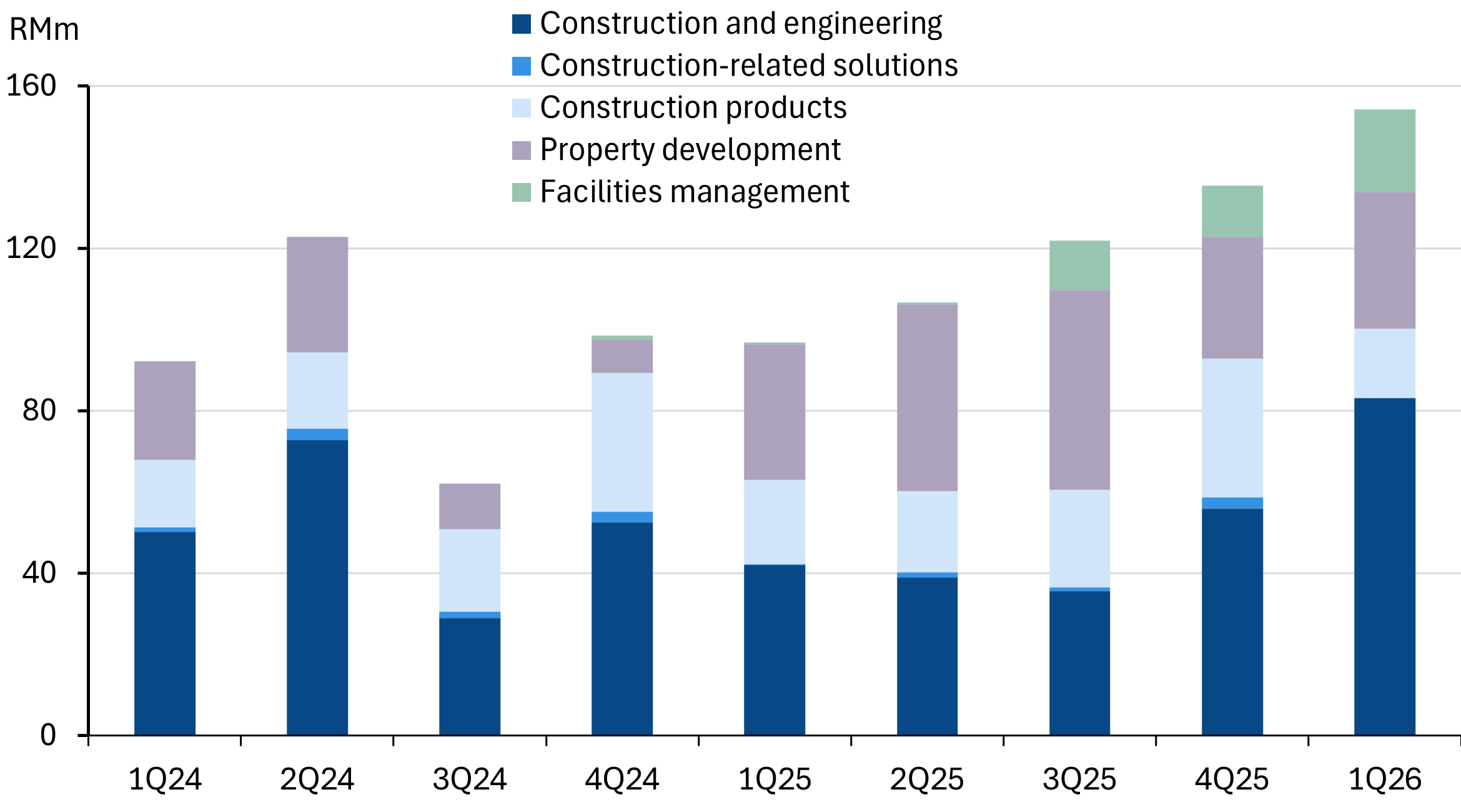

Segmental revenue

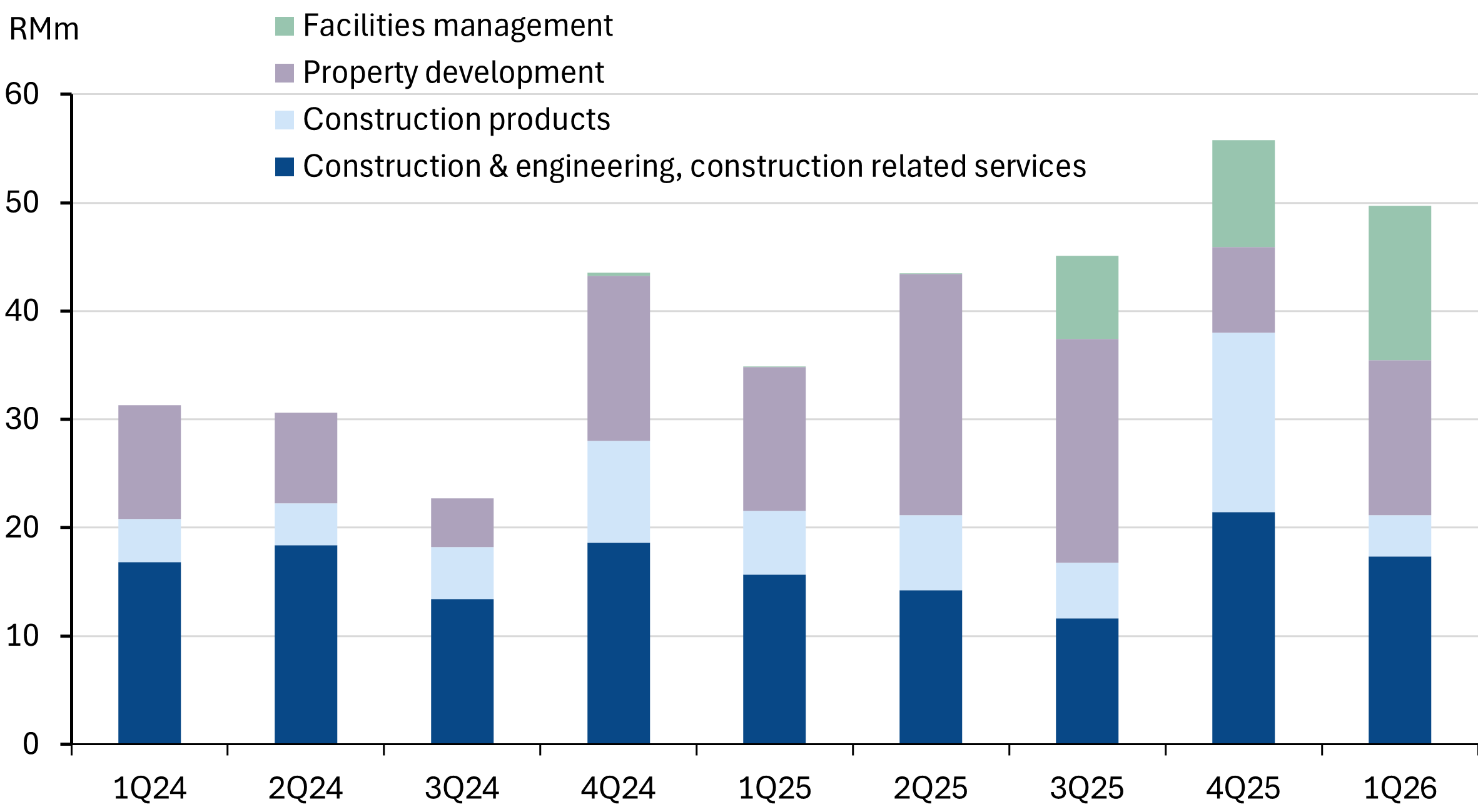

Segmental GP

Lower TP to RM3.00

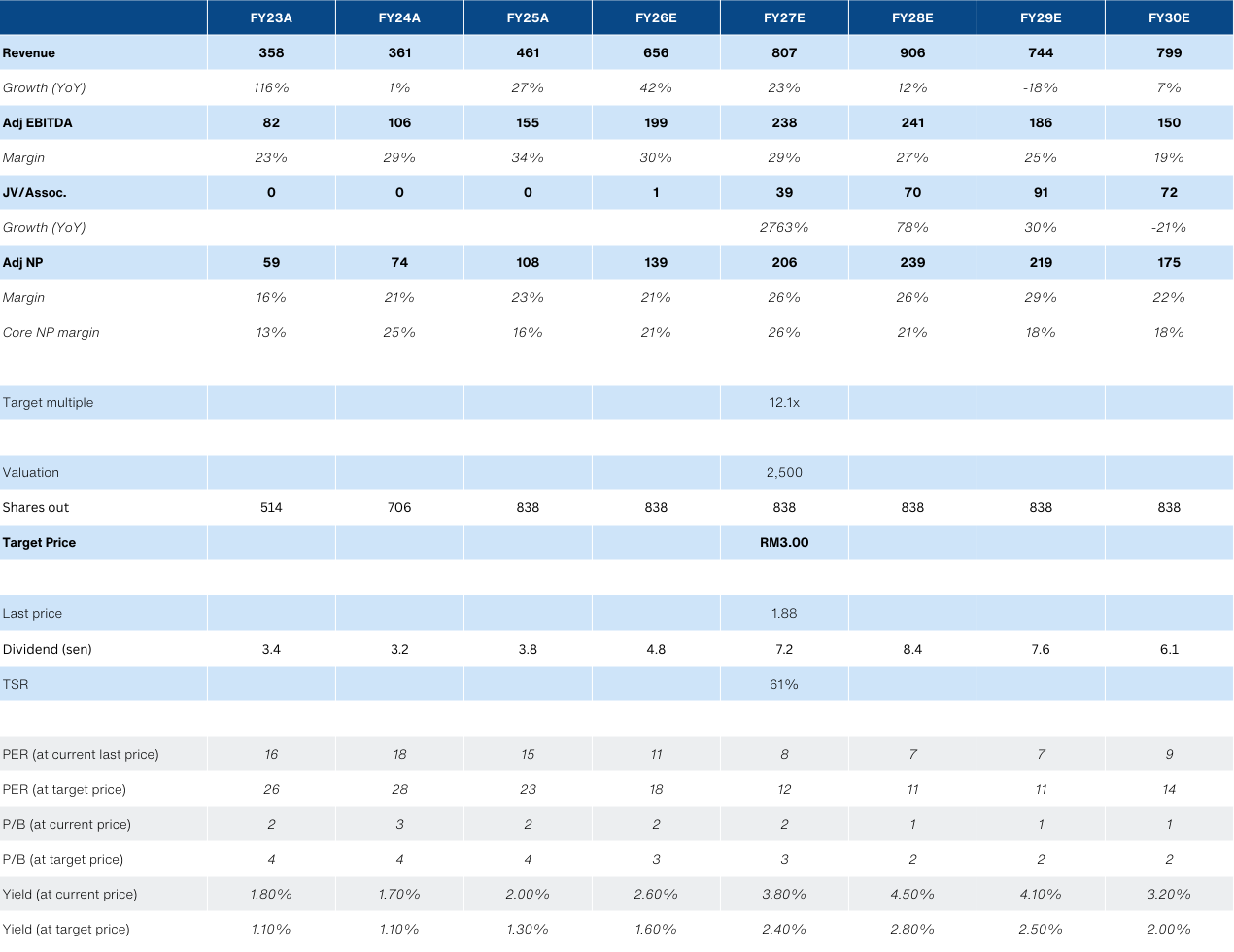

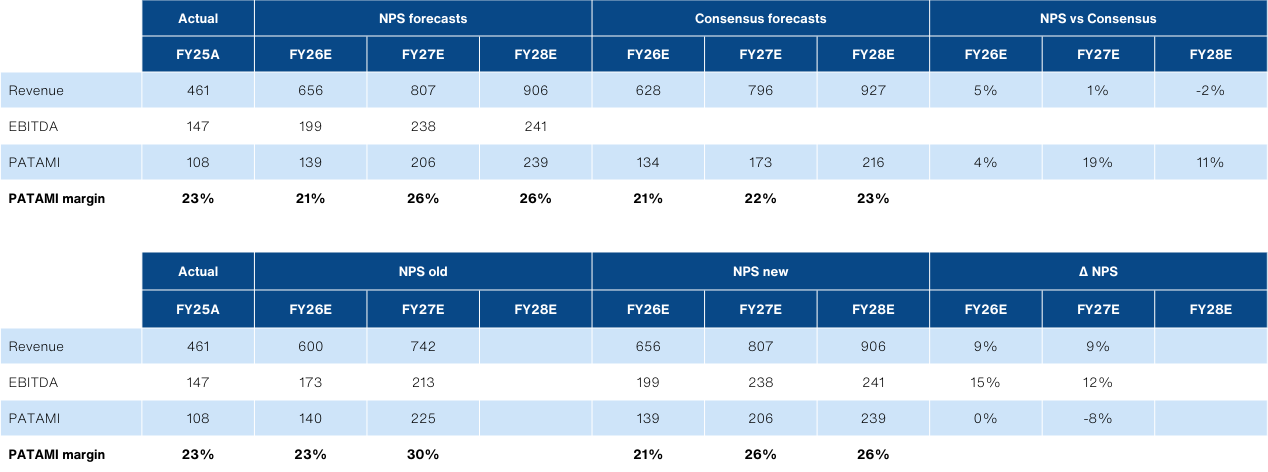

We lower FY27E earnings by -9% but keep FY26E unchanged. This reflects a more conservative view on timing of the infrastructure projects that LSH are pursuing - assuming execution is pushed out.

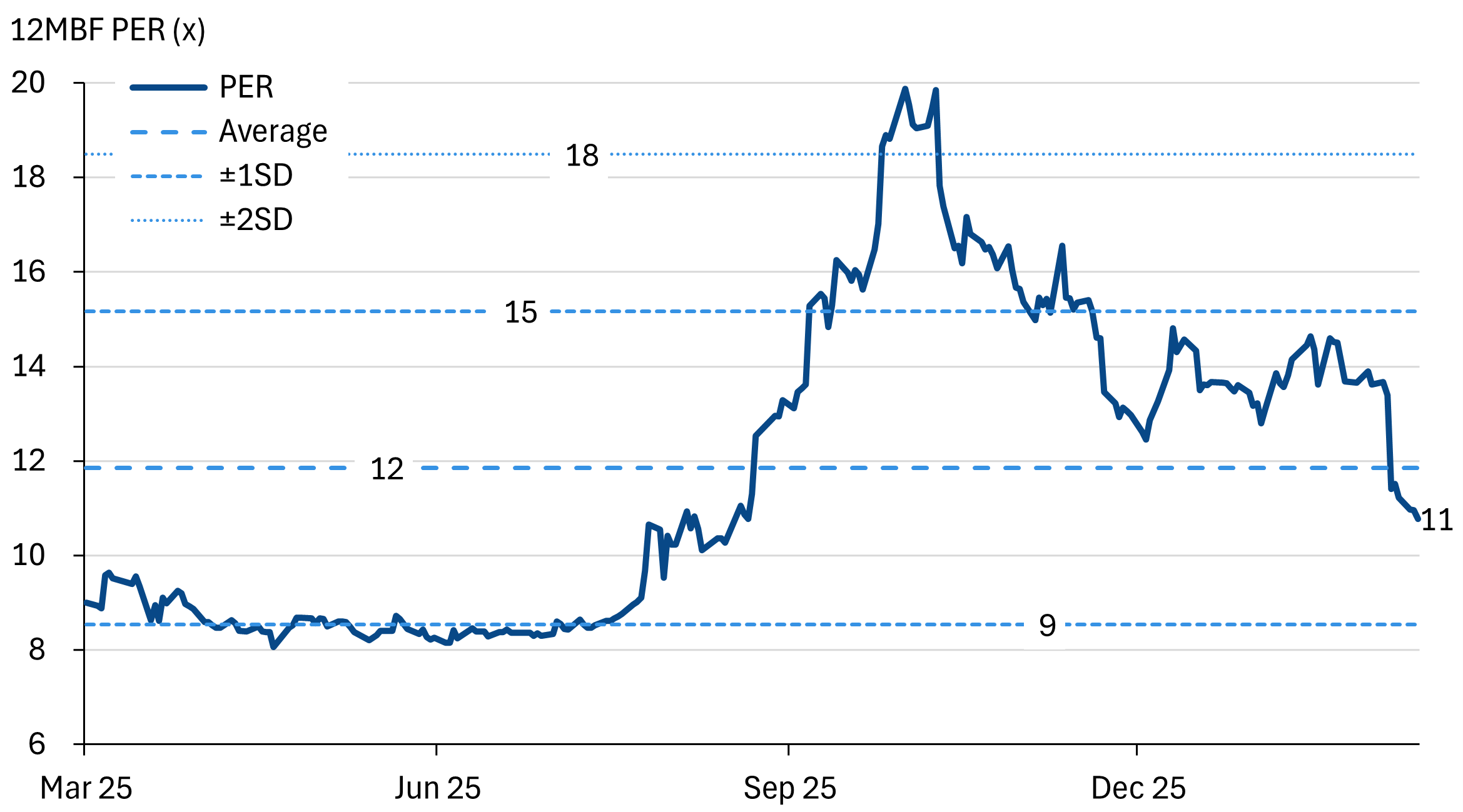

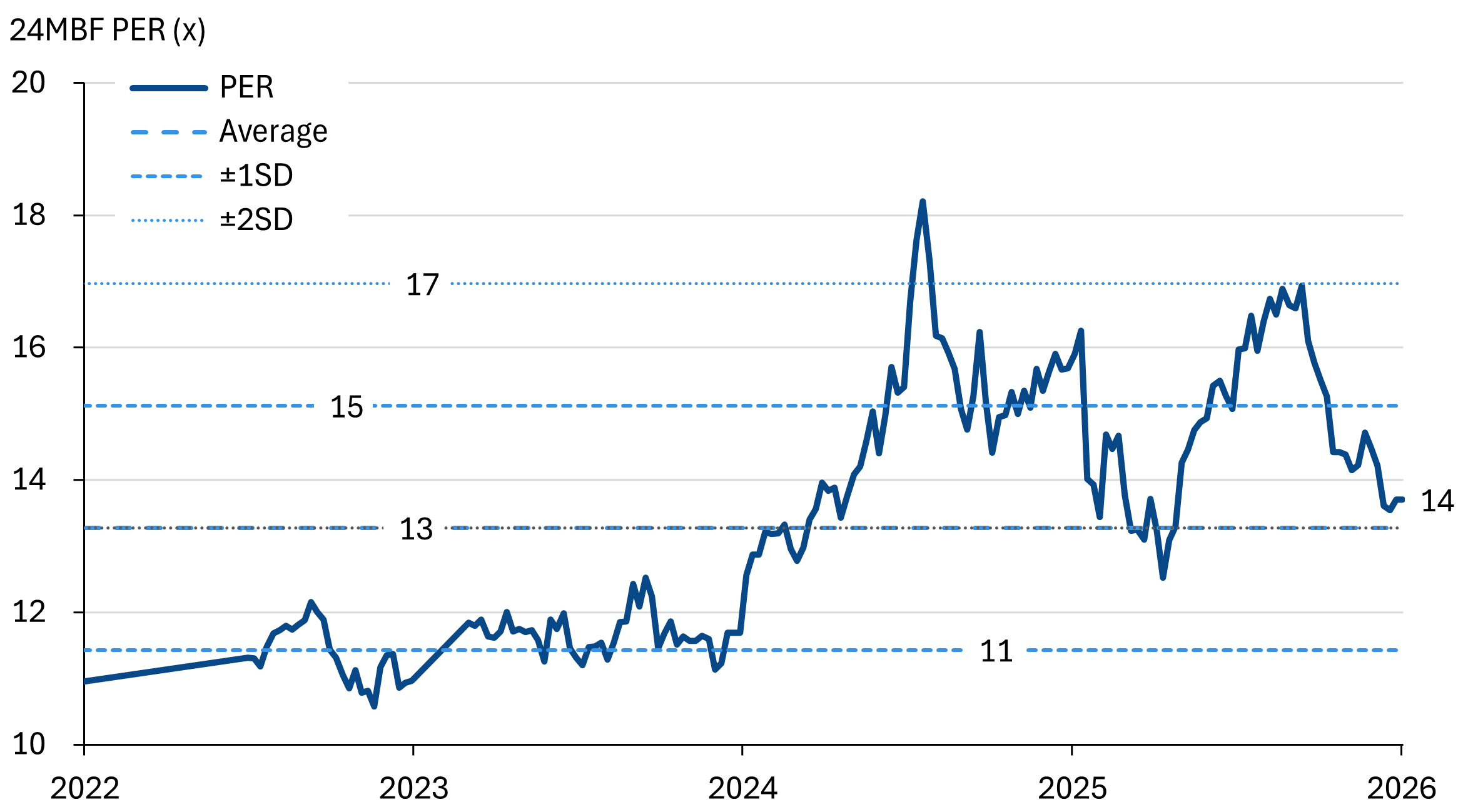

At the same time, we note the broader de-rating in the construction sector that has brought down 24MBF PER to 13x. We lower out PER target to 12x FY27E, which is -0.5SD vs the sector average. This translates to a TP of RM3.00, maintain BUY. The implied FY26E PER is 18x. However, we think this is justifiable given the +40% NP CAGR that LSH is poised to deliver.

Changes to earnings / Valuation methodology

Source: Company Data, NewParadigm Research, March 2026

LSH 12M blended forward PER | KL Construction Index 24m blended forward PER

Source: Bloomberg, NewParadigm Research, March 2026

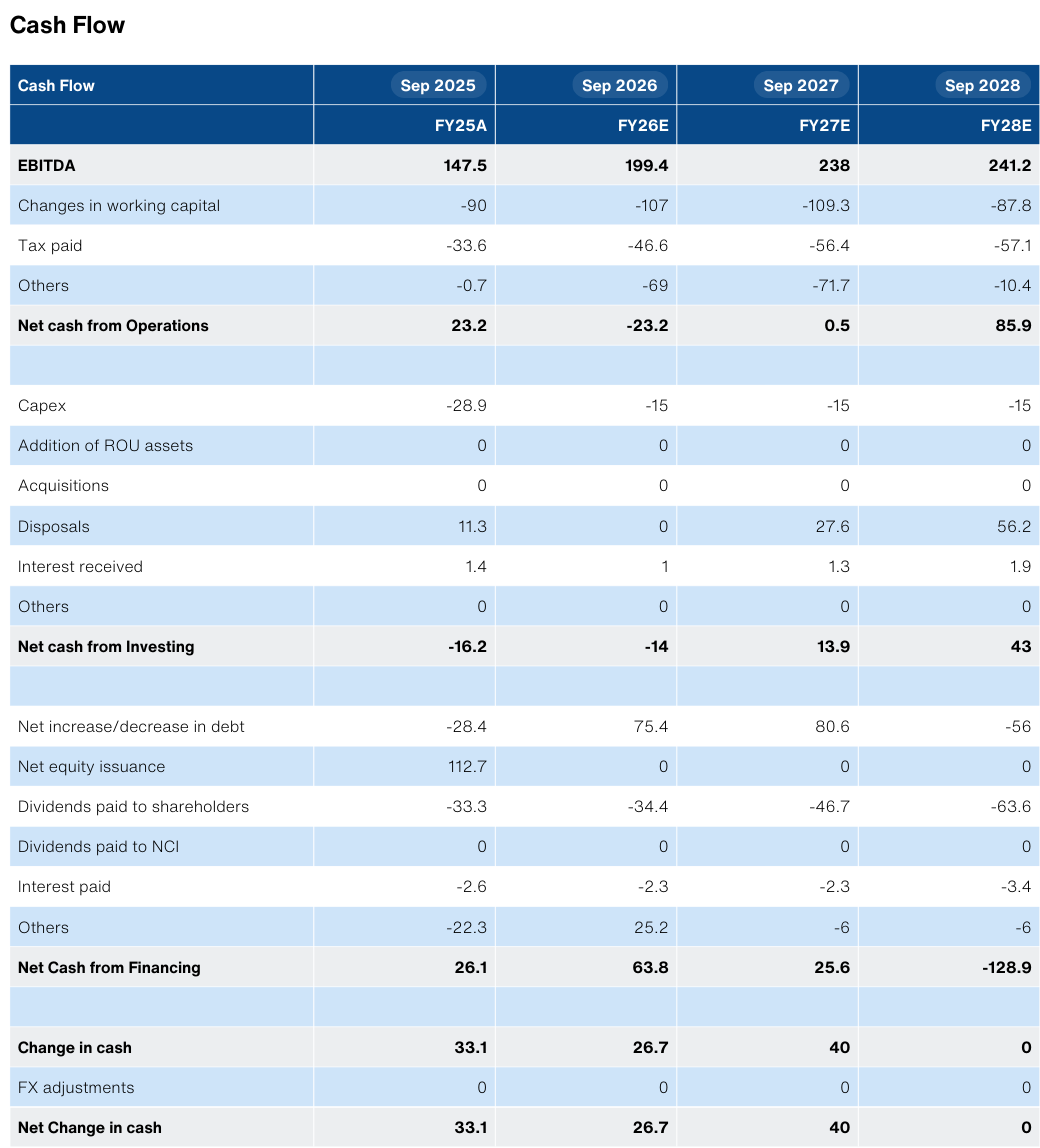

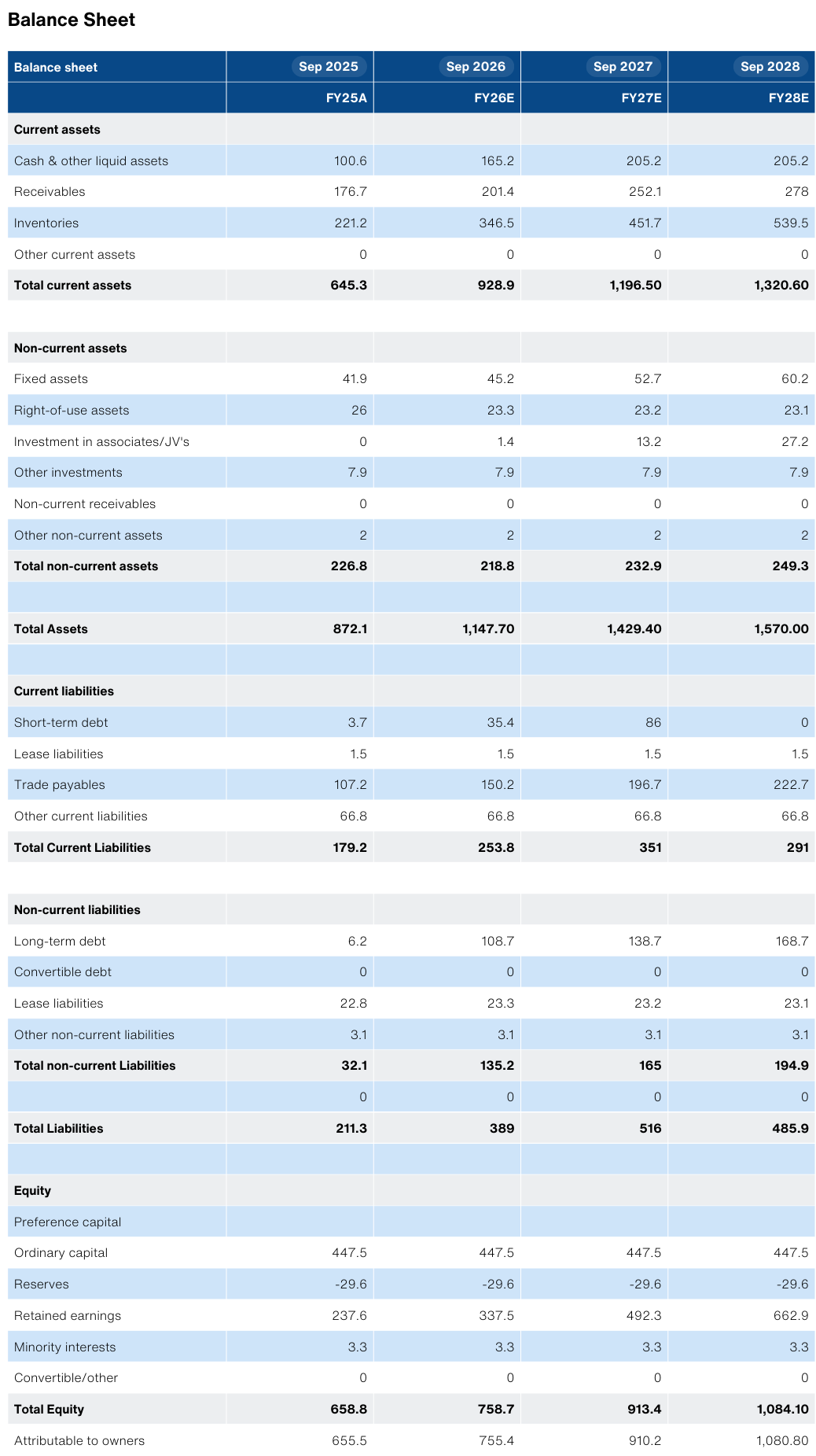

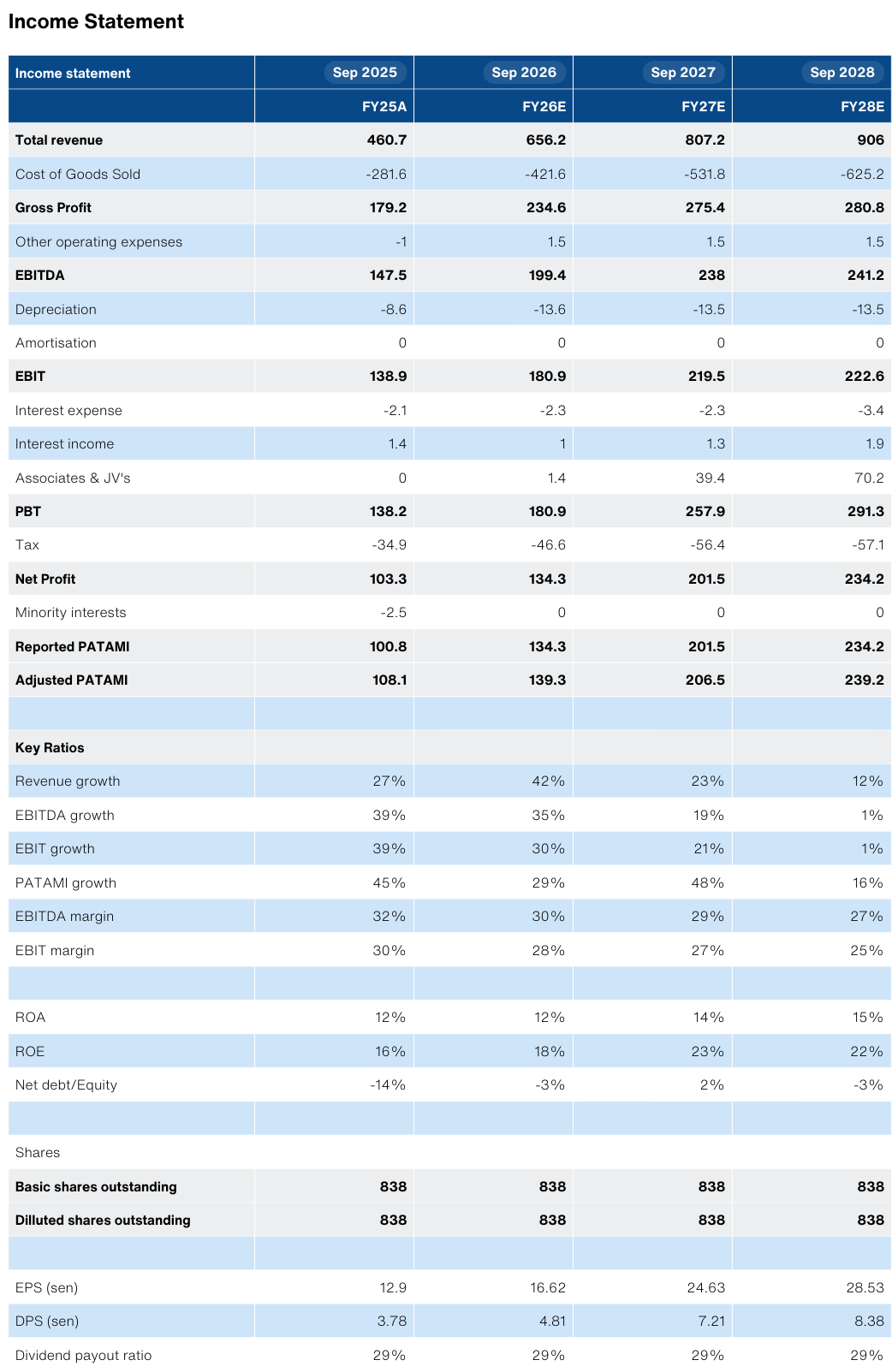

Selected financials

Source: Company Data, Bloomberg, NewParadigm Research, March 2026