Two ideas if the war goes long

Markets have begun to price in a protracted war.

Malaysia Strategy

Disclaimer: By using this information, you acknowledge that you are solely responsible for evaluating the merits and risks of any investment decision and agree not to hold NewParadigm Research liable for any damages arising from such decisions.

Key takeaways:

- What if the war goes long? Here are two stock ideas.

- MISC: Misplaced optimism. The tanker fleet is 73% on LT charters. We count ~5 VLCCs and 4 LNGCs that ply the Strait of Hormuz, with risk of force majeure for LNG operations.

- PMAH: The current supply disruption could get worse and PMAH is shielded from rising energy prices that hurt peers. Consensus expectations are low - only annualizing 4Q25's NP.

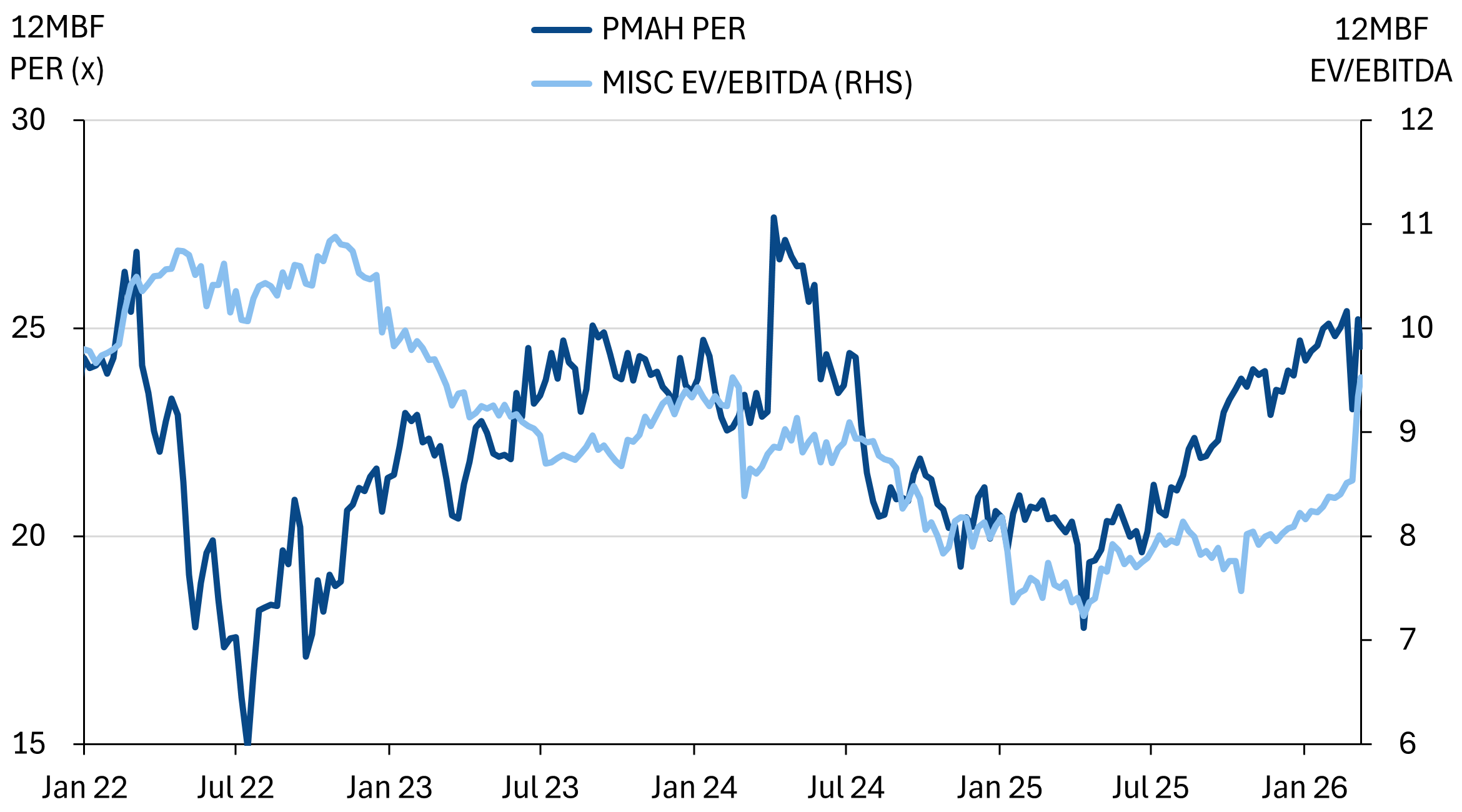

PMAH vs MISC valuations

Press Metal over MISC

- Oil prices are surging past US$100/bbl, as markets beginning to take a view of a protracted conflict. We won’t speculate the geopolitics, but our initial scenario analysis can be found here.

- We now identify two ideas, on the basis that the disruption in the Middle East runs long - we think Press Metal (PMAH) has more upside potential from aluminium supply disruptions while MISC is probably overbought on misplaced optimism.

MISC - Force majeure risks

- While MISC historically benefits from high tanker rates, the war has skewed rate upside to VLCCs, especially for the Middle East to China route. However, >80% of MISC’s VLCCs are on LT charters and almost all Aframax are deployed outside of the Middle East.

- The market also appears to be overlooking the force majeure invoked by Qatar Energy. MISC has a 25% stake in four LNGCs charted to Qatar Energy, with 8 more on delivery by next year.

- We estimate the potential loss of revenue from the existing LNGCs could be ~RM27m/quarter assuming a charter rate of US$75k/day for 25% stake across 4 vessels. Annualized, this would be a ~4% hit to earnings expectations.

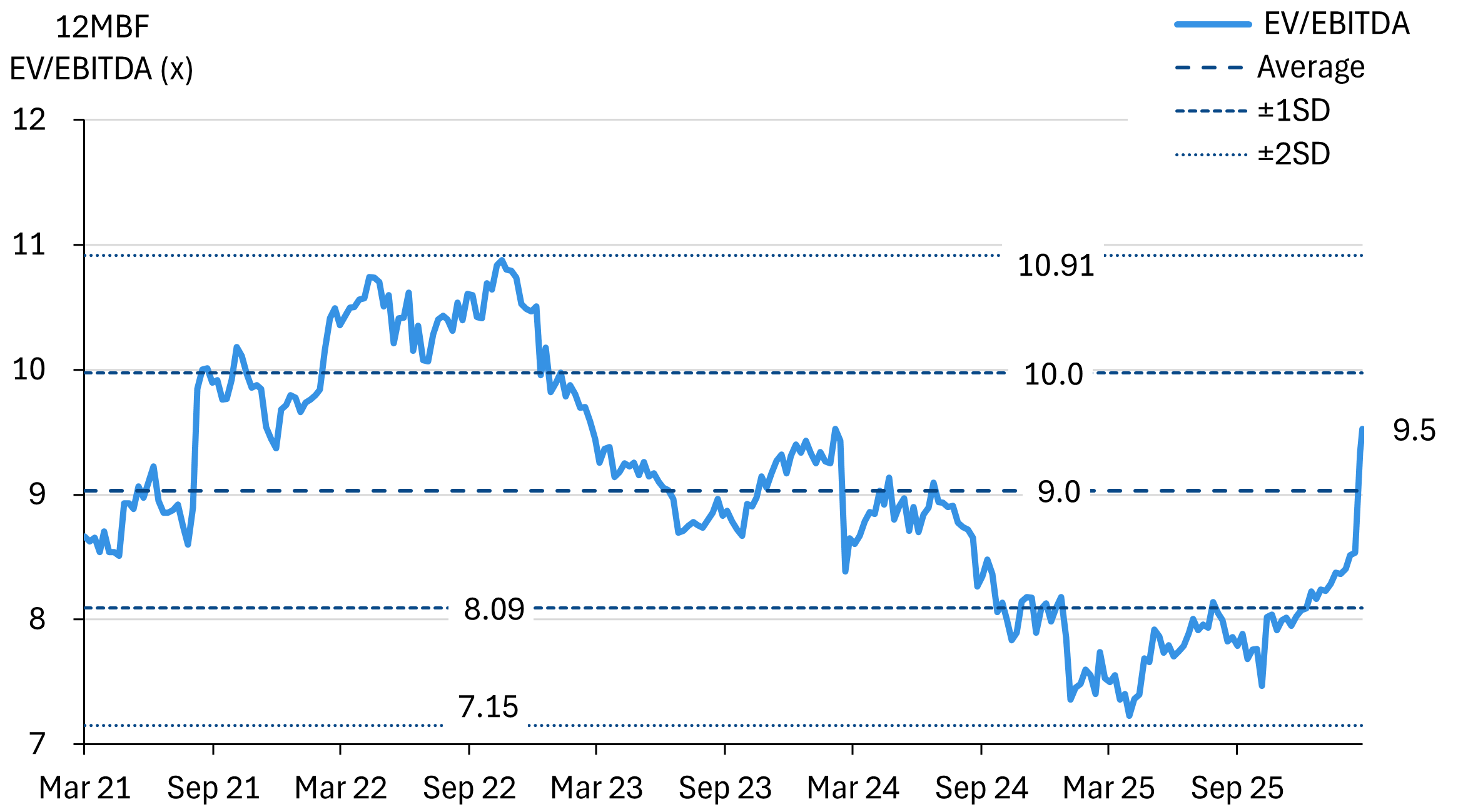

- Assuming a reversion to 8.1x EV/EBITDA (-1SD) with the aforementioned revenue loss annualized, we estimate MISC’s fair value would be RM7.20 (non-rated) vs last close of RM8.73.

PMAH - Double down on supply disruption

- A protracted war will further disrupt aluminium supplies and in a manner that is sticky and slow to recover. Qatar’s state-owned smelter has already taken out 648k MT from supply and will need almost 12 months to restart. But the Middle East has 4.3m MT capacity in total. Alumina supplies could be difficult to deliver as well, driving more shutdowns.

- Additionally, coal prices have risen +24%. PMAH’s own energy costs are fixed but higher electricity costs will hurt Chinese competitors.

- Assuming ~15% upside to consensus FY26 expectations would translate to a fair value of RM8.75 (non-rated) for the stock at 25.9x PER (+1SD vs 5-yr average). Last close price was RM7.49.

MISC - misplaced optimism

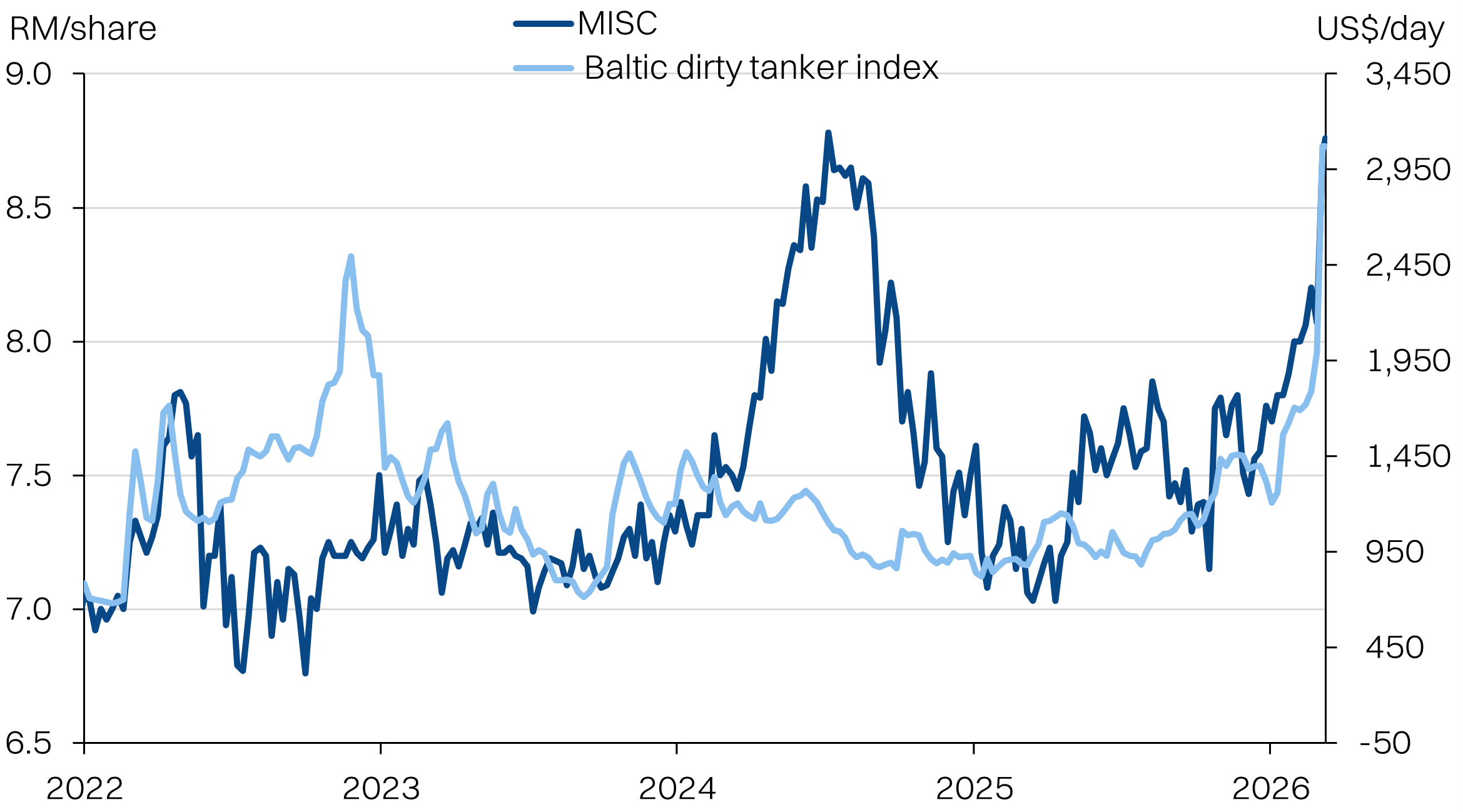

What happened: VLCC day rates for the Middle East-China routes have surged to over US$500k/day, due to increased geopolitical risk. As a result, MISC’s share price has jumped ~9%, to near-record highs. Market appears to be pricing-in ST tanker rates upside but ignoring energy supply disruptions.

What is different this time: MISC’s operating model is skewed towards long-term charters for its VLCC and LNG fleets. Only the Aframax fleet is skewed to spot market exposure, but it tends to operate outside of the Middle East. Unlike previous events that have driven global tanker rates, MISC may have less exposure this time around.

Downside: MISC has 4 LNG carriers servicing Qatar Energy that may see prolonged supply disruptions, with 8 more deliveries by 2027. MISC has VLCCs tied up in LT charters and may have vessels stuck in the Persian Gulf.

Upside: MISC’s LNGCs are released by the client and are able to secure ST charters at premium rates.

Market is pricing-in tanker rate-driven earnings upside for MISC

MISC EV/EBITDA bands

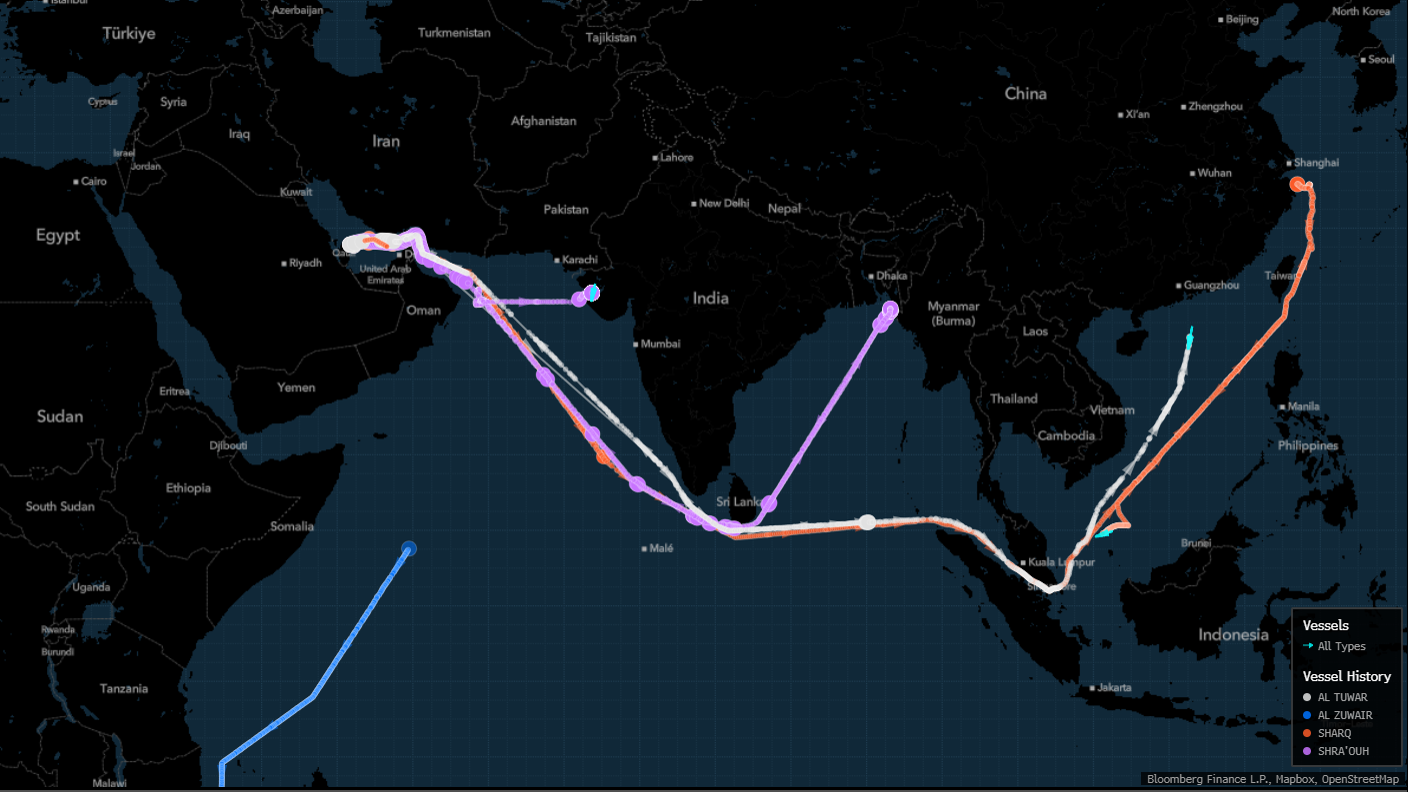

Qatar Energy’s force majeure risk on MISC’s LNGCs

MISC operates 41 LNG carriers. Of these, 4 are operated under a JV with NYK where MISC has a 25% equity stake - Al Tuwar, Al Zuwair, Sharq and Shra’ouh.

Qatar Energy has announced a force majeure event and shuttered LNG production. This has a direct impact on the aforementioned to generate revenue. News reports have indicated Qatar Energy will release as many as 10 of the LNGCs to the spot market, but the named vessels did not include any of MISC’s.

Additionally, this is part of a larger 12 vessel orderbook for MISC and partners, with 8 more deliveries slated by 2027. This means that the MISC could have the equivalent ~3 LNGCs (adjusting for 25% stake) or 7.5% of total fleet at risk, once the deliveries are completed.

In the medium term, Qatar Energy has indicated that it will take months to resume normal operations. Over the long term, any delays to the development of the LNG production and/or liquefaction infrastructure could hurt MISC’s LNGC earnings.

28D movements: MISC has 4 LNGCs (25%-owned) that service Qatar LNG

28D movements: The rest of MISC’s LNGCs operate in Asia Pacific

Can spot rates cover potentially trapped VLCCs?

MISC can benefit from the high VLCC spot rates, which have surged to record highs of US$500k/day for the Middle East-China routes.

However, MISC has an 80% term-spot ratio for VLCCs, limiting opportunities to capture the rate upside. Additionally, MISC is a highly risk-averse operator, and is unlikely to place assets and crew in danger by navigating the Strait of Hormuz without clear indication the danger has passed.

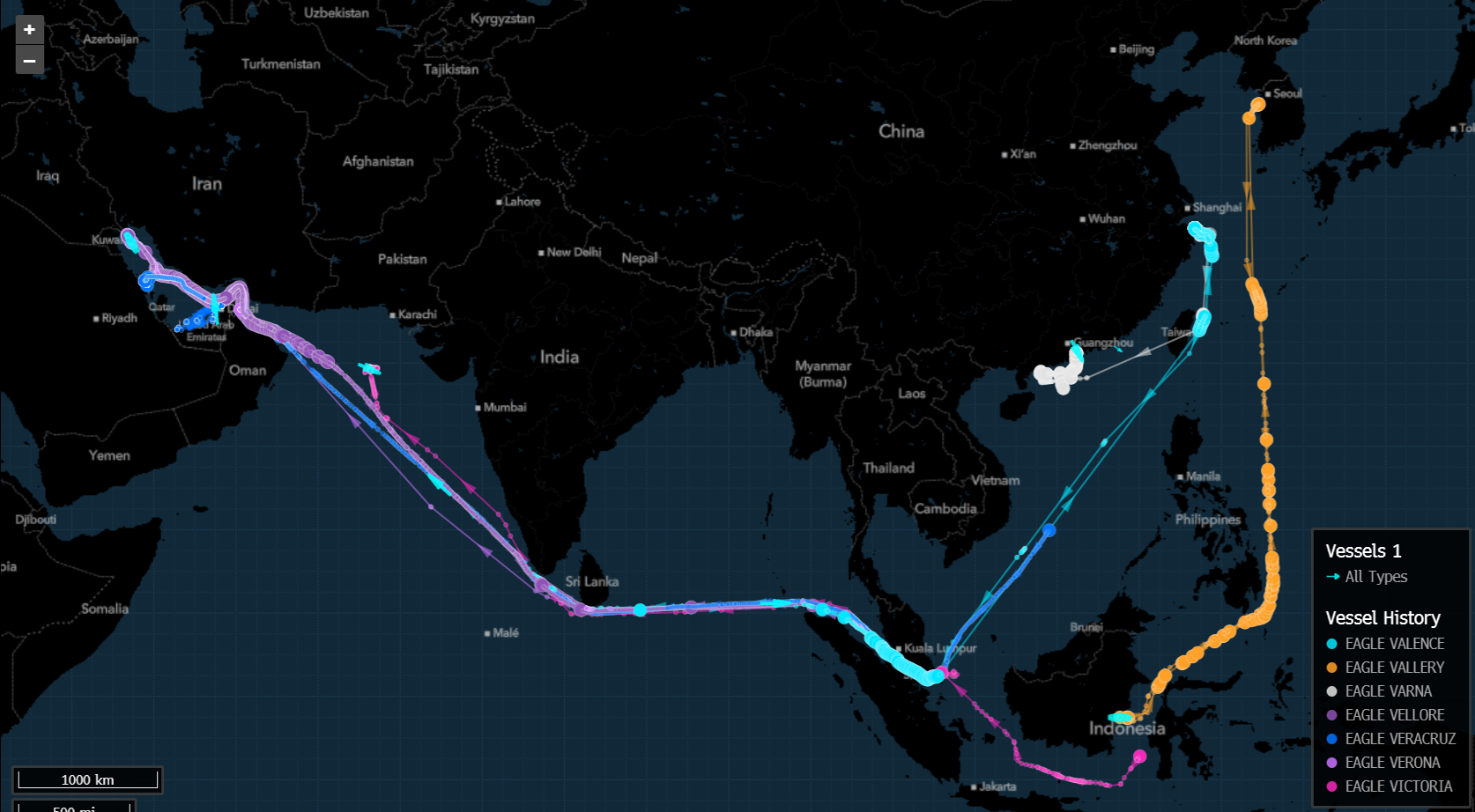

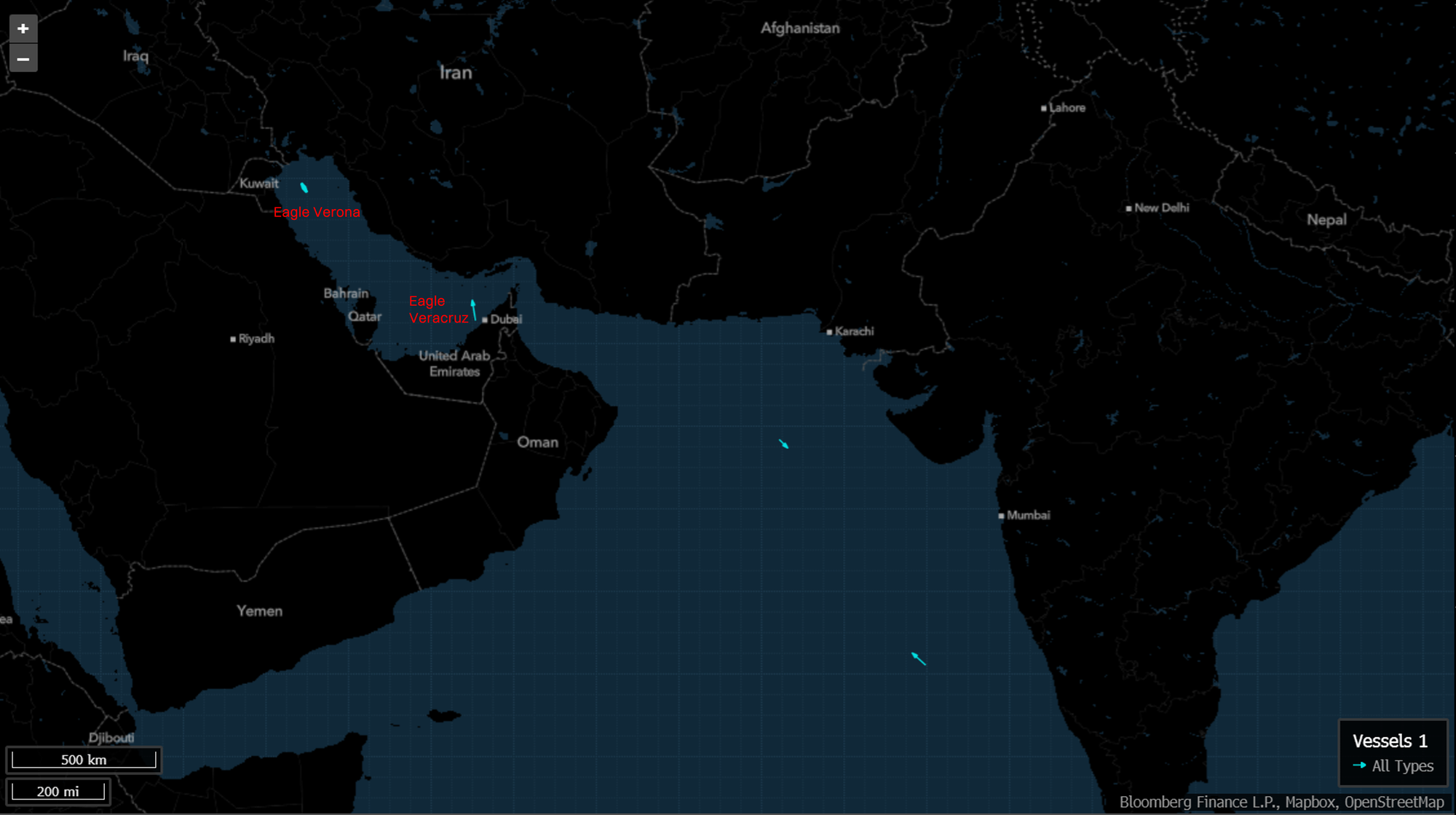

Compounding matters, Bloomberg maritime maps data shows that MISC may have up to five of its VLCCs that service the Middle East-China routes. Of these five vessels, two appear to service this corridor frequently and the other three intermittently through the year. Notably, the “last 30 days” tracking data shows two vessels - Eagle Verona and Eagle Veracruz, could still be located within the Persian Gulf.

We think the ST benefit of the higher tanker rates could be limited. Meanwhile, the LT downside risk from trapped vessels is not being priced in.

28D movements: MISC has up to 5 VLCCs that ply the Strait of Hormuz

30D last seen: MISC has potentially two VLCCs in the Persian Gulf

PMAH - Supply disruption can be sticky

PMAH is potentially one of the best beneficiaries of a protracted disruption to aluminium supplies.

The Middle East accounts for about 10% of global aluminium production and there is already a supply shock. Qatalum (Qatar state-owned) is already shuttering production (648k MT/yr) and could take up to 12 months to restart.

With the potential for other smelters to shutter production, compounded with the difficulty delivering alumina, we foresee room for supply to tighten further.

Against this backdrop, aluminium prices are up +16% YTD. PMAH does sell forward about 65% of its production. But if 35% of volumes are sold at US$3,400/MT, that would translate to a ~15% upside to the US$2,600/MT average realised prices in 2026.

Market expectations are also mixed, with consensus forecasting PMAH FY26E NP of RM2.48bn, which is roughly the 4Q25 result of RM605m annualized. We anticipate another 10-15% upside to consensus expectations.

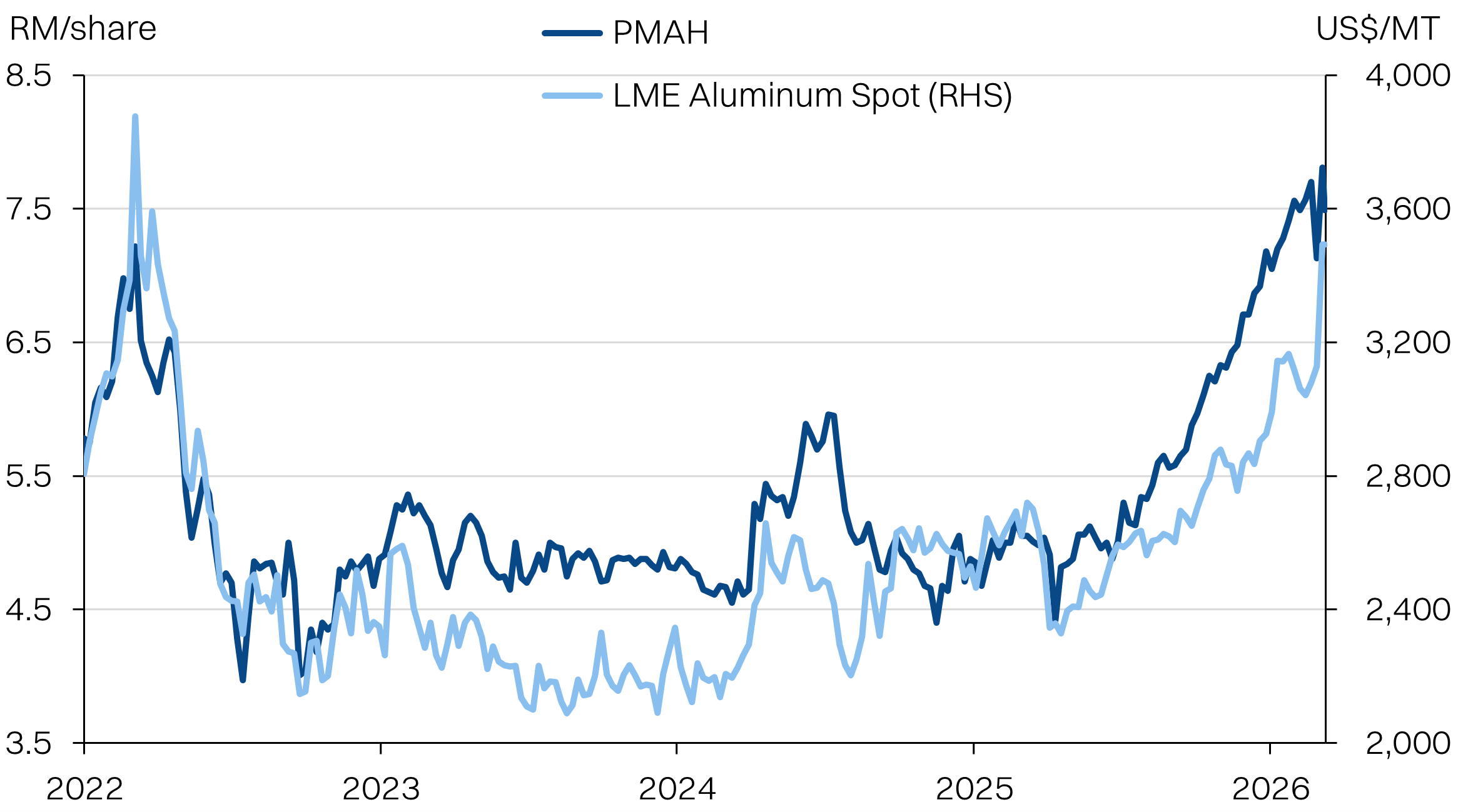

PMAH share price tracks aluminium prices closely

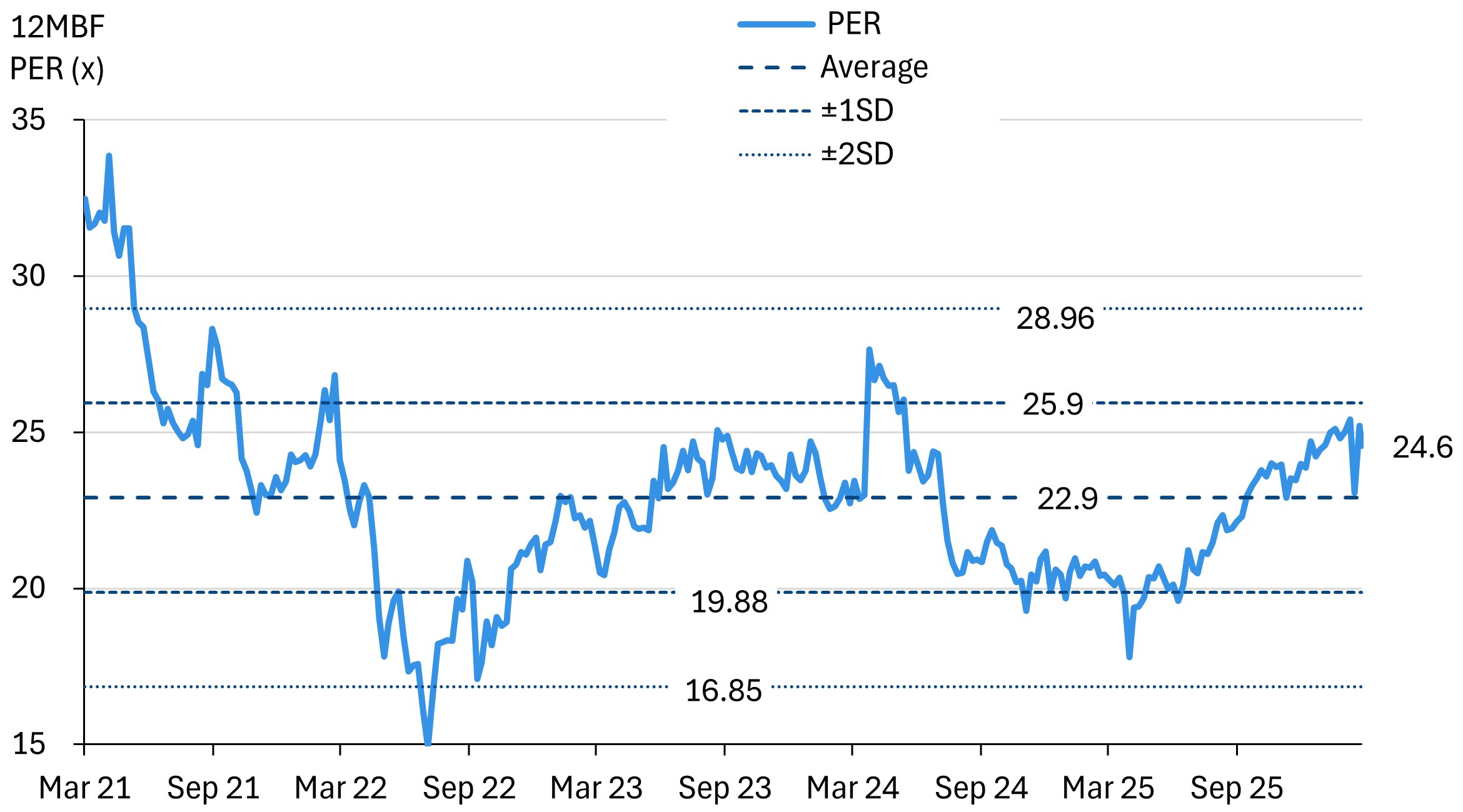

PMAH valuations are still below +1SD

Hedged against energy price inflation

Energy price inflation may not be as pronounced as it was in 2022, when coal prices spiked due to sanctions on Russian coal - especially for Chinese smelters. Nonetheless, we anticipate that there could be more energy prices pressure that could lift coal prices.

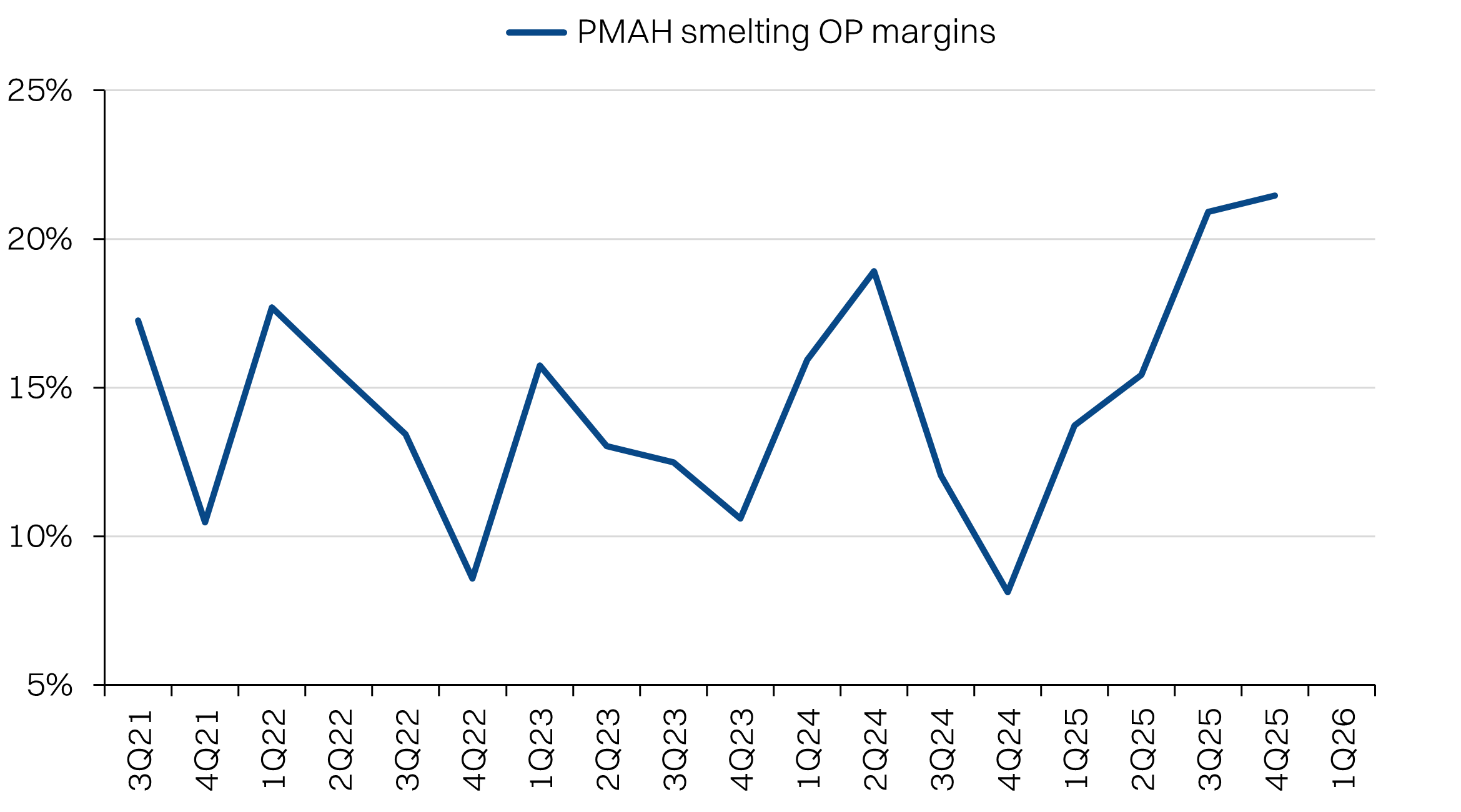

Electricity accounts for 40% of smelting costs, and PMAH has the distinct advantage of a fixed tariff thanks to the power purchase agreement tied to Bakun dam. We see this as a potential longer-term tailwind, given that energy supplies, especially gas, continued to be disrupted. For now, coal prices have already spiked by 24% YTD.

To be clear, we see further smelter shutdowns as the primary catalyst for PMAH. The Middle East produces about 4.3 million MT annually, and only ~16% of that capacity has been shuttered. In turn, further supply tightness will drive aluminium prices.

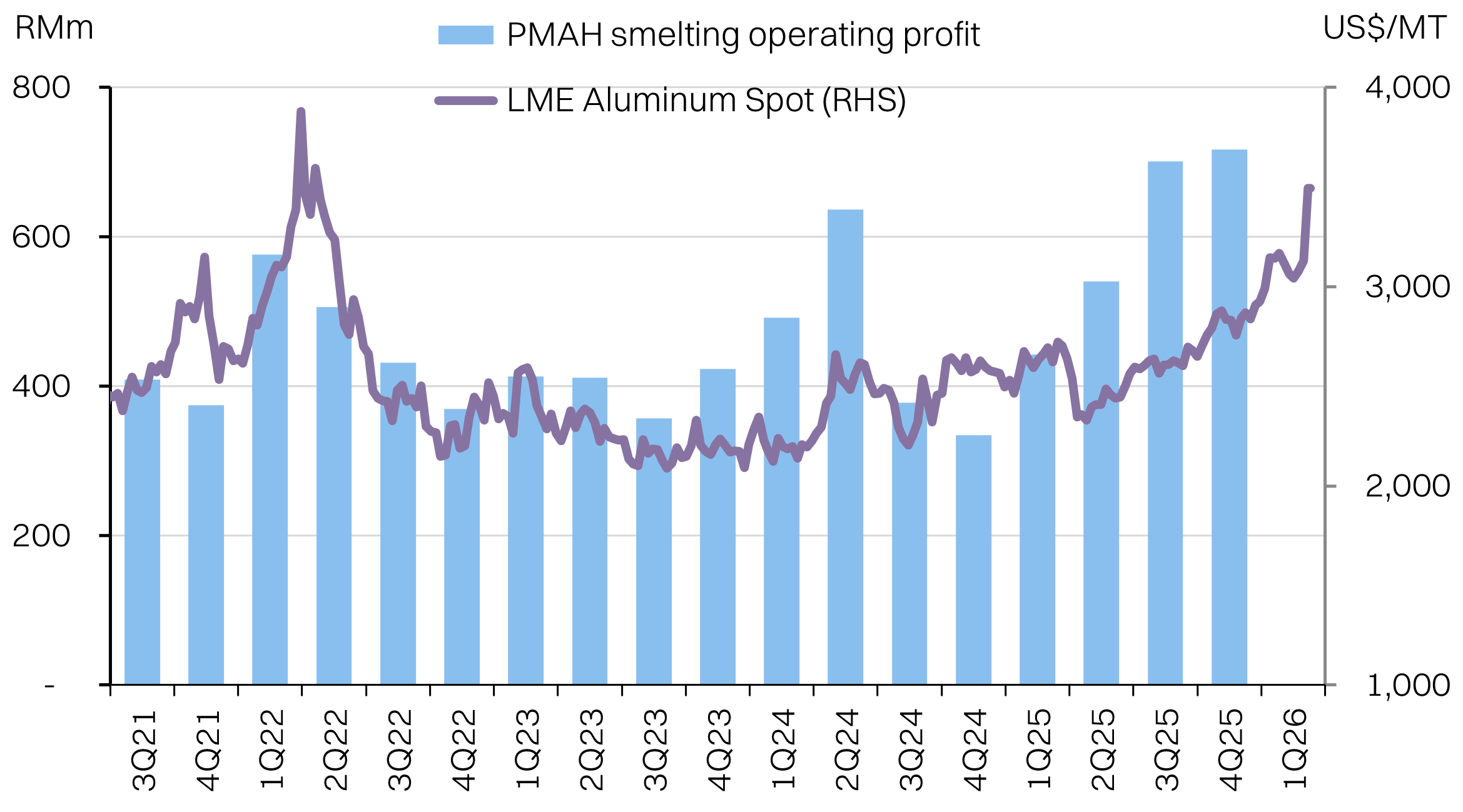

PMAH smelting profitability vs aluminum prices

PMAH should enjoy further margin expansion