Long-term downside risks emerging

MISC has 4 LNGCs chartered to QatarEnergy.

Malaysia Strategy

Disclaimer: By using this information, you acknowledge that you are solely responsible for evaluating the merits and risks of any investment decision and agree not to hold NewParadigm Research liable for any damages arising from such decisions.

Key Takeaways:

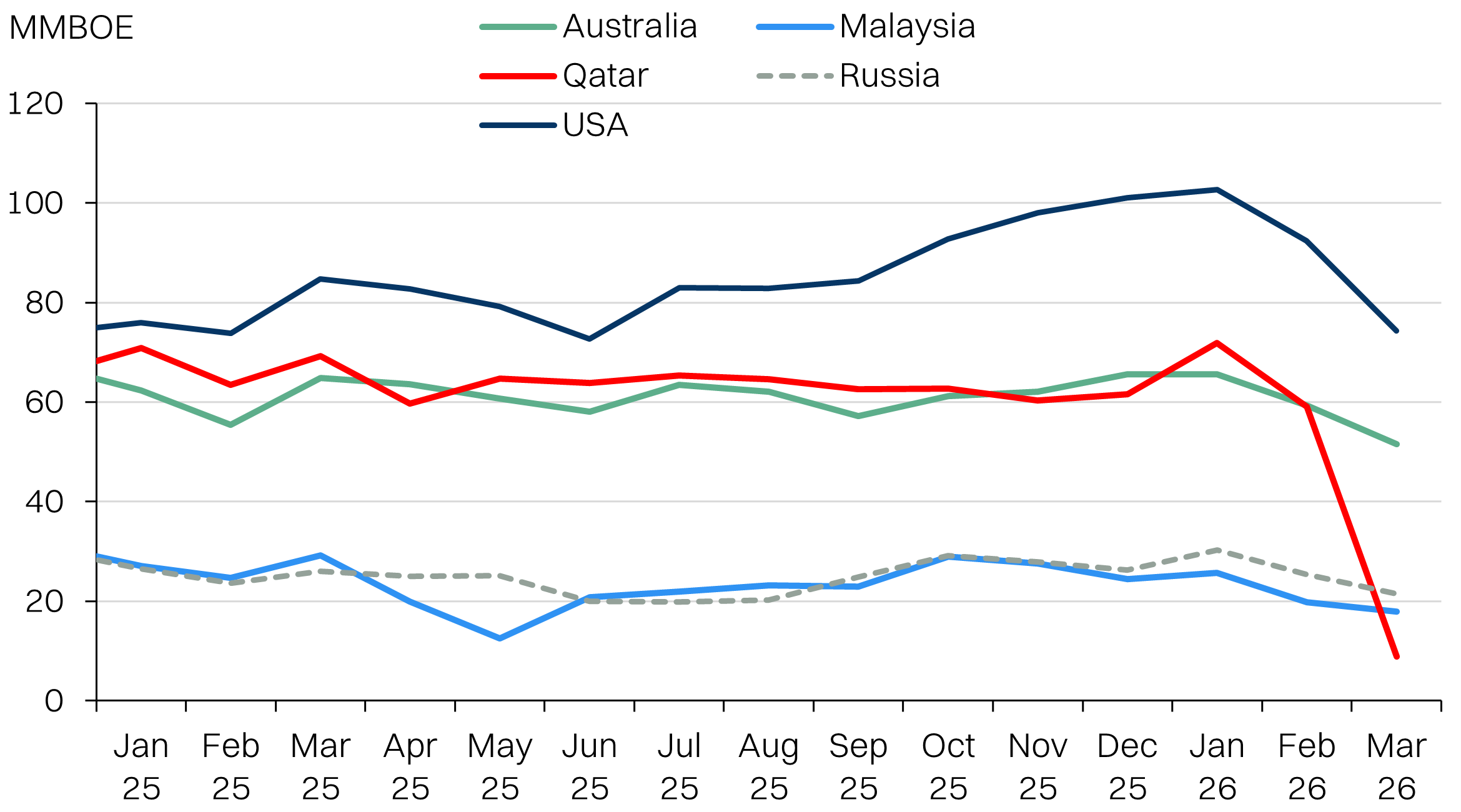

- The Iranian missile strikes on Ras Laffan has damaged 17% of QatarEnergy’s LNG production for 3-5 years. Force majeure risks are turning LT for MISC’s 4(+8) LNGCs serving Qatar.

- Tanker rates outside the strait are stabilizing at lower levels despite recent hostilities, limiting spot tanker rate upside.

- We reiterate our fair value (non-rated) of RM7.20 for MISC, on 8.1x (-1SD) EV/EBITDA.

MISC redirected one Qatari LNGC to the US | Tanker rates are normalising | MISC T3yr valuations

Source: Bloomberg, NewParadigm Research, March 2026

Damage to QatarEnergy will take years to repair.

- Iran’s missile strikes have damaged trains 4 and 6 of Ras Laffan, impacting 12.8m mtpa of capacity - about 17% of QatarEnergy’s exports and QatarEnergy has confirmed the repairs will take 3-5 years to complete. The force majeure risks are shifting from ST (strait closure) to LT (damaged capacity).

- MISC has exposure (via 25% JV) 4 LNG carriers that have long-term charters with QatarEnergy. There are another 8 LNGCs due for delivery by 2027 that could also be affected if QatarEnergy is not able to operate at planned capacity.

- On a positive note, one of the four LNGCs (Shra’ouh) has been diverted to the Sabine Pass, US. It appears to have been released from the time charter with QatarEnergy to pursue opportunities in the spot market.

Tanker rate upside is fading

- MISC’s skew to LT charters means it has relatively low leverage to ST spikes in tanker rates. And now, that rally is fading. In particular, the rates outside of the Persian Gulf have begun to normalise towards pre-war levels due to capacity constraints on demand and increasing supply from re-routed vessels.

- Historically, tanker rates have been a strong driver for MISC’s share price performance, but earnings transmission from this rally should be especially soft since MISC eschews risky routes like the ones that are driving benchmark rates.

Valuations have downside risk

- Market will have trouble quantifying the impact of QatarEnergy’s disrupted production on MISC’s LNGCs, but directionally the impact will be negative and substantial.

- Risk remains tilted to the downside as well, as the longer the war drags on it delays LNG exports while risk for more damage to production facilities remain.

- Our fair value (non-rated) of RM7.20 is based on 8.1x EV/EBITDA, which is -1SD vs the 5yr average.

Emerging LT risks to Qatari LNGC demand

- MISC via a 25% JV with a consortium including Japan’s NYK, operates a fleet of 4 LNGCs under a long-term charter with QatarEnergy.

- This is part of a broader 12 vessel program with another 8 LNGCs due for delivery by 2027.

- As it stands, the QatarLNG has already declared force majeure due to the inability to export LNG due to the closure of the Strait of Hormuz. But following the missile strikes that damaged train 4 and 6 (March 18/19), QatarEnergy indicated that the force majeure could be longer term. The estimated time to repair both trains is around 3-5 years, and that is assuming the conflict ends sooner than later.

- This does not include delays to the the North Field expansion program that was designed to increase output from 77 mtpa to 142 mtpa by 2030. Work on the North Field expansion has been suspended due to the hostilities resulting in delays of at least one year.

- It is highly unlikely that the combined impact of the delays and the damaged LNG trains will allow LNGCs to operate at the intended utilization. The best case scenario, will be QatarEnergy honoring some base payment under the LT charter agreement, even if the vessels are under-utilized.

- In this scenario, LNGCs would still suffer lower effective charters but some of the financial impact will be mitigated by minimum payments.

- However, if exports are impacted by multi-year production disruptions, QatarEnergy may release said LNGCs to undertake opportunities in the spot market. Bloomberg data suggests that one of MISC’s vessels - Shra’ouh, has already been diverted to Sabine Pass, US, to pick up a cargo.

- On balance, effective charter should be depressed in such an environment, given the increased supply of LNGCs released into the relatively shallow spot market.

MISC currently has 4 LNGCs chartered to QatarEnergy (25% stake)

Financial impact

- Regardless of the aforementioned scenarios, the most likely outcome of QatarEnergy’s longer-term production disruption will be impairments to MISC’s assets as well as lost revenue.

- Note that these LNGC’s are held as an associate stake under equity accounting.

- The LNGCs contracted for QatarEnergy have an estimated newbuild price of US$230m (link). MISC’s exposure for the existing vessels in service would be roughly that amount (4 vessels, 25% stake).

- We estimate a 3-year impairment to said contract would have an impact of ~RM100m. This excludes the 8 to-be-delivered vessels that might increase the impairment amount three-fold.

- Based on 25% stake in 12 vessels at US$230m/vessel, MISC’s carrying value at risk of impairments would be ~US$690m or RM2.8bn.

- Based on charter rate of US$80k/day, the potential lost revenue for the existing vessels (25% stake) would be about RM110m/yr.

LNG exports: Qatar’s exports have fallen sharply due to the war.

MISC has 8 more LNGC deliveries chartered to QatarEnergy

Segmental breakdown

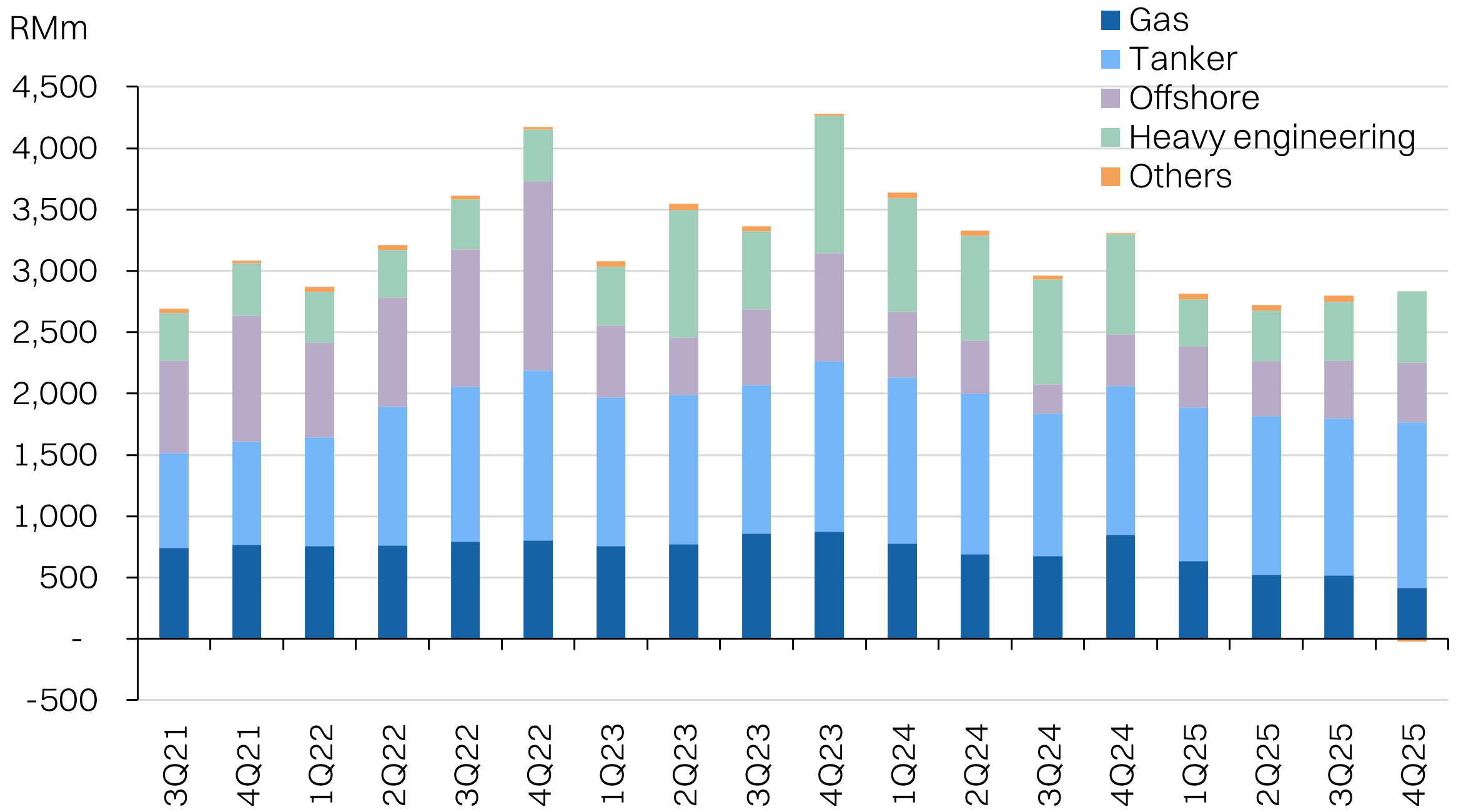

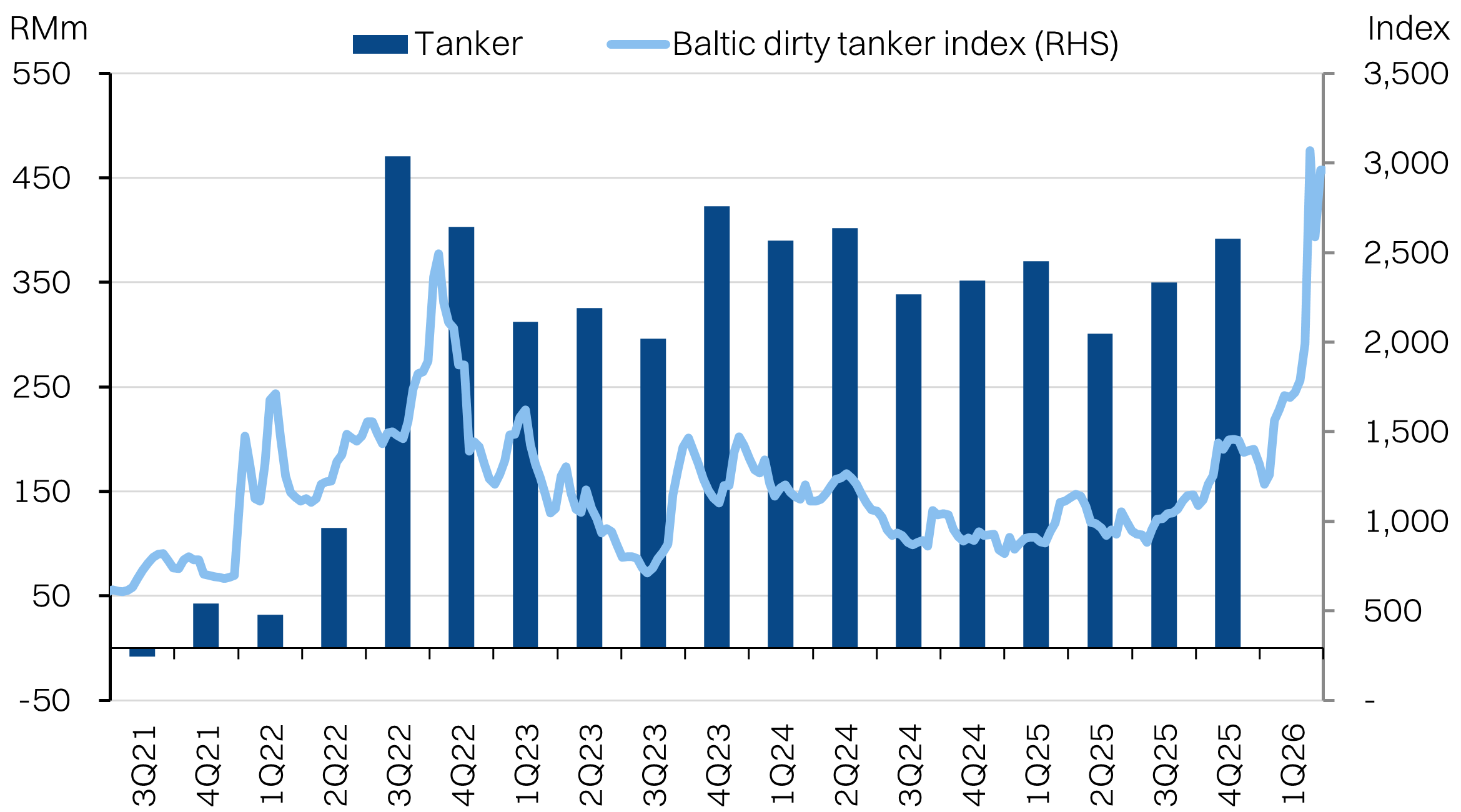

- While MISC has historically been known for its LNG segment, seeded by its parent, Petronas, the group has become increasingly reliant on the tanker segment in recent years.

- While 4Q25 is not representative due to some one-off impairments in the Gas segment, broadly, contributions from gas have fallen from ~40% of operating profits to ~30%.

- In turn, market has shifted more focus to tanker rates when assessing MISC’s outlook, given it contributes ~50% of operating profits. Note that this is also skewed by the shift in LNG earnings recognition into the associate contributions which is not captured in these segmental figures.

MISC segmental revenue - gas falling on aging vessels and shift to associate recognition

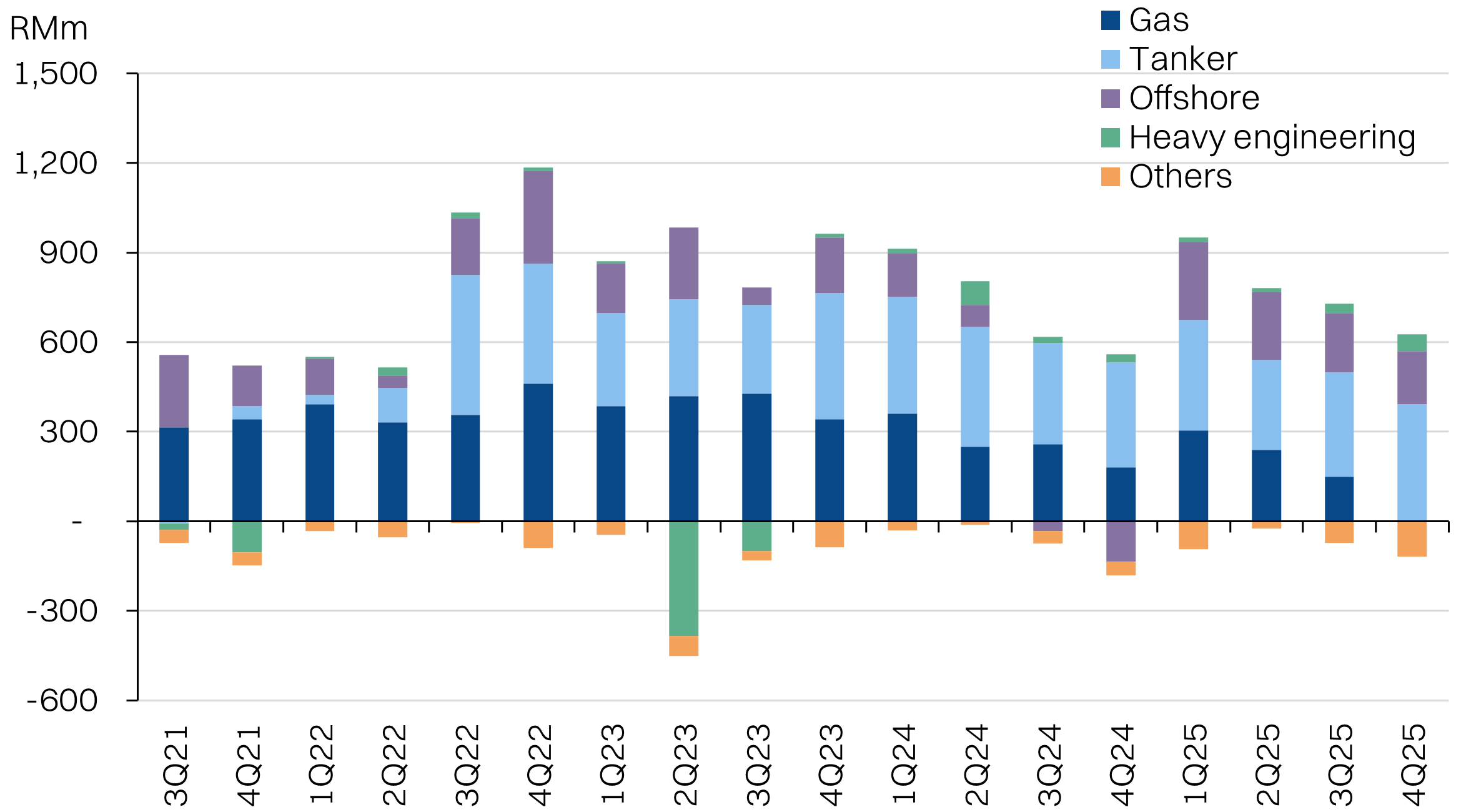

MISC segmental operating profit - tanker dominated in recent quarters

Segmental breakdown

- With a term to spot ratio of 73% for the tanker fleet, MISC has historically enjoyed a more modest earnings correlation with tanker rates.

- Tanker rates would have to remain elevated for a prolonged period for MISC to enjoy the benefits on charter rollover.

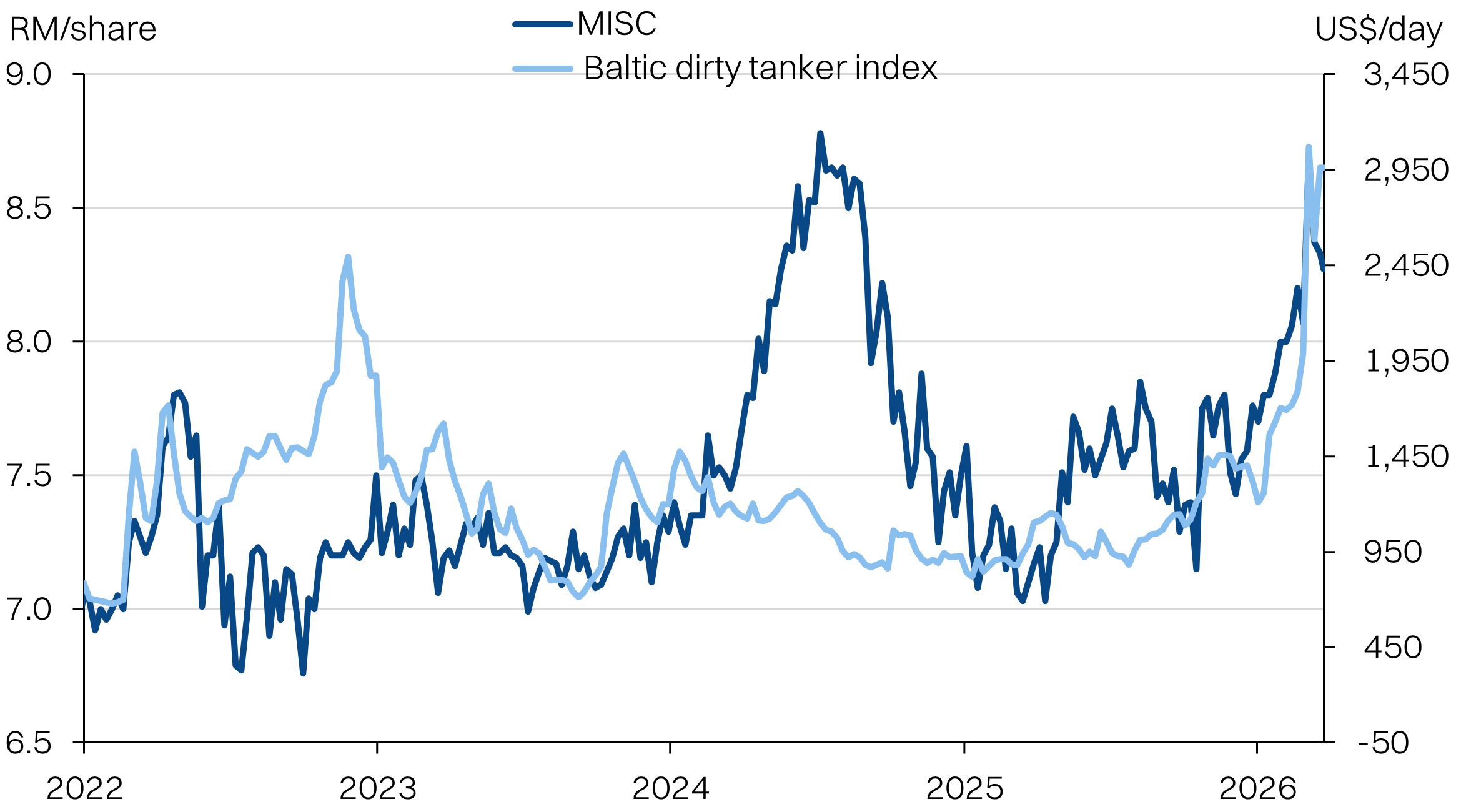

- Nonetheless, the recent share price performance appears to be more closely linked to the tanker rates.

MISC’s tanker segment OP vs BIDY - modest correlation

MISC’s share price vs BIDY - stronger correlation in 2026

But tanker rates are normalizing

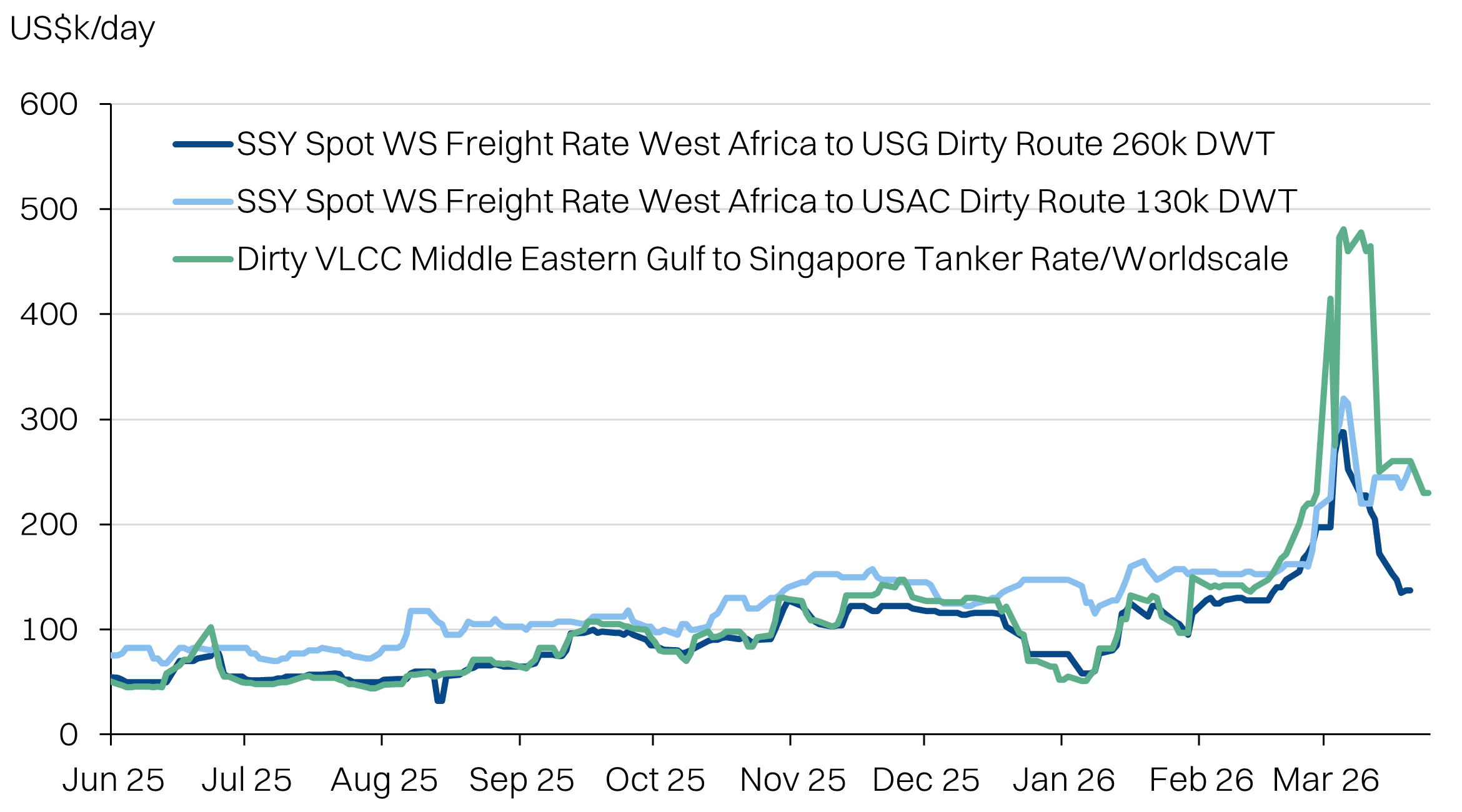

- Unlike previous rallies in tanker rates, the closure of the Strait of Hormuz has had a disproportionate impact on routes from the Persian Gulf to reflect the elevated risk and demand.

- However, most other routes will not benefit from the Strait’s closure. If anything, redirected supply of tankers to other routes should deflate charter rates - especially if there isn’t a corresponding lift in demand.

- Some routes, like West Africa to the US have already corrected to pre-war levels.

- At least for MISC, we anticipate that this will cap upside from MISC’s tanker fleet that primarily operates outside of the Persian Gulf.

Tanker rates - Outside the Persian Gulf, rates are beginning to normalise

MISC is trading at +1SD vs trailing 3yr EV/EBITDA