Stonepeak project on the horizon

Upgrade TP to RM0.86 to reflect iHandal acquisition.

Stock information

KJTS

KJTS | 0293.KL

BUY

Target price: RM0.86

Last price: RM0.76

Market cap (RMm): RM525m

Shares out: 691m

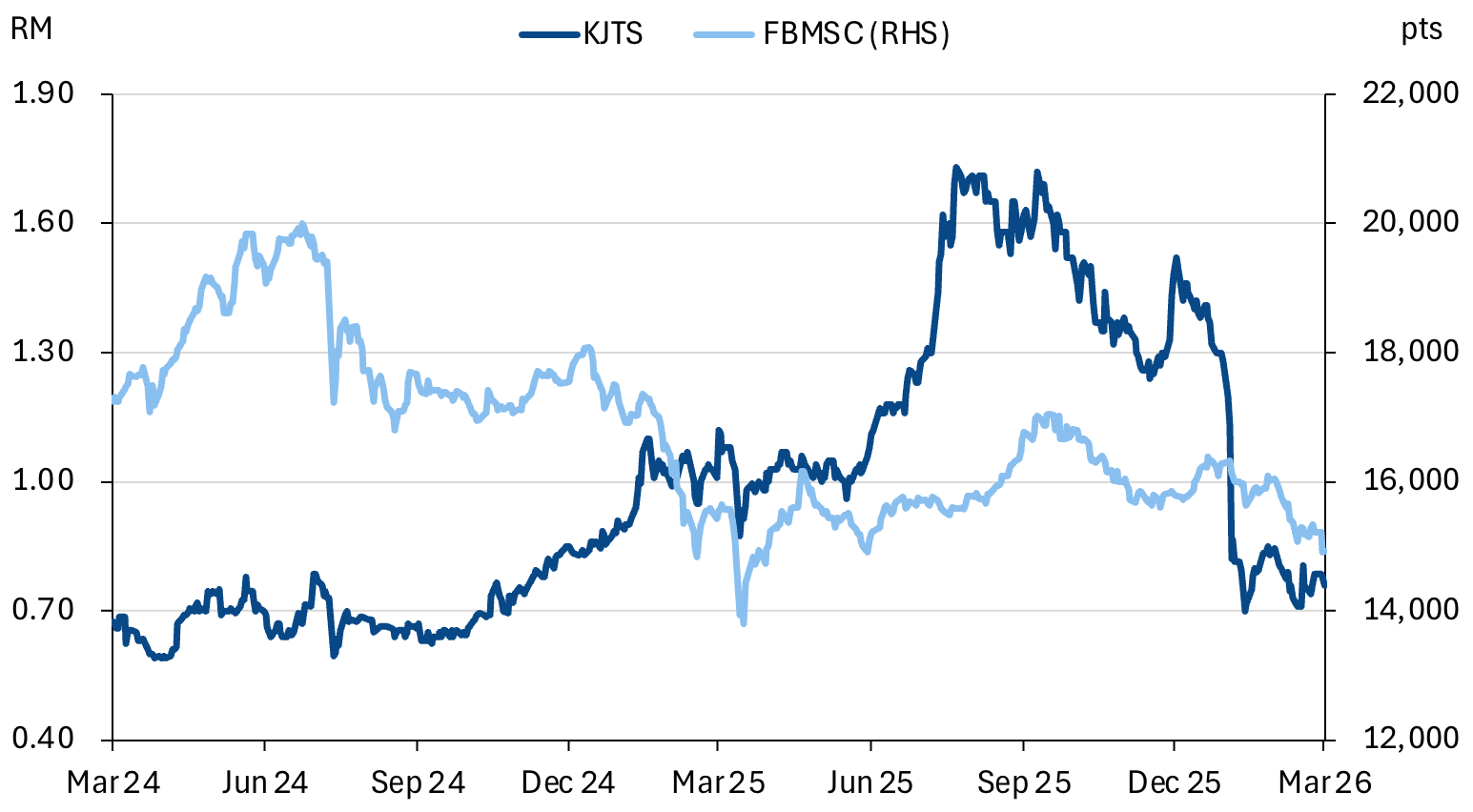

52-week range: RM0.66 / RM1.81

3M ADV: RM1.5m

T12M returns: -23%

Disclaimer: By using this information, you acknowledge that you are solely responsible for evaluating the merits and risks of any investment decision and agree not to hold NewParadigm Research liable for any damages arising from such decisions.

Key takeaways

- Management indicated a potential RM100-150m greenfield project for LCE could be secured within 12m. Principal is Stonepeak, improving certainty.

- iHandal acquisition offers access to patented heat recovery system and RM3m p.a. profit guarantee.

- Long-awaited GLIC investor for LCE should be concluded soon, opening door for more domestic prospects.

Share price performance

Investment fundamentals

| RMm | FY25A | FY26E | FY27E | FY28E |

|---|---|---|---|---|

| Revenue | 212 | 239 | 289 | 345 |

| Revenue Growth | 54% | 13% | 21% | 19% |

| EBITDA | 27.6 | 40.2 | 47.3 | 56 |

| EBITDA margin | 13% | 17% | 16% | 16% |

| PATAMI | 18.2 | 29.3 | 38 | 49.6 |

| PATAMI margin | 9% | 12% | 13% | 14% |

| ROA | 9% | 11% | 12% | 14% |

| ROE | 14% | 18% | 20% | 21% |

| PER | 28.8 | 17.8 | 13.8 | 10.5 |

| P/BV | 3.9 | 3.3 | 2.7 | 2.2 |

| Yield | 1.0% | 1.0% | 1.0% | 1.0% |

Source: Company data, Bloomberg, NewParadigm Research, March 2026

Moving beyond the MUSB disappointment

- The maiden asset for the Lestari Cooling Energy (LCE) joint venture with Stonepeak could be finalized in the coming months. Management shared that it was close to finalizing a greenfield cooling project with an estimated value for between RM100-150m for a capacity of 10k-13k refrigerant tonnes. This would be substantially larger than the now-abandoned MUSB project’s indicative value of ~RM90m.

- The underlying client for this asset is industrial in nature and would have a common principal - Stonepeak. While related party in nature, it should improve certainty of securing the project.

- Recall, KJTS will recognise an EPCC margin (~15%) on capex, which ranges from 30-60% of the value. Broadly, this is in-line with our project win projections, so we maintain our assumptions but with more confidence in delivery.

- Another catalyst for KJTS, is the acquisition of a 70.6% stake in iHandal - a heat recovery specialist with a key HeatFuse patented technology. The floor for the deal is at least RM3m in profit guarantee (~RM2m net). The ceiling will be access to iHandal’s customer base as well as cross-selling of products across cooling and heating.

- The deal does have a call option for iHandal’s current principal (CEO/founder Aaron Patel) to buyback his stake at cost in 3 years, but with KJTS retaining at least 51%. This will help keep the existing iHandal management aligned with growing the business.

- Lastly, management reiterated that the long-awaited GLIC partner should sign on to LCE soon as a partner. This newsflow would be a catalyst for the stock, as a GLIC shareholder in LCE paves the way for the JV to pursue state-owned or state-adjacent cooling assets. It has also been delayed so long, market expectations on this development is low.

iHandal driven upgrade to earnings

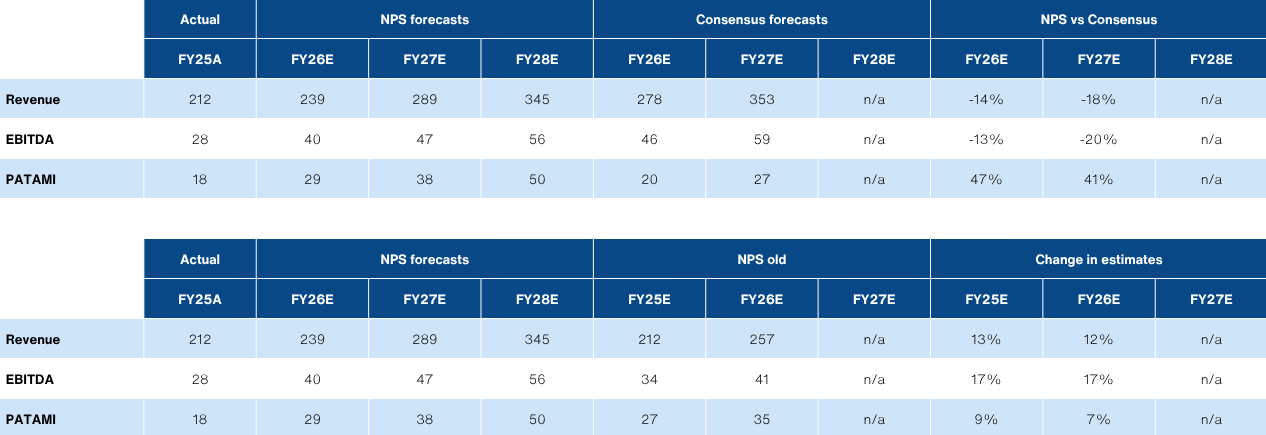

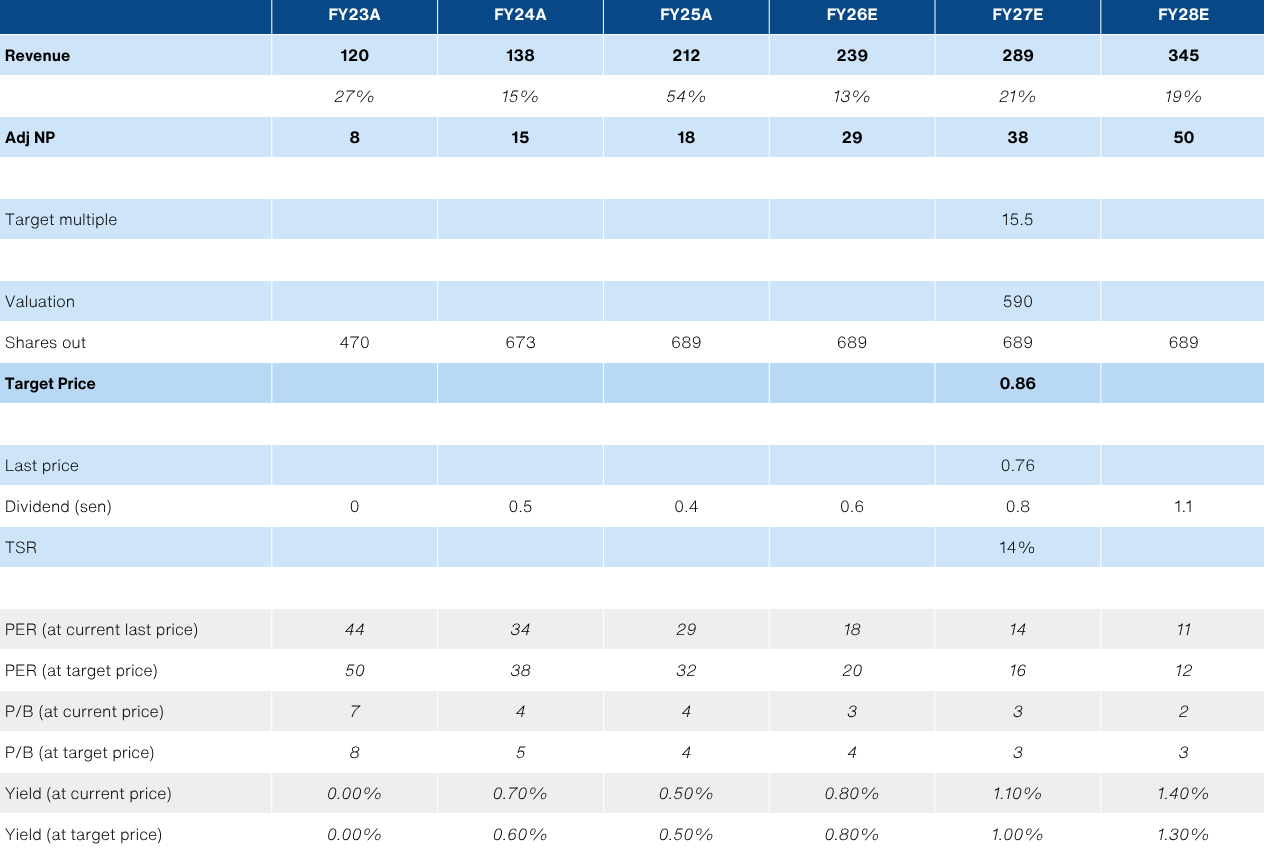

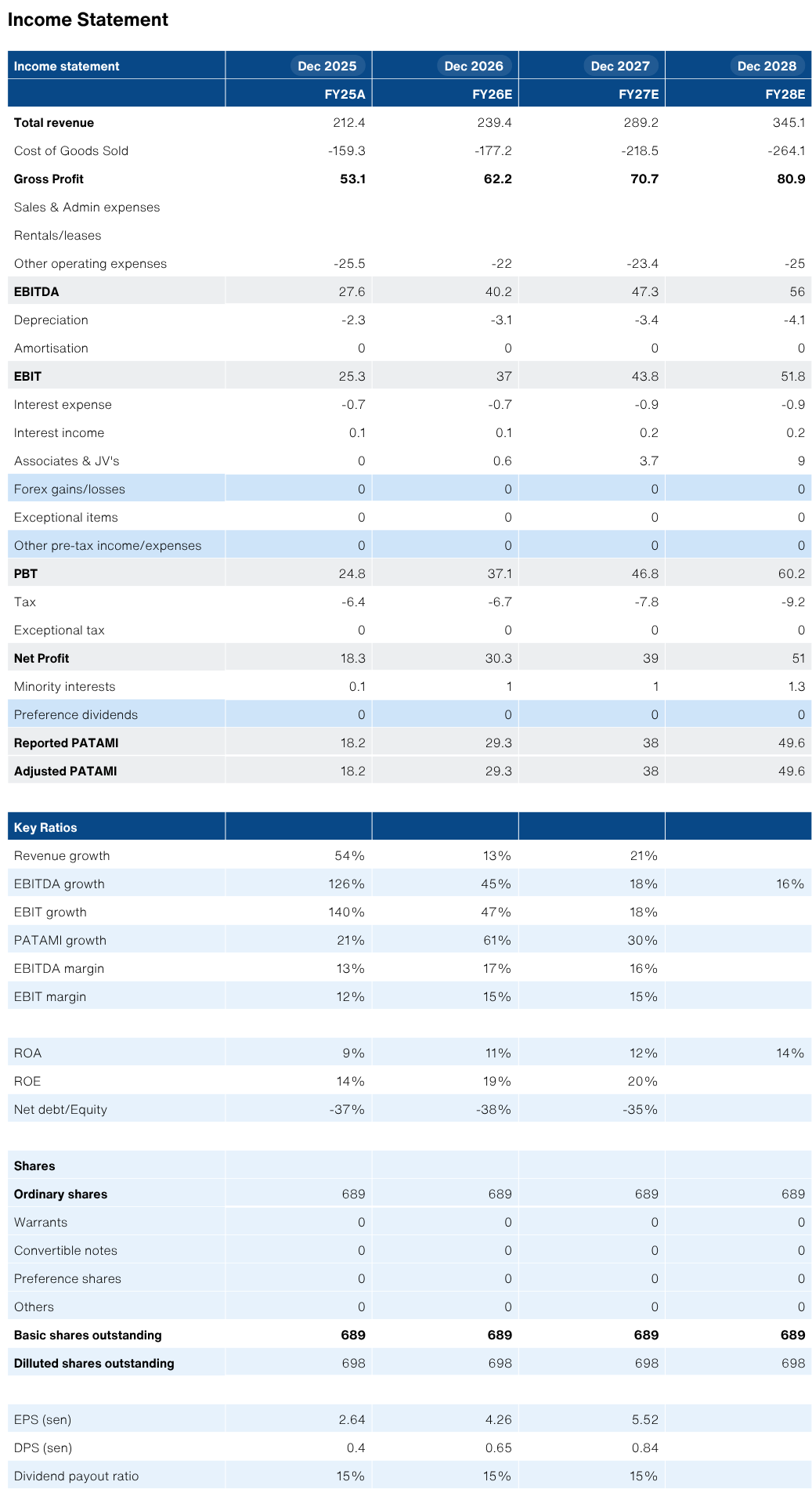

- We upgrade our FY26/27 Adj NP assumptions by +9%/+7% to reflect iHandal’s contributions. Maintain our target multiple of 15.5x FY27E, and raise our TP to RM0.86. Maintain Buy.

- The spectre of rising energy prices should spur more investment into energy efficiency projects, which plays to KJTS’ thematic. Higher electricity prices also offer modest tailwind to cooling concessions.

iHandal - Patented technology

- Established in 2009 by founder/CEO Aaron Patel, iHandal specialises in heat recovery systems for commercial and industrial applications.

- Through its solutions, iHandal captures waste heat, compresses it with a patented HeatFuse technology, and deploys the recycled heat towards a building’s heating/cooling requirements. The primary area of expertise is in commercial hot water systems as well as customised industrial heat pumps.

- An explanation of the company’s solutions can be found here: link.

- A key differentiator for iHandal’s technology is the ability to provide relatively high temperature water - as high as 140°C. Competing heat recovery solutions will skew towards lower temperature applications like domestic hot water.

- A write up on MIDA’s website link cites a payback period of 2-4 years for the HeatFuse technology, boasting up to 70% savings on thermal energy operating costs. The viability of such an investment by potential clients is further supported by MIDA’s Green Investment Tax Allowance that covers 100% of the capital expenditure for 3 years.

- iHandal boasts over 200 completed projects. Key customers include commercial buildings like hotels and customers including the likes of Hilton, Marriott and the Four Seasons. It is also deploying its solutions into industrial applications, thanks to the higher temperatures, into industries like healthcare and F&B.

- iHandal also has customers outside of Malaysia, particularly in Singapore. Other previous export markets includes Vietnam, Australia, Sweden and the US.

- According to management, KJTS has a pre-existing relationship with iHandal from previous projects. Looking ahead, KJTS intends to cross-sell its solutions with iHandal’s existing customer base to drive revenue synergies.

iHandal’s production floor (2024)

iHandal - a look at the financials

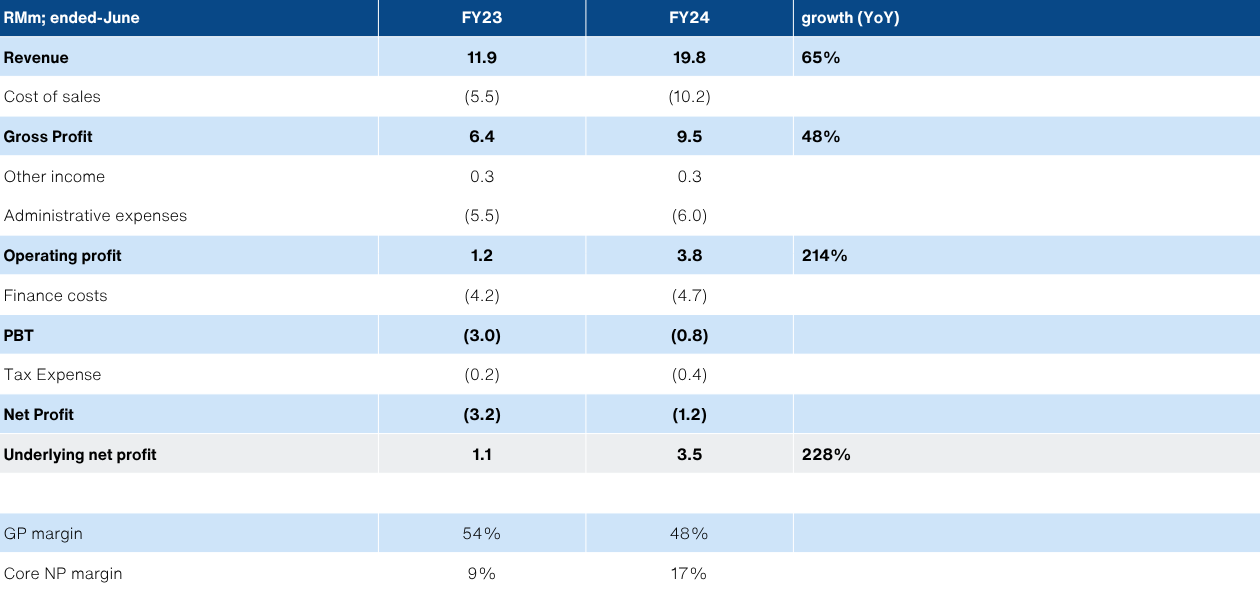

- Management is guiding that the acquisition of iHandal should be able to deliver at least RM3m per year as per the profit guarantee, or about RM1.7m adjusting for the 70% stake.

- We looked into iHandal’s financials (up to FY24 ended-June) and found the company was generating an underlying net profit of ~RM3.5m, excluding onerous finance costs from the redeemable preference shares (RPS) that will be settled before the acquisition.

- In turn, we estimate that iHandal should be able to contribute closer to ~RM2.4m at the current run rate (adjusted for 70% stake), even before any synergies from the acquisition.

- This seems relatively healthy, given the acquisition cost of RM10.5m implies a valuation of ~4.1x PER. We upgrade our FY26/27 Adj NP by +9%/7% or RM2.3m/2.5m to reflect the contribution from iHandal. This translates to an incremental +5.2sen/share upside to our target price, at our previous target multiple of 15.5x.

- However, it is worth noting that the earnings contribution is likely to decline after the first 3 years, once the profit guarantee expires and a call option from the founder/vendor/management of iHandal becomes active. The strike price for the call option is at the present purchase consideration, for up to 49% of iHandal. Broadly, we think this arrangement ensures that the existing management’s LT goals are aligned with KJTS - pushing for more growth. Critically, control of the patents will reside with KJTS.

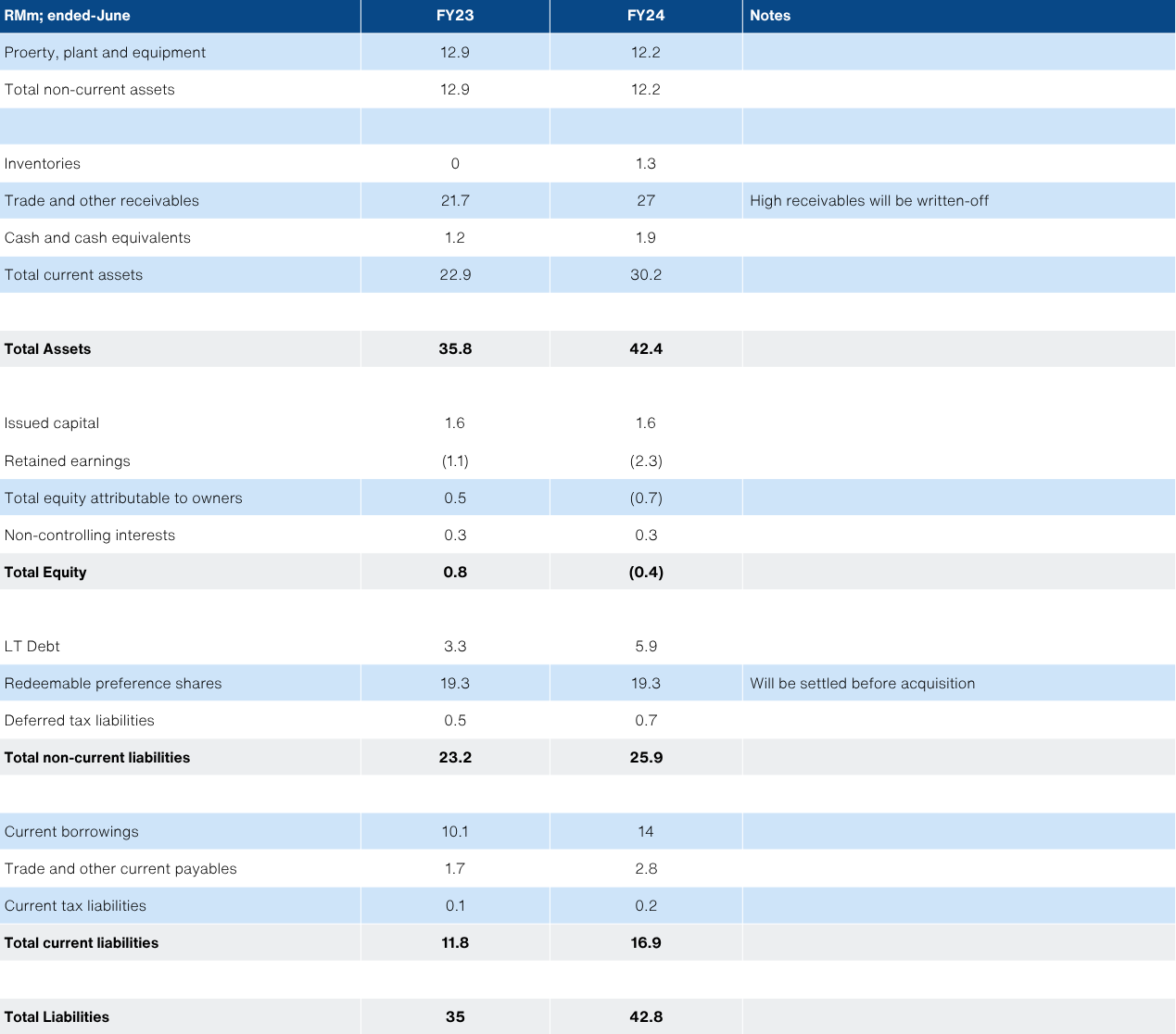

- Another notable feature of iHandal’s financials is the ~RM26m in receivables on the balance sheet as of FY24, which is quite high given the annual turnover is only RM19m. Management confirmed that the entire amount will be written-off prior to the acquisition. Any subsequent recoveries will be accretive on top of the profit guarantee as well.

iHandal’s Income Statement / Balance Sheet

Source: Company data, NewParadigm Research, March 2026

Valuation / Changes to estimates

Source: Company data, NewParadigm Research, March 2026

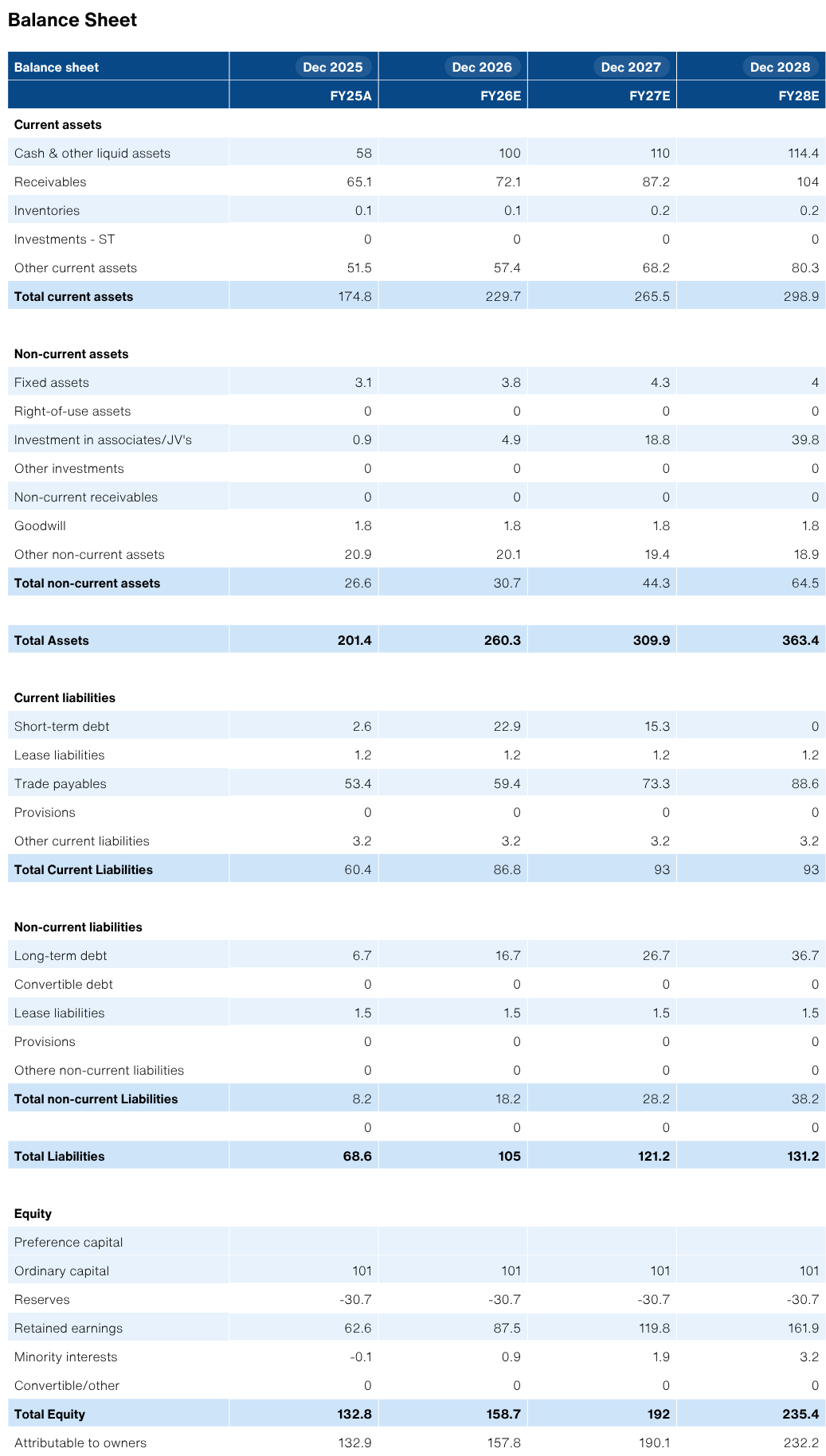

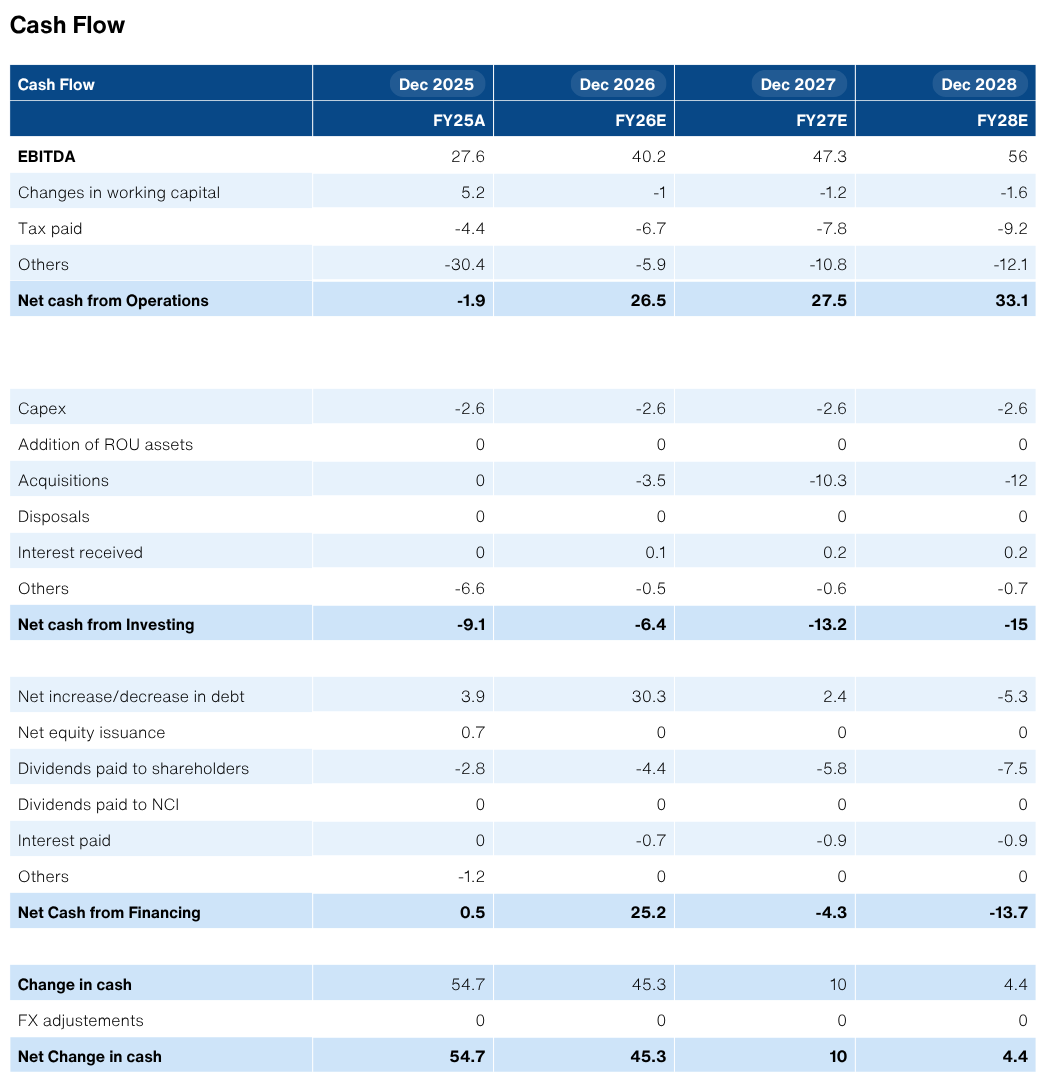

Selected Financials

Source: Company Data, NewParadigm Research, March 2026