1Q26 - Positive margin outlook

Management is guiding for 25-35% underlying growth for FY26.

FRONTKEN

FRCB | 0128.KL

BUY

Target price: RM5.20

Last price: RM4.65

Market cap (RMm): RM8,028m

Shares out: 1,726m

52-week range: RM3.51 / RM4.83

3M ADV: RM19m

T12M returns: 22%

Disclaimer: By using this information, you acknowledge that you are solely responsible for evaluating the merits and risks of any investment decision and agree not to hold NewParadigm Research liable for any damages arising from such decisions.

Key takeaways

- 1Q26 Adj NP of RM40.6m (+1% QoQ, +24% YoY) was 19%/20% of ours/consensus expectations, largely due to seasonal drag.

- Excluding forex movements, management maintained a 20% revenue and 25-30% NP growth target for FY26.

- Warrants have now expired with 242m warrants exercised, raising RM968m against ~15% dilution.

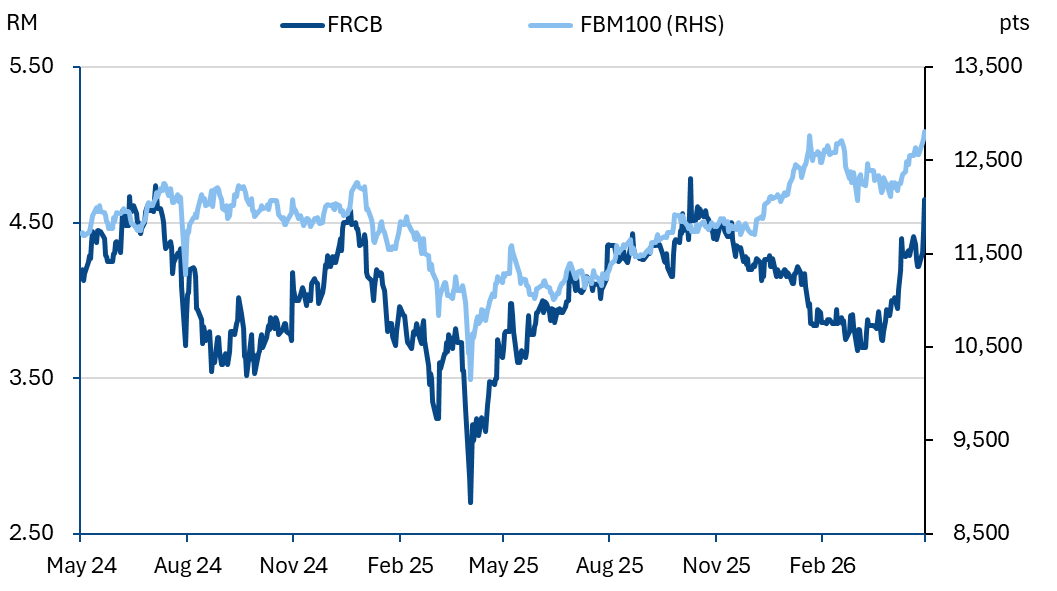

Share price performance

Investment fundamentals

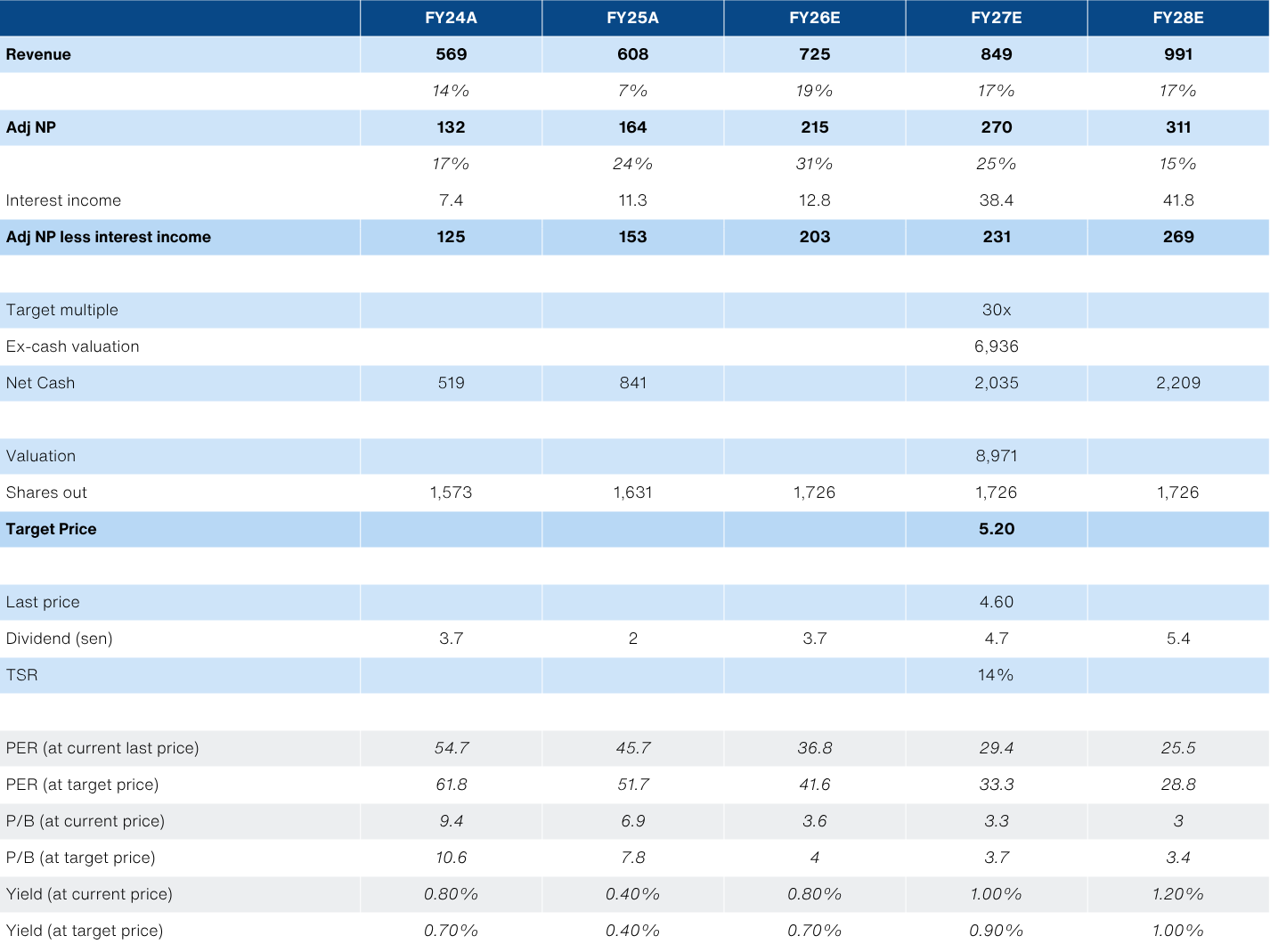

| RMm | FY25A | FY26E | FY27E | FY28E |

|---|---|---|---|---|

| Revenue | 607.8 | 724.8 | 849 | 990.5 |

| Revenue Growth | 7% | 19% | 17% | 17% |

| EBITDA | 234.7 | 324.1 | 378.6 | 441 |

| EBITDA margin | 39% | 45% | 45% | 45% |

| PATAMI | 164.1 | 215.5 | 269.6 | 311.1 |

| PATAMI margin | 27% | 30% | 32% | 31% |

| ROA | 13% | 9% | 10% | 11% |

| ROE | 15% | 10% | 11% | 12% |

| PER | 38.3 | 30.8 | 24.6 | 21.4 |

| P/BV | 5.8 | 3.0 | 2.7 | 2.5 |

| Yield | 1% | 1% | 1% | 1% |

Source: Bloomberg, NewParadigm Research, May 2026

O&G distortion

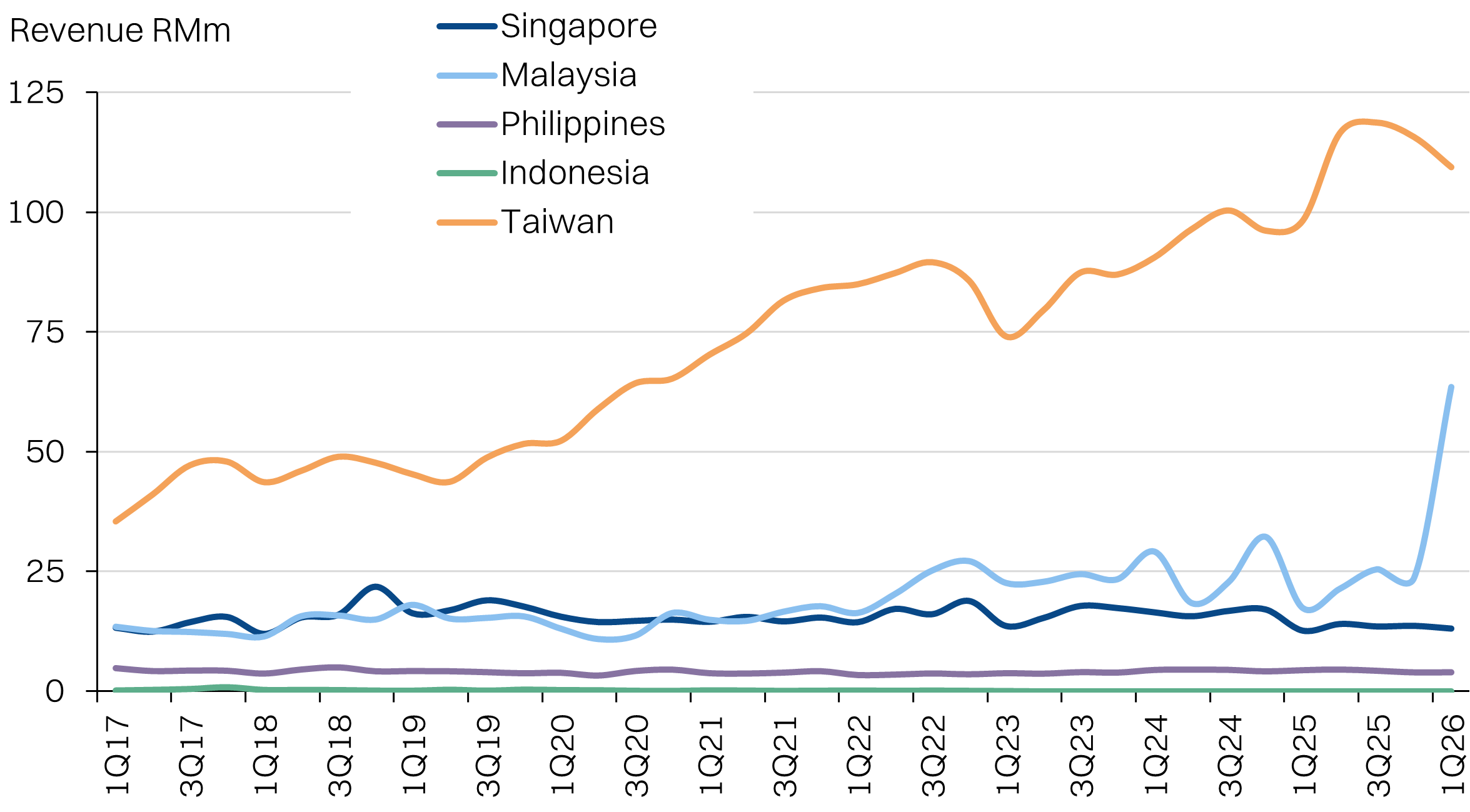

- Revenue surged +21% QoQ and +43% YoY to RM189.8m, but this was driven by a single lumpy project within the Malaysia segment. We estimate the project value is about RM42m, pointing to a more modest +12% YoY topline growth. The bottomline contribution from this project is relatively negligible, as it is low margin. More contribution is expected over the next two quarters of a similar quantum, but we will look past this distortion.

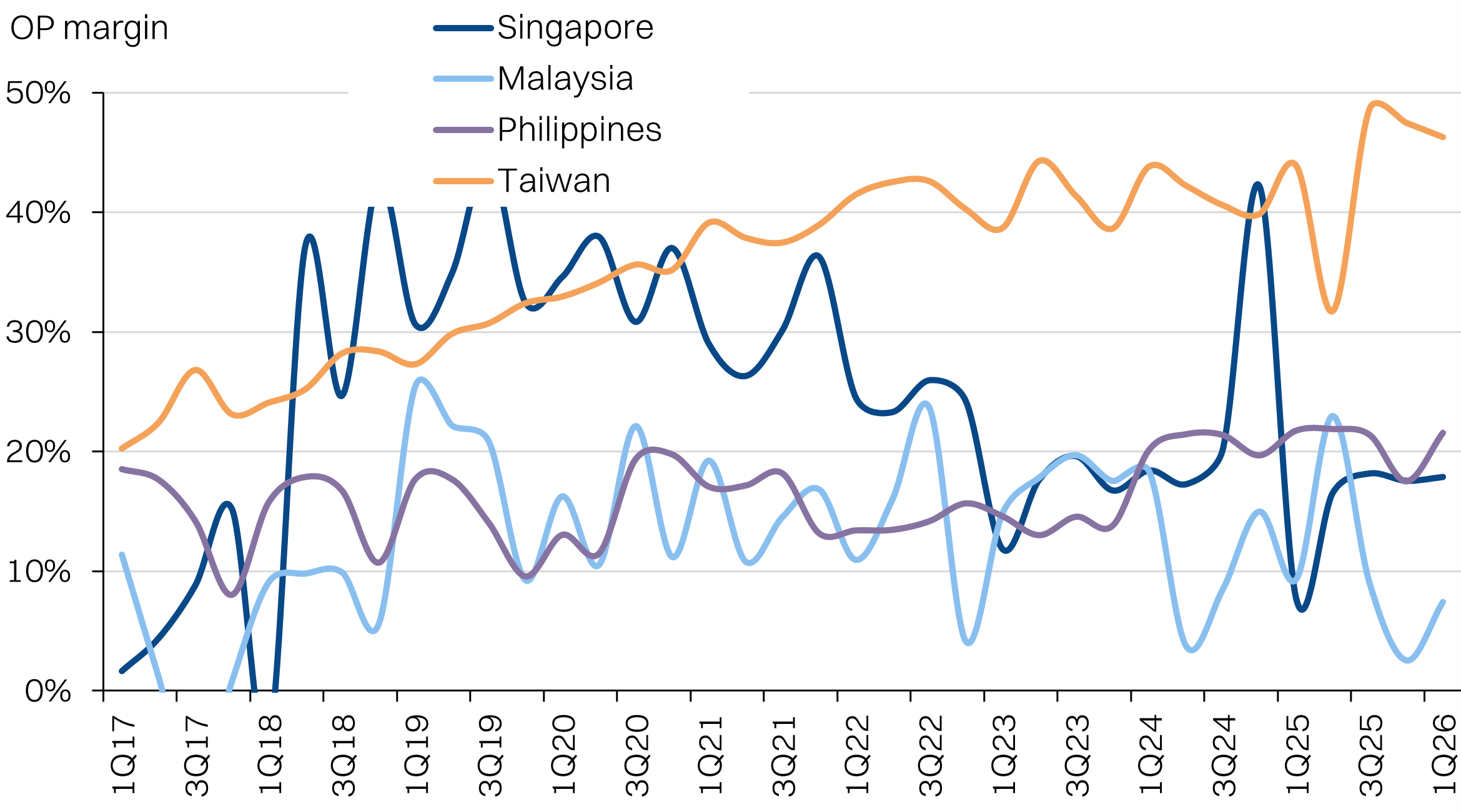

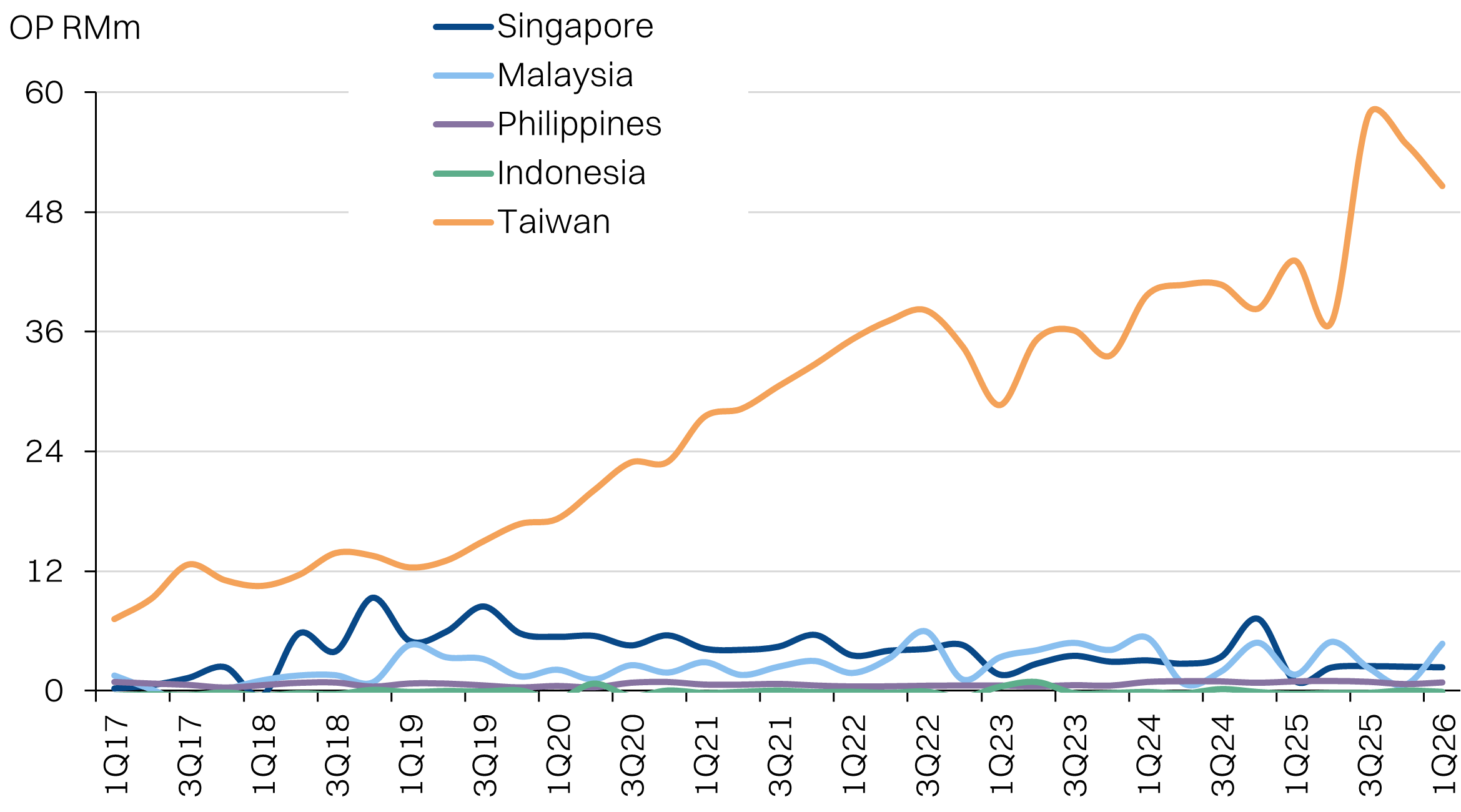

- Underlying performance of the Taiwanese segment was +20% YoY growth and +27% OP, in TWD terms. The main reason for the optically tepid YoY growth was due to the foreign exchange drag - about 8% YoY.

Looking ahead

- Management struck an optimistic tone on margins going forward, despite some of the cost pressures from the Gulf war, as customers have been willing to absorb the impact.

- Headline guidance remained in-line with our estimates. Management expects ~20% YoY topline growth with +25 to 35% growth for the bottomline for FY26. Indicative customer demand remains strong, with the plants running at full utilisation. Additional capacity from the new lines in Plant 2 will underpin this growth, with commencement due in 2Q/3Q26.

- In fact, FRCB is also bringing foward the expansion of Plant 2 (originally due for 2027), reflecting the strong end-demand.

- The warrants conversion overhang has been cleared, following expiry on 30 April. Dilution of 15% came with an additional RM968m for the balance sheet, which brings gross cash to ~RM1.5bn on hand.

- We infer that there is no M&A close to completion from management tone, as the expectations on valuations remains very high. The requirement for 3 years of audited accounts is also a major hurdle.

Rolling forward valuations

We roll forward our valuations to FY27E on a lower target multiple of 30x, and factor in the warrants dilution as well as the increased gross cash on the balance sheet. Underlying earnings are unchanged, but lifted slightly by the higher interest income from the cash. In turn, we upgrade our target price to RM5.20. Maintain Buy.

Earnings

Earnings vs expectations

Updated valuations

Revenue distorted by a single Malaysian O&G project

Operating profits cooled due to slower seasonal 1Q

Margins remain stable