Pricing in the margin pressure

LSH is only trading at implied single digit PER.

Stock information

LSH CAPITAL

LSH | 0351.KL

BUY

Target price: RM2.80

Last price: RM1.79

Market cap (RMm): RM1,509m

Shares out: 838m

52-week range: RM0.770 / RM2.56

3M ADV: RM1.24m

T12M returns: 126%

Disclaimer: By using this information, you acknowledge that you are solely responsible for evaluating the merits and risks of any investment decision and agree not to hold NewParadigm Research liable for any damages arising from such decisions.

Key takeaways

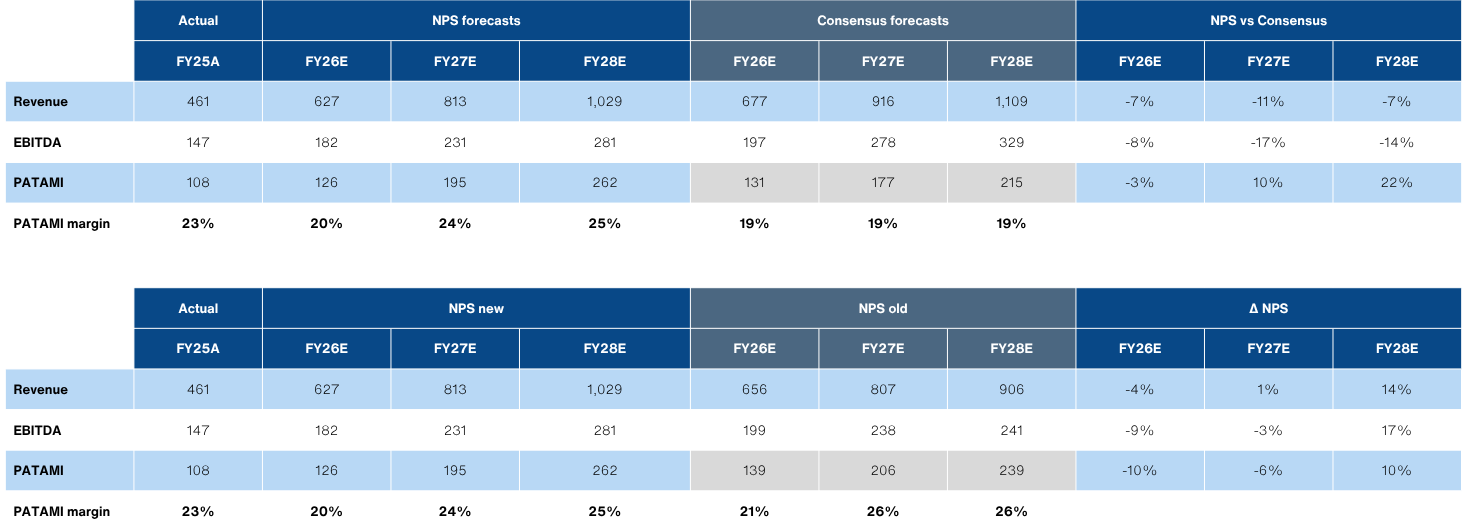

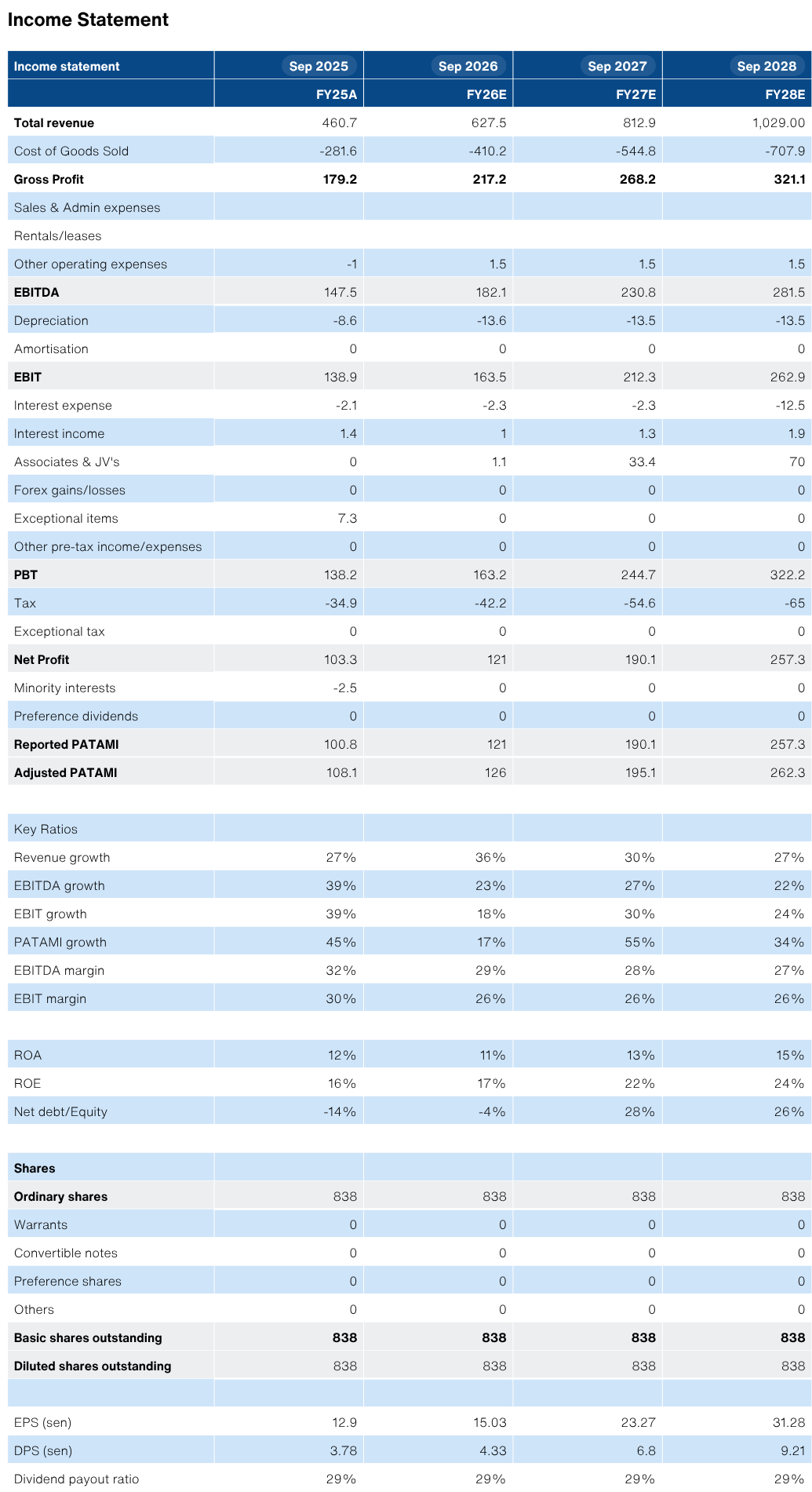

- We trim FY26/27E Adj NP by -10%/-5% on lower margins from cost pressure as well as slower project recognition.

- However, we upgrade FY28 Adj NP by +10%, driven by the inclusion of the 17.4acre Batu 3 land acquisition with an estimated GDV of RM2bn.

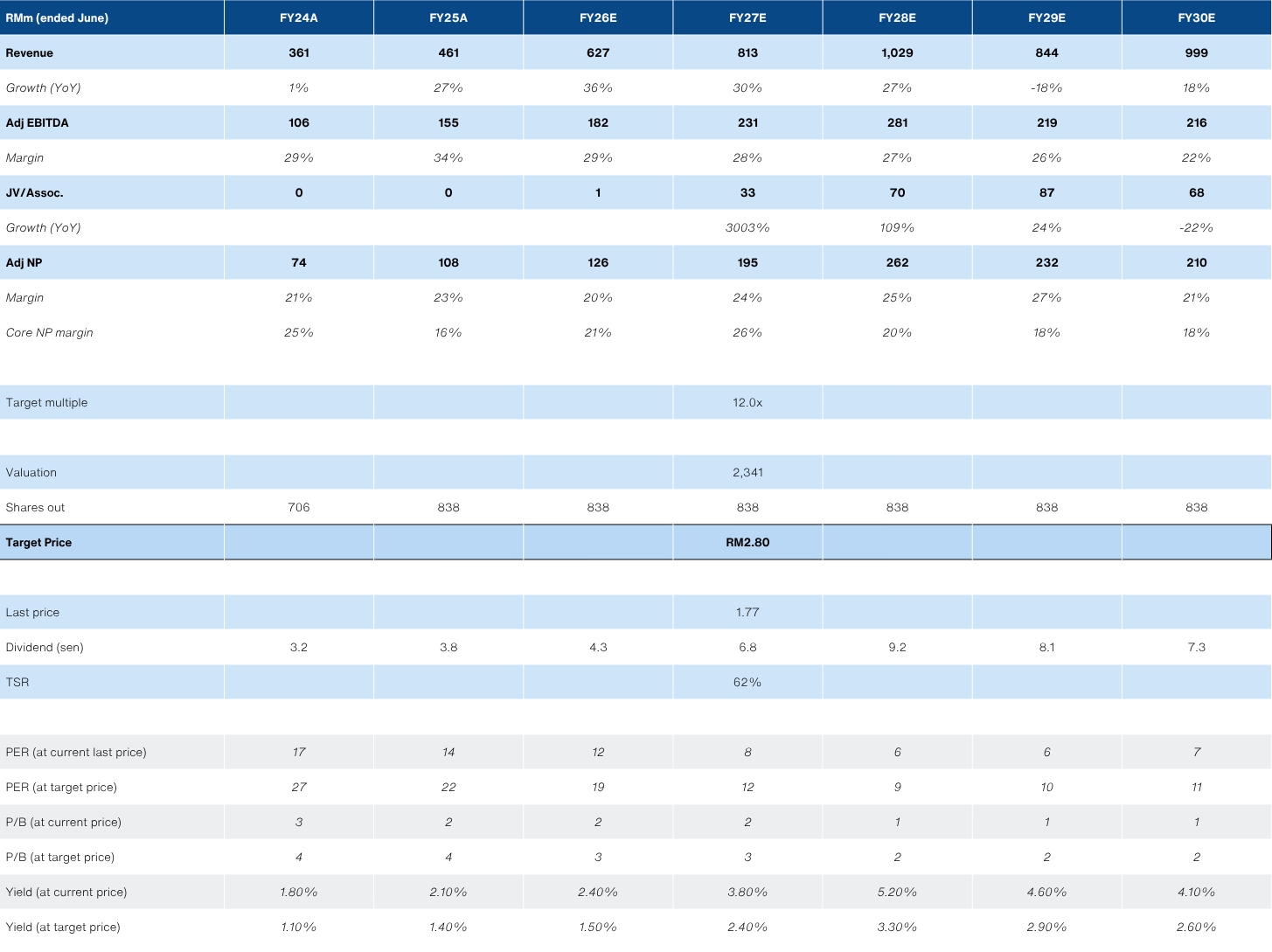

- On the lower ST earnings, we lower our TP to RM2.80 (from RM3.00) based on 12x FY27E PER of RM196m. Maintain BUY.

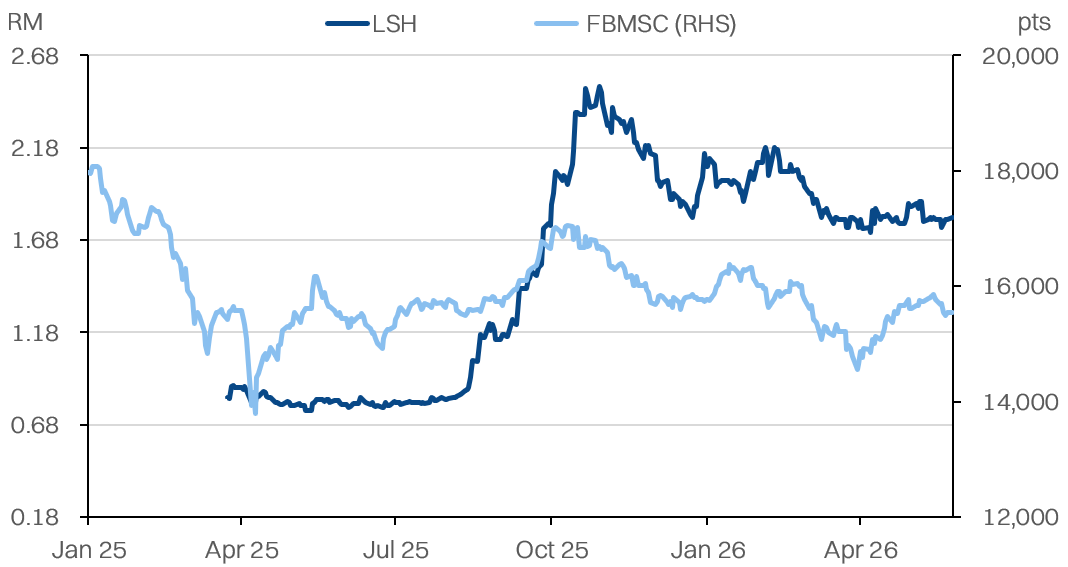

Share price performance

Investment fundamentals

| RMm (ended Sept) | FY25A | FY26E | FY27E | FY28E |

|---|---|---|---|---|

| Revenue | 461 | 627 | 813 | 1,029 |

| Revenue Growth | 27% | 36% | 30% | 27% |

| EBITDA | 147 | 182 | 231 | 281 |

| EBITDA margin | 32% | 29% | 28% | 27% |

| Adj NP | 108 | 126 | 195 | 262 |

| Adj NP margin | 23% | 20% | 24% | 25% |

| ROA | 12% | 11% | 14% | 15% |

| ROE | 16% | 17% | 22% | 24% |

| PER | 13.7 | 11.8 | 7.6 | 5.7 |

| P/BV | 2.3 | 2.0 | 1.7 | 1.4 |

| Yield | 2% | 2% | 4% | 5% |

Source: Company data, NewParadigm Research, May 2026

Improving earnings visibility is being overlooked

- Management clarified that 2QFY26 (ended-March) deceleration was partially due to timing of SPA signings for the Lake Side Homes project, which drove the segment to a marginal EBITDA loss. However, this should normalize in the coming quarters as it is purely a recognition issue.

- However, management was also transparent with the margin headwinds that the broader construction and property industries were facing, due to higher fuel and raw material costs. LSH is already employing various mitigation strategies, included management of project timelines and deferring procurement where possible. All in, management is anticipating a 5-10% higher costs for the construction segment overall.

- In turn, we have trimmed both our revenue and margin assumptions for FY26/27. The lower revenue assumes some slowdown in selected projects, in order to defer procurement amid surging prices. We cut FY26E revenue by -4%.

- We also cut our margin assumptions by -1.4/-1.1ppts for FY26/27E, to reflect the higher raw material and operating costs. In turn, our Adj NP forecast is lowered by -10%/-6% respectively.

Batu 3 land and highway upside

- We added the 17.4 acre Batu 3 land acquisition to our assumptions, with a GDV of RM2bn. We anticipate the project will only begin constrution in FY28, so it does not yet impact our valuations. However, it is worth noting that the project’s contributions in FY28E lowers the forward multiple to 6x implied, based on the last close.

- Management also struck a positive tone on the progress of the Bandar Malaysia-Seri Kembangan Expressway (BSE), which is now pending approval-in-principle from the government. Management’s standing estimate for the project is RM1.75bn, which we have already included in our assumptions.

Longer term outlook intact

While we have trimmed our valuations to reflect the reality of the US-Iran war’s inflationary drag on earnings, we note that the company’s earnings visibility has continued to improve with the new projects secured. Maintain BUY with lower TP of RM2.80.

About the Company

Lim Seong Hai Capital Bhd (LSH Capital) is a construction company with a secondary focus on property development and facilities management. The group differentiates itself from peers by its sector leading margins, low gearing and low reliance on subcontractors (~10%). Within construction, LSH Capital’s primary focus is infrastructure jobs. The group also has a 20-year concession to maintain and operate KL Tower and is pursuing highway concession opportunities as well.

About the Stock

LSH Capital is named after the late Lim Seong Hai and is now co-owned and run by his four children. It is also seen as a breakaway from the Tan Sri Lim Kang Ho’s group of companies (including Ekovest), which have similar operating segments. LSH Capital was initially listed on the LEAP market in 2021 but has since been promoted to the ACE market in March 2025.

Investment Thesis

LSH Capital has a relatively large funnel of construction orderbook and property development launches, compared with its current low-base. Additionally, the group’s peer-leading margins allows for meaningful translation of orderbook wins to earnings. We forecast earnings growth to +45% CAGR (FY27E). Looking ahead, this implies LSH Capital is trading at single-digit PER multiples on FY27E, which is well below sector average.

Key Risks

- Family business - The four Lim siblings collectively control 61% of the company and have full management control. Only 50% of the board is independent.

- Related party transactions - The group has a history of RPT transactions, and injection of related businesses. As LSH Capital transitions to non-RPT work, it remains to be seen if margins will continue to hold up.

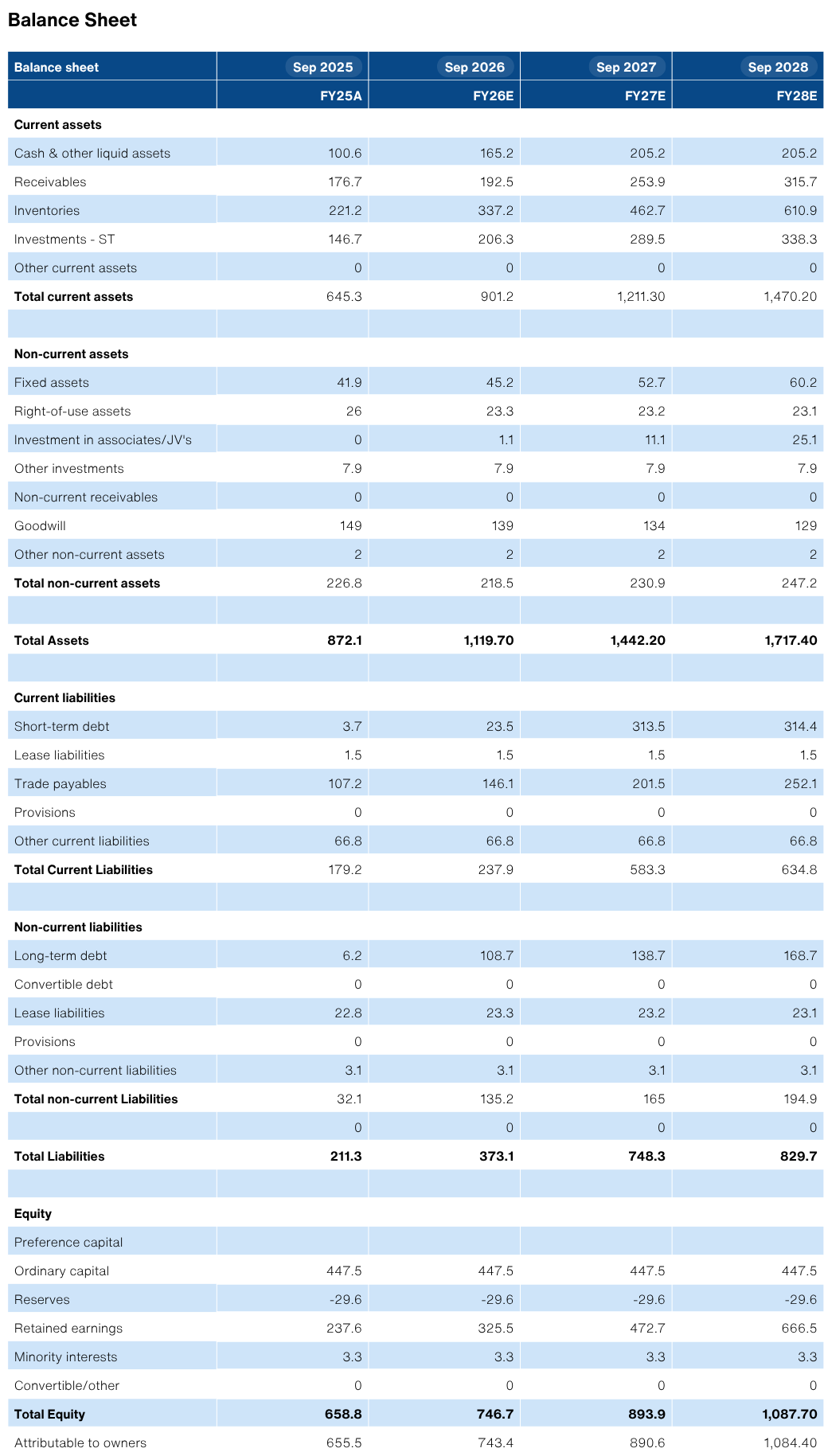

- Small balance sheet - Net tangible assets total only RM509m (excluding RM149 goodwill on consolidation). We anticipate risk of additional fund-raising if capital intensive projects are secured.

- Inflation - The US-Iran war is introduced a spike in fuel and raw material costs. Most construction projects are lump sum in nature and ability for contractors to pass on costs are limited. Additionally, property projects are on a sell first build later basis, so developers have to absorb higher costs.

- Politics - Our thesis on LSH is tied to the group’s ability to secure highway concessions. A potential snap election could delay approvals on large infrastructure projects like this.

Changes to estimates

Valuation table

Valuation bands

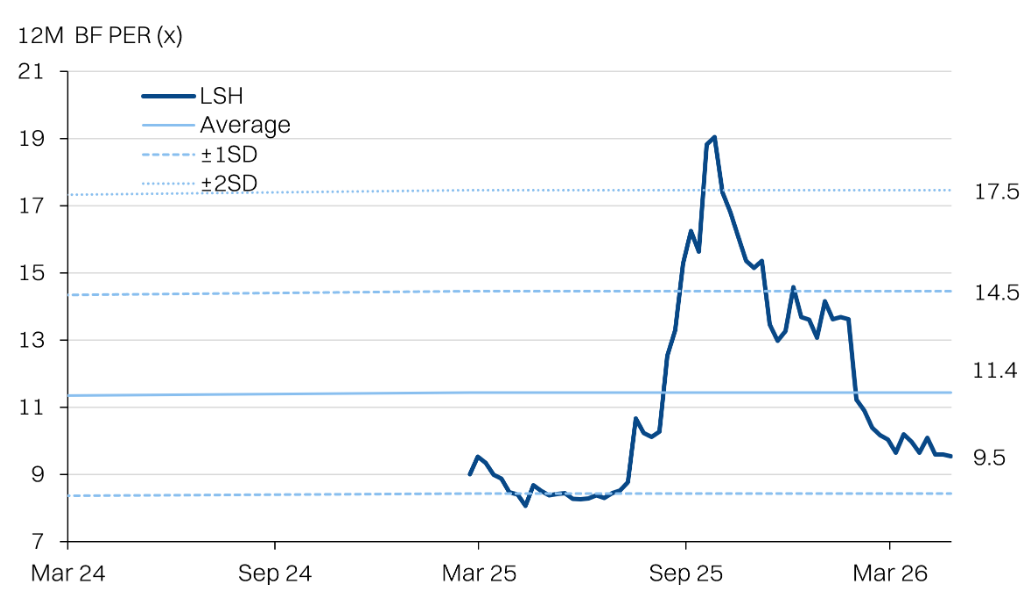

- Given LSH’s relatively recent listing, the stocks own historic valuation bands are not sufficient to use as a benchmark.

- Our 12x PER target is the -2SD range for the KL Construction Index against the hsitoric 3yr average. The sector is currently trading at 15.1x.

- We think this is a sufficiently conservative multiple for LSH, and accounts for its smaller market cap, ACE market listing, and shorter track record in the public market.

LSH PER bands

KL Construction Index PER bands

Batu 3 project overview

- On 15 May, LSH received a letter of offer from RAC for the proposed acquisition of two freehold parcels totalling 17.4 acres in Mukim Pekan Country Heights, Shah Alam, at a land cost of RM197.9m.

- The site is zoned commercial with a plot ratio of 4.0x, supporting a high-density development. The proposed mixed development comprises 3,240 service apartment units and a commercial component, spanning three phases of 1,089, 1,254 and 897 units respectively.

- We estimate the project will have an average selling price of RM667psf, a ~10% discount to Luminar (BRDB, RM739 psf) and ~6% below Alira (Avaland Berhad, RM709 psf), two nearby developments in the area.

- At 3,240 units, it is also meaningfully larger than both Luminar (751 units) and Alira (832 units), giving LSH a significant presence in the area once the project is underway. We expect the competitive pricing to support a healthy take-up rate.

- The site is well connected. KTM Batu 3 is nearby, linking residents directly to KL Sentral and Klang, with the Federal Highway and NKVE both accessible. Management has also flagged plans for an EV bus service to the KTM station, addressing last-mile connectivity for residents.

- Seksyen 13 one of Shah Alam's busiest commercial hubs is just 3 minutes away, with AEON Mall, Shah Alam Stadium and MSU on the doorstep. The LRT3 Shah Alam Line is also expected to commence operations in June 2026, with a dedicated station in Seksyen 13, further strengthening the connectivity case for the area.

Batu 3 project - site location

Batu 3, Shah Alam — Financial assumptions

- We have added the 17.4-acre Batu 3 land acquisition to our assumptions, with a GDV of RM2.0bn. We anticipate the project will only begin construction in FY28, so it does not yet impact our valuations.

- We expect revenue to be recognised progressively over five years from FY28 to FY32, in line with construction progress across three phases.

Batu 3 project - artist render

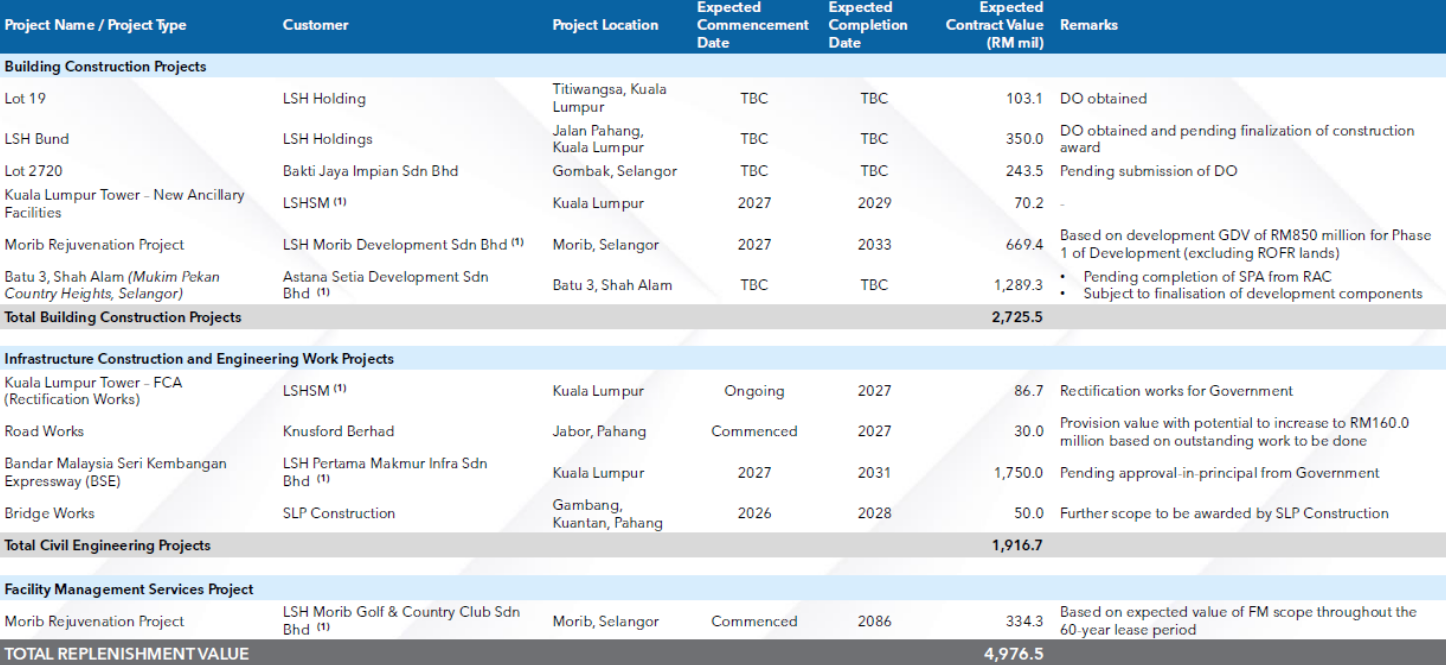

Orderbook updates

- LSH has a reported external orderbook of RM490m. However, the effective orderbook in hand is reasonably at least RM1bn, with the inclusion of the LSH Bund and Lot 2720 (Gombak) projects under the BEST collaboration framework (see: link)

- We’ve included these projects in our assumptions, but the market appears to be discounting it. We anticipate full approval for these projects and formal inclusion in the orderbook could be a catalyst for the stock going forward. Both are pending development orders.

- Management has also improved transparency of its orderbook funnel with the inclusion of the following slide in its presentation, which points to an incremental funnel of RM5bn.

- Of the following projects, we think the BSE highway award would be another major catalyst for the stock. There is scant newsflow on this project and it is perceived as politically sensitive - requiring government approvals to proceed. The biggest risk to this project’s timelines would be a snap election that puts all approvals on freeze.

Orderbook replenishment funnel

Selected financials

Source: Company Data, Bloomberg, NewParadigm Research, May 2026