1Q26 - Recognition timing drag

Management pinned the 1Q26 losses on timing of revenue recognition.

Stock information

Pan Merchant Berhad

PMIBHD | 0361.KL

BUY

Target price: RM0.27

Last price: RM0.22

Market cap (RMm): RM206m

Shares out: 916m

52-week range: RM0.185 / RM0.27

3M ADV: RM0.06m

T12M returns: -17%

Disclaimer: By using this information, you acknowledge that you are solely responsible for evaluating the merits and risks of any investment decision and agree not to hold NewParadigm Research liable for any damages arising from such decisions.

Key takeaways

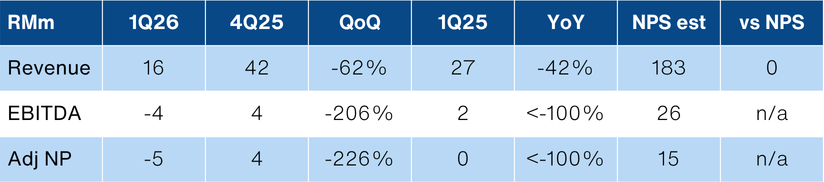

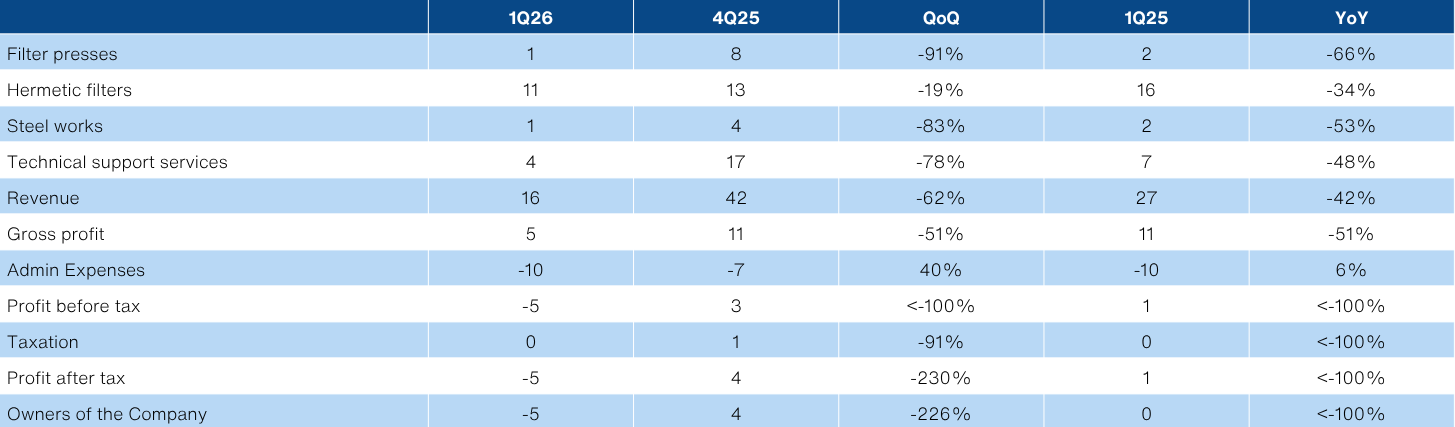

- PMI posted a 1Q26 net loss of -RM5m, which was a substantial disappointment against our expectations. For context, PMI Bhd posted an adj NP of RM6.3m for FY25.

- Management pinned to losses on recognition timing of its projects, coupled with seasonal slowdown in 1Q26. The soft Indonesian demand did not help either.

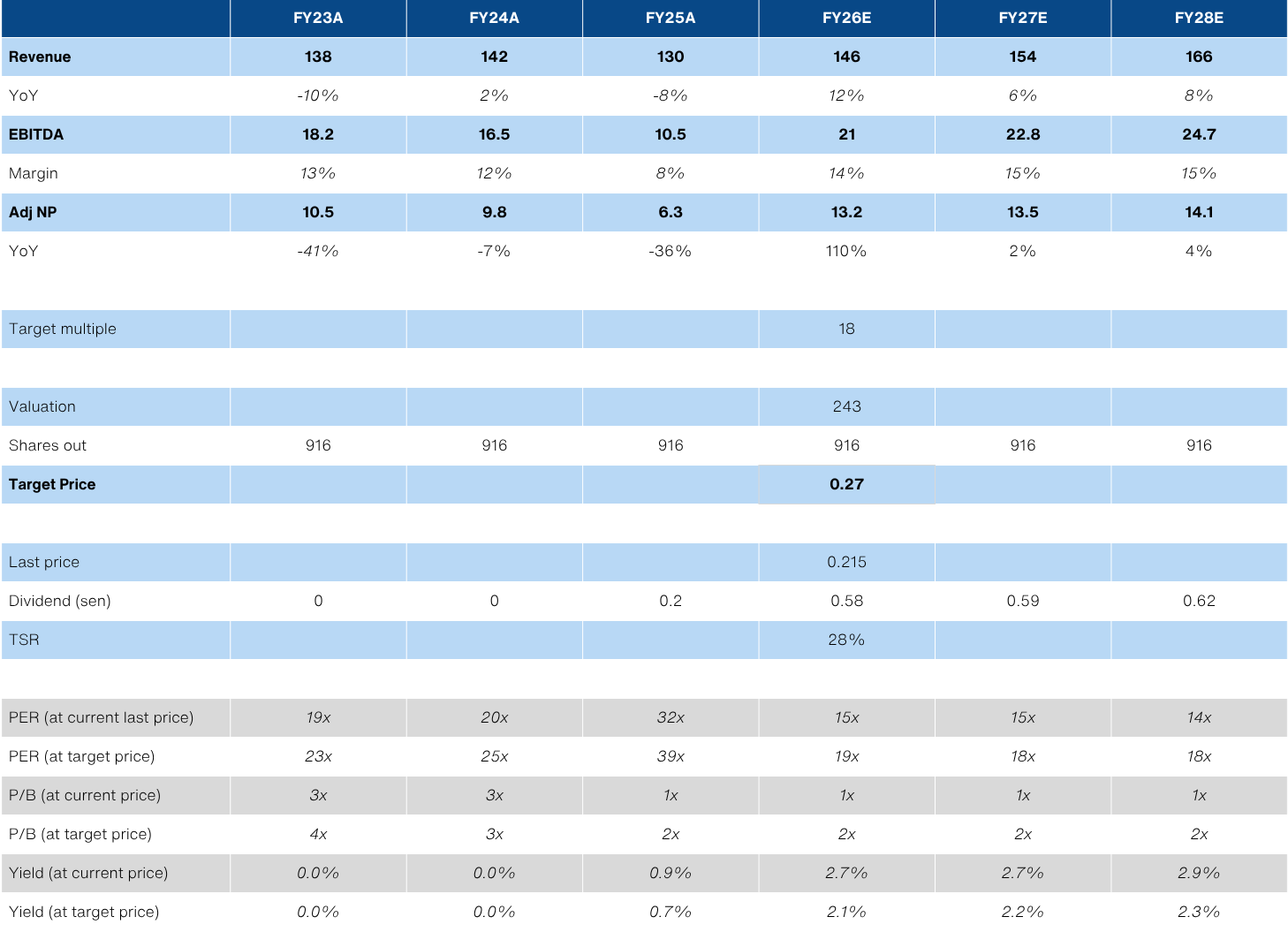

- We cut FY26 earnings by -13% and lower our TP to RM0.27 (from RM0.30) and maintain our BUY recommendation.

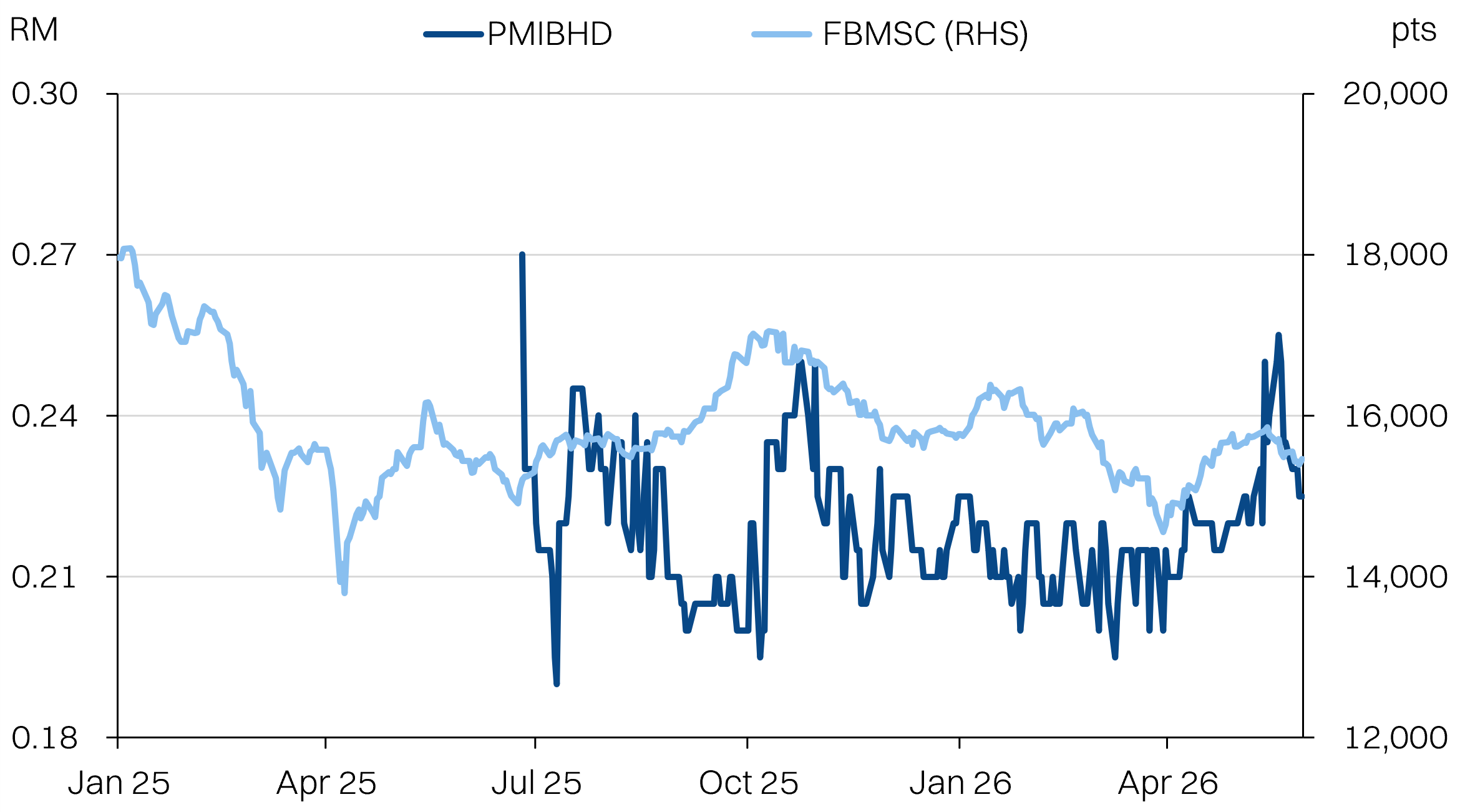

Share price performance

Investment fundamentals

| RMm (end-Dec) | FY25A | FY26E | FY27E | FY28E |

|---|---|---|---|---|

| Revenue | 130 | 146 | 154 | 166 |

| Revenue YoY | -8% | 12% | 6% | 8% |

| Adj PATAMI | 6.3 | 13.2 | 13.5 | 14.1 |

| Adj PATAMI margin | 5% | 9% | 9% | 9% |

| DPS (sen) | 0.2 | 0.6 | 0.6 | 0.6 |

| ROA | 3% | 7% | 7% | 7% |

| ROE | 5% | 9% | 9% | 9% |

| PER | 32 | 15.2 | 14.9 | 14.3 |

| P/BV | 1.5 | 1.4 | 1.3 | 1.2 |

| Yield | 1% | 3% | 3% | 3% |

| Net debt/equity | 43% | 39% | 31% | 27% |

Source: Company data, NPS Research, June 2026

Disappointing losses

- 1Q26 revenue was only 9% of our full year forecasts and drove the big miss vs our expectations. Management indicated the steep quarterly swings were not unusual, given the lumpy and s-curve nature of its projects. However, even for FY25, first quarter revenue was at least 21% of full year numbers.

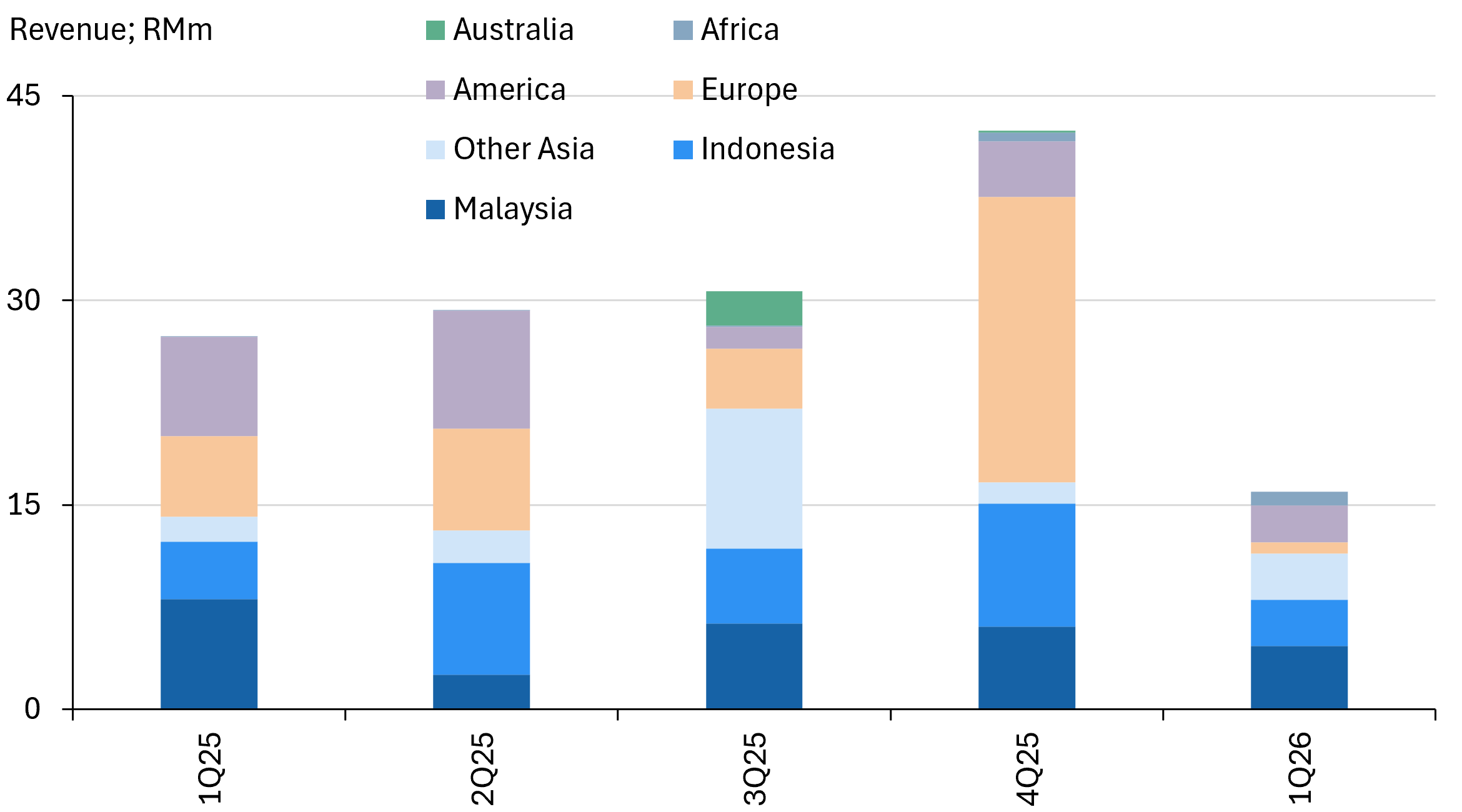

- Both the soft demand from Indonesia as well as the stronger ringgit were drags on the topline. PMI is 70-85% export driven.

- The one positive is that GP margins remained stable at 34%, as costs also fell in tandem, indicating lower manufacturing activity.

- Management is indicating that the orderbook remains at RM50m and is aiming for full year revenues to at least exceed last year’s levels.

Earnings snapshot

Next few quarters are critical

- We flag that our thesis on PMI is undermined by the latest set of results. The next few quarters will be make or break. Critically, PMI needs to book the much-awaited water project for its press filters, that should add RM30-40m to its orderbook.

- The latest bout of politicy interference in Indonesia is also likely to further delay the palm oil refinery capex cycle that PMI historically relied on for 40-60% of revenues. For the past few quarters it has only been 21%.

- We cut our FY26E earnings by -13%, pushing out some revenues to FY27E. In turn, we lower our target price from RM0.30 to RM0.27 on lower earnings, but an unchanged target multiple of 18x.

- Maintain BUY. Medium term catalysts for the stock includes ramp up in biodiesel adoption. Current capacity is ample for the recently announced movfe to B15, but subsequent step-ups might spark capex cycle.

About the Company

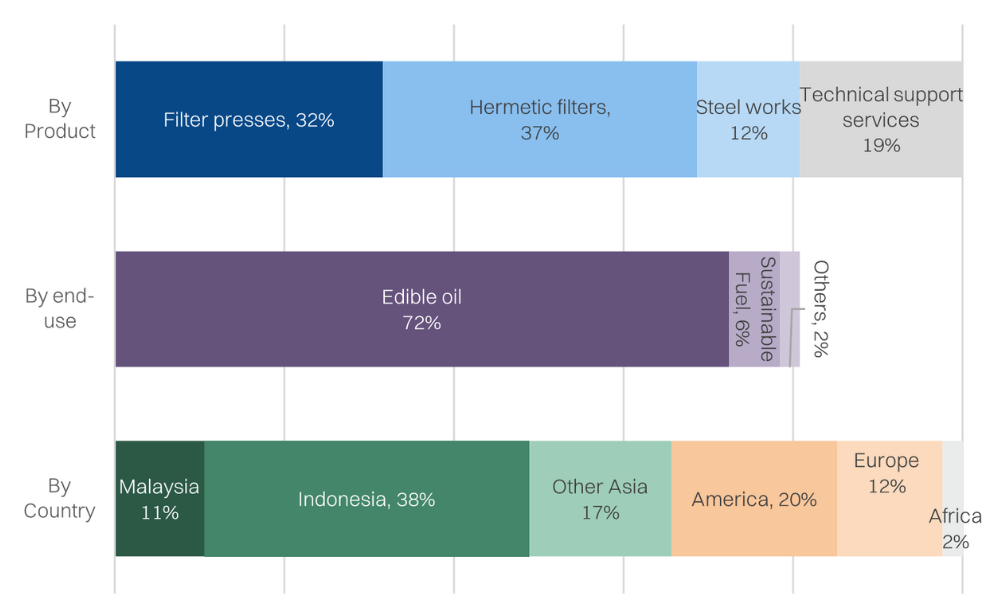

PMI specializes in manufacturing filter presses for liquid-solid separation. The primary application for the presses is in edible oils, and mainly for crude palm oil processing. The secondary application is within waste management, including water treatment as well as mining. This gives PMI potential as an ESG play. PMI is primarily an exporter, with over 85% sales coming from abroad, including countries like Indonesia, Europe, and US.

About the Stock

PMI was listed on the ACE market in June 2025, with the retail portion undersubscribed at only 37% taken up. It remains controlled by the founders' family - which also control the board and management. PMI is a Syariah-compliant stock.

Investment Thesis

PMI is well positioned to capitalize on the development of domestic water treatment projects in Selangor and other states - supplying press filters for waste management. Each phase (there are two) will require ~RM50 worth of filter press (based on projects of similar scale), or ~20% upside to baseline revenue run-rate. Placement of underwritten shares from IPO will also provide a liquidity event.

Key Risks:

- PMI has some customer concentration risk, with over almost 70% of revenues coming from its top 4 customers. PMI is mitigating this risk via diversification into other customers and segments.

- PMI could face competition from Chinese firms in the future. It is reliant on long-standing relationships with customers in the edible oils segment, and proven track-record to fend-off competition.

- Founders/shareholders control most key management positions via family members. This could pose governance, succession planning, and talent development risks.

Revenue composition (FY24)

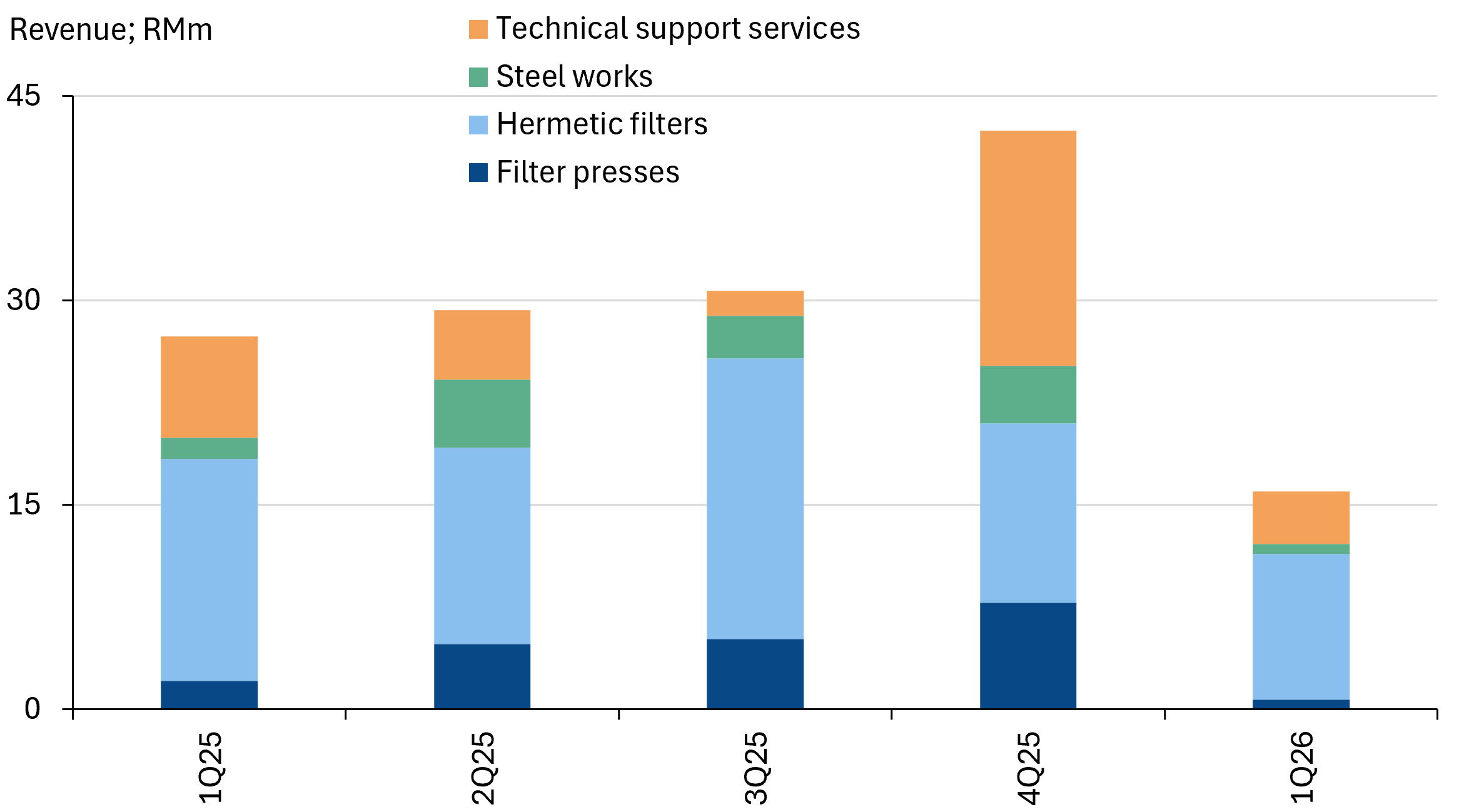

Revenue by segment - sharp drop

Revenue by country - export deceleration

Revenue by country - export deceleration

Revised estimates

Updated valuation methodology - Maintain Buy

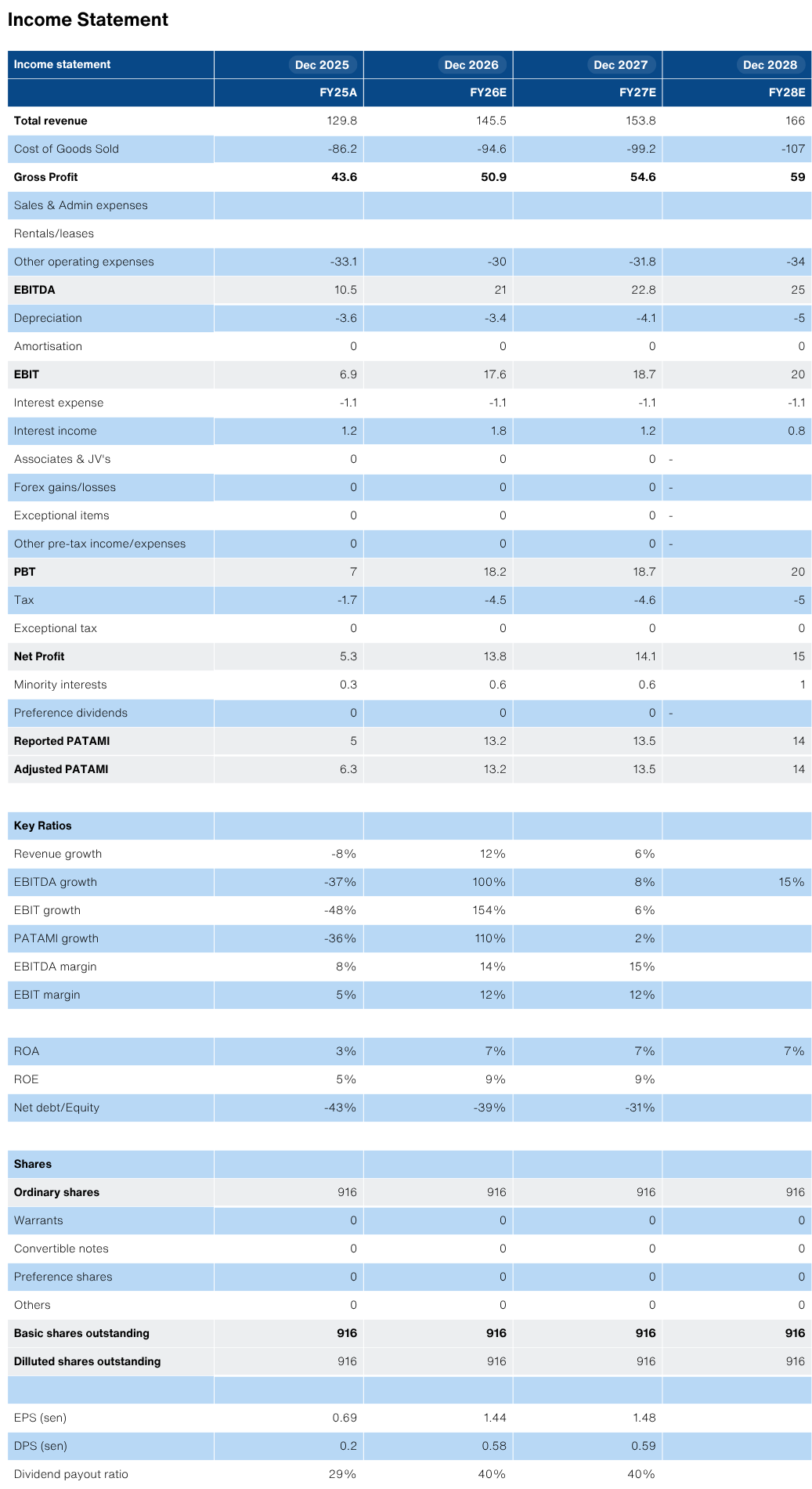

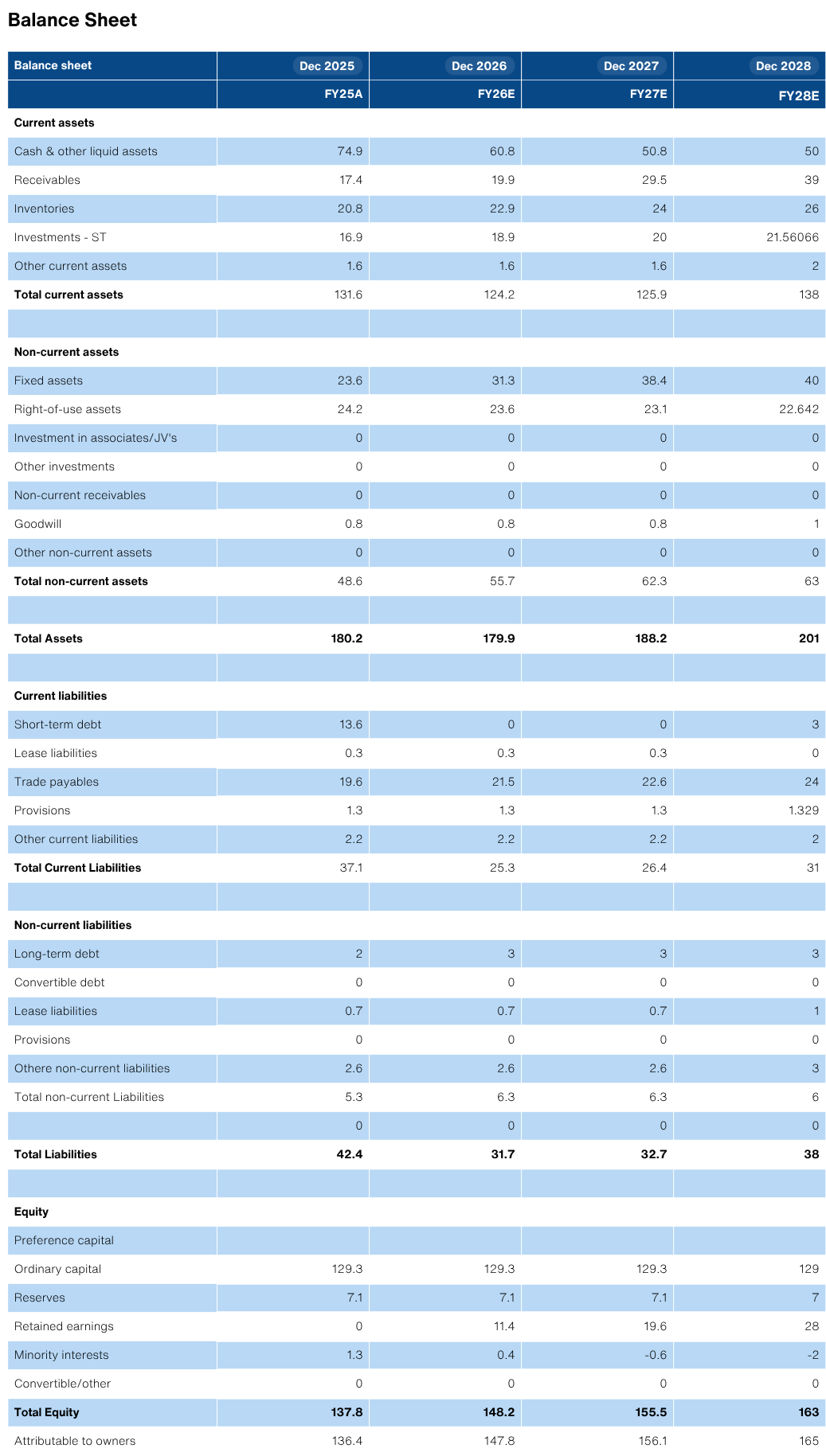

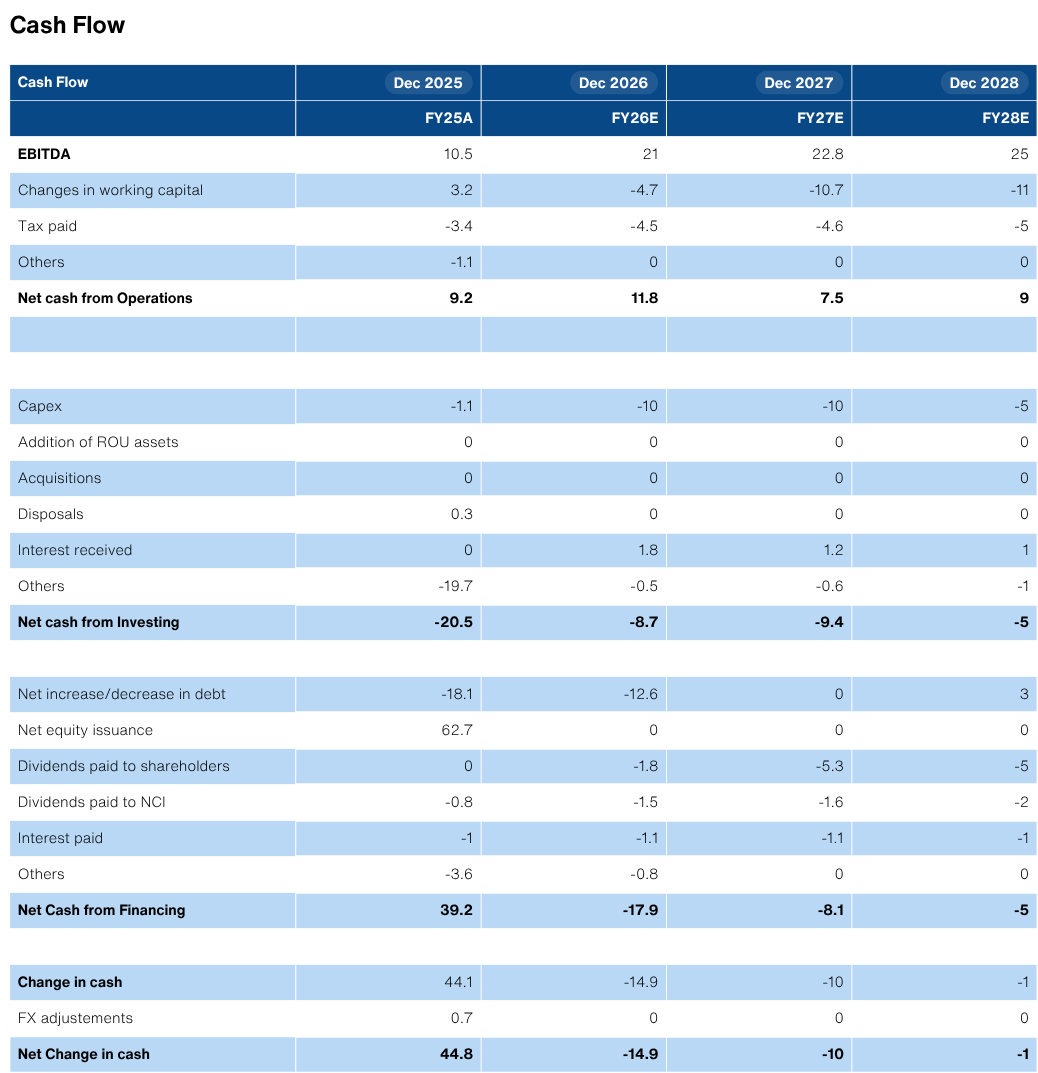

Selected financials

Source: Company Data, Bloomberg, NewParadigm Research, June 2026