Warehouse automation sleeper

PTT Synergy is emerging as a smart warehouse leader.

Stock information

PTT SYNERGY GROUP BERHAD

PTT | 7010.KL

BUY

Target price: RM2.00

Last price: RM1.50

Market cap (RMm): RM716m

Shares out: 485m

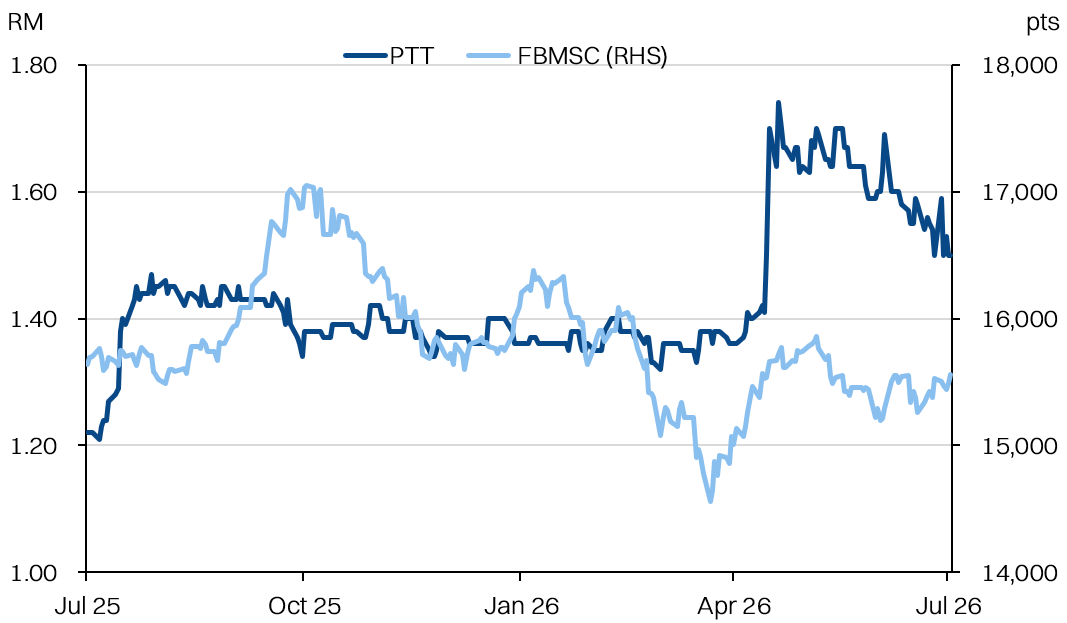

52-week range: RM1.21 / RM1.78

3M ADV: RM0.3m

T12M returns: 24%

Disclaimer: By using this information, you acknowledge that you are solely responsible for evaluating the merits and risks of any investment decision and agree not to hold NewParadigm Research liable for any damages arising from such decisions.

Key takeaways

- PTT Synergy is emerging as a dominant warehouse automation player with ~RM2.5bn GDV in the pipeline.

- Key event: handover of a flagship est. RM550m project to a major US-based semiconductor client later this month.

- Company’s reported financials (high debt, lumpy earnings) mask strong long-term contracts with top-tier clients.

Share price performance

Investment fundamentals

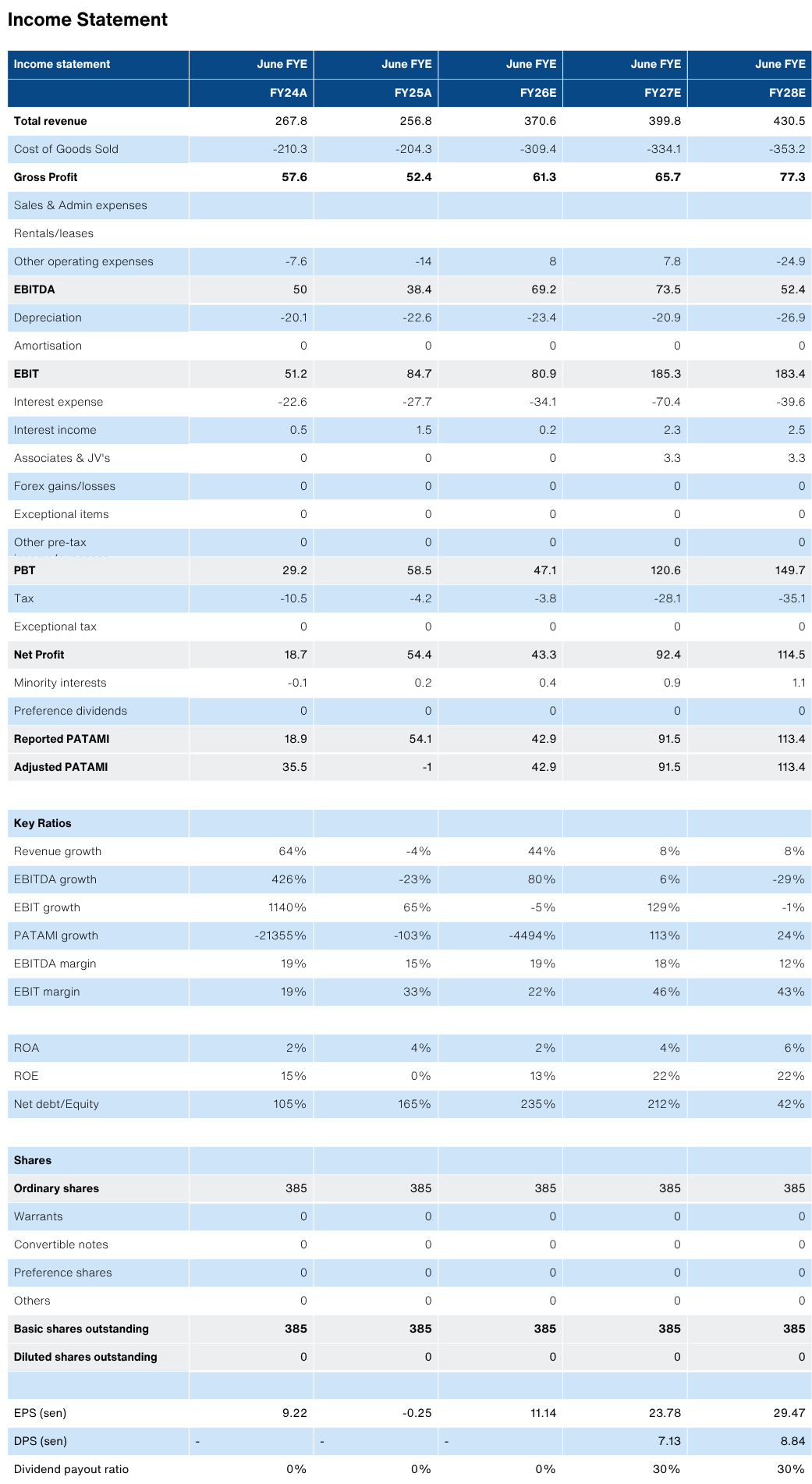

| RMm (June FYE) | FY25A | FY26E | FY27E | FY28E |

|---|---|---|---|---|

| Revenue | 257 | 371 | 400 | 430 |

| Revenue Growth | -4% | 44% | 8% | 8% |

| EBITDA | 38 | 69 | 73 | 52 |

| EBITDA margin | 15% | 19% | 18% | 12% |

| Adj PATAMI | -1 | 43 | 92 | 113 |

| PATAMI margin | 0% | 12% | 23% | 26% |

| ROA | 0% | 2% | 4% | 6% |

| ROE | 0% | 13% | 22% | 22% |

| PER (x) | <-100% | 17 | 8 | 6 |

| P/BV | 2 | 2.2 | 1.7 | 1.4 |

| Yield | 0.0% | 0.0% | 3.8% | 4.7% |

Source: Company data, NewParadigm Research, July 2026

Overlooked automation stock

- We think the headway PTT Synergy has made into warehouse automation has been overlooked by the market. The group has secured top-tier clients, including global FMCG brands and MNC semiconductor supply chain leaders. Management has indicated a GDV pipeline of ~RM2.5bn to drive growth.

- A key catalyst comes later this month with the launch of the Penang-based PTT Semiconductor Logistics Hub 1 in Valdor Business park. The project has an estimated GDV of RM590m, a capacity of 52.2k pallets and a throughput of 680 pallets/hr. Channel checks suggest this are market-leading, at least for Malaysia.

- The attention from the launch should spur more interest in the stock, and hopefully address one of its key pain points - the low trading liquidity. What is promising is that PTT Synergy has recently concluded a 10% private placement, which includes some institutional funds - a promising sign that the stock is enjoying a widening investor base with improving quality.

- It is worth flagging the challenges - PTT Synergy has taken on substantial leverage (~200% net gearing) in order to fund the capex-heavy warehouse build out. However, all these projects have the aforementioned top-tier customers committed to at least 10-year leases. The creditworthiness of the underlying contracts has allowed PTT Synergy to secure bank financing as well as flip its completed projects to counterparties like CapitaLand Malaysia. We expect PTT Synergy will continue to monetise its developments going forward in order to recycle capital into new projects.

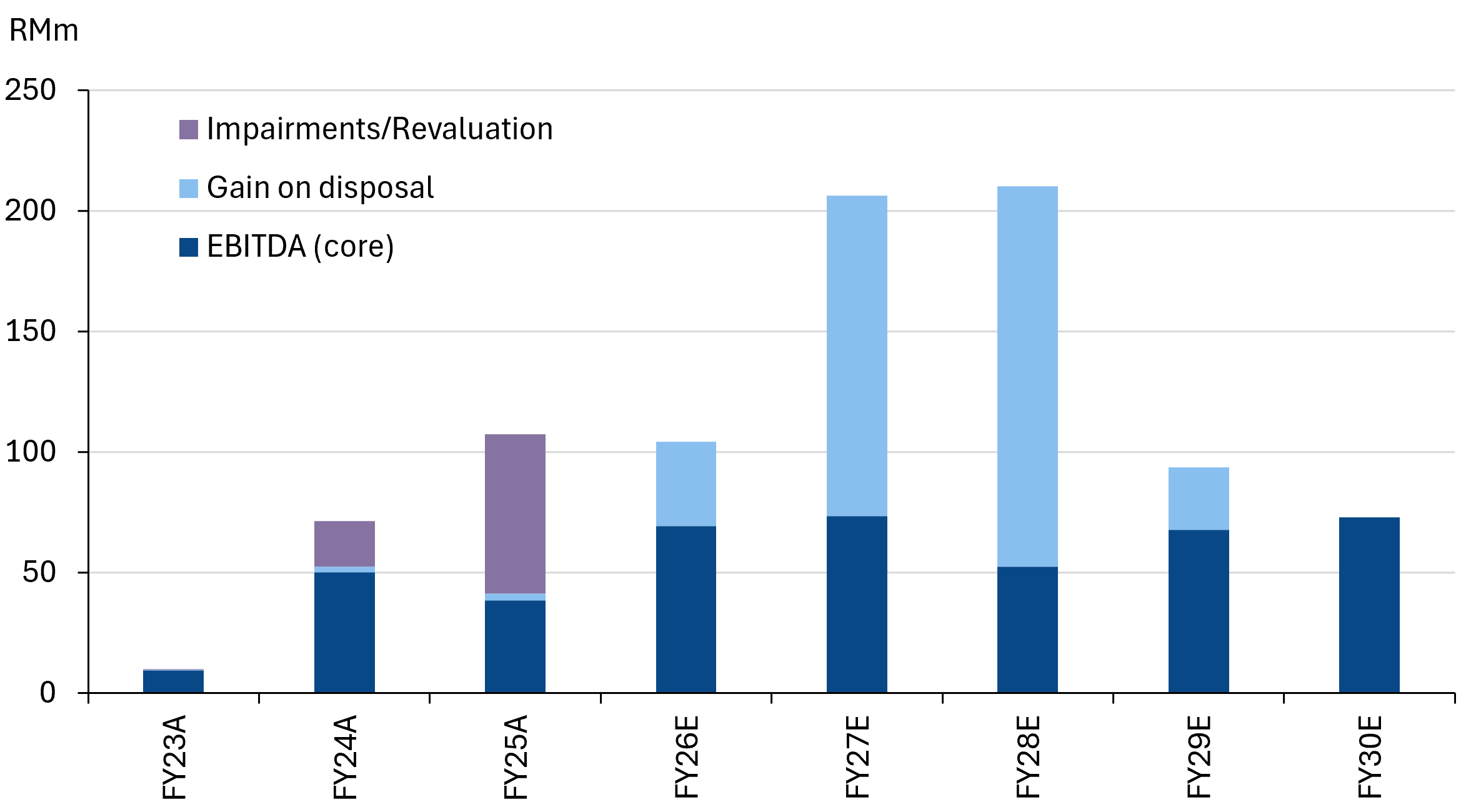

- In turn, the final challenge is the somewhat muddied earnings profile - distorted by lumpy one-off gains, despite the strong underlying recurring rental and robotics income. Nonetheless, we expect to see PTT Synergy potentially hit RM80-90m in NP in FY27/28E, pending timing of asset monetisation.

Initiate with RM2.00 TP

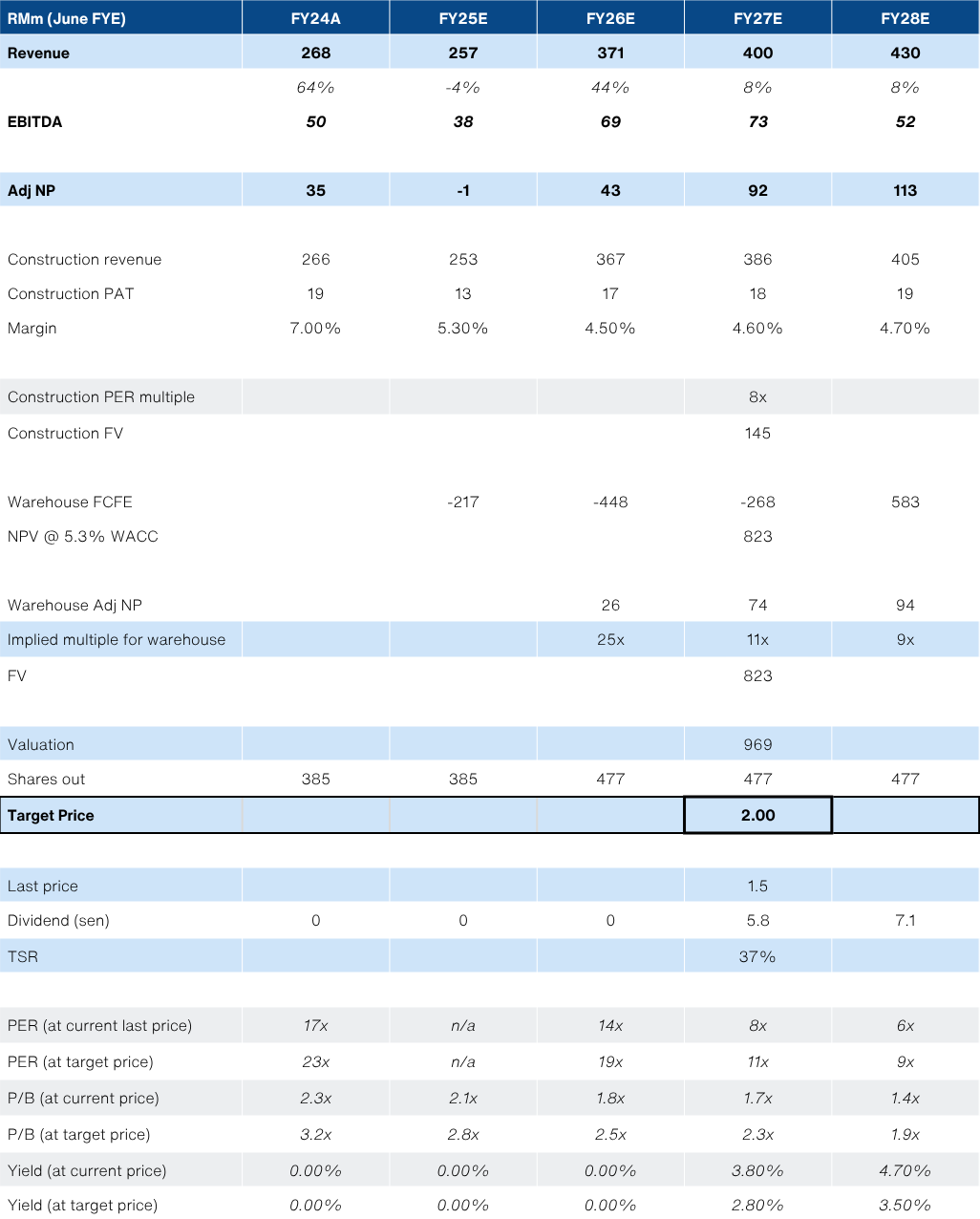

- We initiate coverage on PTT Synergy with a BUY recommendation and a TP of RM2.00 based on a SOP methodology. This implies a PER of 11x FY27E.

About the Company

PTT Synergy has transitioned from a earthworks construction company into an integrated smart warehouse solutions player with a funnel of ~RM2.6bn worth of projects. The smart warehouse soutions are offered via built-to-suit, solutions as a service (SOLAAS) as well as turnkey. The business model is capex heavy, but backed by long-term contracts with clients (typically 10 years). It is still at a relatively early stage with two completed buit-to-suit projects, with one already monetized to recycle capital.

About the Stock

PTT Synergy in its current form is the result of a reverse takeover of Grand Hoover Bhd in 2021. It is a main market-listed stock that is ~54% controlled by founders, directors and brothers - Teo Swee Leng and Teo Swee Phin.

The stock has historically seen minimal institutional interest, but in recent months, the company has managed to attract a few institutional funds to take up shares via a private placement.

Investment Thesis

PTT Synergy’s business model is simple - deliver substantial cost savings to customers by automating warehouse operations. This proposition has already gained validation but limited market recognition.

The first smart warehouse - PTT Logistics Hub 1 - was successfully monetized via a sale & leaseback with CapitaLand Malaysia, backed by a long-term lease with a global FMCG client. PTT Synergy is also attracting top-tier customers. The next project completing in Penang is for a US-listed semiconductor MNC. However, the company has only limited visibility in the market due to confidentiality as well as fairly nascent track-record. Earnings, while genuine are muddied by the asset monetization model - lumpy one-off recognition. At the same time, the front-loaded capex has bloated the balance sheet with net gearing of 200% on net debt of RM731m. However, with an implied interest cost of ~4%, the lenders are signaling that the credit quality of the company is much better than the headline gearing suggests.

We see the coming newsflow on the Penang warehouse handover as well as new customer projects from the RM2.5bn funnel as a catalyst to drive re-rating in the stock’s underlying value.

Key Risks

- Execution risk: PTT Synergy is undeniably highly leveraged. Failure to secure financing for new projects, or poor execution (e.g. delays) pose severe risks if PTT Synergy is not able to continue developing and monetizing its built-to-suit warehouse pipeline.

- Delayed monetisation: PTT Synergy has several options to monetize its developments, including outirght sale, REIT-ing the assets, or stake sale. However, given the high leverage, even a delay spanning multiple months could be very costly for PTT Synergy as the capital needs to be recycled into new projects. This could put the company under pressure to raise funding in other ways, including additional dillutive private placements.

- Competition: While PTT Synergy has a strong headstart in this business, the barriers to entry are low. The underling warehouse automation technology is both mature and somewhat commoditized. The main challenges competitors will face are developing systems integration, designing optimal solutions, and having a strong balance sheet for the up-front capex (for the built-to-suit) model. These are not insumountable.

A short track-record and an impressive funnel.

We anticipate that the launch of PTT Synergy’s Semiconductor Logistics Hub 1 should mark a turning point for the stock - improved visibility on the company’s smart warehouse business that has largely gone unnoticed by the market.

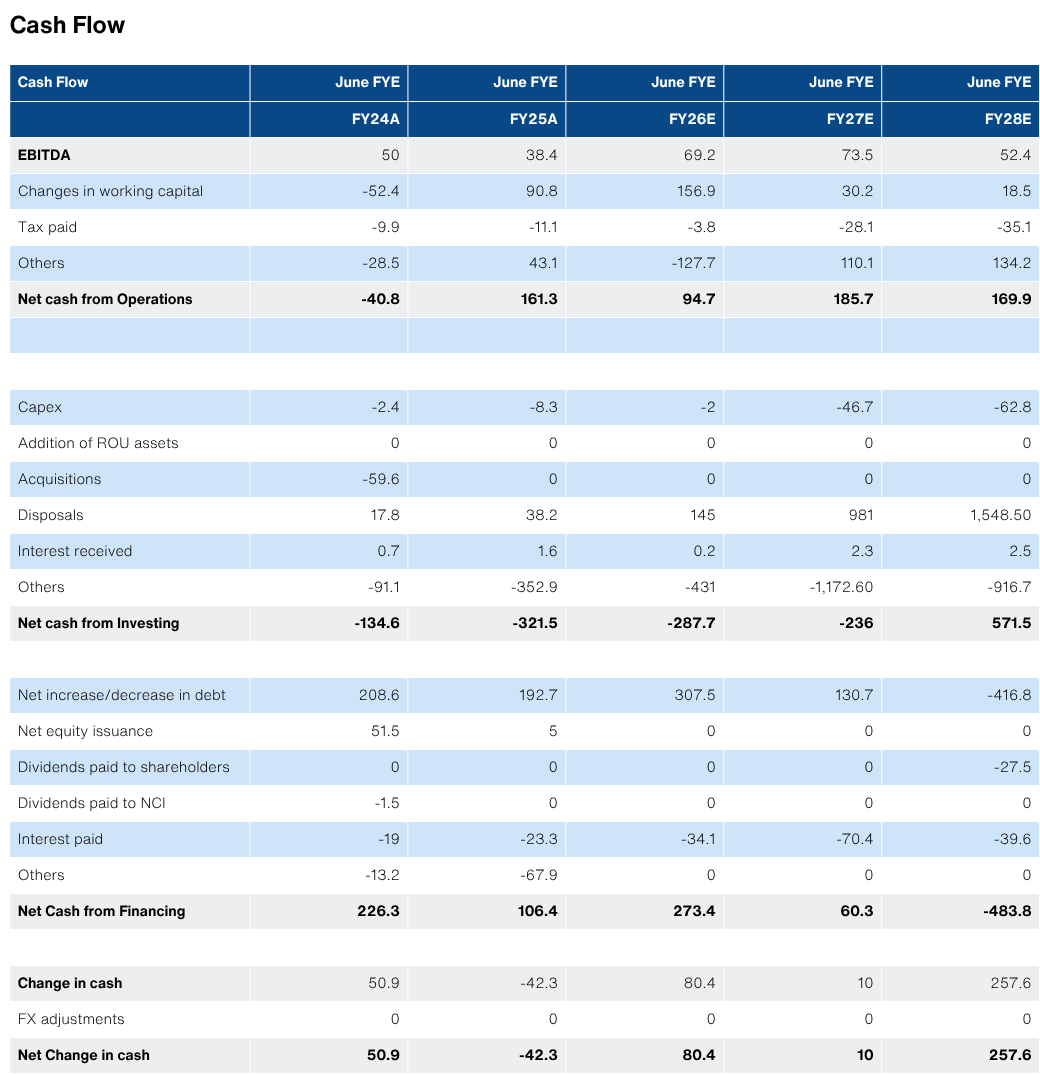

To be fair, PTT Synergy’s track record is limited. It only began the capex-hungry built-to-suit business in March 2024 - PTT Logistics Hub 1 in Elmina West, Selangor. But today, the group has already monetised its first project via a sale and leaseback arrangement with CapitaLand Malaysia (for RM180m in Nov 2025) that netted a tidy ~RM35m gain on disposal.

Crucially, the company has leveraged this track record into an RM2.5bn project funnel, across Selangor, Penang and Johor, as well as Thailand and Indonesia. We had the opportunity to visit the warehouse at Elmina and the operations were impressive. Of the 168,000 sqft, only about 22,000 sqft is accessible by workers. The rest is fully automated. This has allowed for massive reduction in manpower requirements - only ~10% of a conventional warehouse.

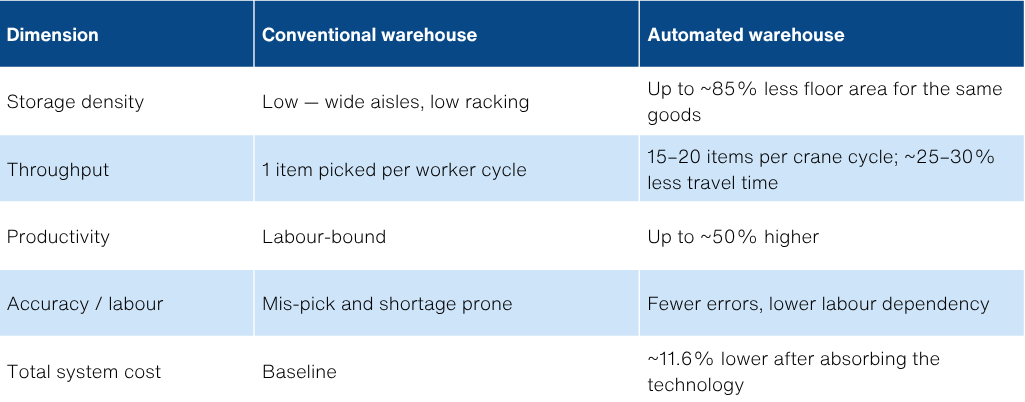

Additionally, the efficiency gains cannot be overstated. The warehouse is able to achieve a throughput of 220 pallets/hour - substantially higher than a conventional warehouse, which typically needs about half a dozen manpower and ~30mins for a single pallet. The use of stacker cranes and within an automated storage and retrieval system (ASRS) also allows the pallets to be stacked much more densely - almost 85% floor space reduction, going from 10sqft/pallet to only about 2sqft/pallet. Real time inventory management is also another huge bonus for clients - with pallets in a restricted area and digital twin inventories - the need for regular and costly inventory checks becomes obsolete.

And PTT Synergy is just getting started. The Semiconductor Logistics Hub 1 in Penang will see 3x the throughput at 680 pallets/hr on 50% more storage capacity. It will be a very high SKU mix, since this will be for manufacturing operations that will require both high throughput and accuracy. For now, the customer name is not released, but is expected to be announced with the launch later this month.

In turn, we see this a key catalyst for the market to take seriously PTT Logistics RM2.5bn project funnel. We ascribe a valuation of RM2.00/share on a SOP methodology that implies a PER of only 11x FY27E earnings.

Advantages of warehouse automation

What makes a smart warehouse?

A smart warehouse integrates multiple autonomous systems, to minimize labour requirements and optimize efficiency:

- Storage efficiency: Conventional warehouses are limited to stacking pallets about 5-6 pallets high. With a stacker crane, a smart warehouse can accommodate up to 30 pallets high - about 5x higher. Additionally, a conventional warehouse would require more space between racks for reach trucks to operate. Overall, a smart warehouse can utilize as little as 2sqft/pallet compared with 10sqft per pallet for a conventional warehouse.

Stacker cranes allow for over 5x vertical stacking of pallets

Less labor: A conventional warehouse might need as many as 7 workers (e.g. forklift operator, power pallet truck operator, reach truck operator) for a single storage/retrieval cycle. In comparison, a smart warehouse all but eliminates most of these tasks, save for the final loading into the trucks. Another example is picking - breaking down pallets to cartons or cartons to pieces. The pallets brought directly to the pickers and the necessary quantities are presented on a screen. The pickers simply scan the cartons (or pieces) and moves it from on side of the station to the other, where a subsequent QC step ensures high accuracy. Overall, a smart warehouse can reduce labour requirements by 80-90%.

AGV’s autonomously retrieve and store pallets

Labour requirements are reduced by 80-90%

Fewer human operated vehicles: A conventional warehouse will require a fleet of forklifts, power pallet trucks and reach trucks. Both power pallet trucks and reach trucks can almost entirely be eliminated. Only forklifts are still required to load the trucks. This has huge savings on maintenance, but also safety, since operator error can result in injury or damage to property over thousands of manhours in operation.

A forklift mobile robot - reduces manual forklift requirements

Pallet stacking robot

Real-time inventory tracking: With scanners, smart warehouses can accurately determine the contents of each pallet, and even the cartons and pieces within. This ensures high accuracy. PTT Synergy’s management claims over 99% accuracy. This is thanks to a scanners that track in/outbound pallets. The more cutting edge Semiconductor Logistics Hub 1, will also implement scanners that can check the contents of the pallets to determine carton/pieces SKU. This also substantially reduces the need for inventory management to prevent pilferage. Typically, a conventional warehouse would have to conduct monthly or even weekly inventory checks. And even then, there is risk of pilferage.

PTT Logsitics Hub 1 has a throughput of 220 pallets/hr

Efficiency and cost savings: Combine the aforementioned benefits, and a smart warehouse is able to achieve high throughput without a labour bottleneck. This also creates substantial indirect savings to total operating costs. For example, higher accuracy reduces returns, faster loading can reduce idle times for trucks, and real-time inventory tracking can reduce auditing costs. The lower headcount also drives huge cost savings, directly, as well as indirectly - reducing the need for large supporting infrastructure like canteens when headcount is in the hundreds. Cost is definitely a significant driver, but the efficiency is also not something that conventional warehouses can replicate. PTT Synergy’s Semiconductor Logistics Hub in Penang is designed for a throughput of 680 pallets/hour - a pace that conventional warehouses simply cannot match.

The business model

PTT Synergy has 3 distinct sub-segments or operating models:

- Built-to-suit: This is the main focus of the group. It is capex heavy since PTT Synergy will have to undertake the full investment up-front - Construction, fixed equipment like racking, and the robotics assets. PTT Synergy either tenders for such projects competitively (as is the case with PTT Semicon Logistics Hub), or begins with a project management consultant (PMC) role, helping the client scope and design a solution. That PMC role is subsequently converted to a full built-to-suit project. PTT Synergy appears to be tapping into its long-term relationship with Sime Darby Property, with a few of its projects located on the latter’s land. PTT Synergy also has some landbank of its own in Pontian (~20 acres) and Kulim (~125 acres). The Pontian project is already sold-on to a financial investor, with several clients committed to the smart warehouse as lessors, thus behaving more like a property development project.

- SOLAAS: Solutions as a service. This requires less capex. PTT Synergy only implements the robotics solutions for a recurring fee. However, the building is either owned by the client themselves or a third party. The one project here that has been announced is the 76,000 pallet capacity warehouse for MyDin. Sime Darby Property will own the warehouse. Prior to MyDin, PTT Synergy has also completed another SOLAAS project for a MNC beverage company.

- Turnkey: This is the smallest focus for the group - selling the solution lock, stock and barrel to the client. This has good margins but is one-off in nature.

PTT Synergy plan is to assume maximum project level leverage - up to 90% - to minimize capital outlay. For land, PTT Synergy typically aims to partner with landowners (like Sime Darby Property) on some sort of profit share arrangement to further reduce outlay. For now, given the high ongoing capital requirements, management aims to monetize the REIT-able portion of its developments to recycle capital into new projects. The disposal to CapitaLand is just one example. Going forward management is exploring more options, include partial equity stake sale as well as transferring the assets into a REIT.

Keep in mind, PTT Synergy still has another service layer on top of the base rental - the robotics income. PTT Synergy charges clients a per-movement fee with a minimum quantity guaranteed of 85%. This means the group has some revenue upside, tied to the actual throughput of the warehouse. We estimate robotics income will be about 8-10% of the base rental.

PTT Logistics Hub 1

Competitive landscape

We view the warehouse automation space as highly competitive. However, key moats for PTT Synergy include - 1) capability to fund capex, 2) strong supply chain support, 3) systems integration track record, 4) delivery at scale.

There are other companies offering similar offerings as PTT Synergy - DNC Automation, XTS Technologies and Ho Lao (a larger China-parented automation contractor). We also found CelcomDigi Bhd venturing into the space as part of its 5G offering (link).

CelcomDigi is a potential competitor

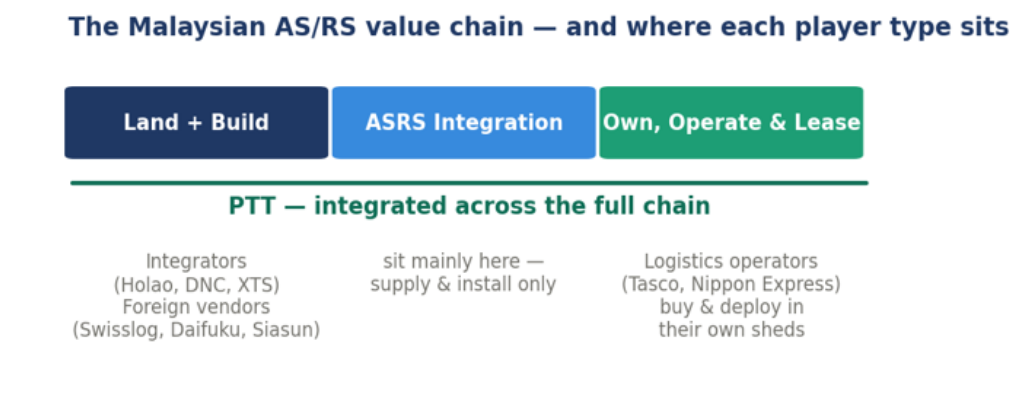

PTT Synergy’s edge appears to be its ability to span the entire value chain and deliver the substantial cost savings to the end-client, while still preserving decent margins for itself. It also helps to be delivering some of the largest projects in the country and being public listed as well.

In contrast, PTT Synergy’s other competitors are private companies (or in the case of CelcomDigi Bhd, only a relatively small non-core venture). Furthermore, the competition appears to only occupy a handful of sub-segments within the value chain. Holao, DNC and XTS are focused on equipment integration. Foreign vendors (Swisslog & Daifuku) focus on supply and install. Third-party logistics (3PL) players (like Tasco Bhd) are skewed to deploying automation to their own facilities.

PTT Synergy’s pitch is that it is able to deliver a solution that is built-for-purpose. Warehousing is not a core competency of most clients - and PTT Synergy is able to provide project consulting at an early stage to help some clients better understand their own requirements.

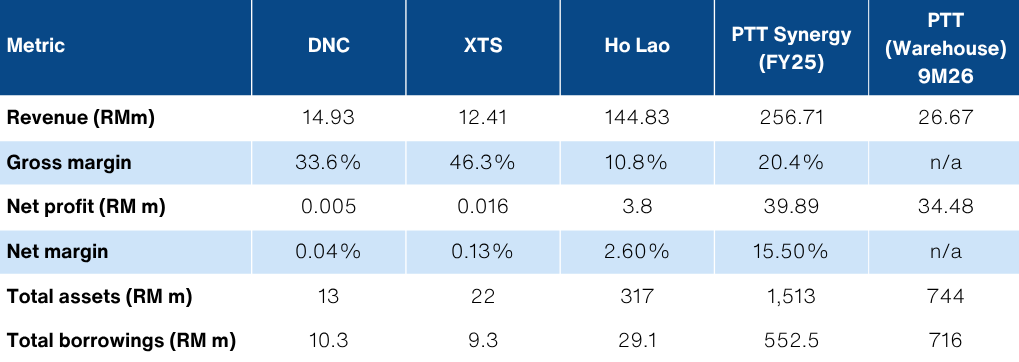

We have compiled the financials of peers, but flag that it is not an ideal comparison. PTT Synergy books substantial inter-company revenues due to the overlap with the internal construction unit that builds the warehouses. Additionally, the nature of the profit recognition is distorted by the one-off and lumpy gain on disposal - margin comparison may not be reflective. However, management indicated that the gain on disposal from PTT Logistics Hub 1 is about 25%. While this is ahead of competitors, it is worth noting that this behaves more like a property development business. Another issue, is that we do not currently have a clean carved out income stream for PTT Synergy’s recurring robotics income which comes on top of the REIT-able income.

Financial comparison

Then again, this comes back to the fact that PTT Synergy does not really have direct peers that are able to span the whole value chain.

PTT Synergy spans the value chain

The funnel

PTT Synergy has already announced 4 smart warehouse projects:

- PTT Logistics Hub 1 (Elmina West, Selangor)

- PTT Logistics Hub 2 (Elmina West, Selangor)

- PTT Semicon Logistics Hub (Valdor Industrial Park, Penang)

- Sekata E-Logistics Hub (Pontian, Johor)

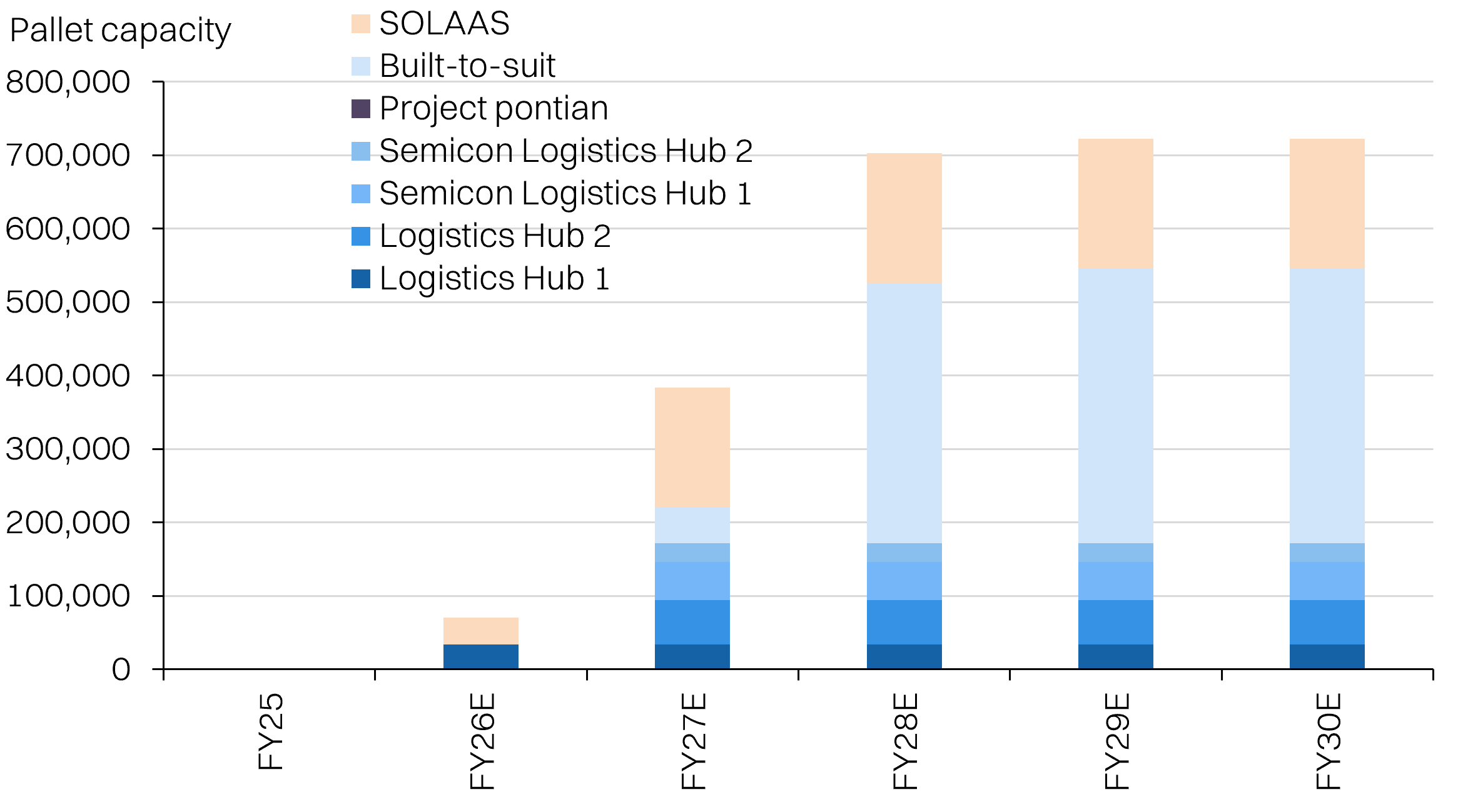

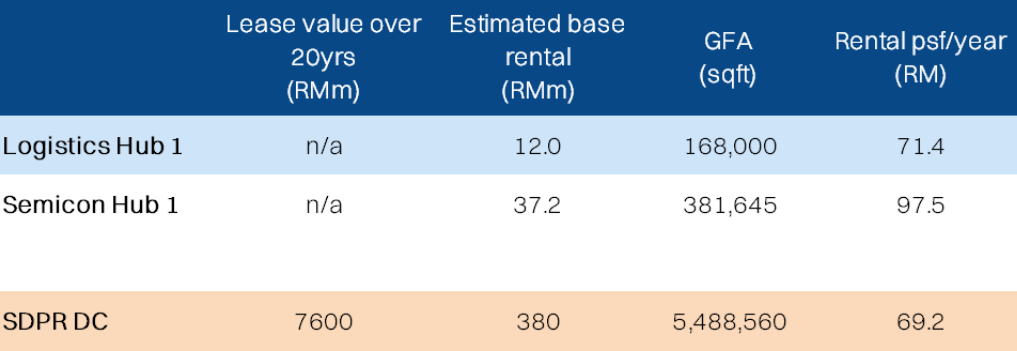

These projects alone have an estimated GDV of RM1.5bn across ~1.1m sqft with an estimated capacity of 220,000 pallets. The potential rental income from these properties would be about RM80m/annum. This does not yet include robotics income which could be another 8-10% on top.

Management indicated that it is pursuing another 8-10 prospects that pushes the overall GDV funnel to RM2.5bn. Critically, the turnaround on these projects are typically quite fast with a construction time of ~12 months to completion - leveraging on PTT Synergies internal construction expertise.

Including SOLAAS, PTT Synergy could hit >700k pallet capacity

What has been holding PTT Synergy back?

It is worth addressing some of the issues that have held back PTT Synergy’s market recognition as well as its share price:

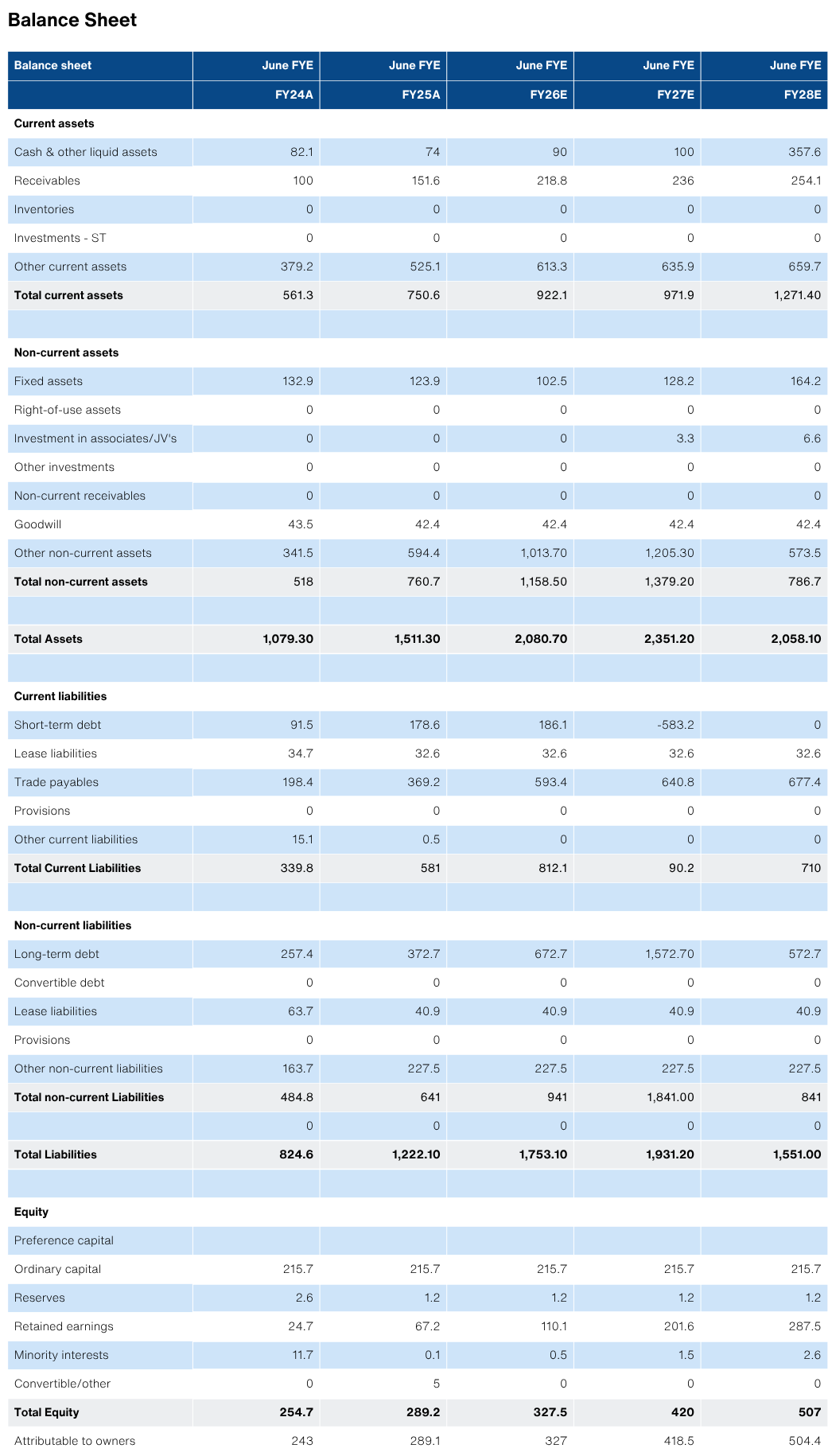

- Gearing is high - With 200% gearing and almost RM1bn in gross borrowings, a quick screen of the balance sheet has been a turn-off for many investors. This is simply a reflection of the capex-heavy nature of the built-to-suit model that PTT Synergy is undertaking. Critically, we noticed that PTT Synergy’s implied interest cost is surprisingly low - only ~4%. The banks appear to be relatively comfortable with the credit risk - at least at the project level - which is backed by (on average) 10-year contracts with top-tier clients. Additionally, this has allowed PTT Synergy to gear up to 90% at the project level.

- Earnings profile is muddy - Is PTT Synergy a REIT? A property developer? A solutions provider? A construction company? This isn’t self-evident from the financials. If anything, the relatively recent exit of non-core business further muddies the earnings trajectory. So far, the primary contribution has come from the disposal to CapitaLand (~RM35m gain). But this is one-off and lumpy. We think this has thrown investors off the scent, on the underlying earnings potential of the RM2.5bn funnel.

- Newsflow has been limited - Due to high confidentiality requirements by clients, PTT Synergy has been highly restricted with what it can announce. Most clients insist on not being named. Thus far the only named end-client is MyDin, under the SOLAAS sub-segment. However, based on the 5 publicly known projects being undertaken (PTT Logistics Hub 1&2, PTT Semicon Hub 1&2, Pontian 5 warehouses), we estimate that there is already ~RM1.5bn worth of projects in hand (GDV).

- Market underestimates value-add - Automating a warehouse does not sound like high-value work. But some of the numbers suggest otherwise. Based on a yield of slightly over 6%, PTT Synergy was able to sell Logstics Hub 1 to CapitaLand for RM180m. This implies a value of >RM1k psf. Additionally, with a rental yield (before robotics income) of ~RM71psf, this is basically in-line with the datacenter yields that Sime Darby Property is generating in the surrounding area. We’d argue that a smart warehouse as high SLA requirements as well - redundant power supply, multiple network failovers, and substantive operational redundancy.

PTT Synergy’s smart warehouses can generate similar rental yields to data centers

Valuation methodology

We ascribed a value of RM2.10 per share to PTT Synergy, implying a PER of 7x FY27E, based on a sum-of-parts methodology. We flag that the PER is articficially depressed because of the lumpy one-off nature of PTT Synergy’s disposal gains.

Which is why for valuing PTT Synergy’s warehouse segment we applied a 2-stage DCF methodology, which arrived at a valuation of RM663m.

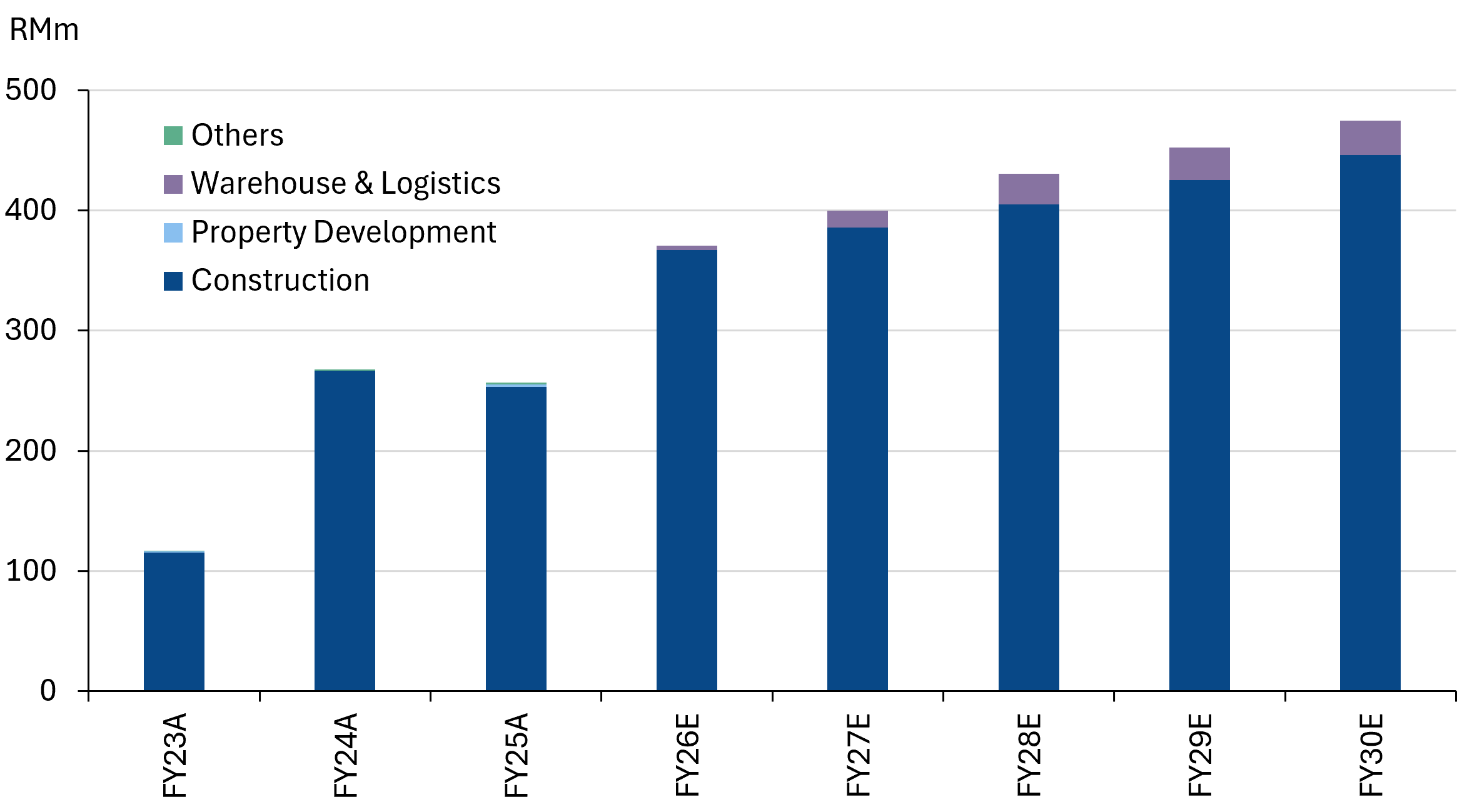

At the same time, we also looked to apply a valuation to the construction arm, which appears to be operating a stable steady-state that generates about RM17-18m in profits each year. We value this segment at 8x FY27E PER, which is roughly a 20% discount to the mid-cap construction peer average PER of 10.6x. We think the discount is reasonable, given there is limited focus to grow this segment’s external orderbook.

Lastly, we flag that our valuations are likely to be diluted by share placements over the next 12 months. We anticipate that management will need to raise more capital to undertake the RM2.5bn funnel that it is planning for, posing up to 10% dilution/

PTT Synergy’s smart warehouses can generate similar rental yields to data centers

Earnings outlook

We have assumed a cumulative ~700k pallet capacity build out by 2030 and a GDV pipeline of RM2.5bn, we estimate that PTT Synergy will be sitting on REIT-able income of ~RM280m gross annually once this pipeline is completed. In addition, there is potential for another RM21.3m in robotics income for the group annually.

However, we have also assumed that the group will continue with its asset monetization model. We have assumed that PTT Synergy will dispose at least 51% of its equity in most assets to deconsolidate it from the balance sheet. Management has indicated multiple pathways to monetize the assets, including outright sale, partial stake sale, and injecting the assets into a REIT.

The monetization pathway is the most unpredictable part of our modelling, since management cannot disclose its plans in detail for each project - over a dozen in the pipeline.

Nonetheless, we have assumed a conservative 15% gain on disposal for each asset, with an average disposal equity of 51%.

Revenue projection - direct contribution from warehouse is masked

Warehouse contribution will be via gain from disposal.

Directors and management

The current Board was assembled following the February 2021 takeover of Grand Hoover Berhad (since renamed PTT Synergy) by Aim Tetap Teguh Group Sdn Bhd ("ATTG"), the private vehicle of Dato' Abd Rahim (51%), Teo Swee Leng (25%) and Teo Swee Phin (24%). The three promoters joined the Board on 18 March 2021 and collectively control led ~62.2% of PTT at the onset, including a collective indirect stake of 45% via a private vehicle, ATTG. That position has since been diluted to 40.77%, with Swee Phin holding another 13.6% directly. The Board comprises five executive directors and three independents.

Governance observations: The Board is executive-heavy (5 of 8), below the MCCG recommendation that at least half the board be independent; all three INEDs date from the 2021 takeover (~5-year tenure); and the Executive Chairman retains an active private construction interest (Aim Concept), a recurring source of related-party transactions. Offsetting this, the key directors control ~54% of the company, aligning interests.

Dato' Hj Abd Rahim bin Hj Jaafar — Executive Chairman

Appointed 18 March 2021. The largest shareholder in ATGG, with a 51% stake. A civil engineering graduate (London South Bank University) with over 28 years in construction and project management, he has undertaken ~RM1.0bn of contracts over 12 years through private vehicles — notably the RM579m UPM Teaching Hospital and RM375m Hospital Pasir Gudang (design-and-build). He remains a shareholder and director of Aim Concept Sdn Bhd, a private design-and-build contractor; related-party dealings are disclosed in the circular dated 28 Oct 2025. No other listed-company directorships.

Terry Teo Swee Leng — Executive Deputy Chairman

Appointed 18 March 2021. Holds 1.9% directly plus 25% of ATTG (40.77% stake). Over 39 years in construction and 16 years in property development, largely through Pembinaan Tetap Teguh Sdn Bhd ("PTTSB") — the earthworks and infrastructure contractor the Teo brothers built (Elmina East/West works for Sime Darby Property, among others), which PTT acquired for RM152m in August 2023 and which now anchors the group's construction division. Honorary Consul of Nepal in Malaysia (2017–2027). Elder brother of Teo Swee Phin.

Teo Swee Phin, A.M.T — Group Managing Director

Appointed 18 March 2021. The largest shareholder overall with a direct stake of 13.6% as well as 24% of ATTG (40.77% stake). Over 24 years in construction and 17 years in property development alongside his brother at PTTSB; sets group business direction and oversees construction operations. Diploma in Technology (Building), TAR College; Executive MBA (2023). Conferred the A.M.T by the Sultan of Terengganu in April 2025.

Tracy Tang Choi Peng — Group Chief Strategy Officer cum Executive Director

The group's most senior professional (non-family) manager. Joined PTTSB in 2009, rising to Group Financial Officer (2016); appointed CFO of PTT in September 2021, promoted to Group CEO cum ED in March 2024, and redesignated Group CSO on 2 March 2026 — with the Group CEO role passing to Dan Then Ikh Choo (ex-CEO of PTT Logistics), who sits outside the Board. Accounting and finance graduate (Leicester) with ~29 years across construction and property, including Gadang Land and Tanco Holdings.

Datin Ng Fong Shiang (Angie) — Executive Director

Appointed 29 May 2023. Leads the group's corporate finance function — capital structuring, funding and financial advisory. Over 23 years in financial advisory across banking, construction, property and steel. Also a director of Straits Energy Resources Berhad.

Independent directors

Dato' Mahamed bin Hussain — Independent Non-Executive Director

Appointed 18 March 2021; chairs the Audit, Remuneration and Nomination Committees. A retired senior civil servant — formerly Head of the Development Division at the Ministry of Higher Education, with earlier stints in land administration (Ulu Selangor, KL Land Office).

Datuk Ir. Ruslan bin Abdul Aziz — Independent Non-Executive Director

Appointed 18 March 2021. A career JKR engineer (from 1984), retiring in February 2021 as Senior Director heading the Road and Building Divisions; previously JKR State Director for Malacca and Selangor. Over 40 years in public building and infrastructure delivery.

Toh Seng Thong, JP — Independent Non-Executive Director

Appointed 28 April 2021. Chartered Accountant (MIA, MICPA, CA ANZ) with over 35 years in audit, tax and corporate advisory. Also an independent director of Rhong Khen International Berhad and Adventa Berhad.

Key Senior Management

Dan Then Ikh Choo — Group Chief Executive Officer

Appointed Group CEO on 2 March 2026, succeeding Tracy Tang; he does not sit on the Board. Over 19 years in intralogistics consultation and planning — distribution operations, regional distribution networks, 3PL warehouses and end-to-end supply chains for automated warehouses, distribution centres and e-commerce fulfilment hubs. Joined as CEO of PTT Logistics in May 2023, leading the warehouse and logistics division — the group's growth engine. His elevation signals the group's pivot from construction-led earnings toward the PTT Space smart-logistics platform.

Leong Kam Lan (Michelle) — Group Chief Financial Officer

Appointed Group CFO on 1 July 2026, promoted from Head of Accounts and Finance. She brings over 30 years of experience in audit, accounting and financial management across the construction, property development and IT sectors, with prior roles at Glenmarie Properties, IOI Properties Berhad and Dataprep Holdings Berhad. A Fellow of the ACCA (UK) and member of the MIA. She holds a direct interest of 413,184 PTT shares, with no directorships in other public companies and no family ties to directors or major shareholders. She succeeds Gan Chong Wei (Group CFO from March 2024), who ceased the role the same day to assume a new, undisclosed position within the group. We note that this is the second CFO transition since 2024.

Selected financials

Source: Company Data, Bloomberg, NewParadigm Research, July 2026