1Q26 - Seasonal drag

KJTS should benefit from rising energy costs.

Stock information

KJTS

KJTS | 0293.KL

BUY

Target price: RM0.86

Last price: RM0.745

Market cap (RMm): RM515m

Shares out: 691m

52-week range: RM0.66 / RM1.81

3M ADV: RM0.9m

T12M returns: -25%

Disclaimer: By using this information, you acknowledge that you are solely responsible for evaluating the merits and risks of any investment decision and agree not to hold NewParadigm Research liable for any damages arising from such decisions.

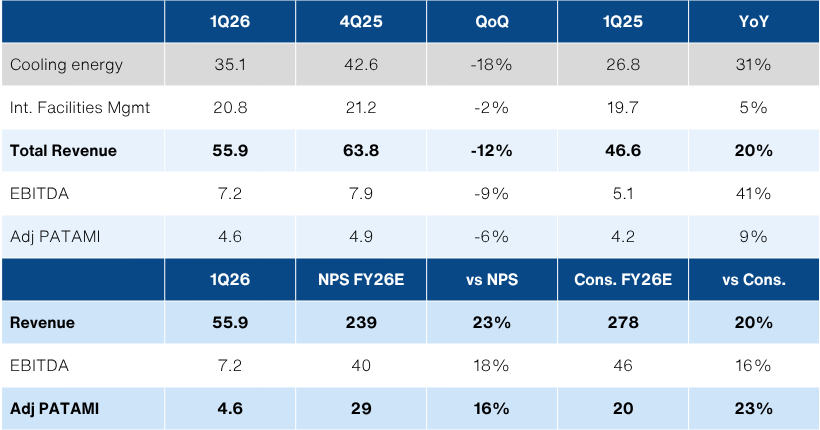

Key takeaways

- Adj NP of RM4.6m (-6% QoQ +9% YoY) was behind/ahead of ours/consensus FY26E expectations.

- Softer revenue recognition from lumpy EPCC works is partially due to seasonality and should see recovery in coming quarters.

- Maintain BUY with RM0.86 TP. Look past the soft 1Q26. KJTS is a beneficiary of higher energy costs.

Share price performance

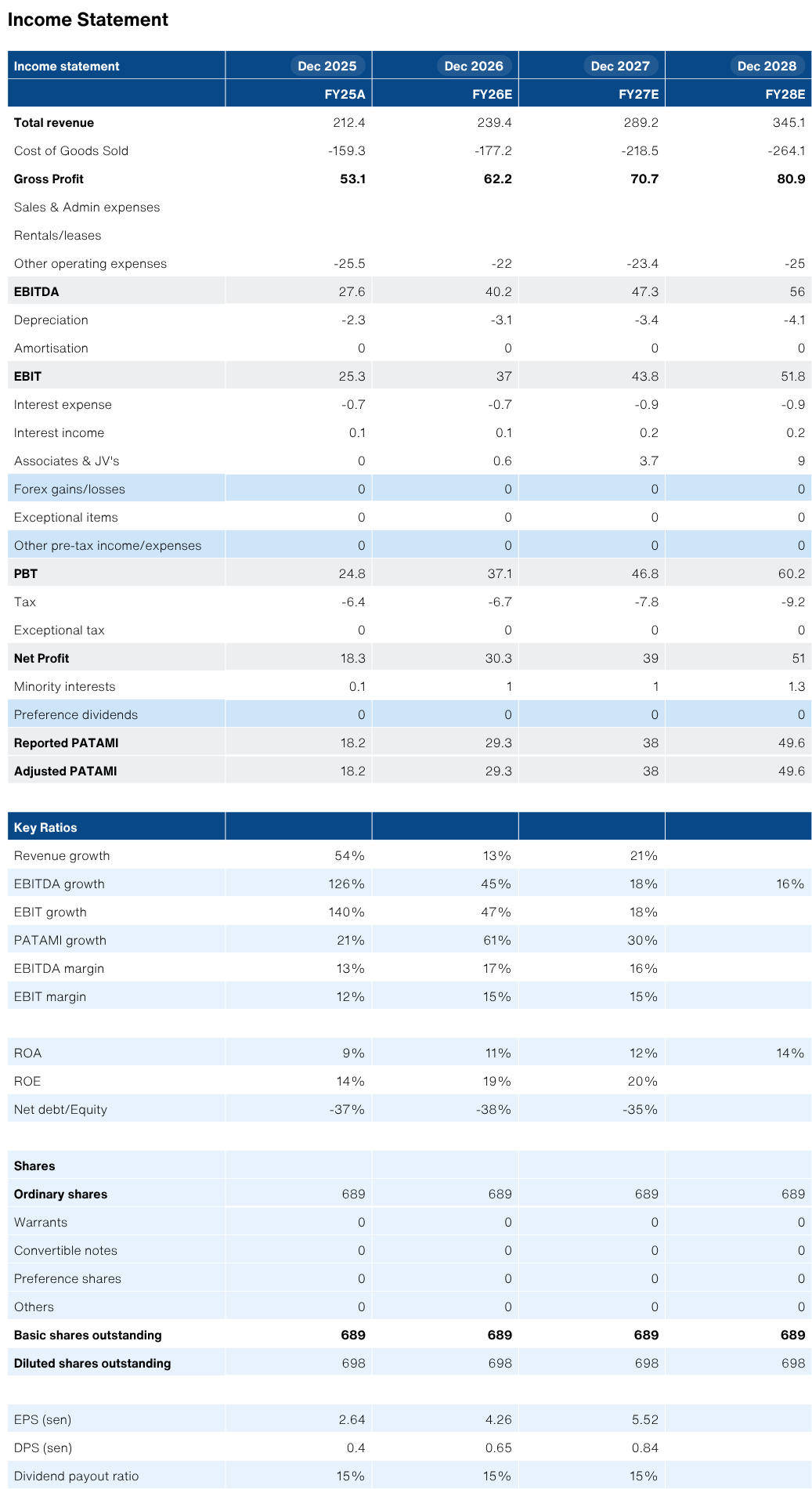

Investment fundamentals

| RMm | FY25A | FY26E | FY27E | FY28E |

|---|---|---|---|---|

| Revenue | 212 | 239 | 289 | 345 |

| Revenue Growth | 54% | 13% | 21% | 19% |

| EBITDA | 27.6 | 40.2 | 47.3 | 56 |

| EBITDA margin | 13% | 17% | 16% | 16% |

| PATAMI | 18.2 | 29.3 | 38 | 49.6 |

| PATAMI margin | 9% | 12% | 13% | 14% |

| ROA | 9% | 11% | 12% | 14% |

| ROE | 14% | 18% | 20% | 21% |

| PER | 28.2 | 17.5 | 13.5 | 10.3 |

| P/BV | 3.9 | 3.2 | 2.7 | 2.2 |

| Yield | 1% | 1% | 1% | 1% |

Source: Company data, Bloomberg, NewParadigm Research, May 2026

Underlying recurring income should be stable

- Revenue for 1Q26 of RM55.9m (-12% QoQ, +20% YoY) tracked our/consensus expectations, at 23% of full year estimates. In turn, the primary divergence between ours/consensus expectations are the margins - we have forecast 12% net margins against consensus 8%.

- Margins remained stable, despite the revenue contraction, but we note that the management fees from Lestari Cooling Energy is no longer being booked as other income, but recognized as revenue. In turn, the comparable margin is actually slightly better, despite the lower volumes.

Income statement

High energy costs to drive earnings growth

- Recall, the core thesis for KJTS is delivery energy efficiency gains for customers. In a rising energy price environment, demand for such solutions should increase. This will be boosted by the expansion into heat recovery solutions, that was acquired via iHandal.

- We estimate every 10% increase in the electricity tariff will drive up earnings by ~3%, from the recurring cooling management services. Additionally, management has indicated a sharp uptake in enquiries for energy management solutions across cooling and heat recovery as well.

- We reiterate our BUY call with unchanged TP of RM0.86. Normalization in earnings momentum should drive stock re-rating against the relatively low expectations currently.

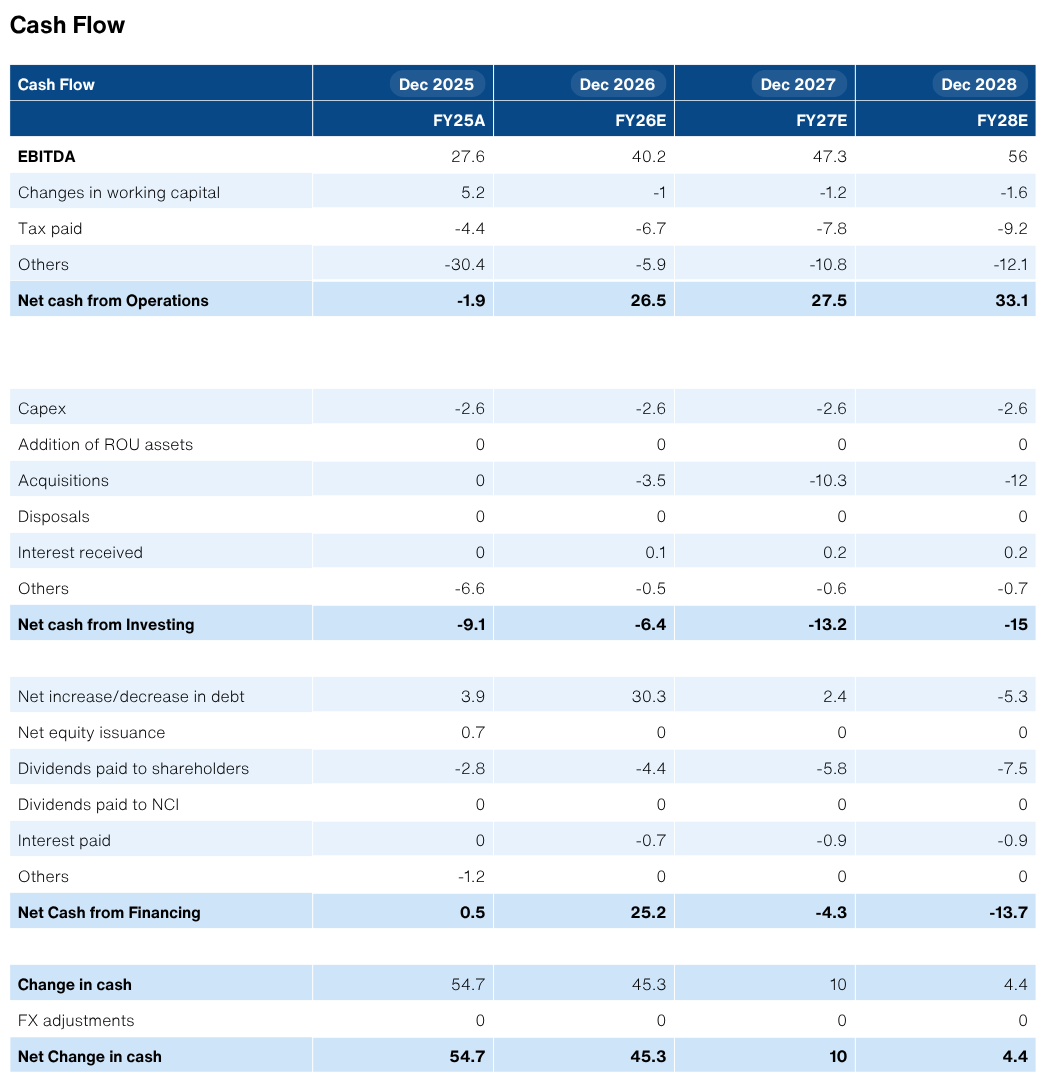

Selected financials

Source: Company Data, NewParadigm Research, March 2026