1Q26 - Seasonal weakness

Orderbook remained stable at RM244.7m

WASCO GREENERGY

GENERGY | 5343.KL

BUY

Target price: RM1.10

Last price: RM0.60

Market cap (RMm): RM298m

Shares out: 500m

52-week range: RM0.59 / RM0.98

3M ADV: RM0.2m

T12M returns: -41%

Disclaimer: By using this information, you acknowledge that you are solely responsible for evaluating the merits and risks of any investment decision and agree not to hold NewParadigm Research liable for any damages arising from such decisions.

Key points

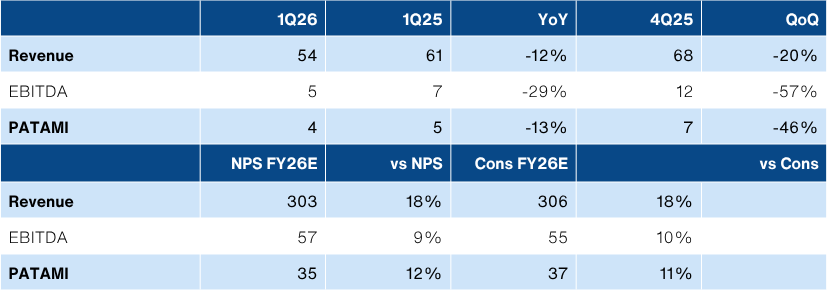

- Earnings fell -13% YoY to RM4.1m, only 11% of ours/consensus expectations. This was a miss.

- Management pinned this on seasonality, dragged down by the festive season in the quarter. But the soft Indonesian outlook did not help.

- Orderbook rose marginally to RM244.7m (+1% QoQ), driven by Malaysian orders.

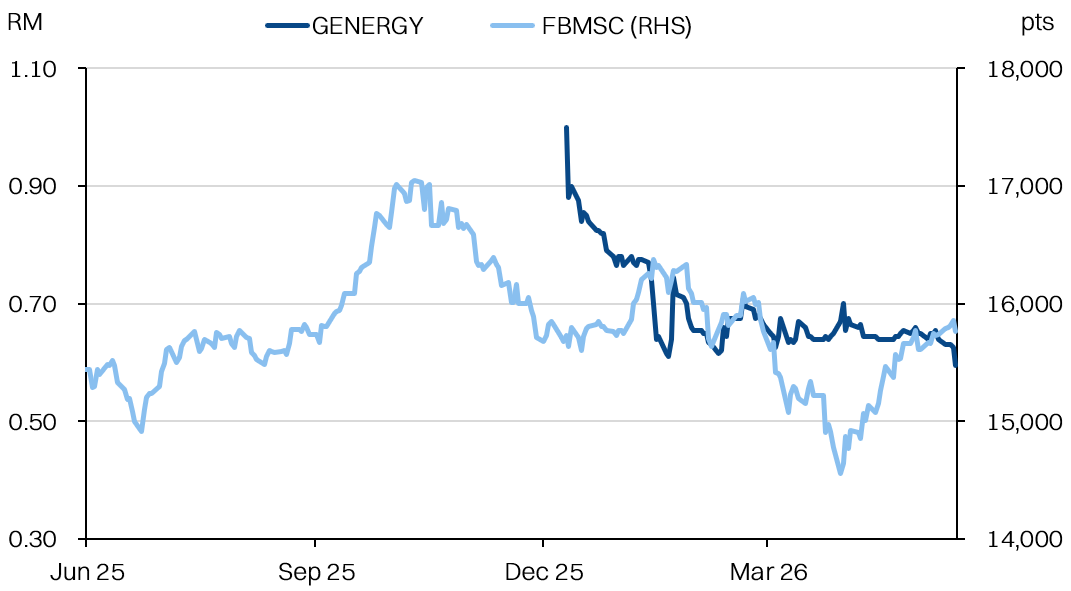

Share price performance

Investment fundamentals

| RMm (end-Dec) | FY25A | FY26E | FY27E | FY28E |

|---|---|---|---|---|

| Revenue | 267 | 303 | 341 | 359 |

| Revenue YoY | -4% | 14% | 13% | 5% |

| Adj PATAMI | 28.6 | 34.7 | 40.1 | 41.5 |

| Adj PATAMI margin | 11% | 11% | 12% | 12% |

| DPS (sen) | 2 | 2.4 | 2.8 | 2.9 |

| ROA | 7% | 8% | 8% | 8% |

| ROE | 11% | 12% | 12% | 11% |

| PER | 10.5 | 8.7 | 7.5 | 7.2 |

| P/BV | 1.1 | 1.0 | 0.9 | 0.8 |

| Yield | 3% | 4% | 5% | 5% |

| Net debt/equity | 16% | 15% | 17% | 18% |

Source: Company data, NPS Research, May 2026

Positive topline guidance, but with risks

- The start to the year was soft, due to the double festive seasons in the quarter which trimmed productivity. While the direction is expected, earnings coming in at only 11% of expectations places it squarely as a miss.

- The one bright spot was the stable orderbook which rose slightly to RM244.7m in the quarter, indicating a book-to-bill ratio of roughly 1x. However, it is worth noting that 1Q26 was an especially slow quarter in terms of orderbook consumption - the slowest over the past 5 quarters. Management indicated that outlook in Indonesia remains soft, as the clients continue to refrain from investment due to the ongoing asset seizure by the Indonesian government. This is further compounded by the US-Iran war that has increased uncertainty.

- Still, management is guiding that revenues in FY26 should exceed FY25, based on the existing orderbook. We have assumed ~13% YoY revenue growth.

- The main risk might not be the topline, but rather from rising raw material costs due to the war. The impact has not yet materialized but could be felt in the second half of the year.

Results snapshot

Gas Malaysia MOU adds BOO funnel

- The coming hike in domestic gas prices appears to be driving more interest for adoption of biomass solutions as an alternative. The MoU with Gas Malaysia opens a new front for GENERGY to source potential clients while also tapping into the former’s balance sheet.

- Still, the prospective brownfield acquisition appears to be moving slowly and we flag newsflow catalysts could be absent in the ST.

- Maintain our earnings and TP of RM1.10.

About the Company

Wasco Greenergy Bhd (GENERGY) is one of the top biomass power equipment EPCC companies in Malaysia and Indonesia. This encompasses boilers that are fabricated in-house and the distribution of Shinko steam turbines. GENERGY differentiates itself from its direct competitor, BM Greentech, by providing engineering for customized solutions. It will further differentiate itself by venturing into asset ownership of biomass-to-steam systems for industrial customers.

About the Stock

GENERGY is listing on the main board of Bursa Malaysia and will be a Shariah compliant stock. It is a renewable energy spin-off from its listed O&G-focused parent, Wasco Bhd, which retains a 62.5% stake. GENERGY is a professionally-managed company with a majority independent board.

Investment Thesis

GENERGY is an early-stage opportunity to invest in a high-growth renewable niche of biomass-for-steam power. Not just as an EPCC, but as an asset owner. Between the abundant and under-utilized biomass supply and the estimated 30% cost savings compared with natural gas-powered steam, which we estimate to be an RM2-3bn market. Thematically, GENERGY will be a strong ESG play as it helps customers decarbonize while decoupling from global energy commodity prices.

Key Risks:

- Execution risk: By far the biggest hurdle will be securing the first greenfield biomass-to-steam contract and subsequently delivering on the expected payback period of 5 years. GENERGY has no track record with asset-ownership.

- Competition: GENERGY has sizable EPCC competitors in the space. While some lack direct engineering capability, they have the resources and balance sheet to close the gap and compete for the same assets.

- Feedstock: The business model counts on biomass remaining at least cheaper than conventional fuels. Competing use for biomass that threatens feedstock prices would upend the business model.