A two-week ceasefire

Malaysia Strategy

Disclaimer: By using this information, you acknowledge that you are solely responsible for evaluating the merits and risks of any investment decision and agree not to hold NewParadigm Research liable for any damages arising from such decisions.

Key Takeaways

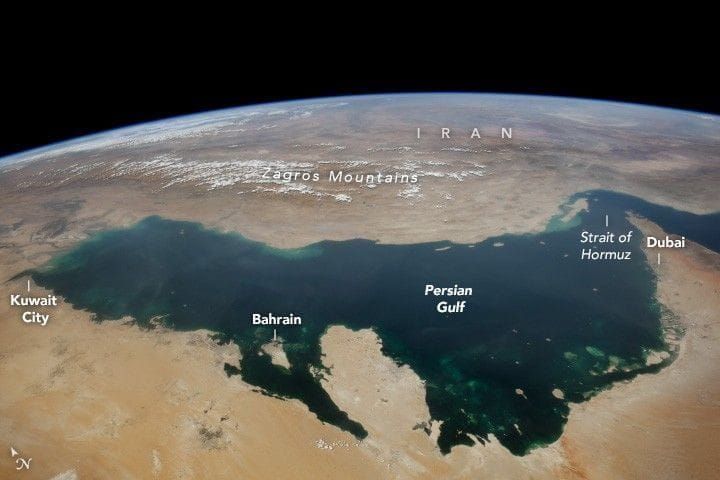

- US and Iran have declared a 2-week ceasefire and reopening of the Strait of Hormuz.

- Deescalation bias is encouraging, but maximalist demands from both sides, especially around enrichment makes negotiations challenging.

- Trade the relief, but mind the 2-week check. Risk of aggression in the ST remains, especially with Israel.

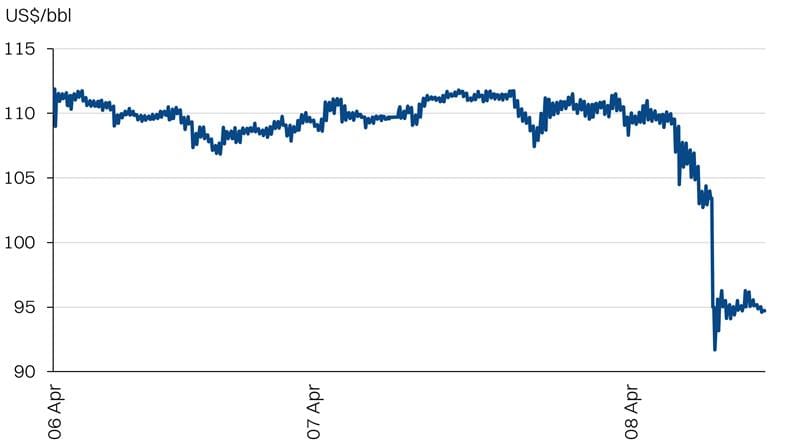

Crude oil prices | Large cap performance | Sectoral performance

Source: Bloomberg, NewParadigm Research, April 2026

Relief immediate, but repairs take time

- We recommend trading into the relief rally as the market digests the positive newsflow of a ceasefire and reopening of the Strait of Hormuz. This should provide some immediate reprieve to tight oil and gas supplies, especially to Asia, as laden tankers make their way out.

- However, we flag two considerations. Firstly, some of the damage from the conflict will take months to resolve and in some instances, years. Secondly, risk of reescalation remains.

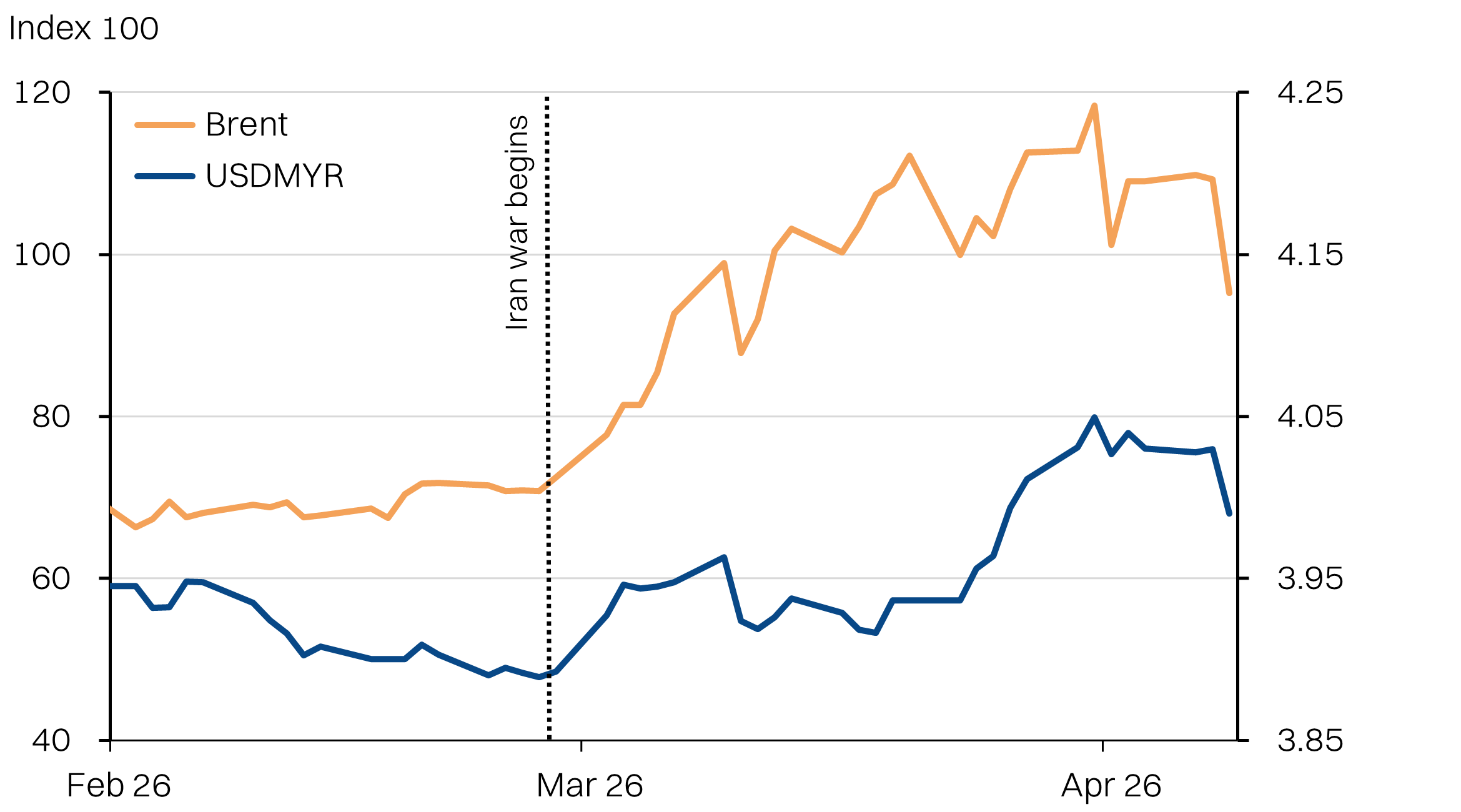

- We anticipate Brent will trade above US$70-80/bbl till end of the year. This is because resumption of oil production will take some time. Production shut-ins have already taken place and the temporary nature of the current ceasefire makes it difficult for producers to commit resources to restarting production. Data from Rystad Energy shows approximately 44% of Middle East production is currently offline, or about 10.8Mbpd. Roughly 30% of the shut-in capacity can be restarted in 1-2 weeks, while 50% will need 3-5 weeks. The balance will take 2-3 months, estimates Rystad Energy.

- Additionally, there is the physical damage to production infrastructure. The two damaged trains of QatarEnergy’s LNG facilities will take 3-5 years to repair. As we have written, this places a more sticky risk on companies like MISC (link).

- While the trajectory is encouraging, it is tough to rule out reescalation. Israel has already stated that the ceasefire does not include Lebanon as it continues its offensive against Hezbollah. The 2-week deadline could be extended if negotiations are constructive. However, at this stage, the maximalist demands from both parties place significant burden on a deal - especially on the matter of Iran’s enrichment plans.

Reversion to pre-war levels, partially

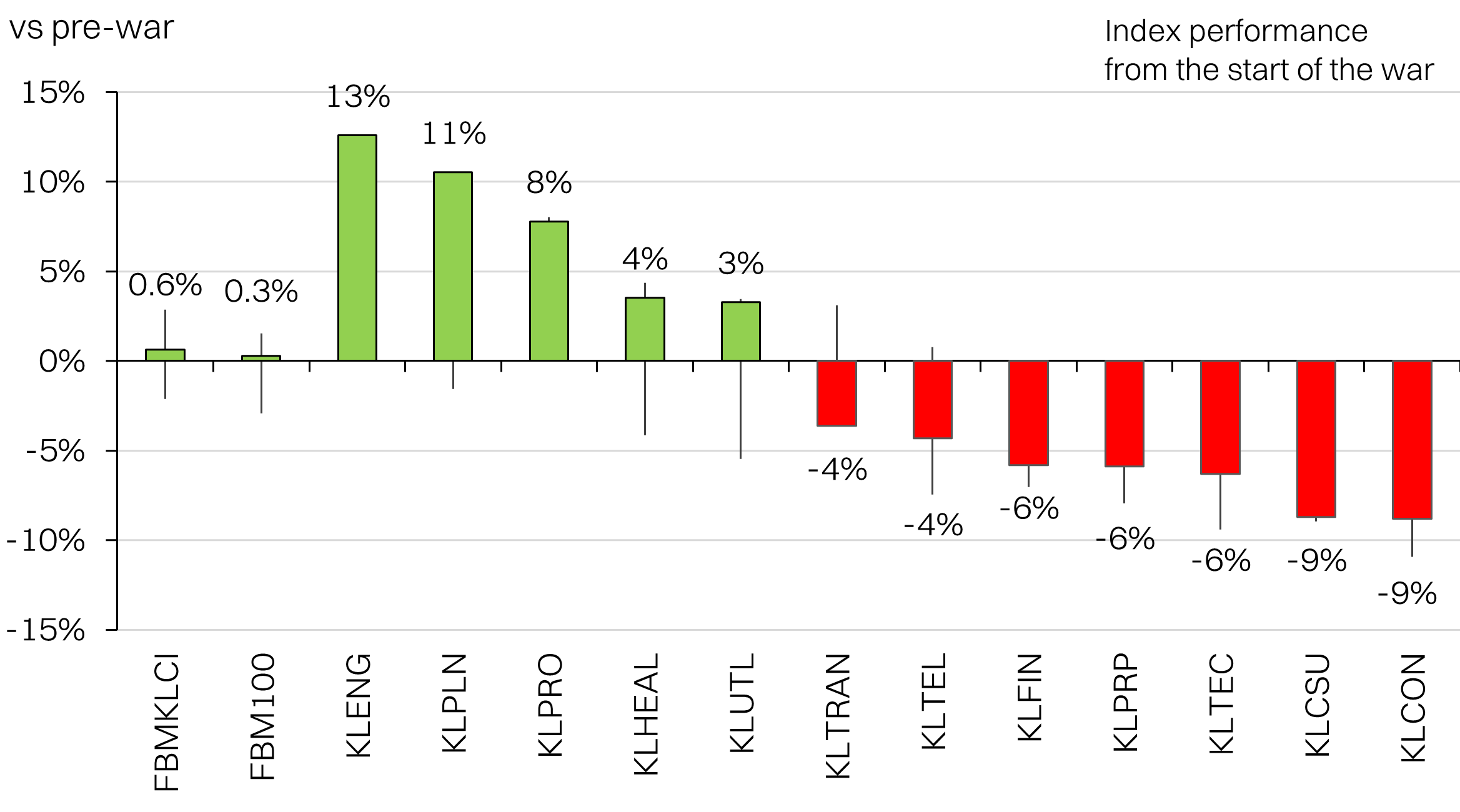

- We anticipate ST normalization towards pre-war prices and valuations. Even if fundamentals might be supportive (earnings drivers intact despite ceasefire), we anticipate the initial sentiment adjustment will dominate.

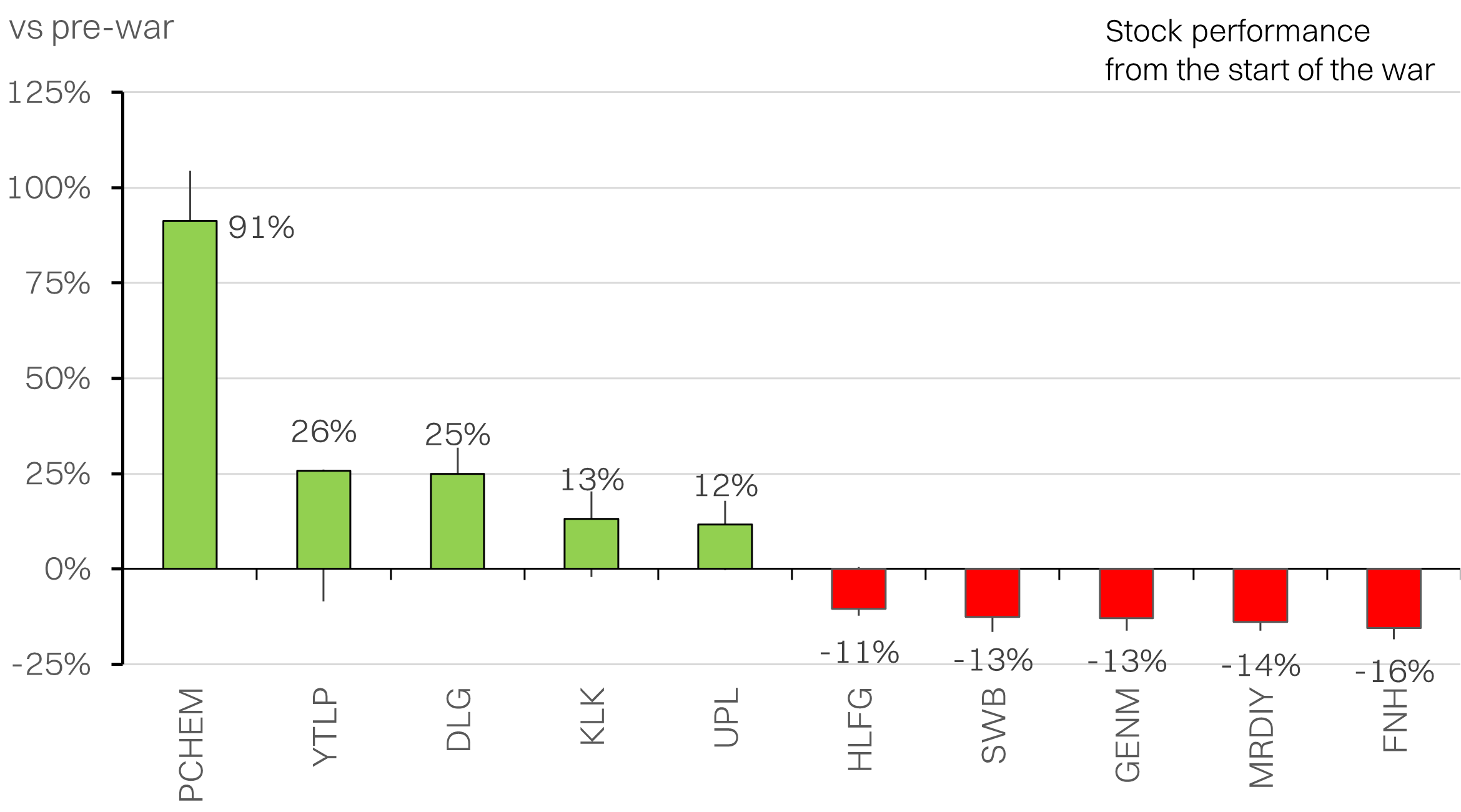

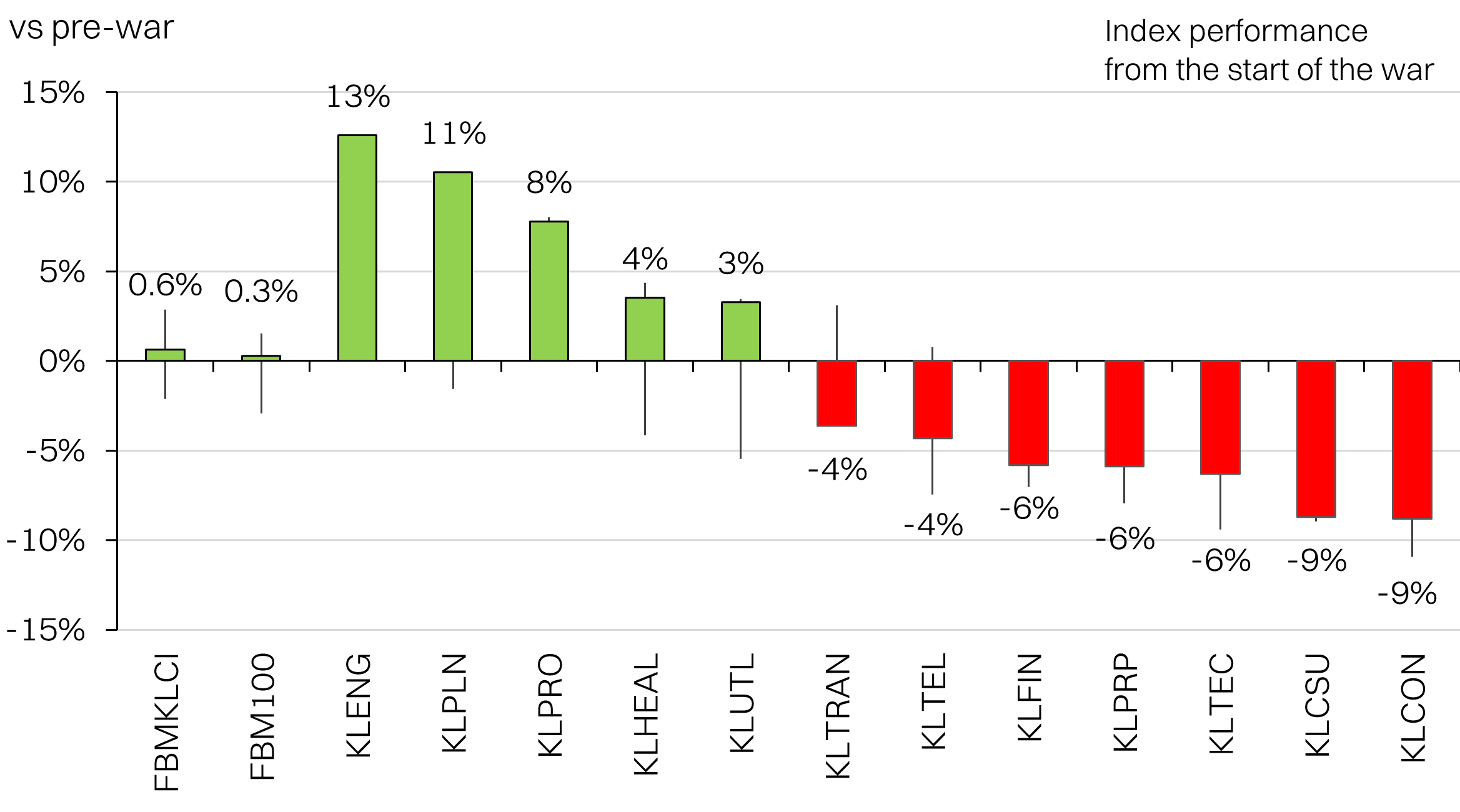

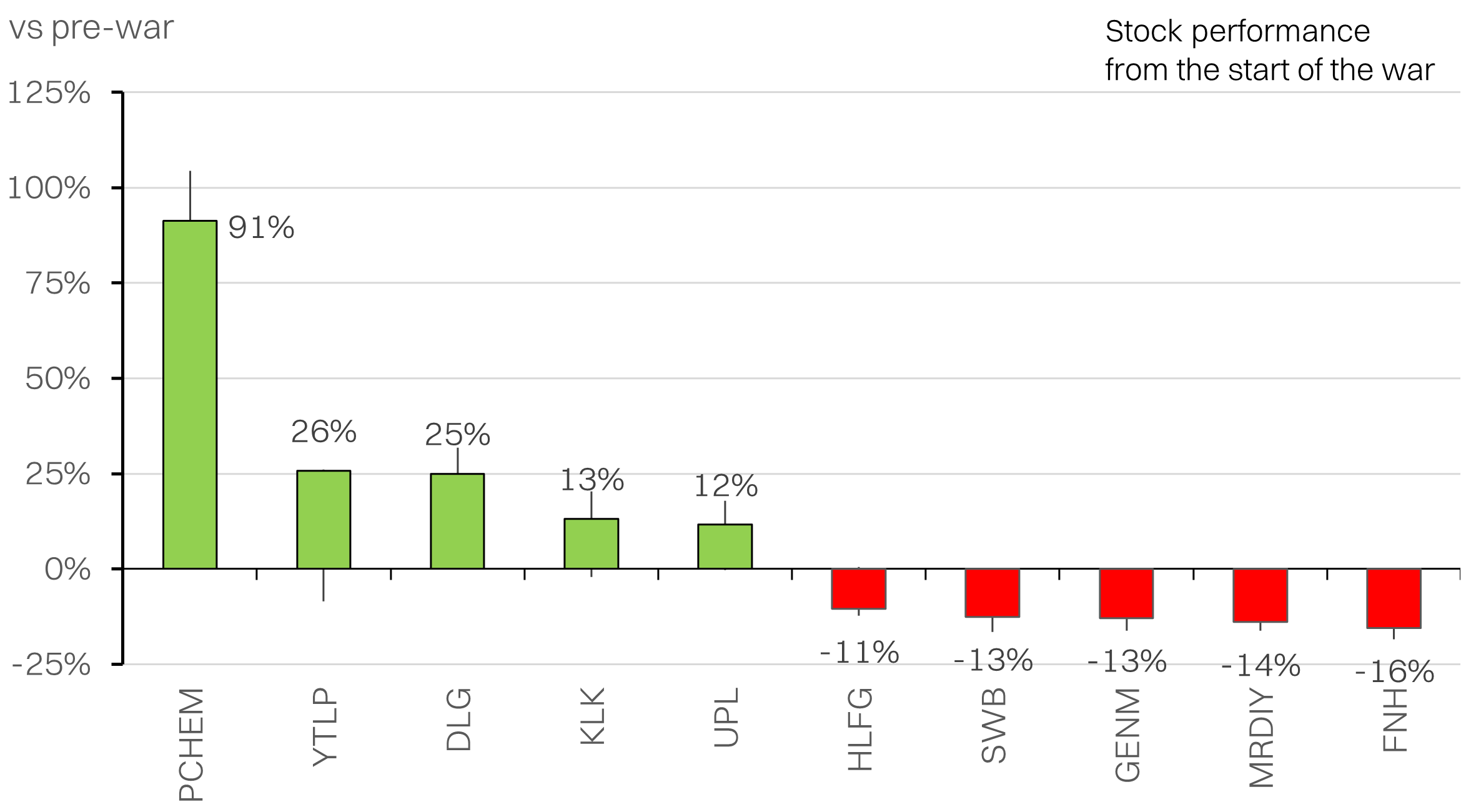

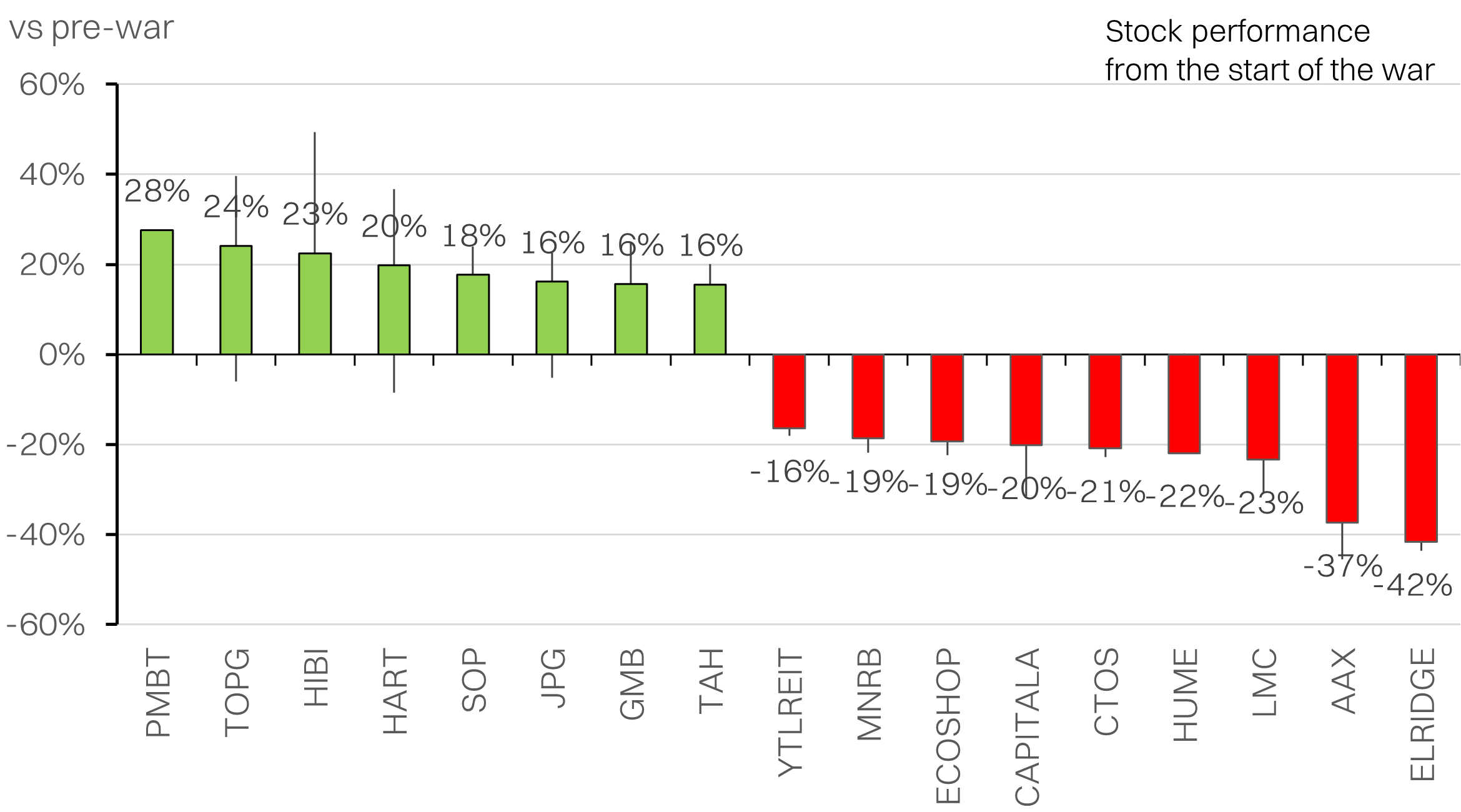

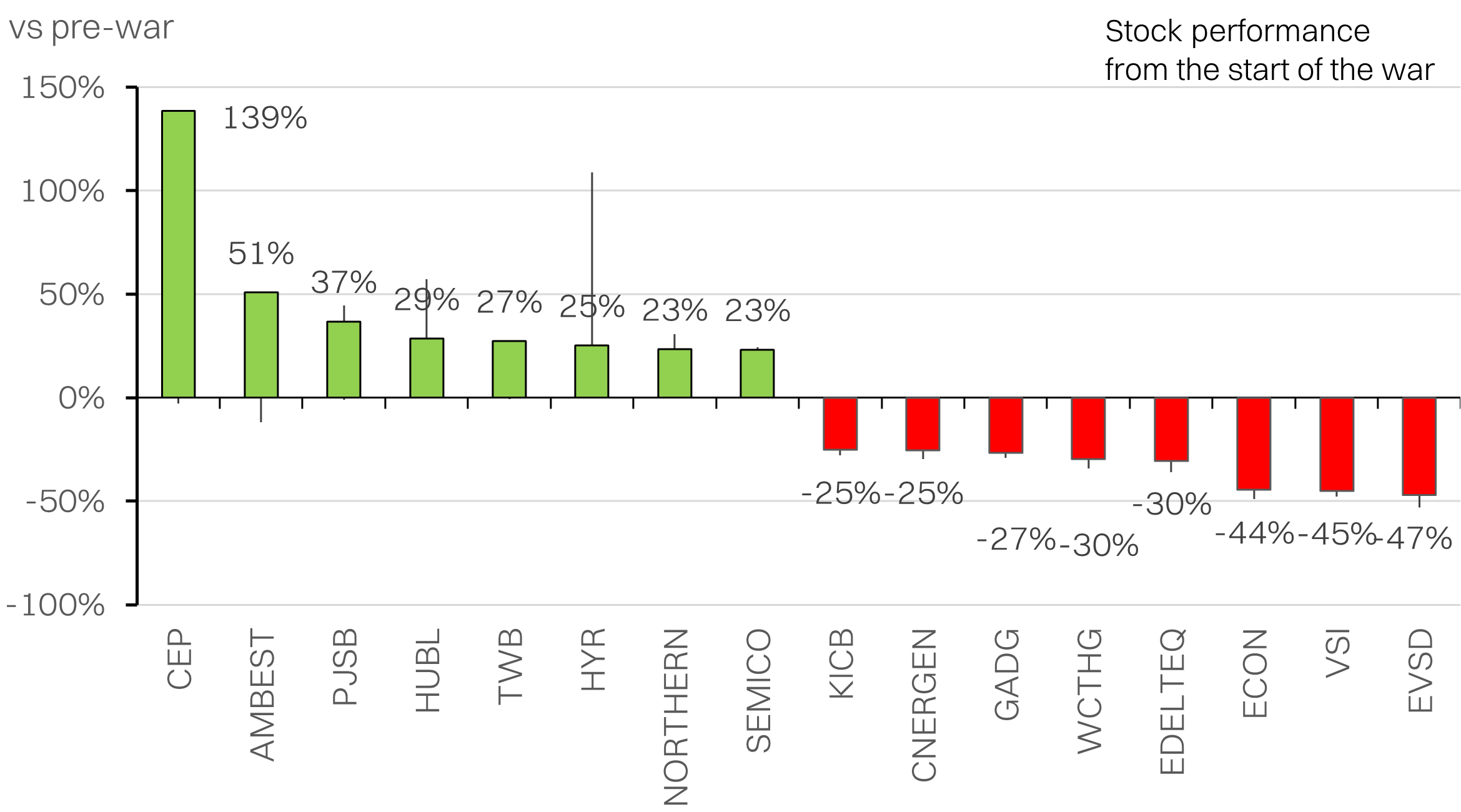

- Outlier sectors have been energy (+13%), plantations (+11%) as well as construction (-9%). Among large caps, PCHEM stands out the most (+91%), on the fertilizer price surge. Notable losers include AAX (-37%) on higher jet fuel prices.

- We recommend trading into the relief rally and trimming stocks that are war beneficiaries, given deescalation bias.

Nuclear impasse

We have organized the key demands from the US and Iran from most to least maximalist. The biggest hurdle, relatively, appears to be the structural impasse on uranium enrichment. Either side will find it highly challenging to reverse its publically stated position. Comparatively, the other demands have more wiggle room to negotiate. Another key stumbling block in the negotiations is Israel, which has its own maximalist agenda and has demonstrated much less willingness to engage with Iran.

Charting the war’s impact on the market

- We compiled some charts to show the gainers/losers from the war, across the key benchmark sectoral indices as well as stocks (large cap, mid cap, small cap).

- We anticipate some pull back towards pre-war levels on the ceasefire news, with the biggest outliers likely to see the biggest corrections.

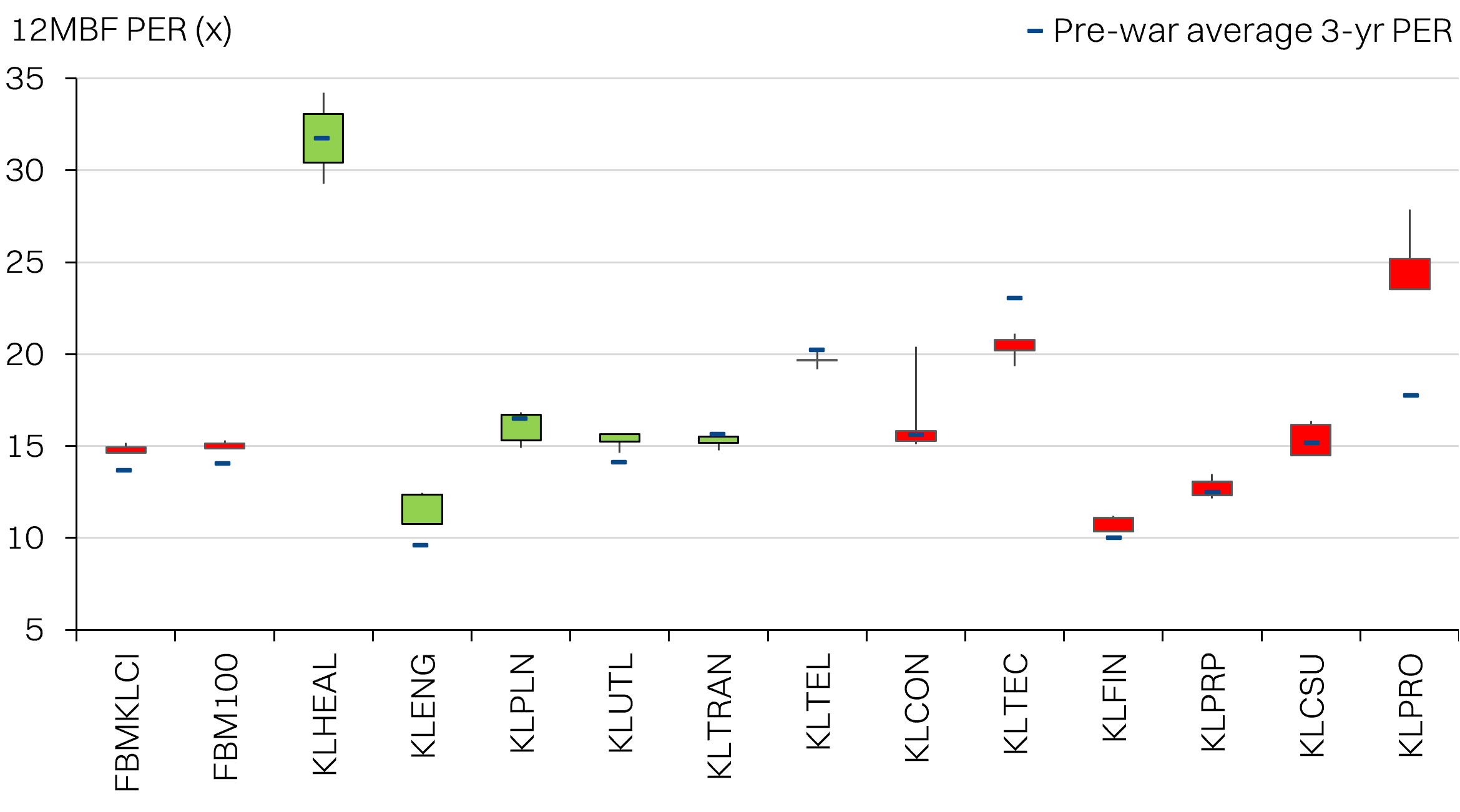

Sectoral index performance from start of the war / Sectoral valuation changes from start of the war

Source: Bloomberg, NewParadigm Research, April 2026

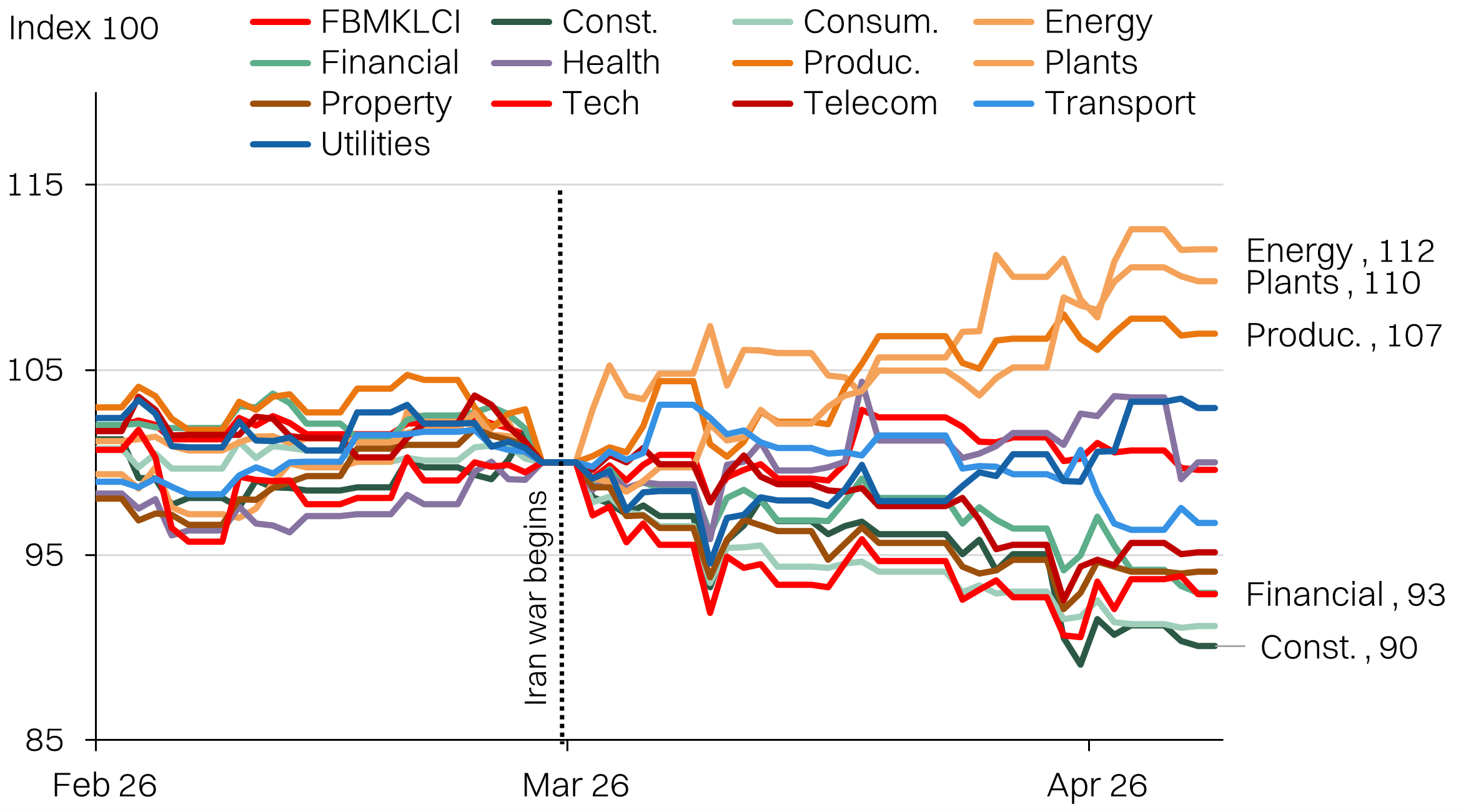

Key indices performance from start of the war / Oil prices and the ringgit

Source: Bloomberg, NewParadigm Research, April 2026

Large cap (>RM10bn) top gainers/losers from the war / Mid cap (<10bn, >RM1bn) top gainers/losers from the war / Small cap (<1bn, >RM0.1bn) top gainers/losers from the war

Source: Bloomberg, NewParadigm Research, April 2026