Another 20 stocks won't fix the KLCI

FTSE Russell is proposing to enlarge the FBM KLCI to 50 stocks from the current 30.

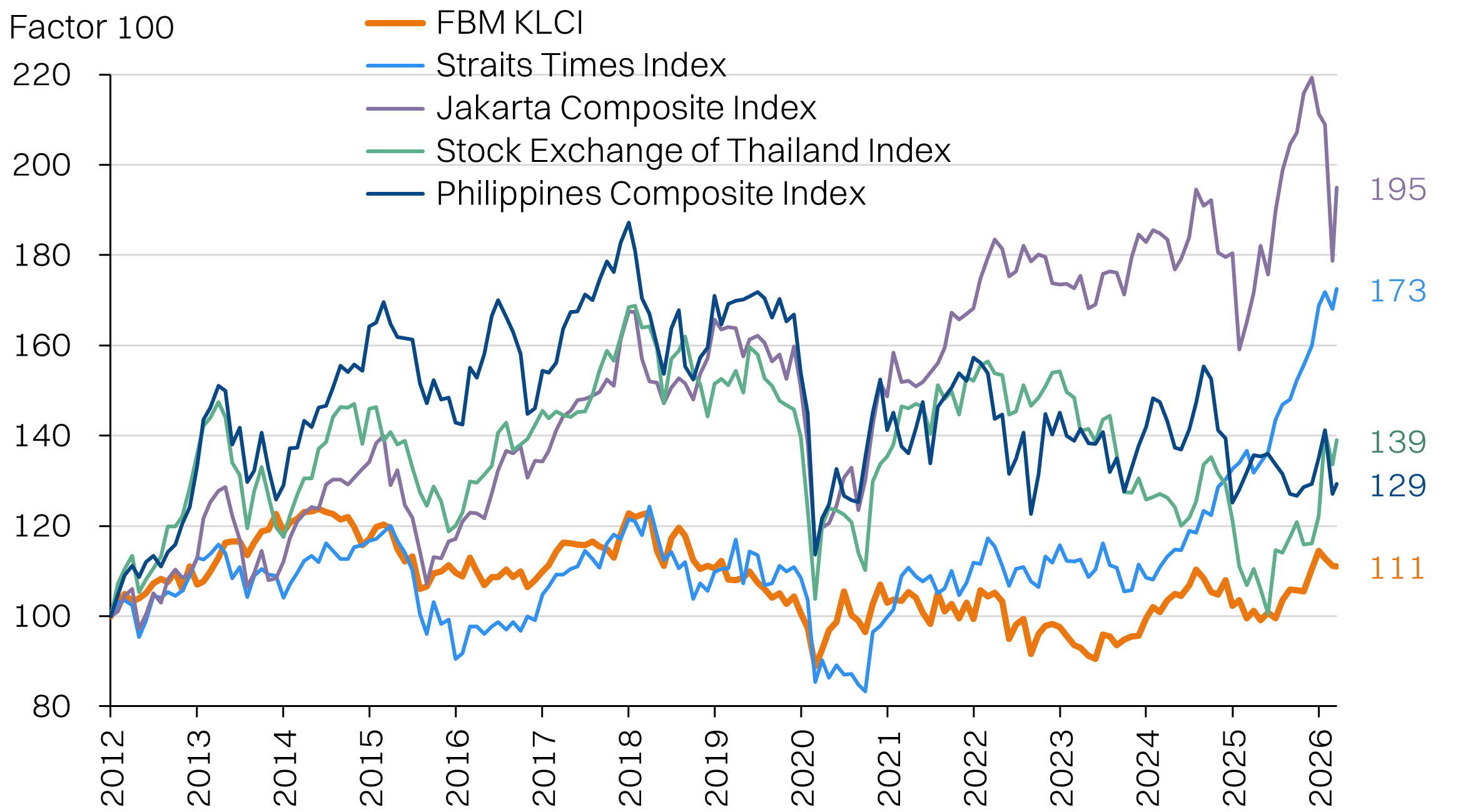

The 30-stock FBM KLCI index may be the bellwether for the Malaysian stock market, but one has to admit, it can be a little uninspiring. Post-GFC, the KLCI has underperformed Asean peers, only growing by 11%, closing at 1,690 points this week.

At the same time, the Malaysian economy more than doubled in the same period (nominal Ringgit terms), growing at 5.6% CAGR. It isn't news that the stock market is a poor representation of the broader economy, nor is it unique to Malaysia. But the divergence of the benchmark index is becoming tougher to ignore.

There are many causes for this issue, but the incoming proposed prescription is to expand the KLCI by another 20 stocks to 50.

Regional benchmark indices - KLCI lags

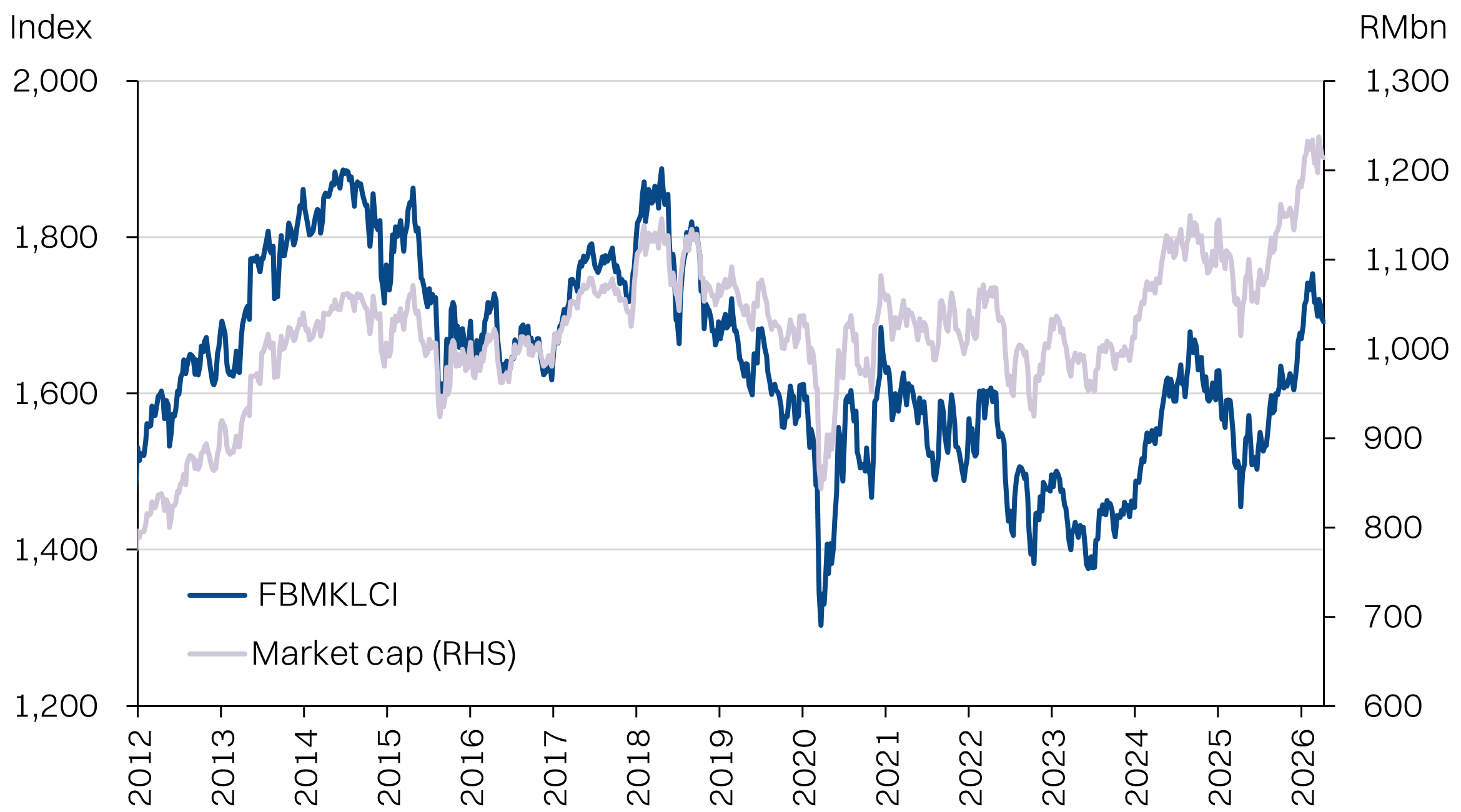

Market cap paints better picture

Disclaimer: By using this information, you acknowledge that you are solely responsible for evaluating the merits and risks of any investment decision and agree not to hold NewParadigm Research liable for any damages arising from such decisions.

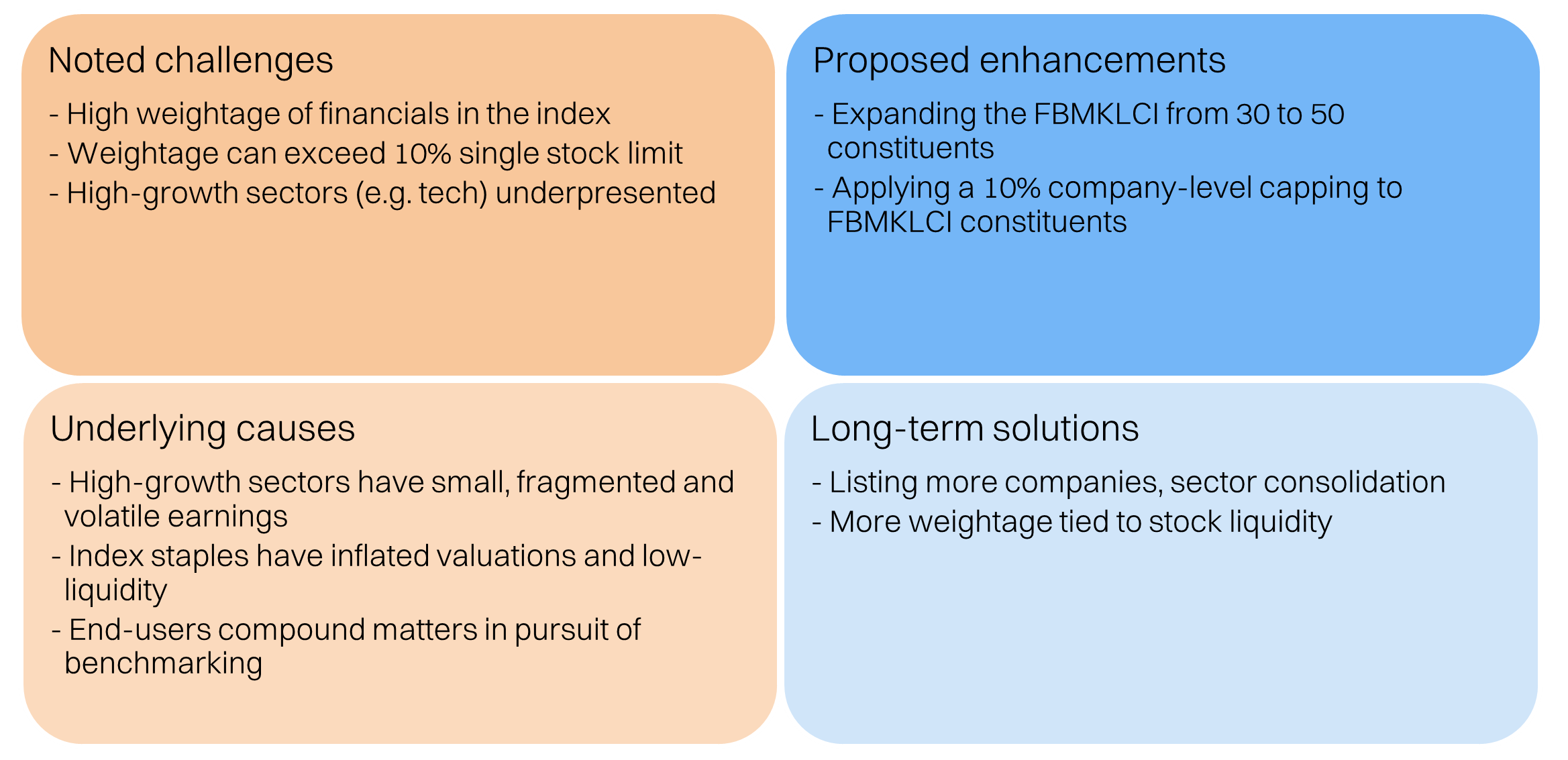

The proposed enhancements:

- Expanding the FBM KLCI from 30 to 50 constituents.

- Applying a 10% company-level capping to FBM KLCI constituents.

- Reducing the FBM70 from 70 to 50 constituents.

Quick side-track: The FBM KLCI as well as a number of other key indices are jointly managed by FTSE Russell and Bursa Malaysia; key resources available here.

Good intentions, wrong medicine

It is worth understanding what the expansion of the index is trying to achieve and we recommend diving into the full consultation linked above. Our brief summary:

- Reduce the weightage of a few of the largest stocks

- Reduce the overall weightage of financials to the index/ improve representation of the broader market

- Improve liquidity depth of the index

These are good objectives.

Currently, there are four stocks with weightage above 10%: Maybank (13.4%), Public Bank (10.8%), Tenaga (10.2%) and CIMB (10%). With most funds capped by a 10% exposure limit (vs NAV), the high weightage means most funds are perpetually unable to overweight these stocks.

The high weightage of financials to the index is not in itself a problem, but it means other sectors of the economy tend to be under-represented. The index is skewed to old economy stocks with mature growth profiles and fails to capture new economy and high-growth sectors.

That said, some of the underlying causes for these problems are not being addressed. And to be fair, it falls outside the purview of the index managers.

Challenges vs solutions matrix

Too small, volatile and pricey

Let's look at the data.

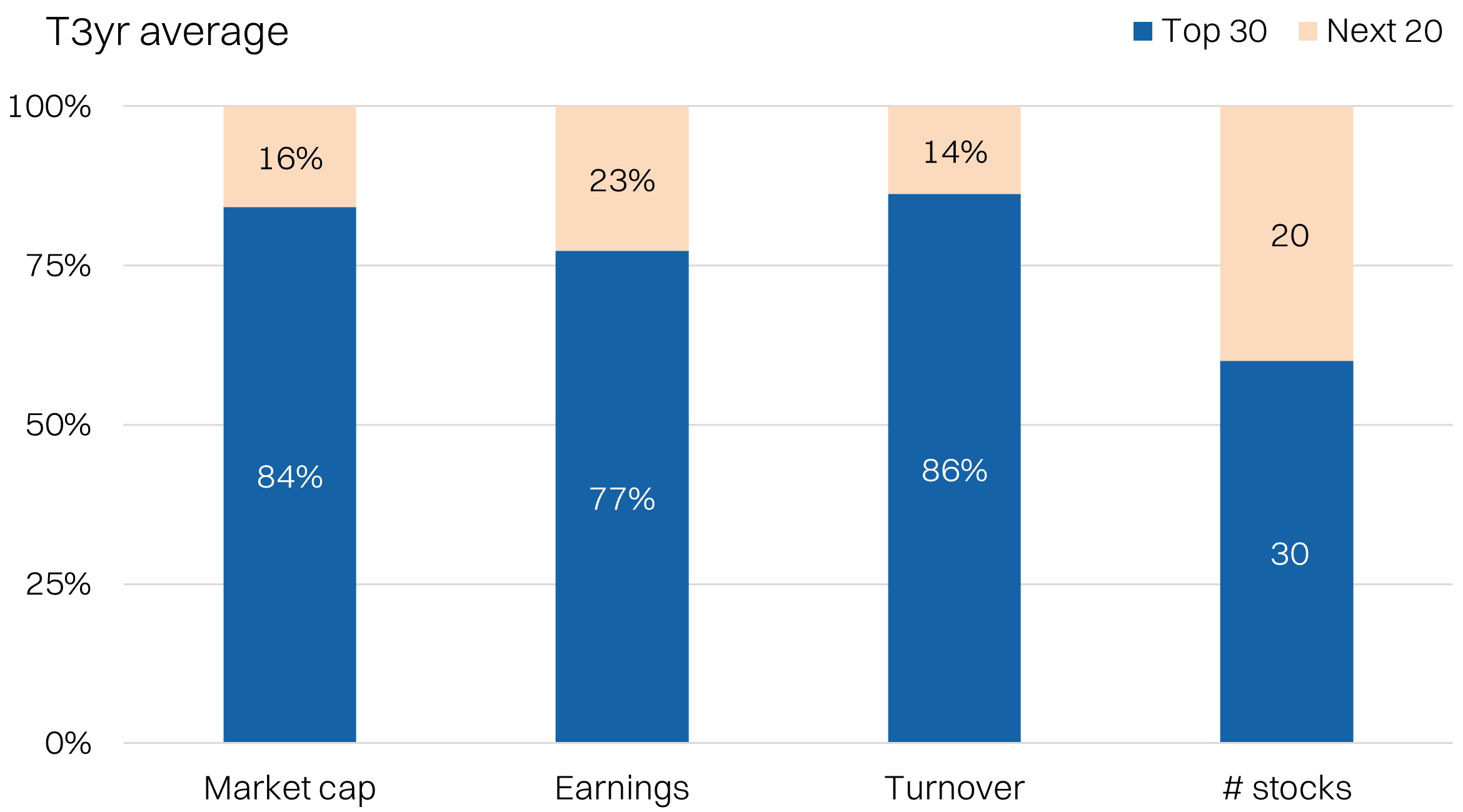

The first issue is that the sheer size of the top-30 stocks makes the inclusion of another 20 stocks relatively negligible.

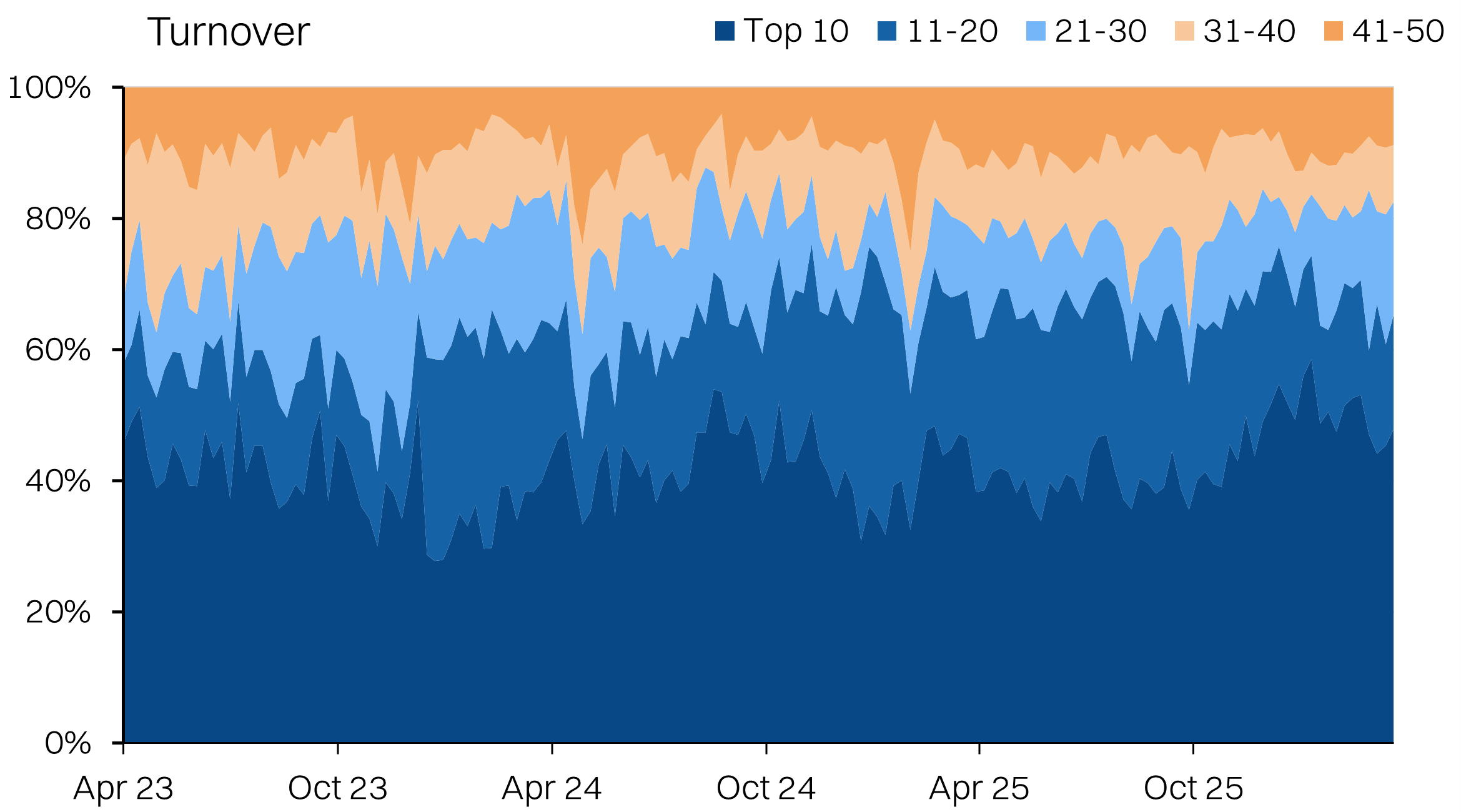

The additional 20 stocks would make up 40% of the enlarged index. But based on the trailing 3yr average, the "next 20" stocks would only make up 16% of the enlarged market cap and ~14% of earnings. The share of market turnover would be slightly better at 23%.

Keep in mind, this is on aggregate. Individually, these stocks would struggle to move the index. Currently, 30th stock in the index has a weightage of >0.7%. this comes back to the sheer discrepancy in size, with the average market cap of the top-30 stocks hovering around RM37bn while the "next 20" stocks average RM10bn.

As for the turnover, there tends to be large swing in the turnover for smaller stocks. Our simplified back test shows it can range from 14%-60% of the enlarged index.

The "next 20" stocks are proportionally small.

Stocks grouped by market capitalisation

Source: Bloomberg, NewParadigm Research, April 2026

More churn

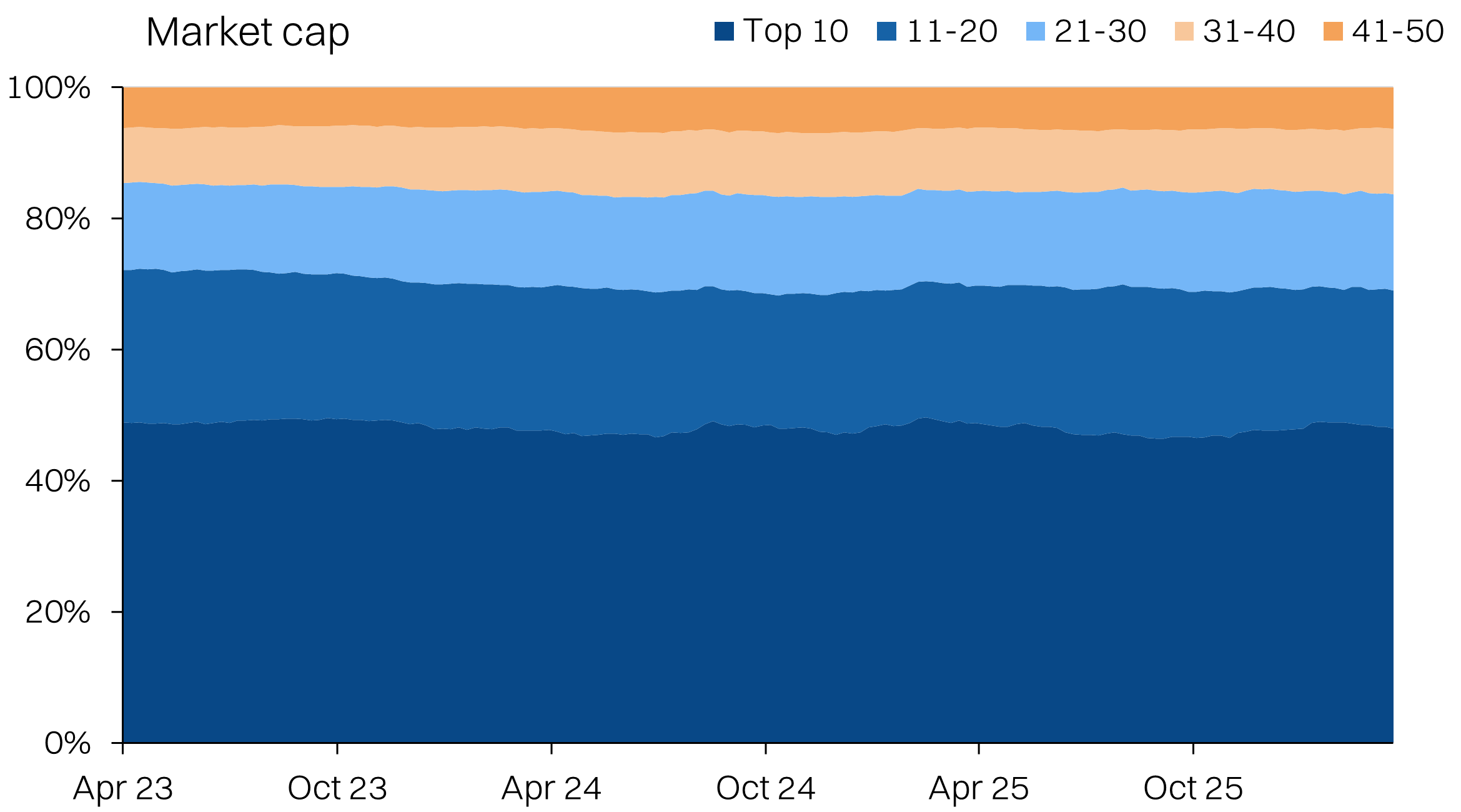

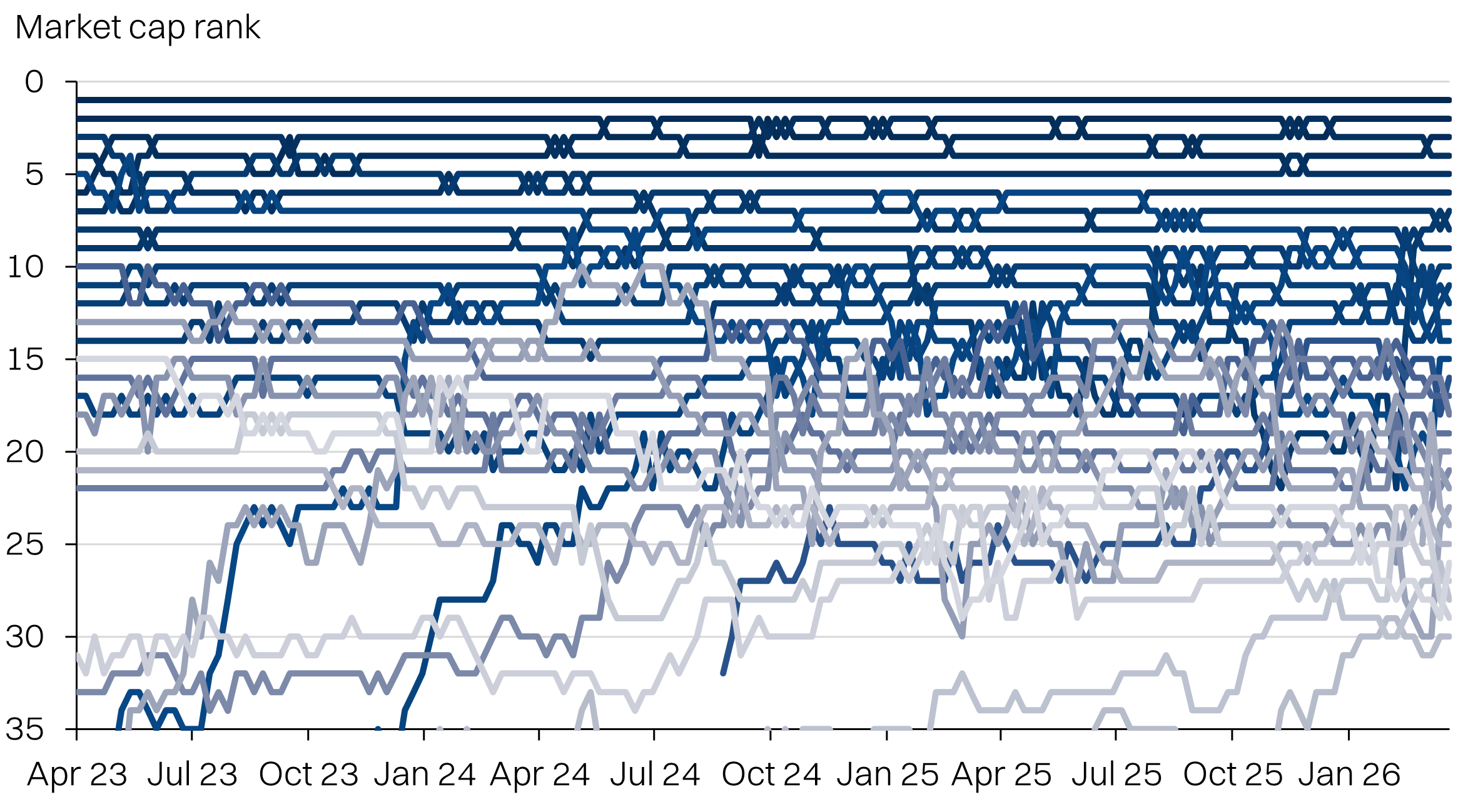

The next issue is churn. Back testing for the past three years (weekly close), there have been 40 names in total that have at some point qualified as one of the top 30 stocks. Yes, the index inclusion criteria is a little more rigorous. Which is why the average addition/removal from the index has been 1-2 stocks only during the biannual review period.

Below, we can see that the top-30 stocks tend to be fairly stable over the past 3-years, with most of the churn limited to #25 and below.

Top 30 stocks - historical market cap ranking

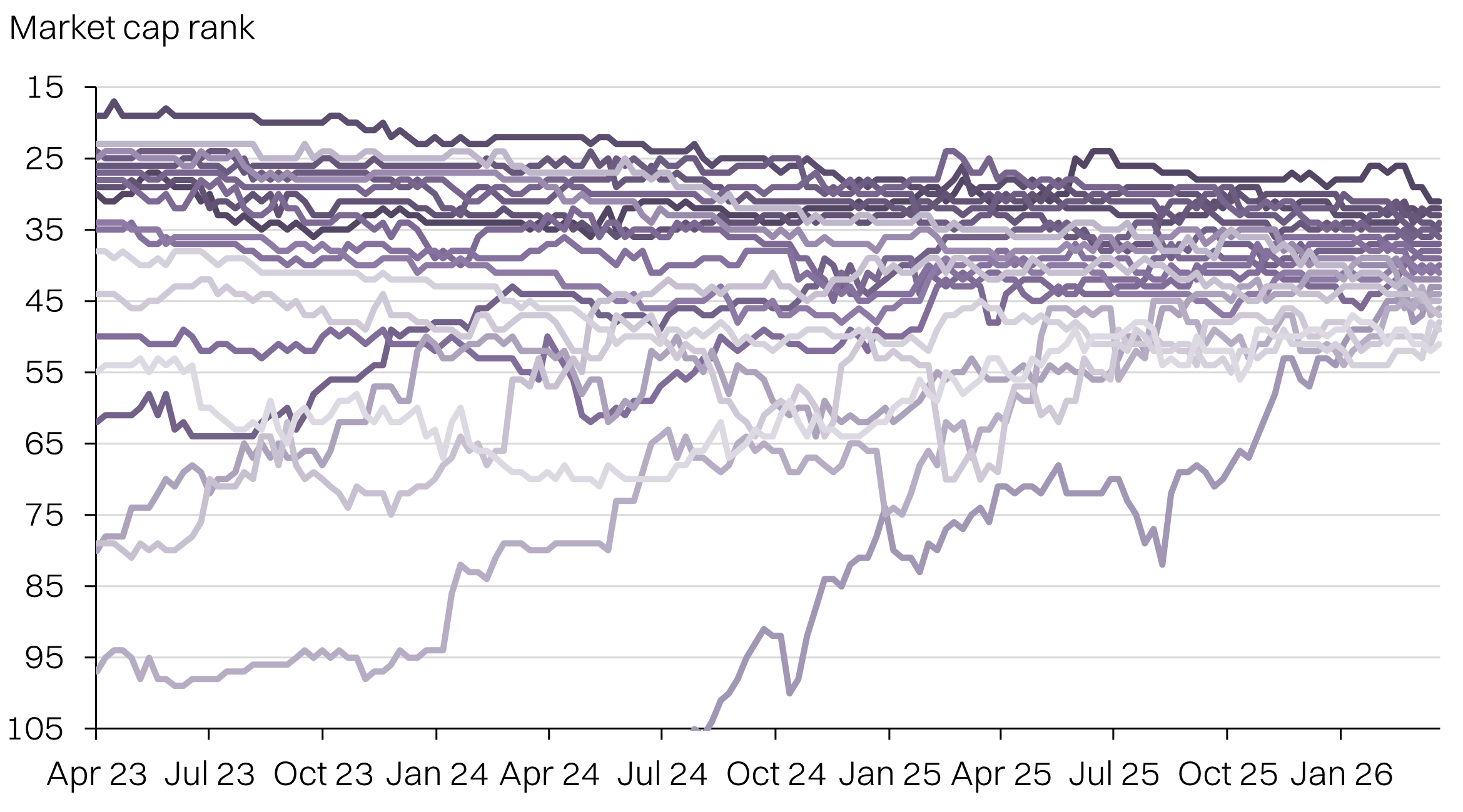

But when we look at the "next 20 stocks", the potential for churn is huge. Over the past 3 years, over 47 stocks have cycled through this bucket at some point. The same screen run against just the current "next-20" stocks, shows a massive dispersion of performance. For context, the FBM100 regularly sees 6-8 inclusions/exclusions.

Criteria could be tightened to minimize churn. However, it would still increase the relative churn for the KLCI and require more resources for funds to monitor and comply.

"Next 20" stocks - historical market cap ranking

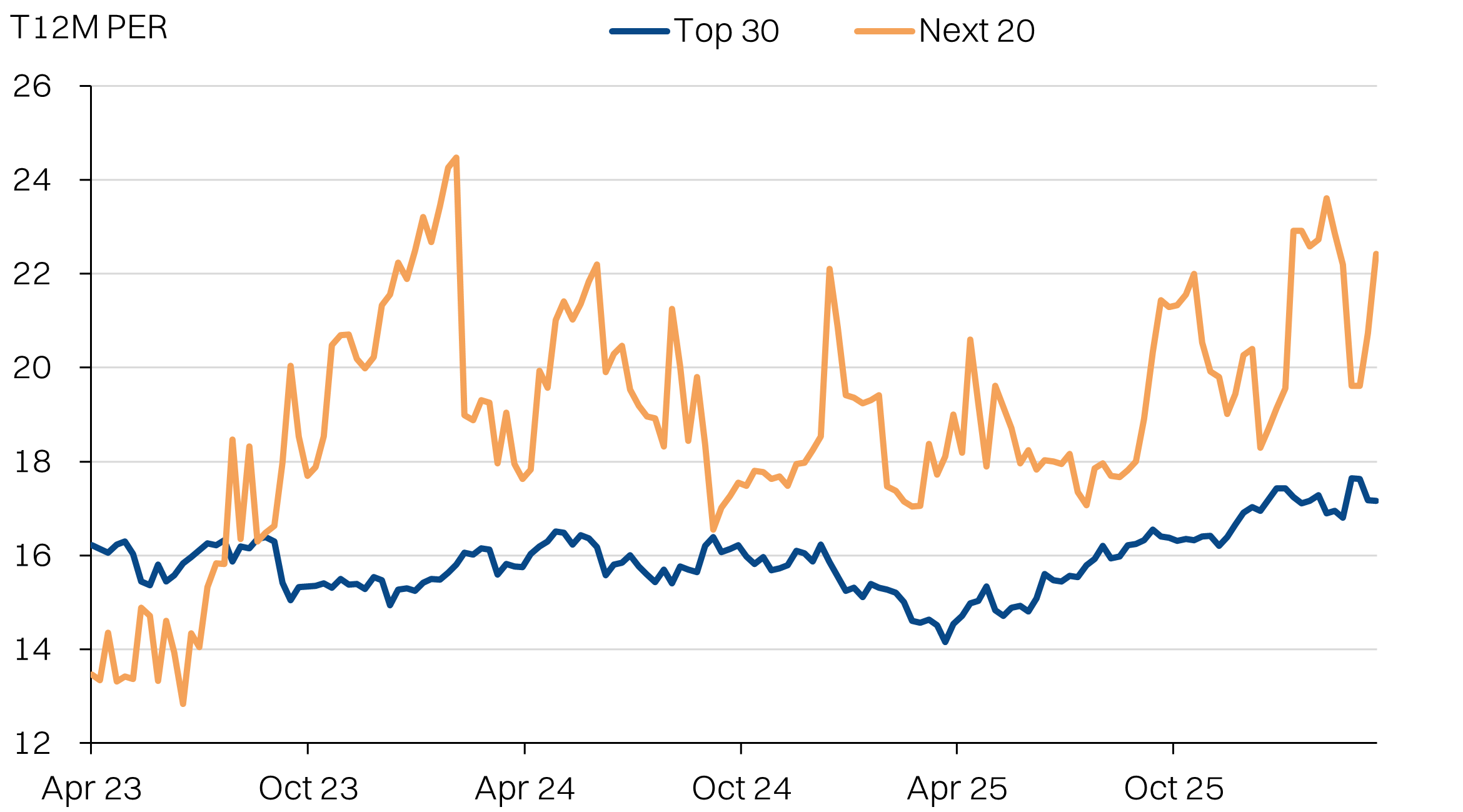

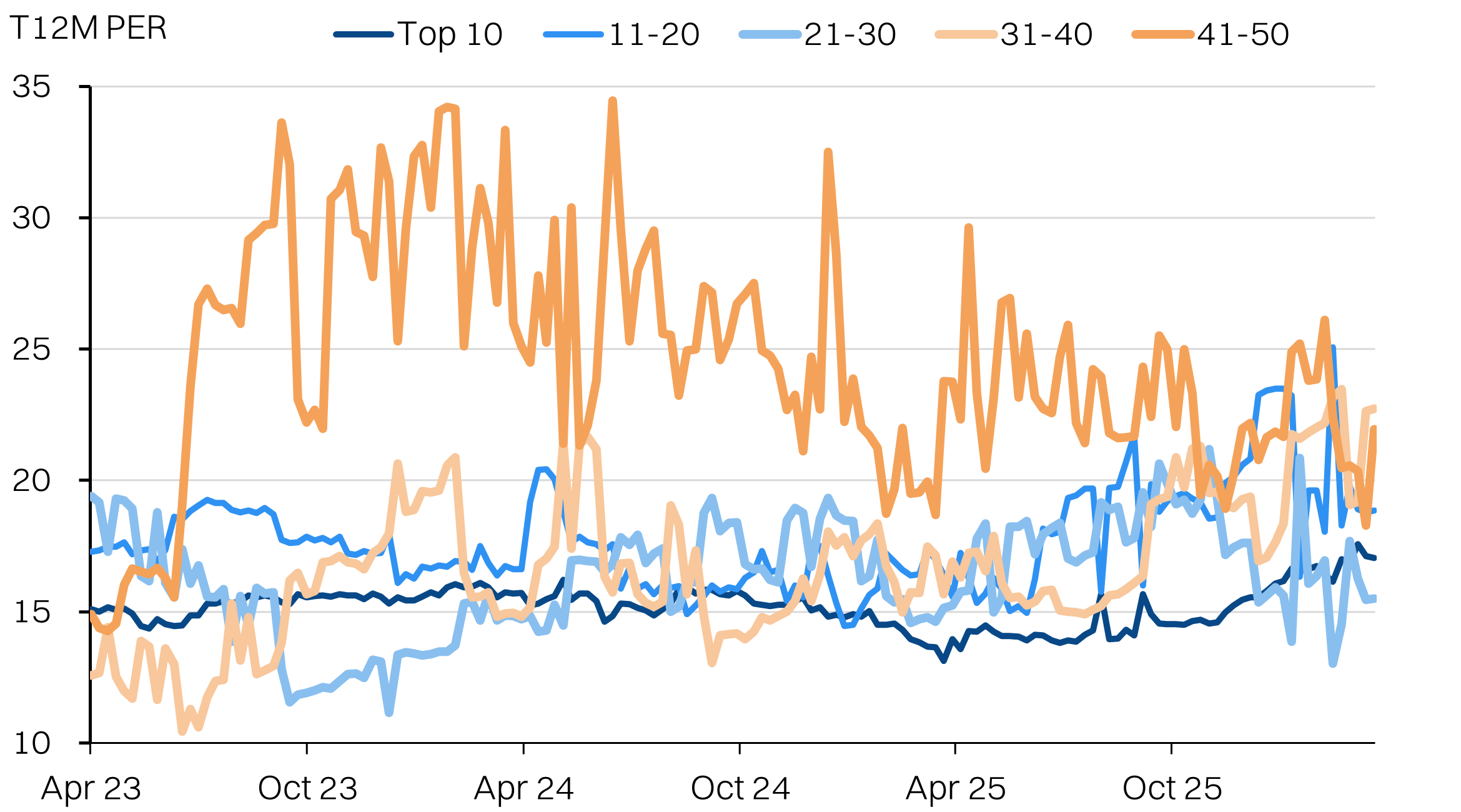

The "next 20" stocks also tend to have higher valuations than their top-30 counterparts. One reason for this, is that the former tends to have higher growth and attract higher multiples.

Stocks in the "next 20" bucket currently have a PER of 23x compared with the top-30's ~17x. However, this varies substantially when looking back, due to the high variability of stocks that cycle through the "next-20" group.

Average valuations by market cap grouping

Admittedly, the stability of the top-30's valuations comes from the top-10 stocks, which are very stable. However, even when splitting out the breakdown into 10-stock groupings, the higher multiples and increased variability of valuations for smaller cap stocks becomes very apparent.

This is due to a combination of lower earnings quality (more variable) as well as more cyclical earnings drivers for smaller stocks.

To be clear, there are some quality names on the cusp of index inclusion. Some are even former constituents that have fallen out and are now on the reserve list. This would include QL Resources, Westports, Dialog, and KPJ to name a few.

Average valuations by market cap grouping

What about breadth?

The most glaring omission from the FBM KLCI is the lack of tech/semiconductor names. With Malaysia making up ~8% of global semiconductor backend capacity, it is a substantial portion of the economy that is completely unrepresented. Sadly, only one name potentially makes the cut for an expanded KLCI - ViTrox at ~RM9bn market cap. The rest of the "next 20" list (currently) is primarily property developers, consumer, and construction - not exactly new economy names anyway.

This brings us back to addressing the root cause of the KLCI's lack of spark. Take the lack of big cap semiconductor names, for example. Despite the sector's relevance to the economy, the fact is a substantial portion of semiconductor revenues accrue to local arms of foreign multinationals that have no interest for a domestic listing. The rest of the locally-owned companies are somewhat fragmented and are still relatively small.

Inari at its historic peak did manage to break into the KLCI and stuck around for 1.5 years. But Inari needed cyclically peak earnings (RM390m) as well as record high multiples (32-38x, forward PER) to claim a spot. Once earnings normalized, Inari quickly fell out of the index.

The market might simply have to wait on the semicon sector to compound growth till the earnings base is large enough to justify inclusion into the index. In fact, we covered it in this Frontken report.

Closing the feedback loop

The final piece of the puzzle are the end-users of the index, fund managers. From passive funds and ETFs to insurance funds that benchmark to the KLCI, a large proportion of AUM actively tracks changes in the index and adjust portfolio positions accordingly.

In turn, this creates a feedback loop. Especially with low-liquidity and/or low-free float stocks, where some funds are compelled to bid-up valuations in order to secure sufficient weightage for the portfolio. This has been further compounded by the institutionalisation of funds over the years. Actively managed funds with more flexible mandates can skirt this problem, but alas, it cannot be completely ignored.

The KLCI's users matter too

Capping weightage for a start

We foresee the upsides from expanding the index will be relatively limited. Largely due to the sheer size of the existing big caps that make additions somewhat irrelevant. But also, because underlying problems with the index' underperformance cannot be addressed this way.

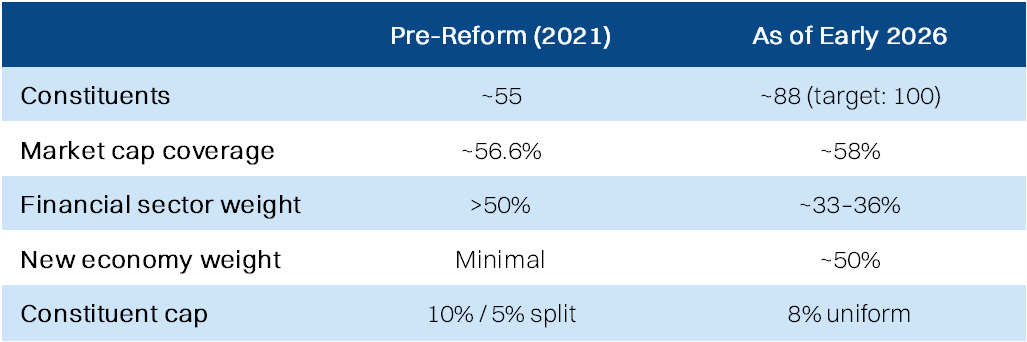

It is worth studying the move to expand Hong Kong's Hang Seng Index (HSI) that began with consultations in 2020. The HSI is a little different from the KLCI. It began in 1969 with 33 constituents but gradually grew to 55 over the years via ad hoc additions. The plan was to expand the index to 80 stocks by mid-2022, and subsequently to 100 stocks. Similar to the KLCI, the criticism of the HSI was the higher weightage of financials (>50% at the time) and other old economy sectors like property developers.

The index did manage to expand to 88 stocks, but the inclusion of new economy weightage stocks in the index proved unfortunate timing. Beijing's sweeping regulatory crackdowns that began in 2021 hurt key stocks like Alibaba, Meituan and Tencent. Ironically, the inclusion of new economy stocks that were supposed to revitalize the index turned into a drag.

Today, it appears the aspirational target of 100 stocks has been quietly shelved. At least one of the main objectives - lowering the weightage of financials - was achieved.

Hang Seng Index reforms

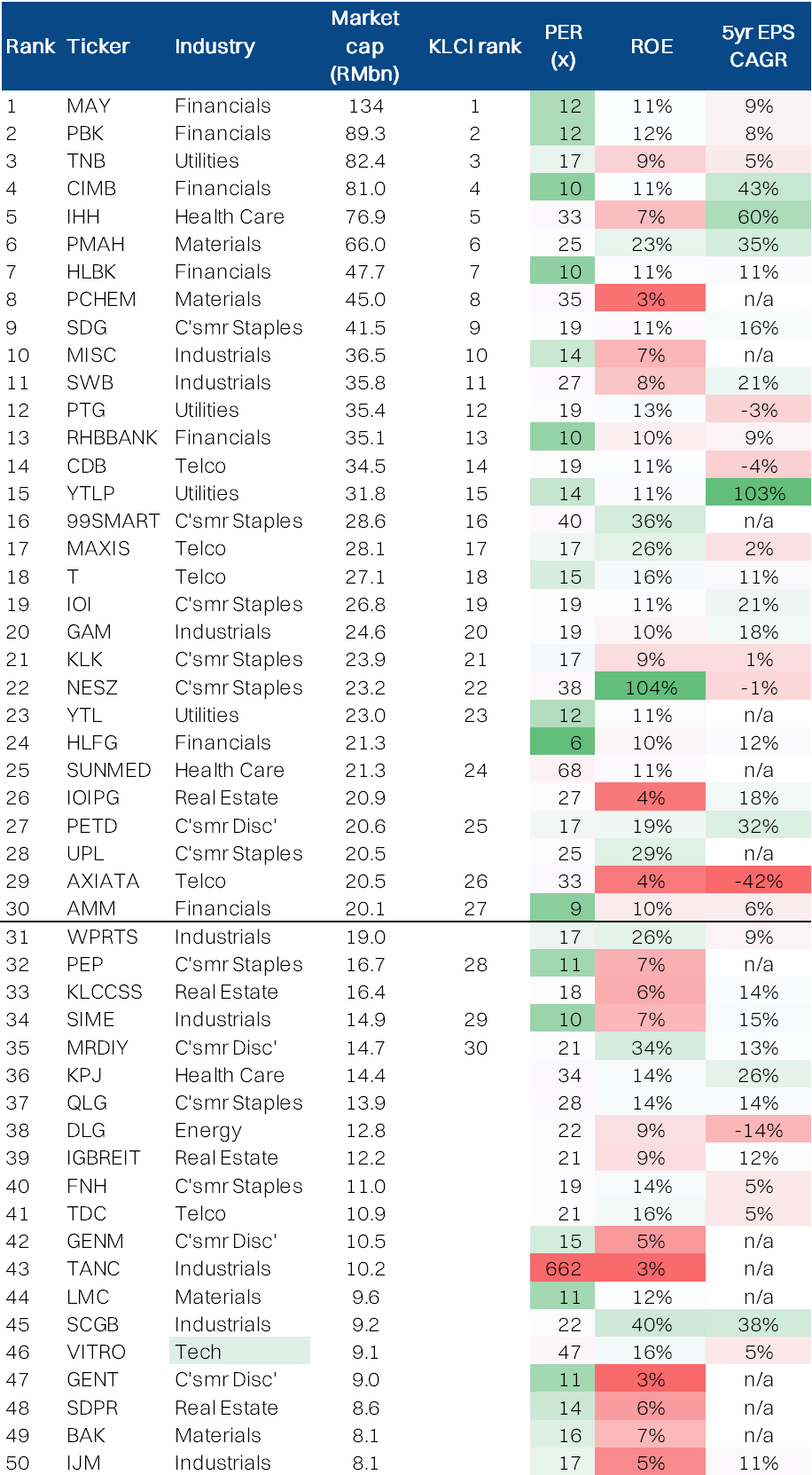

We'll wrap up with this table that shows the current KLCI constituents and the potential 20 additions (at the time of writing at least). With only one technology name (ViTrox), the proposed expansion feels more like a minor update than a reform.

Bursa Malaysia: Top 50 stocks by market cap