Aussie diesel cost risks are overlooked

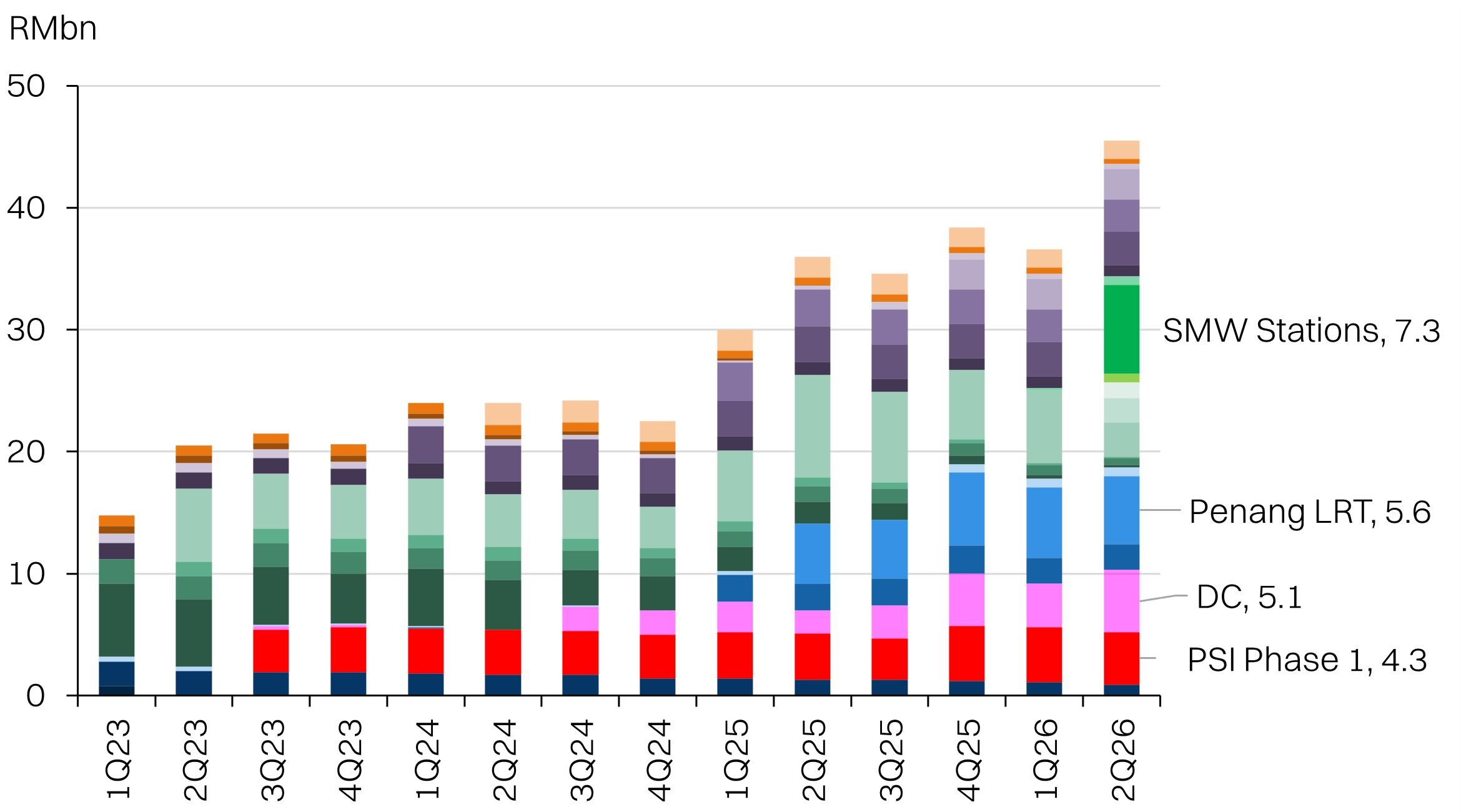

The RM7.3bn Sydney Metro West Stations Package West has no cost pass-through.

GAMUDA

GAM | 5398.KL

Not Rated

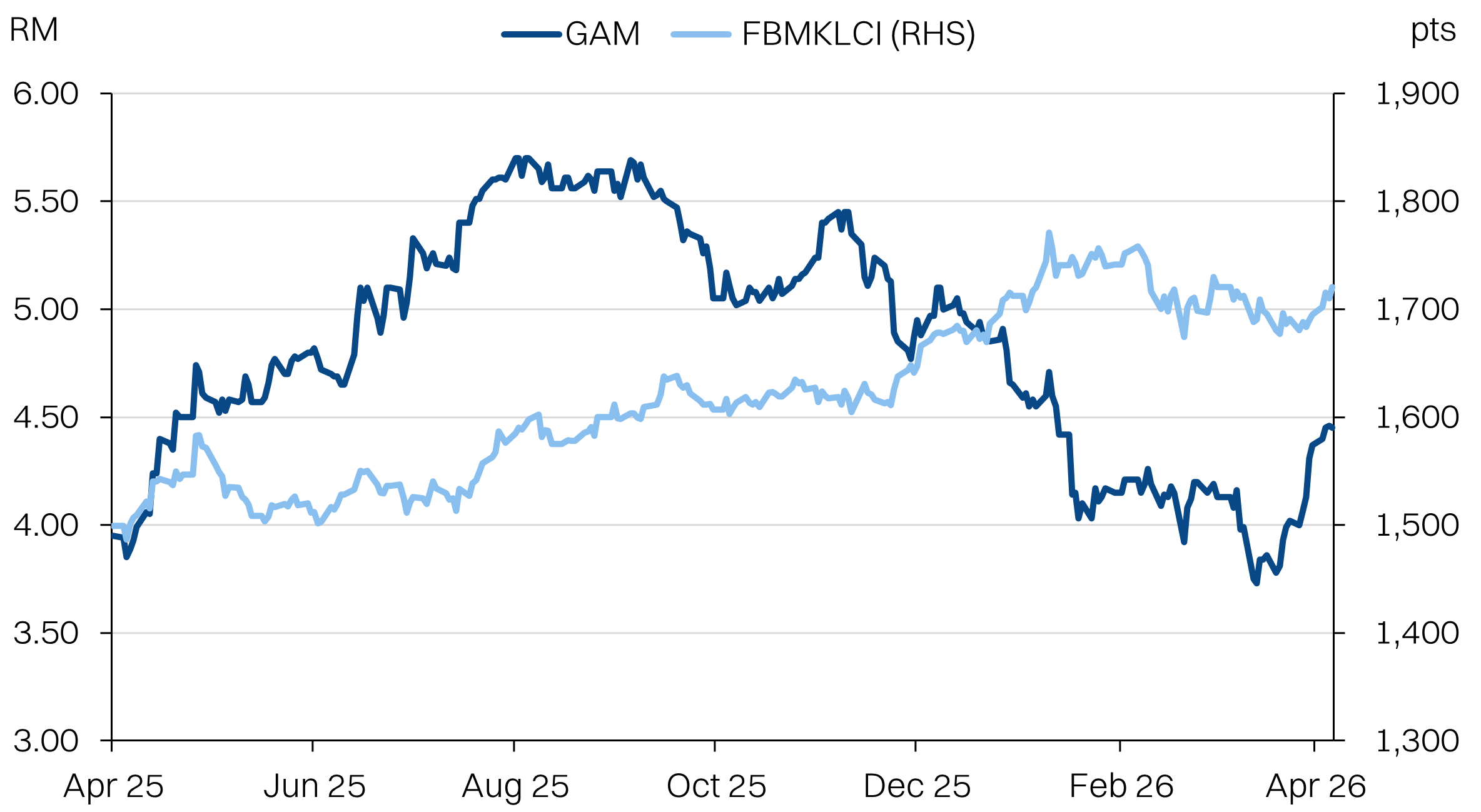

Fair value: RM3.90

Last price: RM4.45

Market cap (RMm): RM26,506m

Shares out: 5,956m

52-week range: RM3.70 / RM5.80

3M ADV: RM91.0m

T12M returns: 18%

Disclaimer: By using this information, you acknowledge that you are solely responsible for evaluating the merits and risks of any investment decision and agree not to hold NewParadigm Research liable for any damages arising from such decisions.

Key takeaways

- We estimate a 1-2% net margin risk from the diesel price escalation (50-60%) for Gamuda, or 15-30% hit to FY26E consensus NP.

- Main drag stems from Sydney Metro West station works in Australia as well as the Penang Land Reclamation project.

- This sensitivity excludes other cost escalation as well as the impact to the property segment.

Share price performance

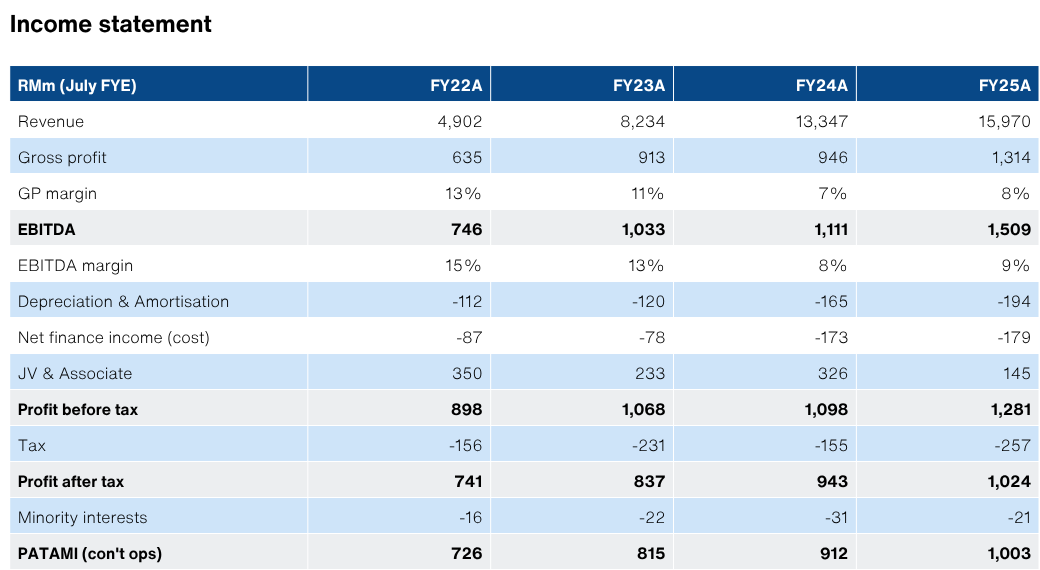

| RMm (FYE July) | FY23A | FY24A | FY25A | FY26E |

|---|---|---|---|---|

| Revenue | 8,234 | 13,347 | 15,970 | 17,165 |

| Growth YoY | 68% | 62% | 20% | 7% |

| EBITDA | 1,033 | 1,111 | 1,509 | 1,429 |

| EBITDA margins | 13% | 8% | 9% | 8% |

| Adj NP | 815 | 912 | 1,003 | 913 |

| NP margins | 10% | 7% | 6% | 5% |

| ROA | 3.4% | 3.4% | 3.3% | 3.0% |

| ROE | 7.5% | 7.9% | 8.3% | 7.0% |

| PER (x) | 32.5 | 29.1 | 26.4 | 29.0 |

Source: Company data, NewParadigm Research, April 2026

No rise and fall clause in Gamuda’s largest project

- Sydney Metro West - both the Western Tunnelling Package (RM0.2bn and the Stations Package West (RM7.3bn) explicitly do not have “rise and fall” clauses, according to public record contracts. Fortunately the diesel intensive WTP is already at the tail end of the project with the TBM works completed last year. However, for the stations project, Gamuda will not be able to pass on costs.

- Over in Malaysia, government projects are lump-sum and do not have a pass-through mechanism. This will apply to major projects like Penang LRT (RM5.6bn), Rasau Water Treatment Plant (RM0.9bn) and Upper Padas Hydro Dam (RM2.1bn).

- However, the biggest pain point will be Penang Silicon Island, Phase 1 (RM4.3bn), as Gamuda is the principal and will have to absorb all the additional cost. Land reclamation is also highly fuel-intensive.

- Mitigation strategies: Gamuda has proved capable at navigating crises and minimising the impact. For the Australian and Malaysia public sector jobs, the primary mitigation strategy is to lobby the respective governments for relief. The Australian Civil Contractors Federation (CCF) is already making a case for it (link). As for PSI, Gamuda will likely scale back works. As the principal, Gamuda can afford to delay the project with a trade-off being the interest costs and machinery overheads.

Australia is highly exposed.

- Gamuda’s overseas construction margins are very thin to begin with, less than 4% net. A 1ppt drop in margins will knock off 25% of segment profits.

- Australia is highly exposed to the Gulf energy crisis, importing almost 90% of its diesel requirements. Diesel prices peaked at +90% vs pre-war before the government’s temporary cut to excise duty brought it down to +78%.

- We also flag that the shortages will take time to resolve since many of the oil production assets in the Middle East have been shut in and will require time to restart. Our base case assumption is US$80/bbl oil by year-end, assuming the strait is reopened within 1 month.

Earnings risk

- The low-end of our assumption suggests a 20% earnings downside risk as the construction segment net margins are only 5%.

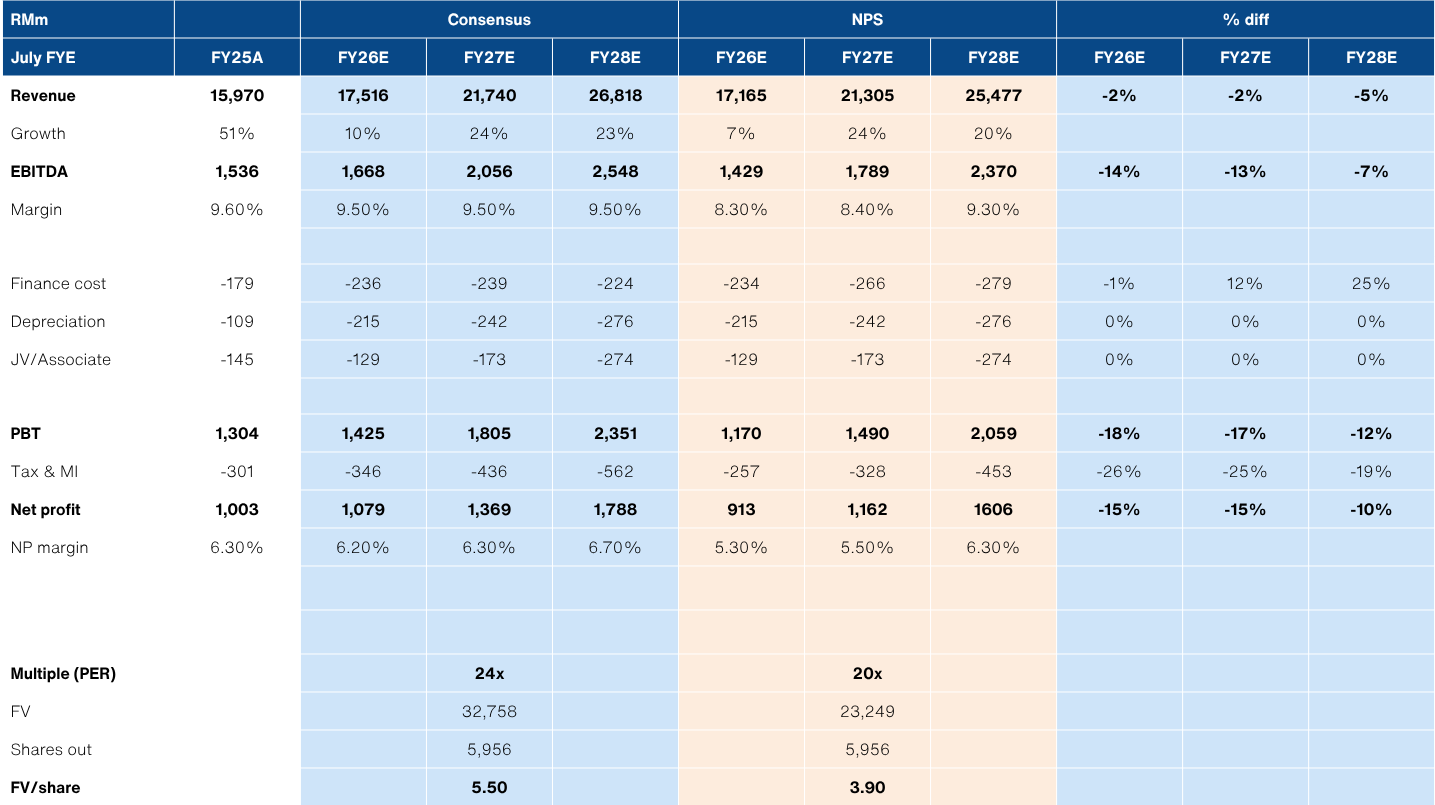

- We ascribe a FV of RM3.90 on 20x FY27E adj NP of RM1.2bn (-15% vs consensus) on bearish operating outlook.

About the Company

Gamuda is the flagship construction company in Malaysia with a focus on large infrastructure projects. Gamuda since 2022 has expanded its footprint abroad with Australia, Taiwan and Singapore now making up almost 60% of the group’s sizable RM45.5bn orderbook. Australia is by far the largest overseas market with an RM15.7bn orderbook, boosted by the acquisition of DTI in 2023. Domestically, Gamuda has been a beneficiary of the datacentre boom, with roughly RM5bn in DC orderbook.

Gamuda also boasts a sizable property development segment, which contributes ~37% of earnings. The group’s Malaysian property arm is focused on township development while the overseas arm employs a quick turn-around strategy. The property division has an orderbook of RM8bn.

About the Stock

Gamuda is an FBM KLCI constituent stock with a market capitalization of RM26.5bn, making it the largest construction stock in Malaysia. It is also highly favoured by analysts with unanimous buy calls on the stock and an average target price of RM5.50 which implies a PER multiple of 23x consensus’ FY27E earnings.

Gamuda’s stock is well-institutionalised. The single largest shareholder is the Employee’s Provident Fund with a stake of 20.26%.

Investment Idea

Consensus earnings expectations are simply too high for FY27/28E, at RM1.37bn/RM1.79bn respectively. It assumes margins will hold flat in FY26/27E (at 6.2/2.3%) and expand in FY28E (6.7%). We see substantial downside risk to these numbers.

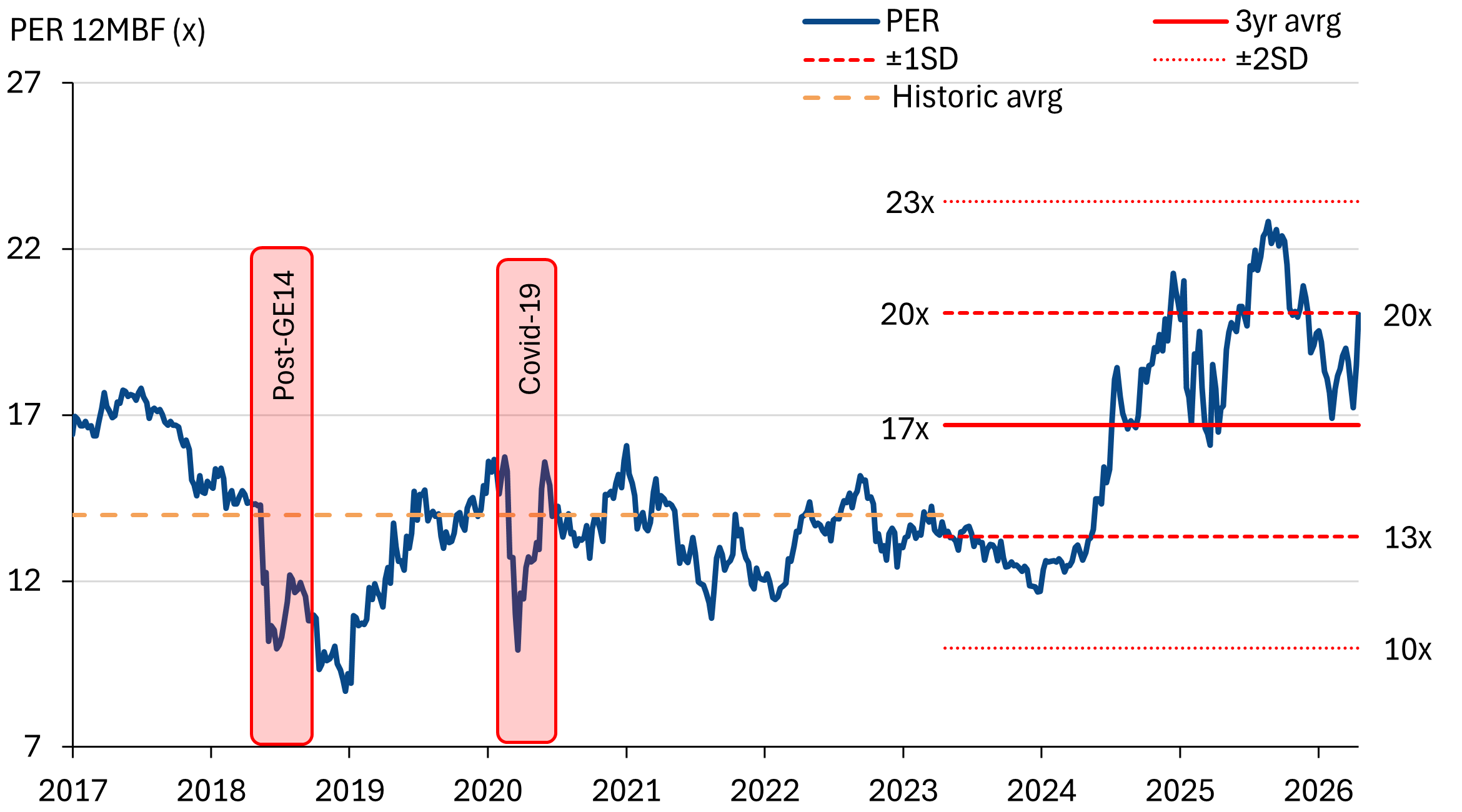

Meanwhile, Despite the recent correction in valuations, Gamuda continues to trade at +1SD vs 3yr average PER, at 20x 12MBF.

We anticipate continued margin pressure from diesel prices will hurt both the construction and property segments. Additionally, there is more risk from rising raw material prices as well as potential for softening demand (particularly on the property segment) if the war does more lasting damage to the global economy.

Even with an optimistic lens, if the market prices through the worst of the margin compression (FY26) to focus on FY27E, Gamuda would need to hold on to its current 20x PER multiple for a fair value of RM3.90 per share. This is on the basis that street is too bullish on earnings expectations and we estimate a -15% downside that brings margins to 5.4%.

Key Risks & Catalysts

- Risks: We did not dive deep into the potential earnings impact from higher costs hitting the property development segment. Gamuda cannot pass on the costs for existing projects under the sell first build later model that it adopts for most of its projects. Additionally, the economics of the PSI investment could be severely degraded if costs exceed previous planning.

- Catalysts: A rapid end to the war would put Gamuda back on bullish footing. Additional demand for datacentre projects, driving new project wins over the next 12 months would also be a positive catalyst. Finally, Gamuda could be bailed out of the diesel cost crisis by the respective governments.

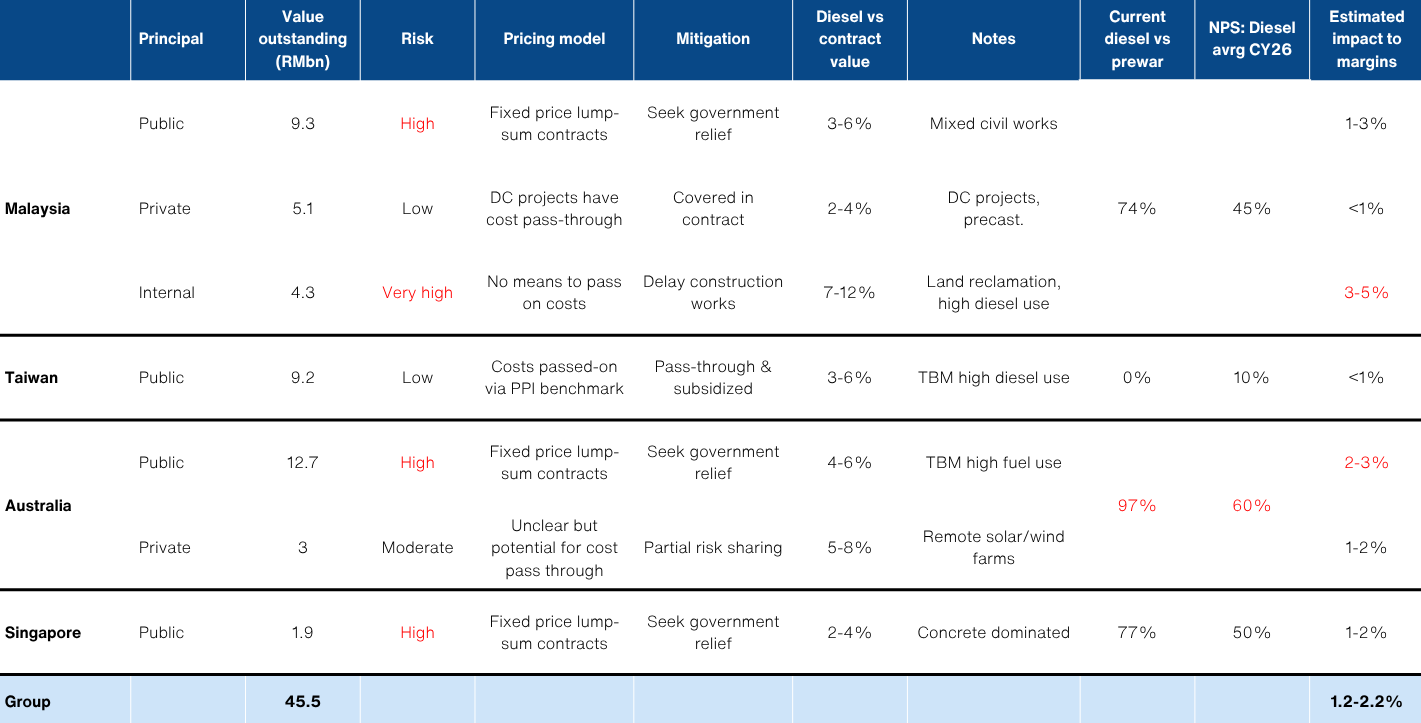

Gamuda’s construction risk matrix for diesel

Gamuda’s earnings will be negatively impacted by the surge in diesel prices. Consensus numbers do not appear to be pricing this in, given forecast margins remain flat. Anecdotally, we think street has assumed >70% of orderbook to have cost pass-through built in. In contrast, we estimate that half of Gamuda’s projects carry high risk, with limited means to pass on costs within existing contracts.

Meanwhile, we see about one-third of projects as being either shielded from diesel prices escalation and/or protected by cost pass-through mechanisms. The balance were either difficult to determine or should carry moderate cost risk.

On balance, we estimate a 1.2-2.2% risk to construction net margins, based on a 45-60% diesel cost surge (vs pre-war) assumption.

Diesel risk matrix

The big risks

- Sydney Metro West, Stations Package West - This project is worth RM7.3bn and is meant to begin works this year. It is the single largest project in Gamuda’s orderbook and is fixed-price. Margins are also very thin for Gamuda’s overseas operations and as a foreign contractor, relief might be more challenging to secure.

- Penang Silicon Island, Phase 1 - This carries the most long-term risk to Gamuda, since it is also the principal for the project. Any cost escalation today will directly eat away at the project’s economics, which are already challenging to begin with. Land reclamation is one of the most energy intensive modes of construction as well. Fortunately, Gamuda can slow down operations since it has control over project timelines. However, borrowing costs and machinery overheads will persist.

- Malaysian government projects - This broadly amounts to RM9.3bn. Malaysian public works contracts are typically fixed-price. The only outlet would be an appeal to the government for relief. Oftentimes, this might be done via variation orders.

- Singapore government projects - Contractors rarely secure relief for cost overruns under the fixed price contracts. At most, there could be some flexibility with delivery milestones or financing support.

Gamuda’s resilience - about one-third of orderbook

We did find a number of projects/project types where Gamuda will be resilient to the diesel price shock:

Taiwan - safest regime for contractors

- While Taiwan is virtually 100% dependent on imports, of which 97% is imported from the Middle East, the Taiwanese government uses subsidies to intervene on pricing which minimises the transmission to the economy. At the time of writing, diesel is NT$31.0/l which is only 15-24% above the pre-war level. The CPC Corporation (state-owned O&G company) is absorbing the difference which is in excess of NT$7/l. Taiwan currently has one of the lowest diesel prices globally, for a non-oil producing country.

- Critically for contractors like Gamuda, Taiwan’s public sector procurement follows a model contract template that includes a mandatory price index adjustment mechanism under the payment terms (article 5), by default. The cost pass-through is calculated based on the prior month consumer price index (since 2022).

Australia - Marinus link and road projects.

- The largest contract from Gamuda’s Australian book that would be shielded from cost shocks is the Marinus Link (RM1.3bn), which falls under an incentivised target cost (ITC) model. This is a hybrid, collaborative construction approach that is similar to the alliance model. The provisions are clear from publicly available documents, that the direct cost increase can be shared with the project principal. However, the quantum is not made clear.

- Most of Gamuda’s road projects should include some rise and fall provisions. The Richmond Road (RM500m) and M1 Motorways (RM100m) should be covered. Though, the remaining balances are relatively small.

Malaysian DCs

- Over in Malaysia, management is guiding that the datacentre projects have risk sharing clauses that will allow most of the cost surprise to be passed on to the client. Considering the civil works cost for a DC project is relatively small compared with the total build cost (around ~10% only), it is reasonable to assume that the DC’s principals should be able to absorb the cost increases. Gamuda has approximately RM5bn of datacentre related projects in hand.

Market expectations could resist earnings downgrades

Key management guidance includes an orderbook of RM50bn by end of the year and RM10bn in sales for the property segment. Additionally, management has indicated that margins should be relatively defensive, despite the diesel cost headwinds. In turn, earnings expectations are well-anchored around RM1.1-1.2bn.

Key factors that would allow Gamuda’s share price to remain resilient to earnings downgrades and incrementally negative expectations include:

- Forward-looking bias towards new orderbook wins

- Expectations that the Strait of Hormuz will open sooner than later, allowing for diesel prices to stabilise.

- Newsflow on governments moving to support contractors.

- Continued concentration of institutional investors in large cap construction stocks for indirect exposure to datacentres.

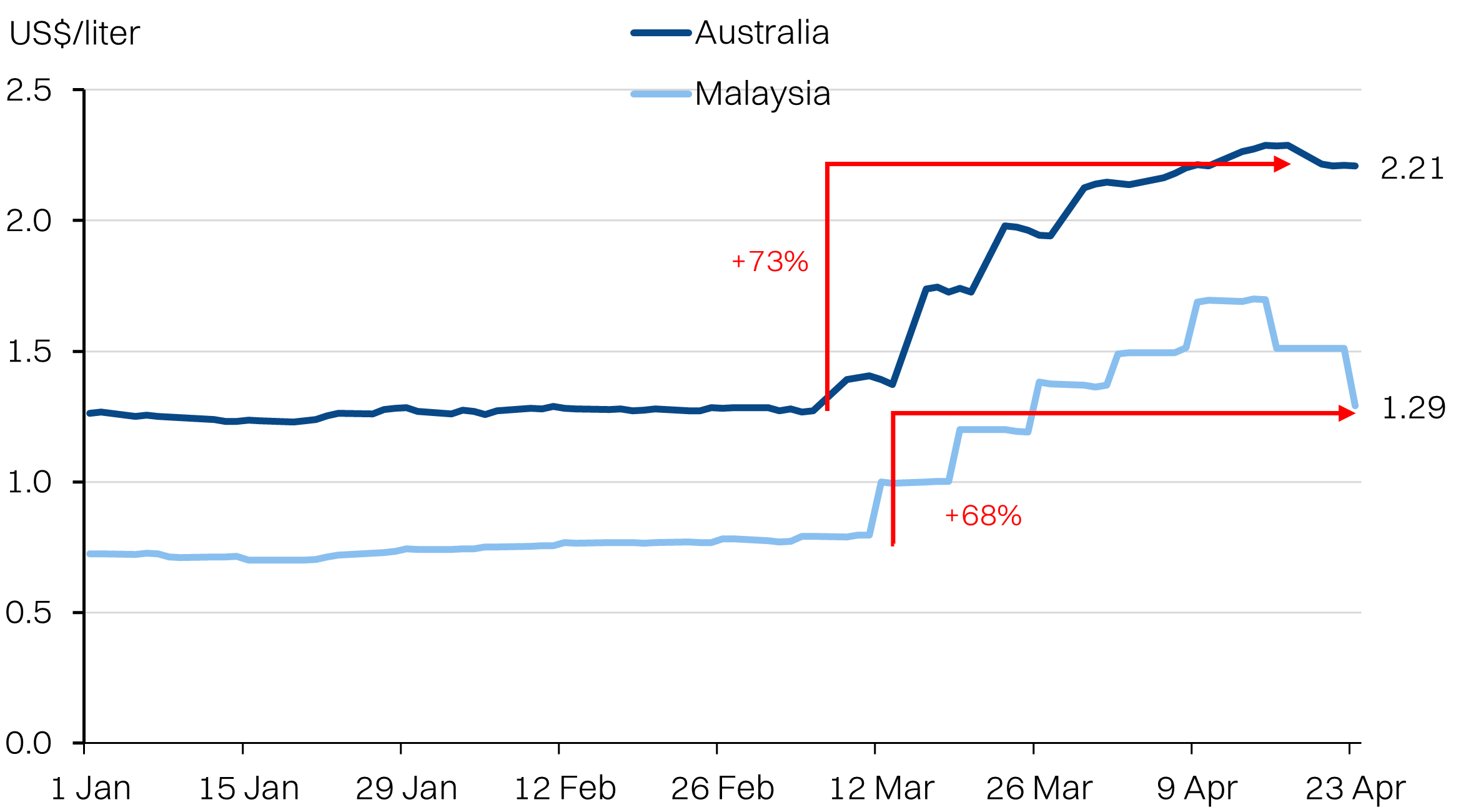

Australia’s diesel prices spike

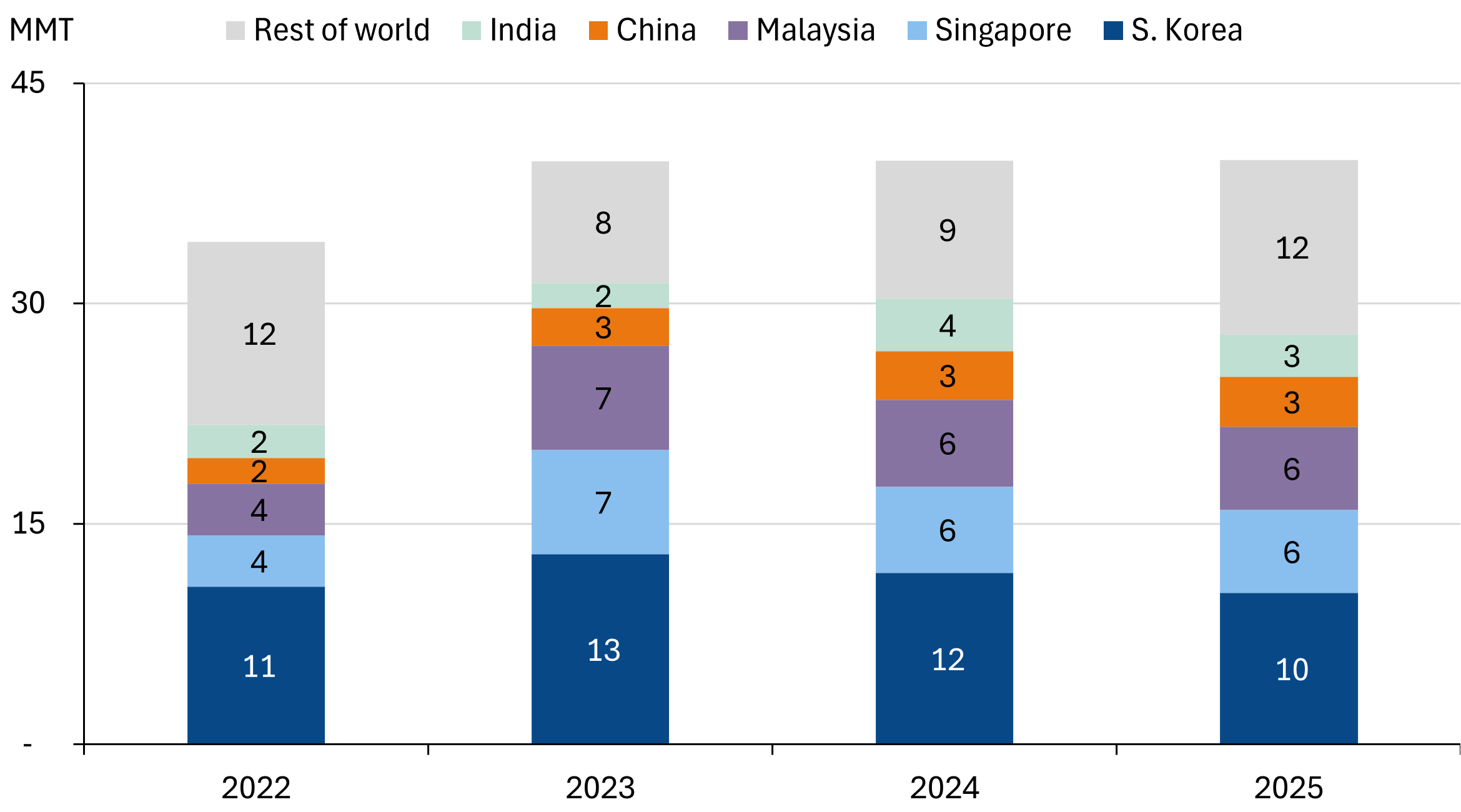

Australia is more exposed to the shock of the US-Iran war than Malaysia, despite being an oil producer, as the country has very limited onshore refining capacity. Roughly 90% of the country’s diesel requirements are imported and the top exposures include South Korea, Singapore, Malaysia, India and China. Notably, China has curtailed export of refined products. And excluding Malaysia, the other countries are not oil producers themselves but heavily reliant on Middle East crude oil.

This has resulted in relatively high spreads vs crude oil, with Aussies paying a crack spread of nearly US$50/bbl - almost double the pre-war spread. The one saving grace for Australia, is the country’s LNG exports which account for ~20% of global exports. This gives Australia some leverage to help secure diesel supplies in exchange for LNG, which has also been disrupted by the closure of the Strait of Hormuz.

Our base case view is for crude oil to remain above US$80/bbl by year end, on the assumption that the Strait is gradually reopened over the next month.

Diesel imports to Australia - country of origin

Diesel prices

Australia’s CCF warns of insolvencies if Federal and State governments do not act

The Australian Civil Construction Federation published a detailed report earlier this month to sound the alarm bells on the potential damage the surge in diesel prices could entail on the sector.

It estimated the spike in diesel prices by 78% (after the temporary cut in fuel excise implemented) in Australia could result in additional cost of ~1.2% of annual engineering construction value, compared with the 3-5% margins that large civil works (>A$1bn projects) typically enjoy. In contrast, the CCF estimated that 80-95% of contracts were fixed price with no means to pass on costs. Even the contracts with “rise and fall” provisions, were not directly linked to fuel prices, but rather to benchmark indices like the producer price index, that the CCF argues is an inadequate mechanism to pass on costs.

Keep in mind that this report only addressed the fuel price spike and not the broader rise in other construction material inputs that would be affected as well.

The point of the report was to persuade the state and federal governments to provide relief to contractors, or risk substantial damage to the economy. ASIC statistics already show that the sector with the highest number of insolvencies were in construction, of which the bulk came from NSW.

One of the key proposals from the CCF specifically calls for government support for public works, which we will quote:

“.... the Federal and State Governments should provide targeted top-up grant funding to councils to address unanticipated input cost increases, particularly for projects already underway where contracts do not allow for cost escalation.”

Australia insolvencies: construction sector leads

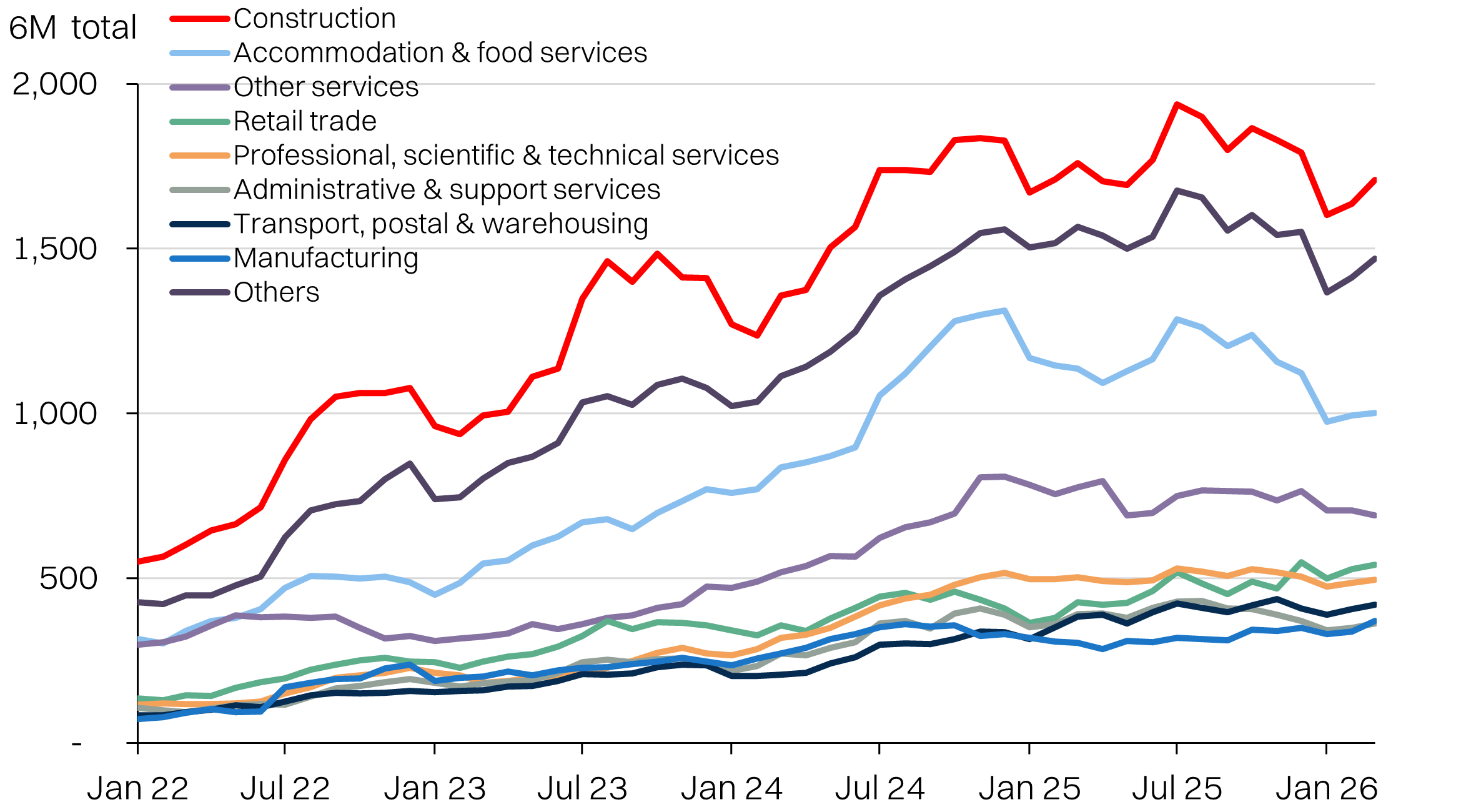

Aussie construction stocks

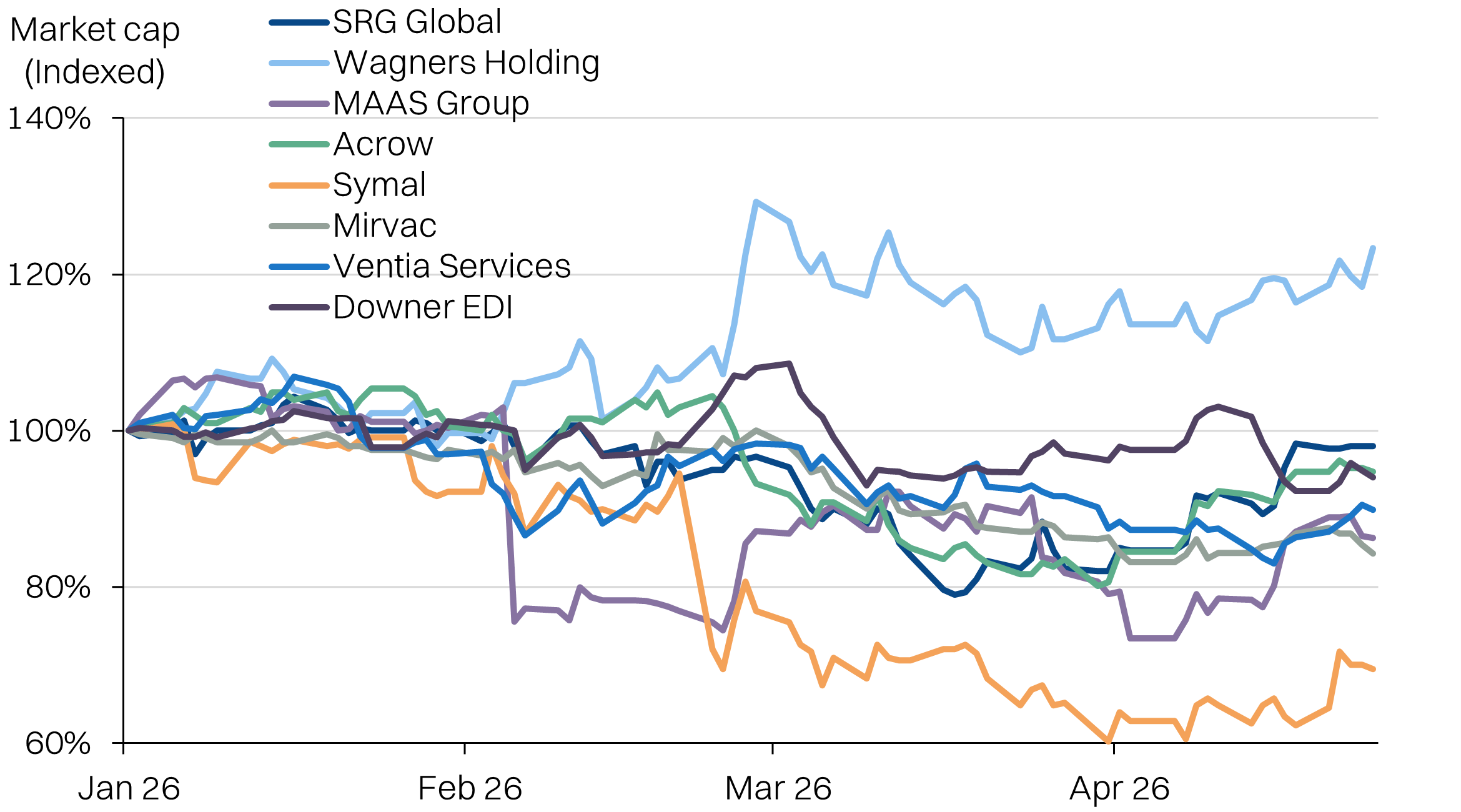

It is also worth taking a look at the valuations and market sentiment on Australian construction companies. The onshore investors there will have a better feel for the sector’s pulse. Of the 8 companies we screened only one is trading in the green from the start of the year.

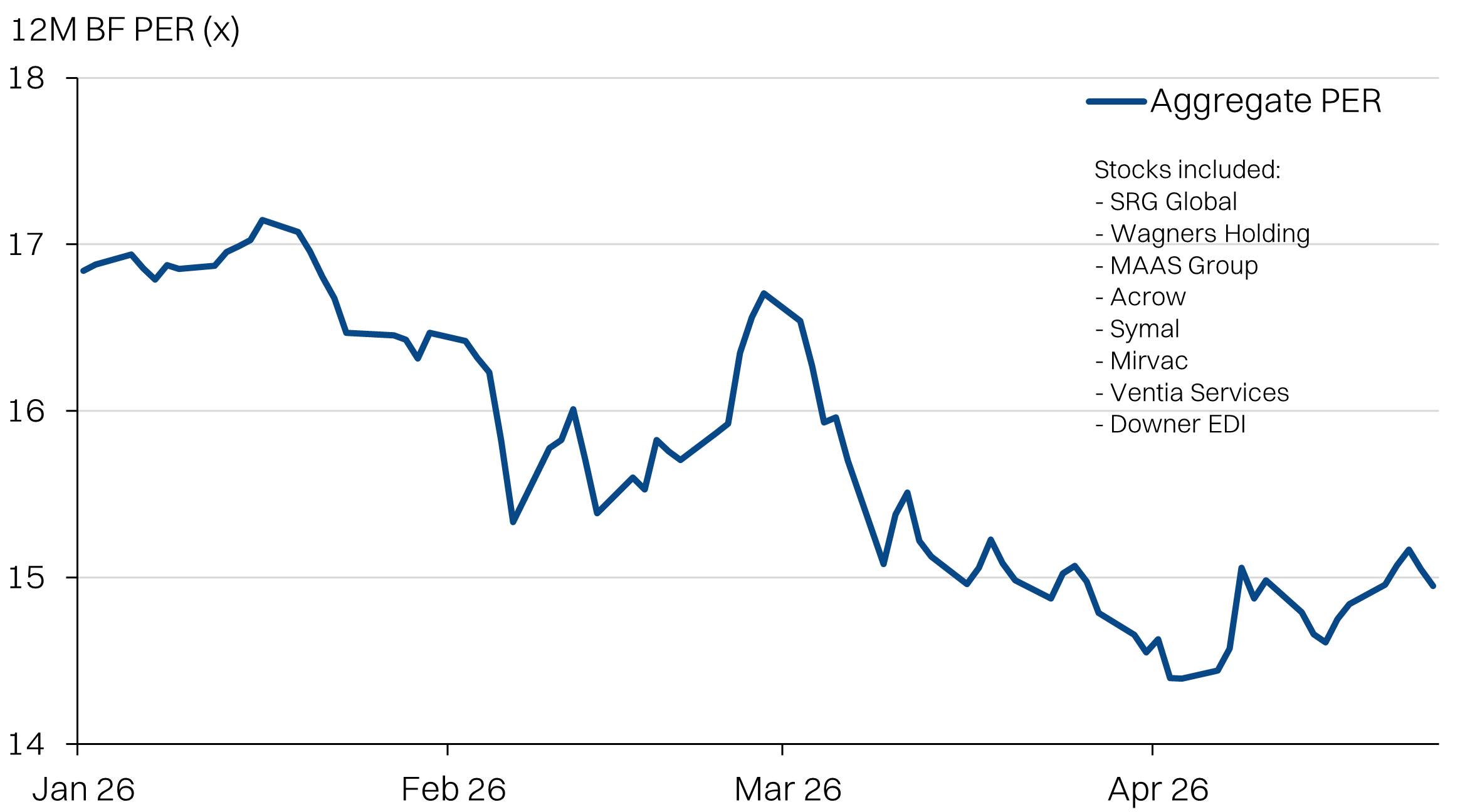

Looking at valuations, the 8 stocks we screened saw aggregate PER (12M BF) fall from 17x at the start of the year down to 15x.

Key Australian construction stocks market cap performance YTD

Key Australian construction stocks forward PER

Orderbook breakdown

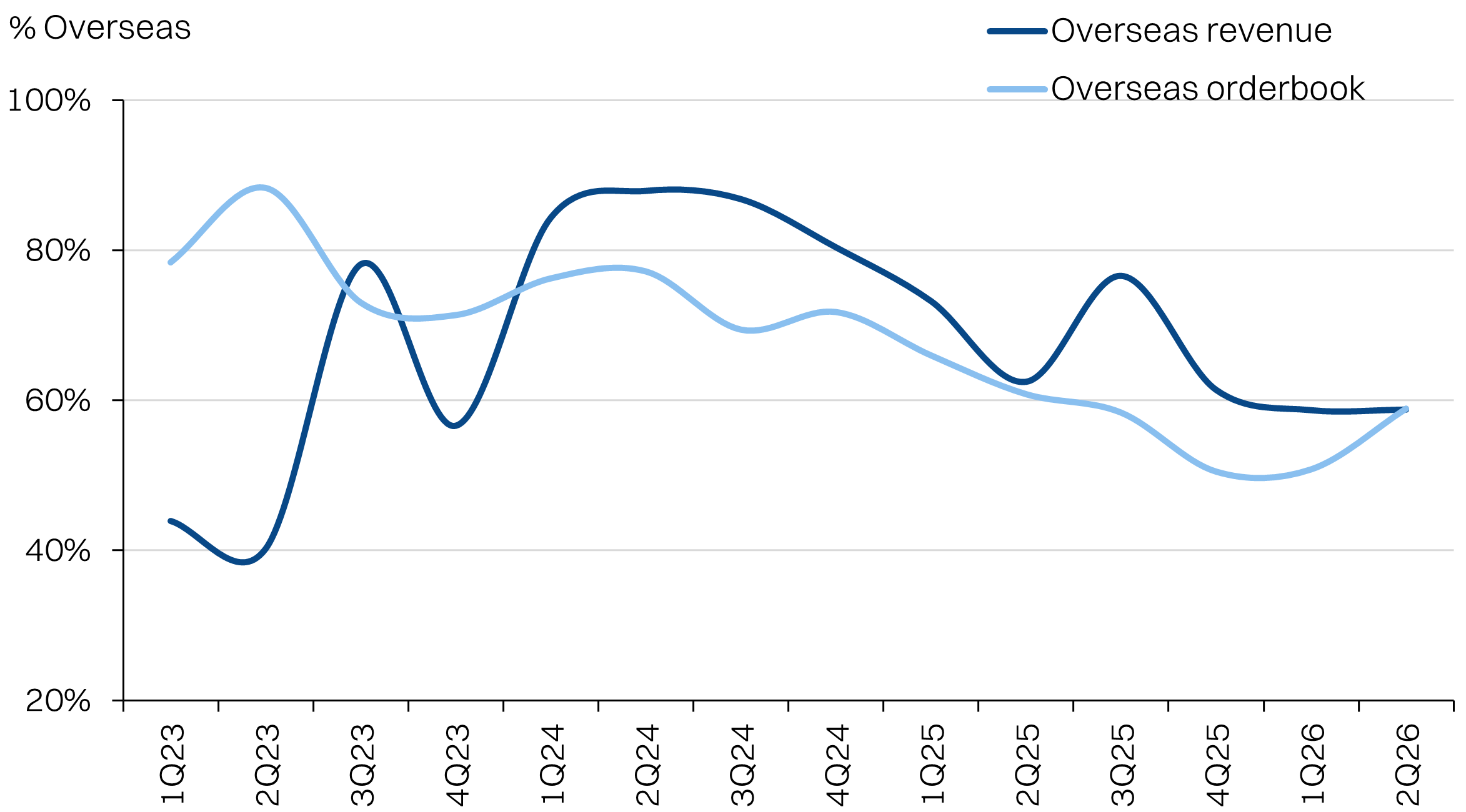

Australian project have underpinned Gamuda’s overseas expansion and now makes up ~35% of the book. In fact, the group’s single largest contract - the Stations Package West for Sydney Metro West (SPW), RM7.3bn) - has been the biggest driver of orderbook growth in the past year. It alone makes up 17% of the group’s orderbook.

Other notable projects are:

- PSI Phase 1, which is an internal project. This makes up almost 10% of orderbook. We have flagged this as a high-risk project, where the incremental cost is borne by Gamuda.

- Datacentre projects have risen to RM5.1bn after the recent RM1.7bn win, making up about 11% of book. We expect cost escalation for DC projects to be passed on.

- Penang LRT - this will be a fixed cost lump-sum contract. The state government is already operating with a very tight budget for this project and will have limited scope to share additional costs.

Orderbook breakdown: Aussie jobs make up ~35% of the book

Overseas mix holding at ~60%

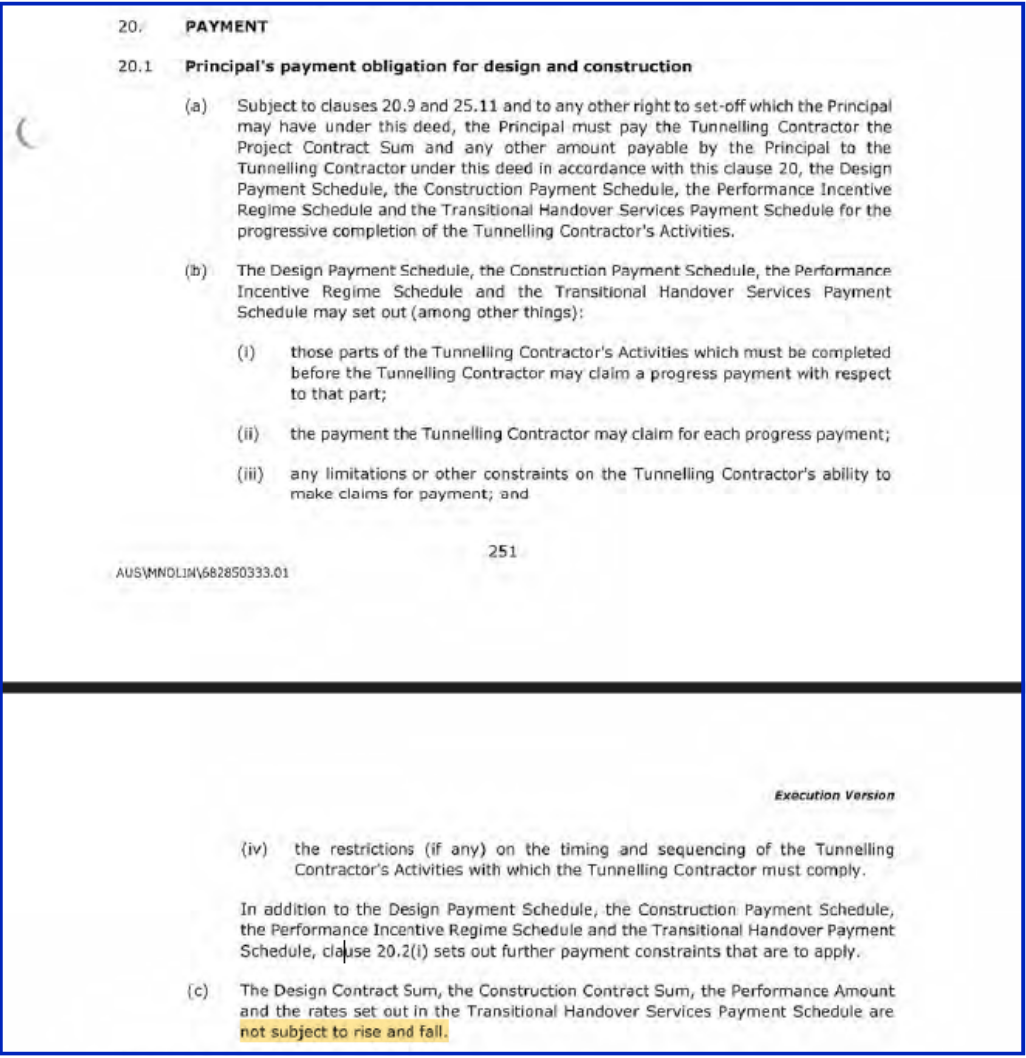

Western Tunneling Package - RM200m

One of Gamuda’s earliest and largest projects in Australia, that was worth RM6.5bn (AUD2.7bn) at the time of award. Gamuda has a 50% stake in this project together with Laing O'Rourke. The project is for 9km of twin metro rail tunnels. The project was first awarded in 2022 and is due for completion this year. As of January, progress was already 98%.

The main details of the contract can be found here, but we have extracted the key payment section where it explicitly states there is no rise and fall clause for this contract.

Fortunately for Gamuda, this project was able to achieve its delivery milestones and the tunnel boring machine (TBM) excavation completed late last year. TBM works are highly diesel intensive and would have been a bigger challenge if primary tunneling works were still underway. Only RM200m work is outstanding as of January.

Sydney Metro West, Western Tunneling Package - no rise and fall clause

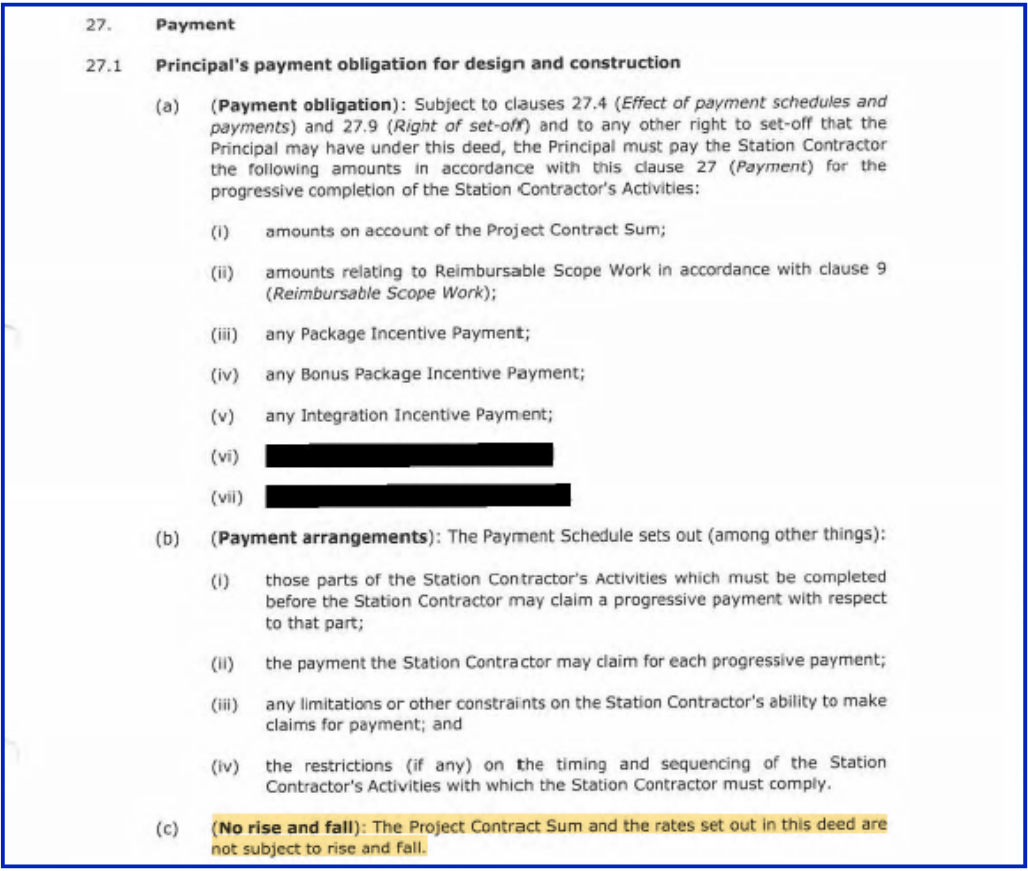

Station Package West - RM7.3bn

The largest single job on Gamuda’s books is the Stations Package West contract worth RM7.3bn (AUD2.7bn), that was awarded in 2025. The job is for 5 underground metro stations and package scope will include the construction of station boxes, entrances and access points, station fit-out works and integration with surrounding precincts.

Gamuda is the sole contractor for this project. Work is supposed to commence in 2026 with completion due in 2031. As of January 2026, work has not yet begun with the project still in the mobilisation stage.

The main details of the contract can be found here, but we have extracted the key payment section where it explicitly states there is no rise and fall clause for this contract.

The primary mitigating factor for this project is that works have not yet commenced. Gamuda could potentially delay or resequence work, waiting for diesel prices to come down. However, the relative savings might be limited.

Sydney Metro West, Station Package West - no rise and fall clause

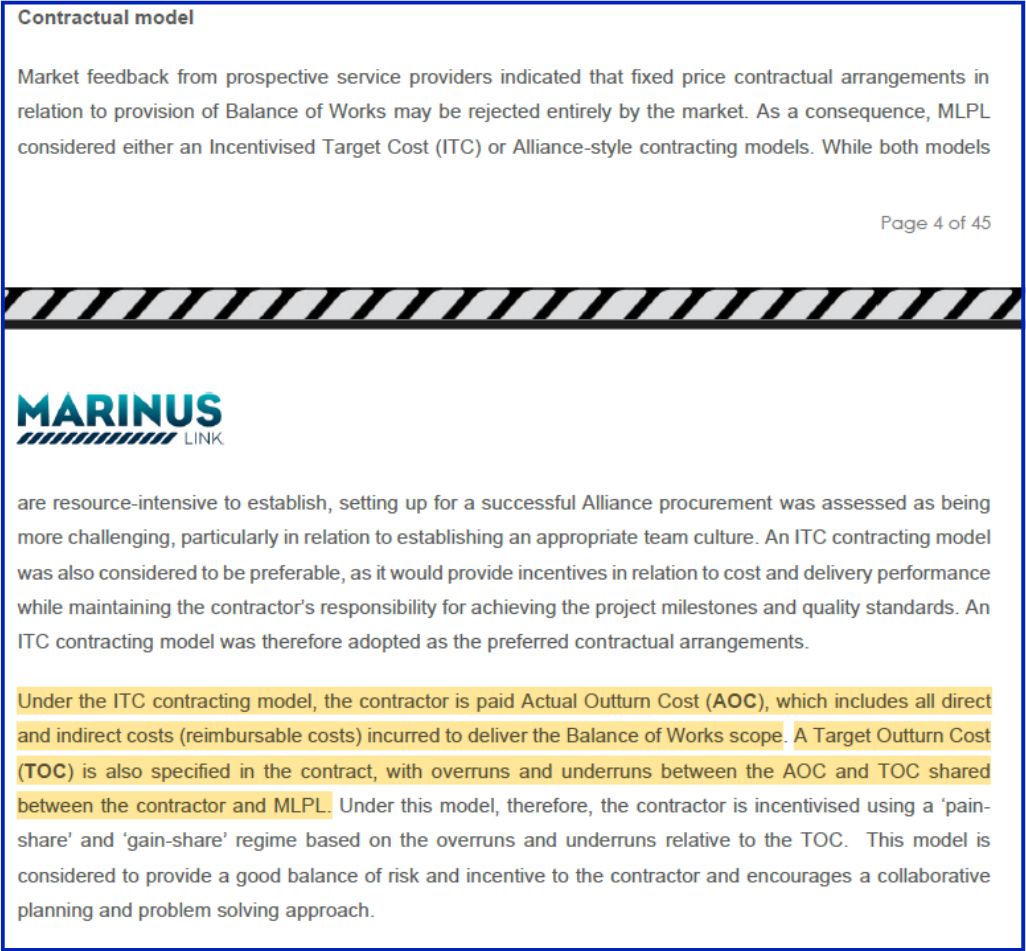

Marinus Link Stage 1 - RM1.3bn

Gamuda’s 3rd largest project in Australia, with a balance of work of RM1.3bn. The project was awarded last year and is due to be completed by 2030. As of January, only 2% of the works have been completed, and is still in the mobilisation stage. The project is a 50:50 JV between Gamuda’s associate, DTI and Samsung C&T Corp.

The high-level outline of the contract can be found here, but we have extracted the key excerpt where it explicitly states that increase in costs can be shared with the principal. Note that this is not the actual contract (like the NSW disclosures) but the planned capital expenditure requirements by Marinus link.

The actual quantum of “pain-sharing” and “gain-sharing” is not disclosed.

Marinus link

Earnings & valuations

We estimate a fair value of RM3.90 for Gamuda based on 20x (+1SD) FY27E Adj NP of RM1.16bn which is 15% below consensus assumptions.

A major difference in our assumptions is a -1.2ppt/-1.1ppt cut to FY26/27E EBITDA margins arising from the cost inflation. Additionally we assumed some revenue curtailment of -2% as Gamuda moves to defer key projects like PSI to defray costs. Additionally, we expect finance costs to grow in-line with net debt (+12% in FY27E), whereas consensus is assuming flat finance costs.

Earnings assumptions and valuations

Gamuda PER bands: still trading at +1SD vs 3yr average

Peaking upgrade cycle?

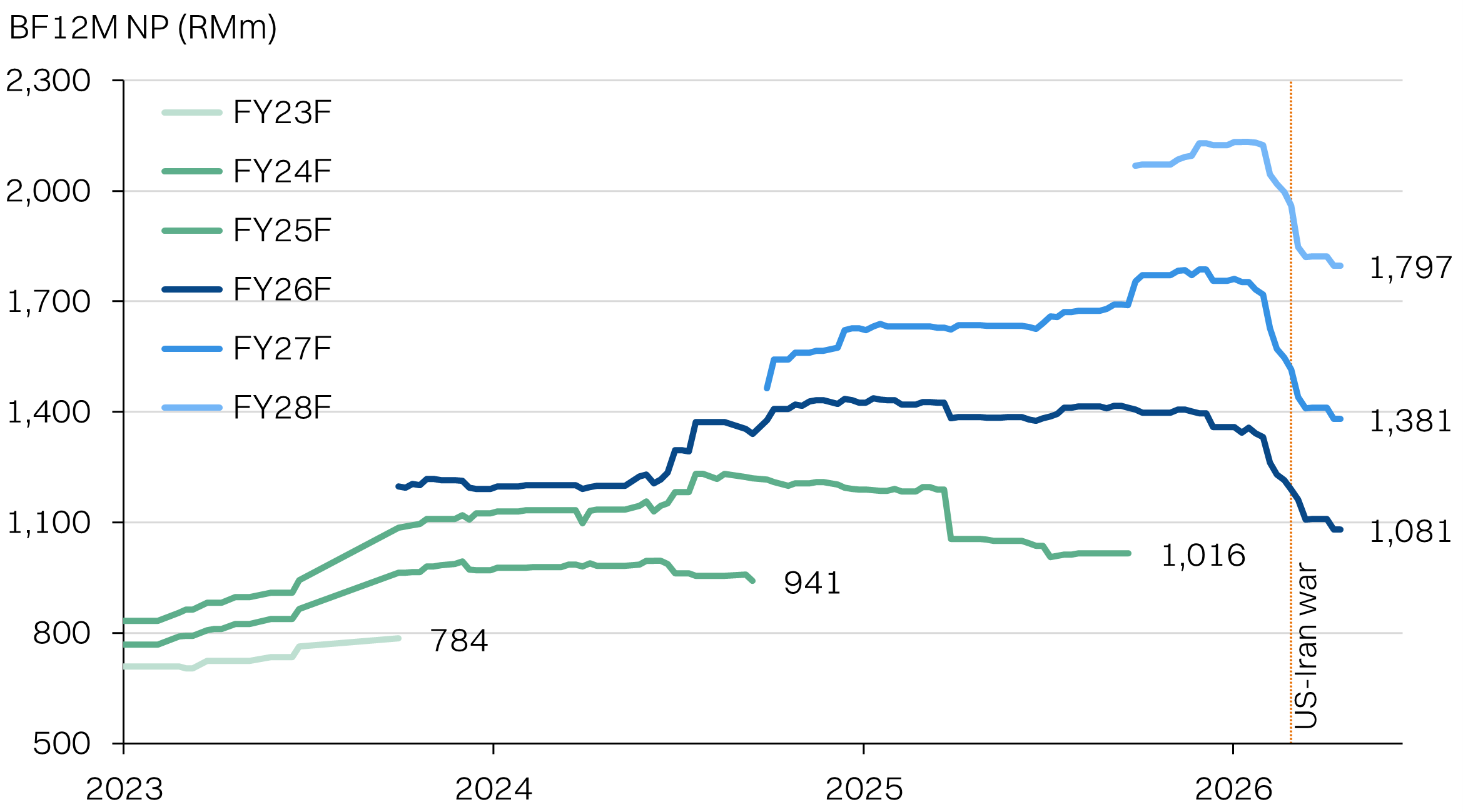

Gamuda’s underperformance this year has not been driven by the war alone. Earnings downgrades began in earnest following the 2QFY26 results and was amplified by the war breaking out. Gamuda’s share price has also moved in tandem with the downgrades.

As per our earnings divergence with consensus, we think the margin assumption remains too optimistic, given the operating environment. Furthermore, the finance costs is not reflecting the steady increase in net debt of the group - at a time where inflation will keep interest rates on an upward bias.

The primary catalyst for further share price correction will be the further downgrade in consensus earnings expectations, on the aforementioned drivers.

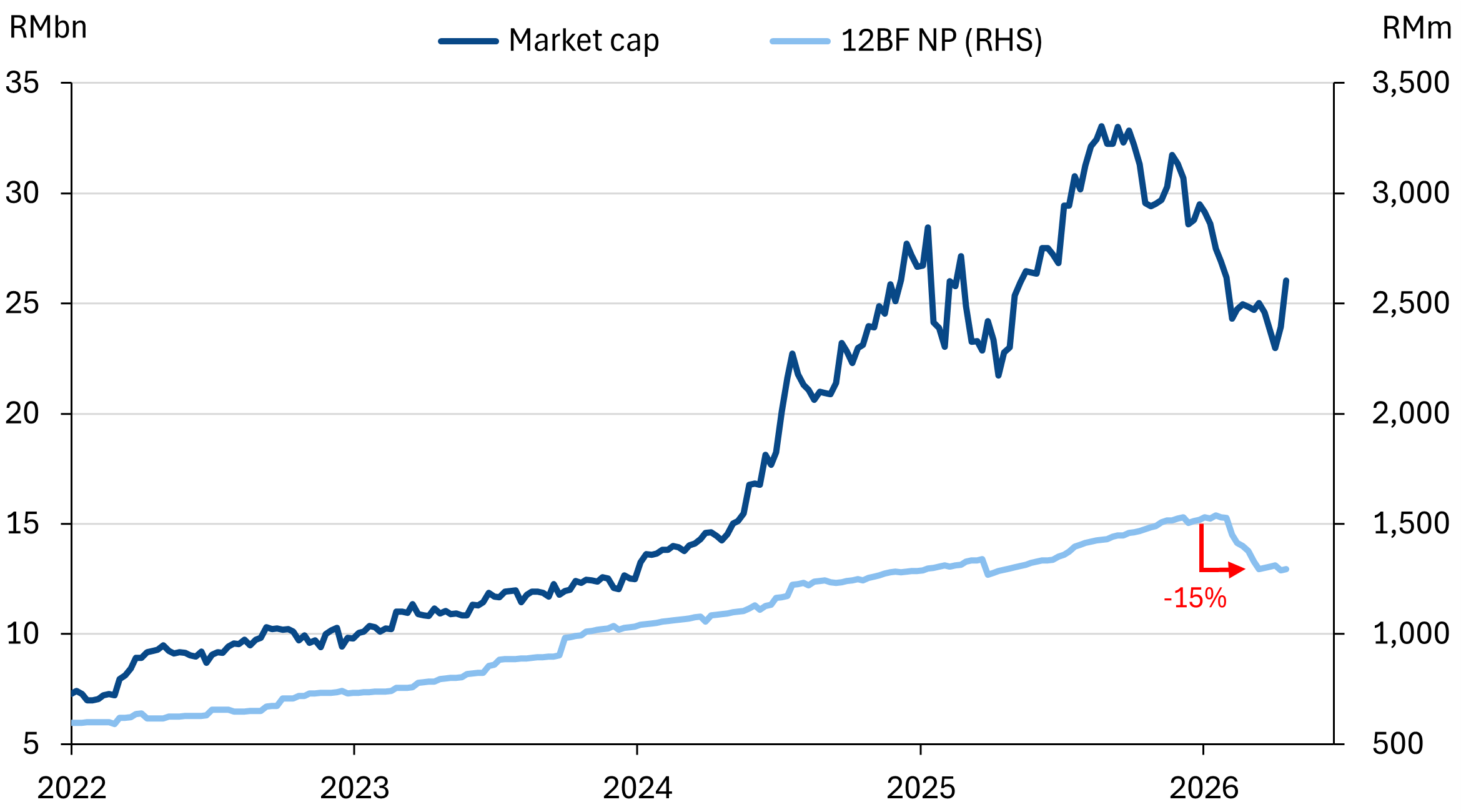

Gamuda market cap has outpaced earnings expectations

Consensus has cut expectations by -15% since 2QFY26 results came out

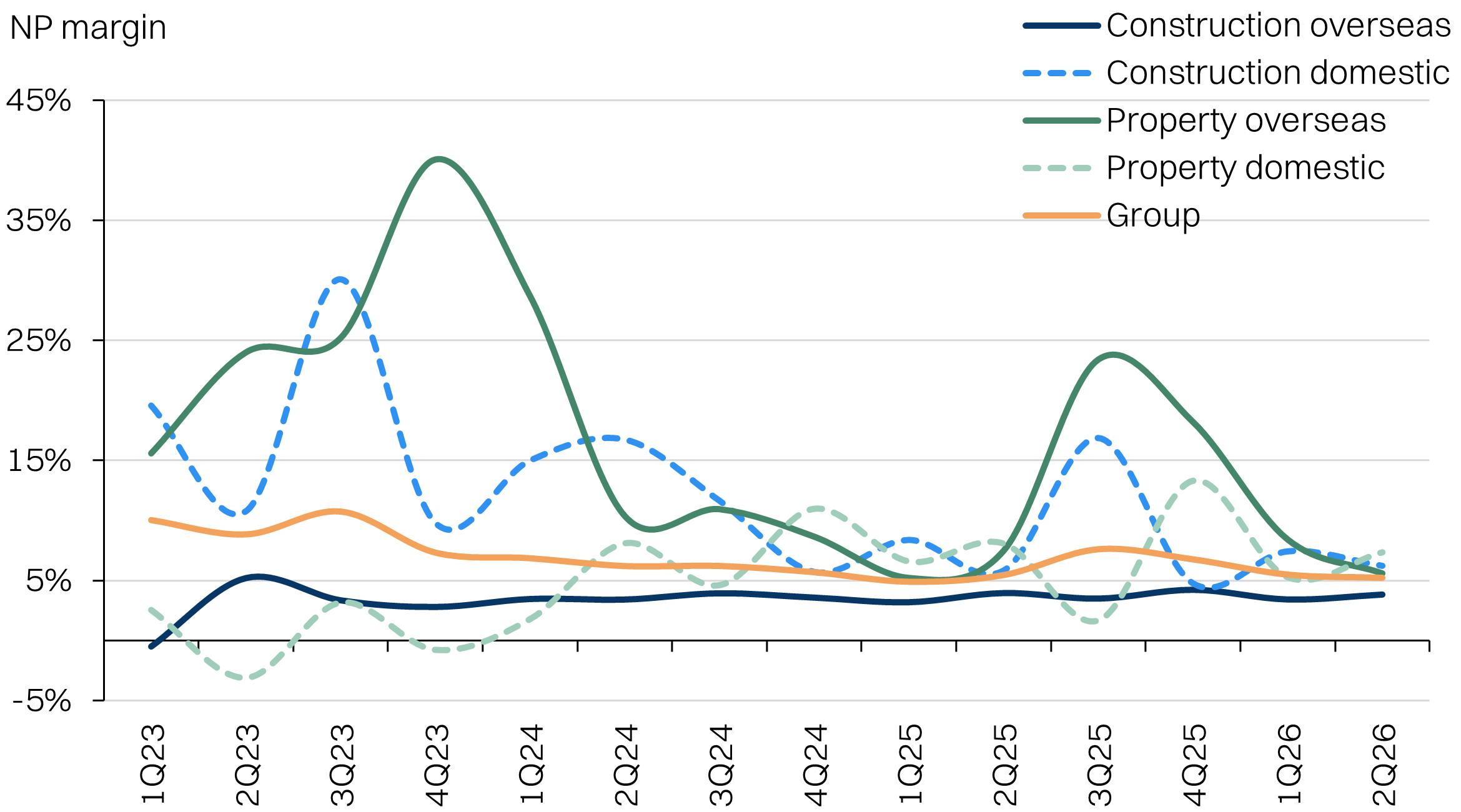

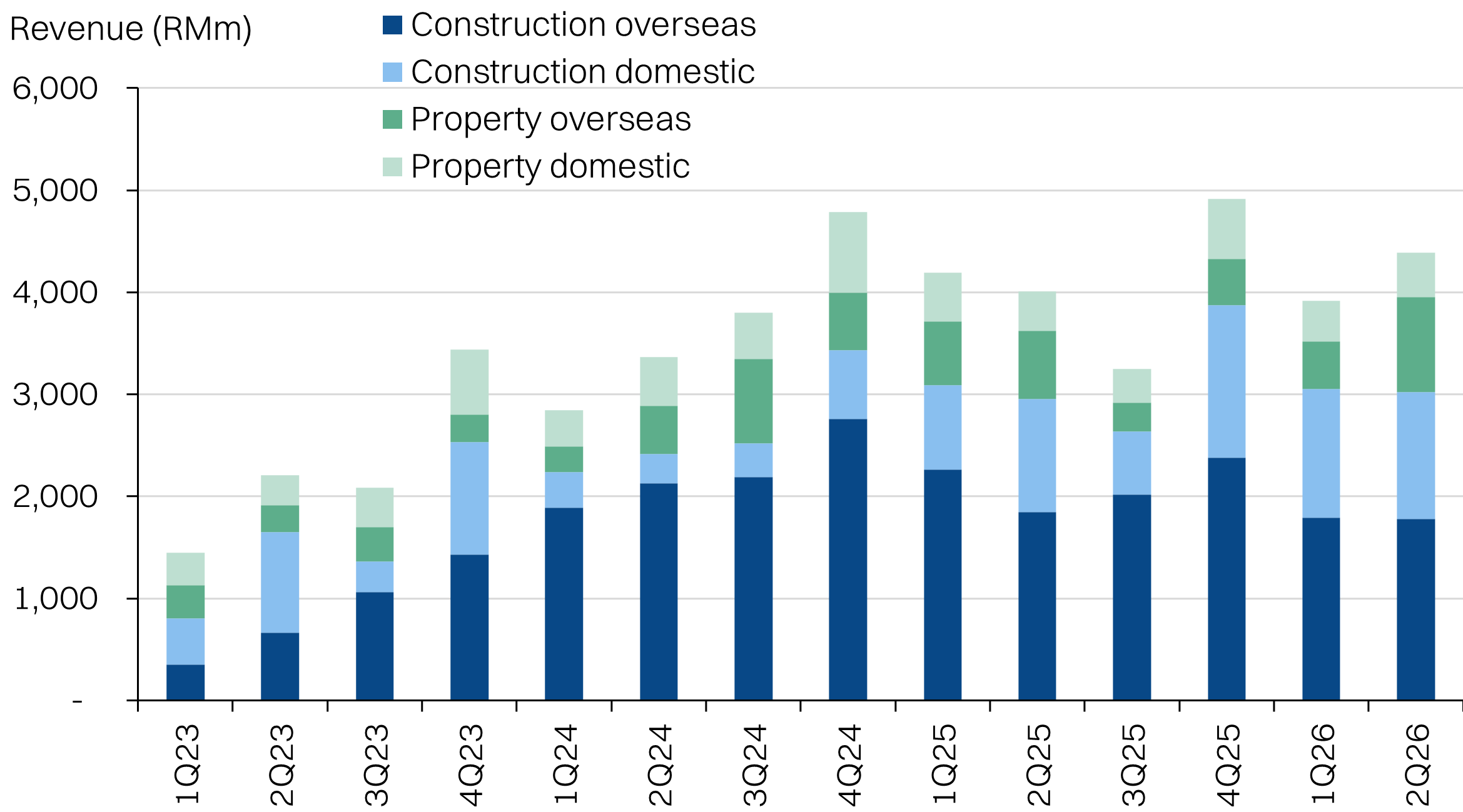

Gamuda’s net margins by segment and geography - on the decline / Gamuda’s revenue by segment and geography - strong growth / Gamuda’s net profit by segment and geography - flattish growth

Source: Company data, NewParadigm Research, April 2026

Bonus read: RTCCO for diesel costs

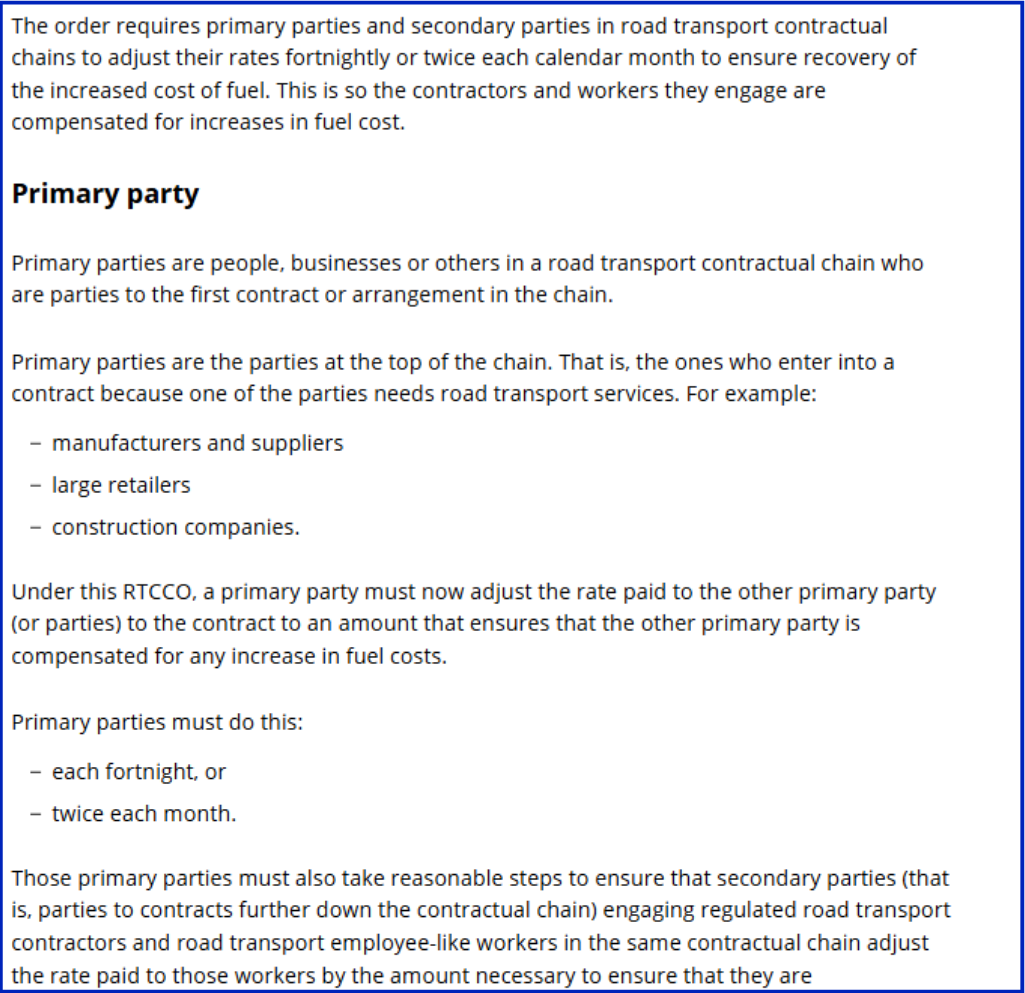

The Australian Fair Work Commission has issued a road transport contractual chain order that will ensure the elevated diesel prices can be passed on by road transport operators to end-clients. This includes construction companies like Gamuda.

Find the full order here.

The order allows for adjustments to existing contracts to include provisions that will allow for adjustments to rates on a fortnightly basis. The primary objective is to ensure that road transport operators (e.g. logistics companies) can pass on the higher fuel costs to primary parties.

Examples of primary parties include:

- Manufacturers and suppliers

- Large retailers

- Construction companies.

In this instance, Gamuda would be the primary party in a road transport supply chain for materials delivered to site, for example. Previous costing locked in would have to be adjusted to reflect the higher prices. Critically, this does not allow Gamuda to pass on costs to the project principal, since Gamuda is only providing construction and engineering services.

Australia insolvencies: construction sector leads

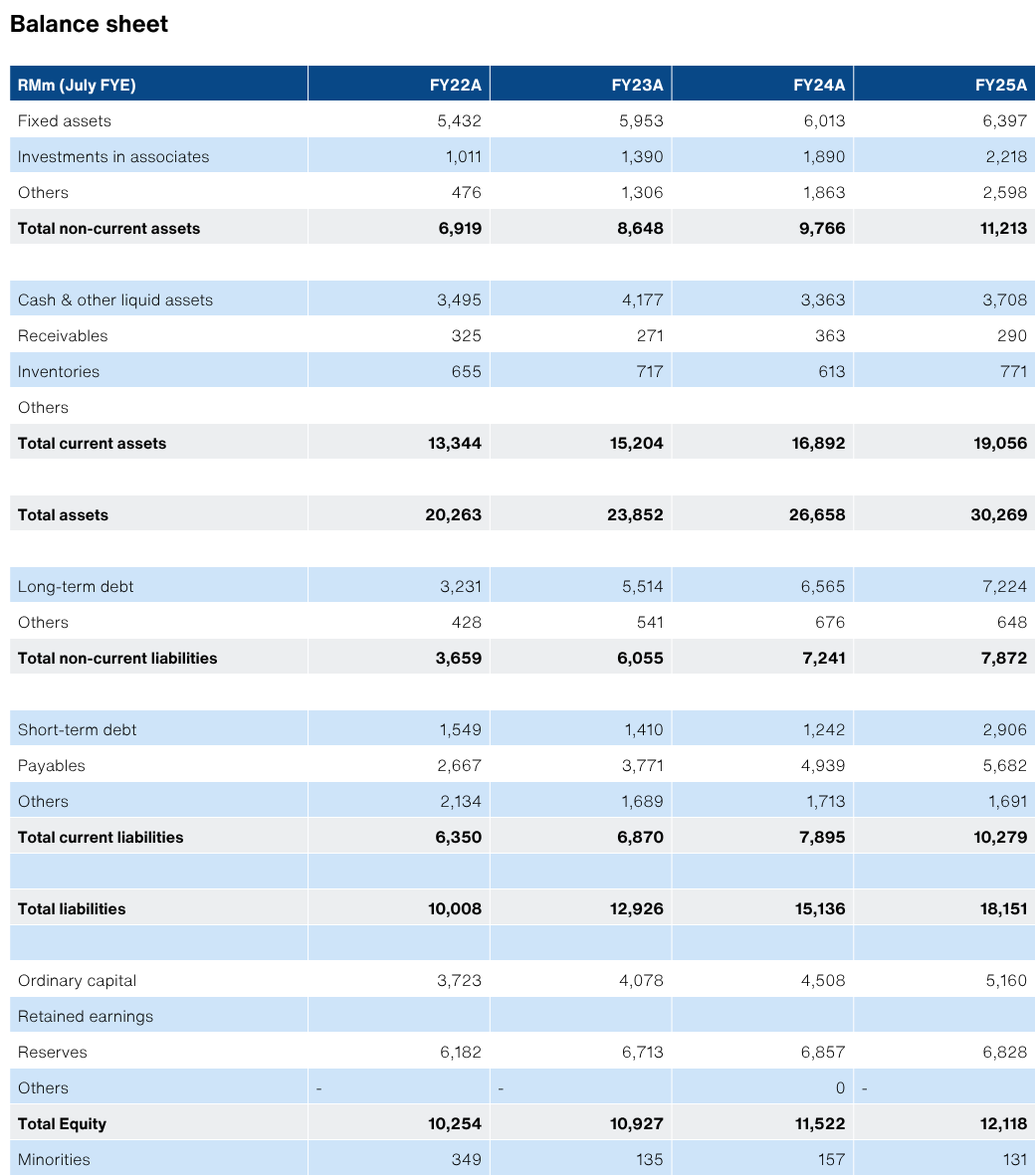

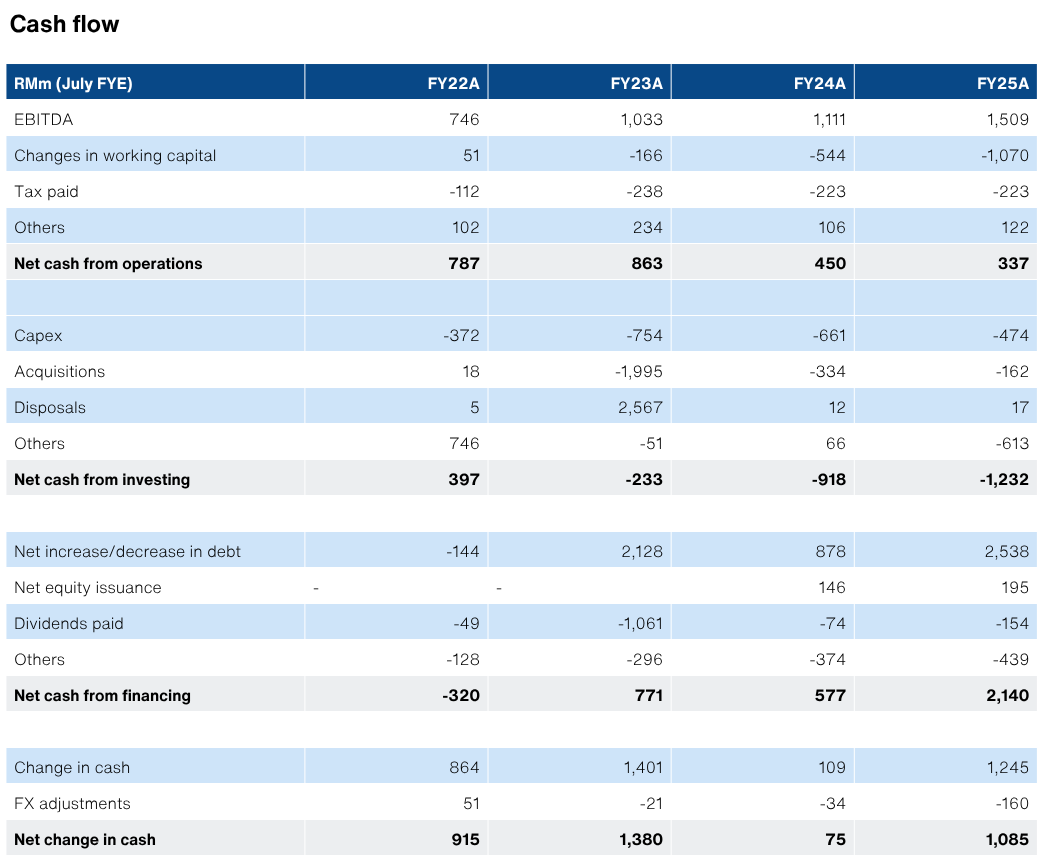

Selected financials

Source: Bloomberg, NewParadigm Research, April 2026