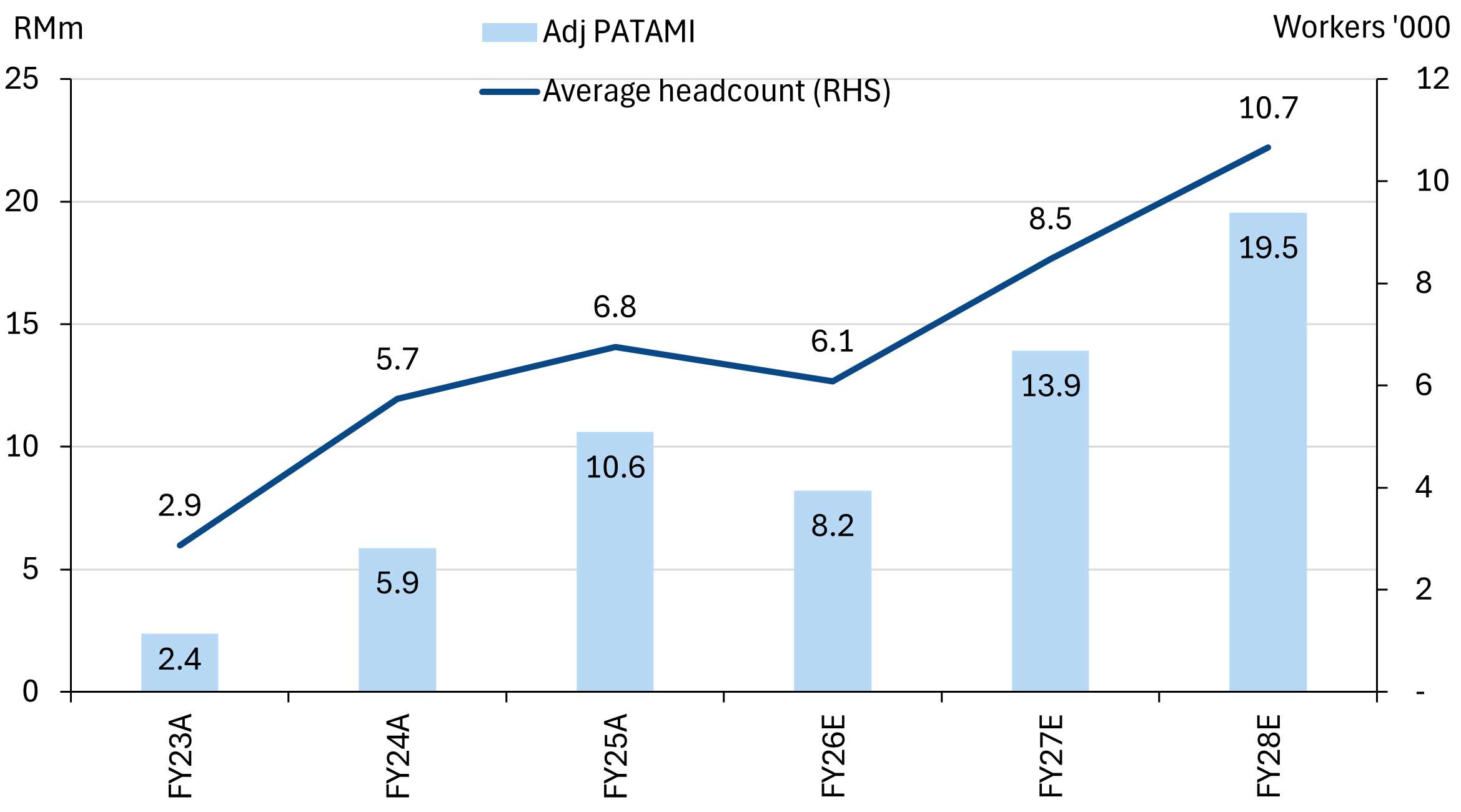

Headcount-led growth

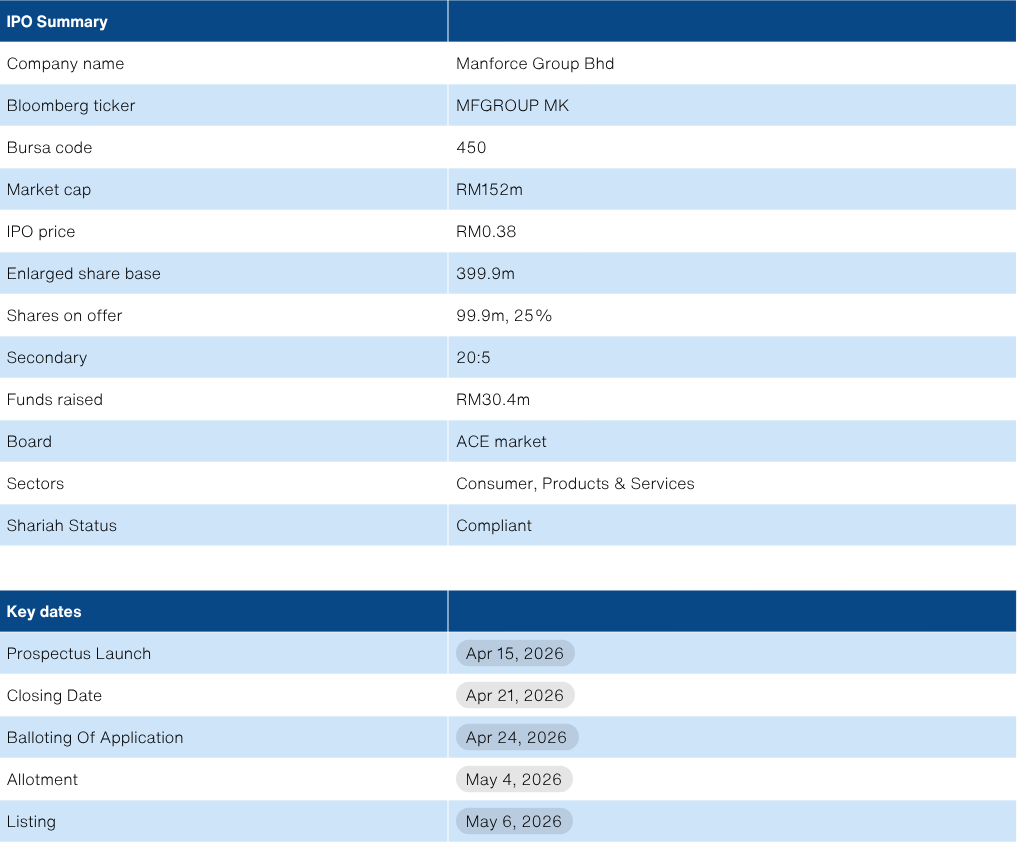

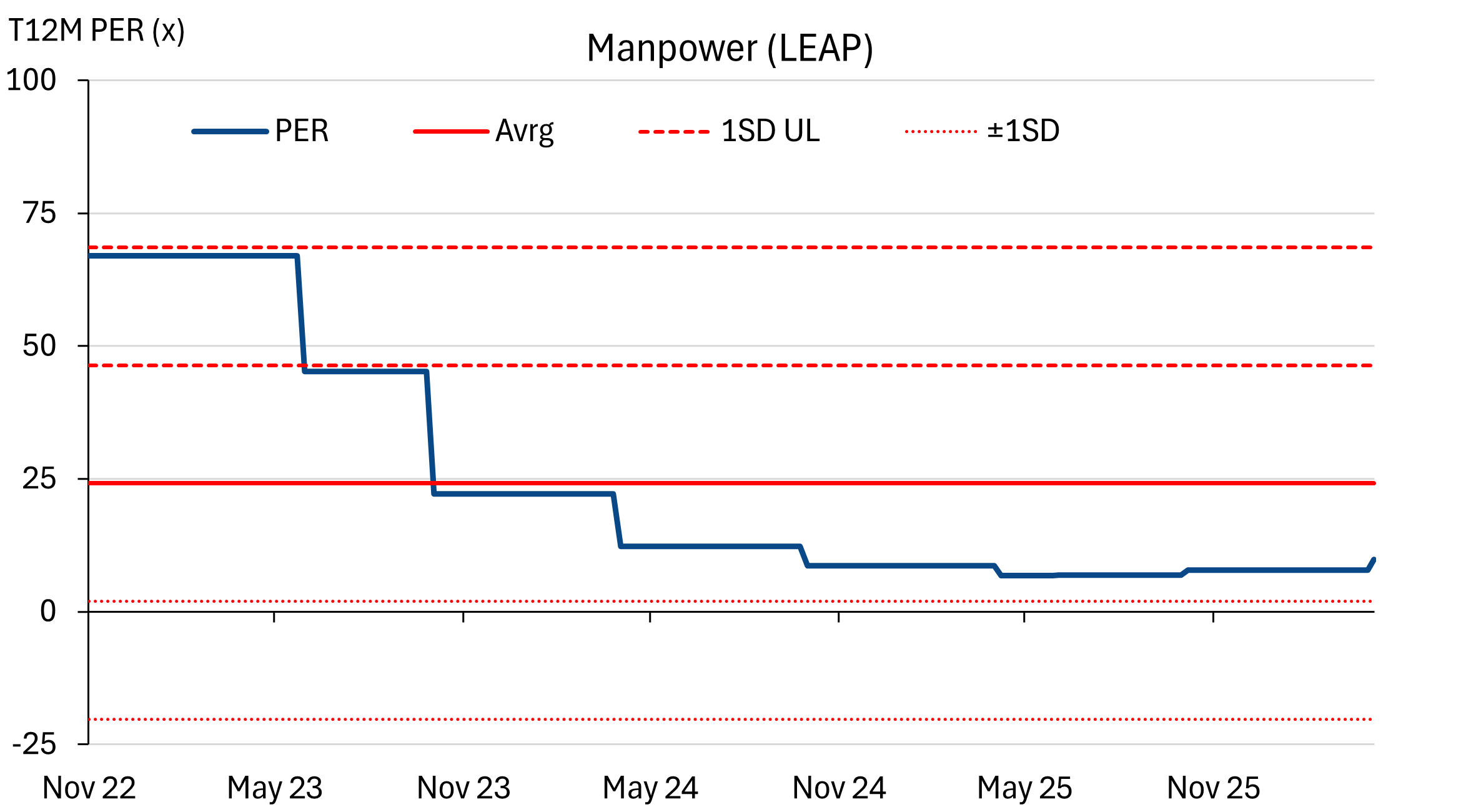

Manforce is moving up from the LEAP to the ACE market on 6 May.

MANFORCE GROUP

MFGROUP | 0450.KL

BUY

Target price: RM0.48

IPO price: RM0.38

Market cap (RMm): RM152m

Primary:Secondary offering: 20:5

IPO shares/total shares: 99.9m / 399.9m

Funds raised: RM30.4m

Float: 25%

Disclaimer: By using this information, you acknowledge that you are solely responsible for evaluating the merits and risks of any investment decision and agree not to hold NewParadigm Research liable for any damages arising from such decisions.

Key takeaways

- We estimate +23% NP CAGR (FY25-28) that is underpinned by sizable 10k foreign worker application funnel.

- We have assumed 60% approval rate, with 10% attrition; headcount should grow from ~6.1k to ~10.7k by FY28 (ended-Feb).

- IPO price implies only 11x FY27 PER. At 14x PER, our TP is RM0.48 and implies +26% upside.

NP vs worker headcount

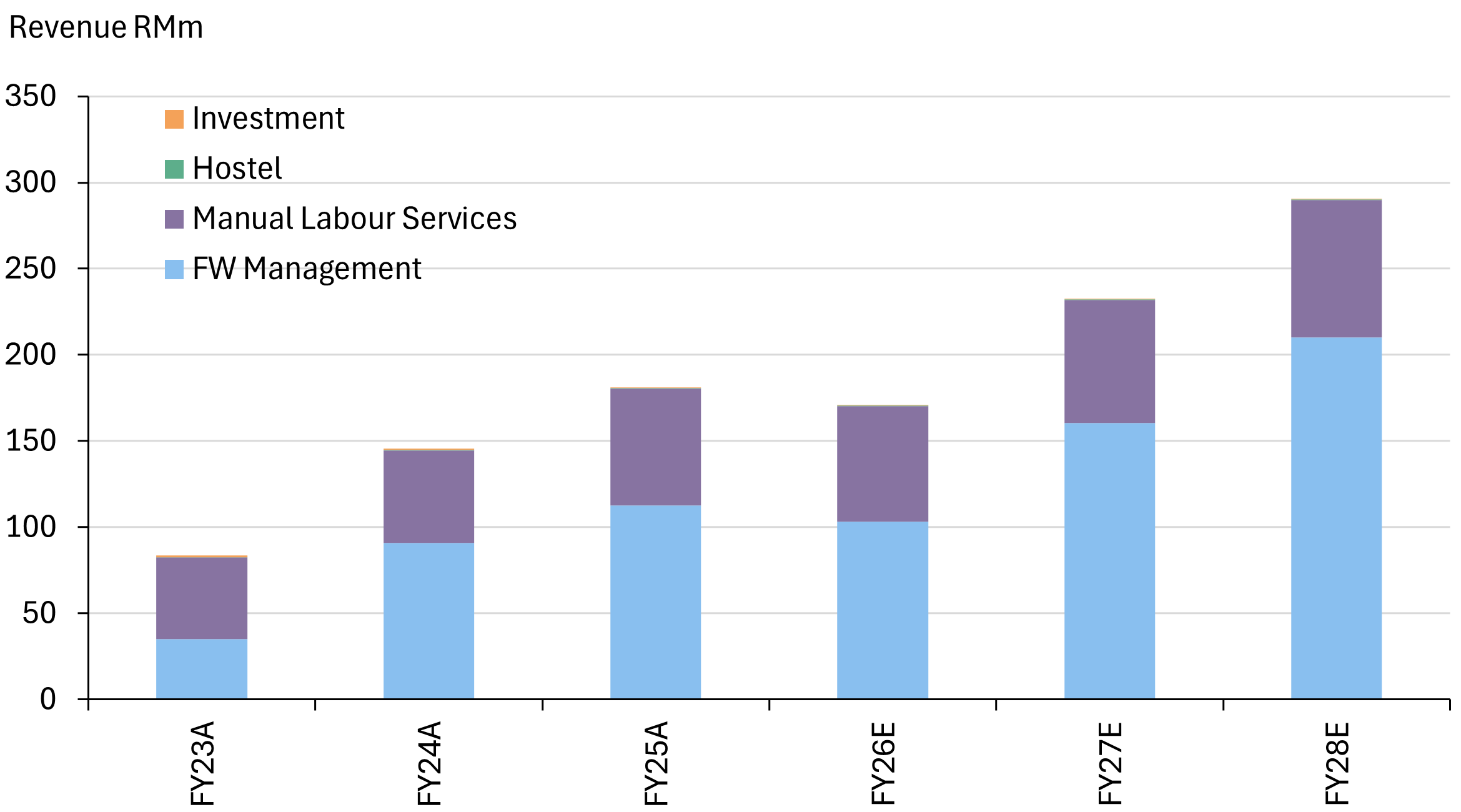

| RMm (end-Feb) | FY25A | FY26E | FY27E | FY28E |

|---|---|---|---|---|

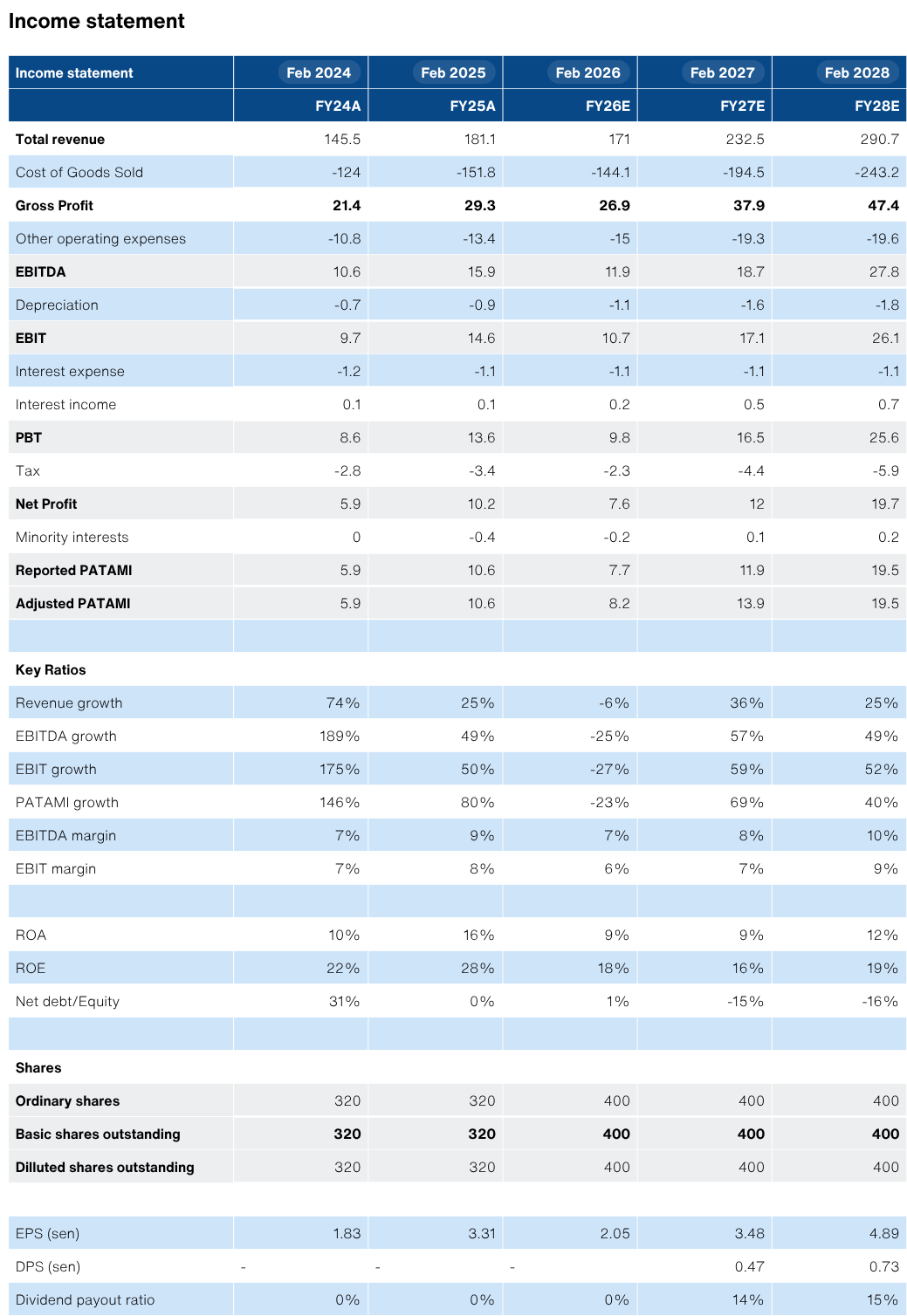

| Revenue | 181 | 171 | 232 | 291 |

| Revenue Growth | 25% | -6% | 36% | 25% |

| EBITDA | 15.9 | 11.9 | 18.7 | 27.8 |

| EBITDA margin | 9% | 7% | 8% | 10% |

| Adj PATAMI | 10.6 | 8.2 | 13.9 | 19.5 |

| Adj NP margin | 5.9% | 4.8% | 6.0% | 6.7% |

| ROA | 16% | 10% | 11% | 12% |

| ROE | 29% | 18% | 16% | 19% |

| PER | 14.3 | 18.5 | 10.9 | 7.8 |

| P/BV | 4.1 | 3.4 | 1.8 | 1.5 |

| Yield | 0% | 0% | 0% | 2% |

Source: Company data, NewParadigm Research, May 2026

Leveraging demand for foreign workers

- Manforce operates a unique business model of managing foreign workers for clients, in addition to direct labour services. Recruitment is outsourced and quota’s/employment are linked to the clients themselves. Manforce instead focuses on generating predictable recurring income from the provision of services to clients and their foreign workers. Key sectors are services, manufacturing and construction. Key customers include The Food Purveyor (Village Grocer), Supermax, and Panasonic.

- This results in stable earnings floor for existing headcount. Looking ahead, the recent foreign worker quota application window provides the growth runway for FY27/28E. Manforce has a funnel of 10k applications (1k own, 9k client). Assuming a blended 60% approval rate (historic: 60-80%), this should underpin growth for the next two years - pending physical arrival of workers.

- Focus should be on the gross profit line, as payrolls (sometimes not included) can distort the topline. Manforce averages a gross profit of RM300-400/worker/month with the FY26E (ended-Feb) average headcount of 6,088.

- This business model creates a natural incentive for Manforce to keep workers satisfied and happy in order to minimise costly attrition.

- The business model is also unique as it is supply-limited, rather than demand-driven. Foreign worker quotas and poor participation of domestic labour has created a sizable shortage in the related roles/sectors that Manforce addresses. In other words, there is ample demand. Policy direction remains the biggest long-term risk, but we don’t see practical solutions to addressing the foreign labour dependency.

Initiate with a BUY

- We initiate coverage on Manforce with a RM0.48 target price and a BUY recommendation.

- We estimate a NP CAGR of +23% (FY25-28E), driven by the current cycle of foreign worker applications. Against this, we apply a PER target of 14x which is >0.5x PEG. For reference, the current weighted average PER of the peers are 14.4x (12MBF) and the historic weighted average is even higher: 15.6x.

- Our bull case valuation is RM0.60, assuming an additional 1.5k approvals and a higher target multiple of 15x.

About the Company

Manforce Group Berhad (MFGROUP) operates two core segments:

- Foreign worker management services whereby the group manages foreign workers on behalf of clients covering accommodation, transportation, insurance, payroll and government related levies.

- Manual labour services whereby the group directly employs and deploys its own workers primarily for cleaning and manufacturing related services, and hostel management services catering to workers from other companies.

About the Stock

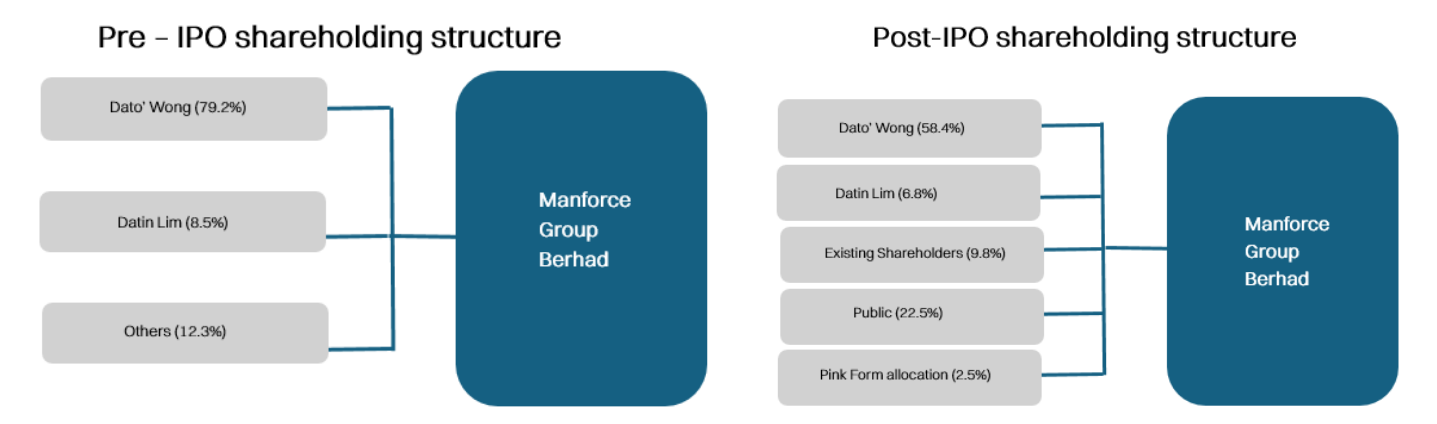

Incorporated in Malaysia on 26 April 2017, Manforce Group Berhad was initially listed on the LEAP Market on 11 December 2018 before undertaking its subsequent uplisting to the ACE Market. The company is Shariah compliant and falls under the consumer services sector on Bursa Malaysia. Upon completion of its ACE Market IPO, newly issued primary shares represent 20% of the enlarged share base while the offer for sale by the founder represents 5%. Post-listing, the two principal shareholders Datuk Wong and Datin Lim will retain 58.4% and 6.8% respectively.

Investment Thesis

Manforce’s existing earnings has a high floor, riding on existing worker headcount and contracts that range from 1-3 years. Meanwhile, growth is driven by new foreign worker quota approvals and Manforce has a funnel of 10k applications for the current cycle. Assuming a 60% approval rate, this should drive NP growth to +23% CAGR (FY25-28E, ended Feb).

Against this outlook, the IPO price of RM0.38 implies a relatively low multiple of 11x FY27 PER. At 14x PER (>0.5x PEG), our target price is RM0.48.

Key Risks

- Approval rates: The primary risk for Manforce would be lower-than-expected quota approvals. Note that quotas are applied by customers (foreign worker management, FWM) and historically ranged from 60-80%. While the process is supposed to be quantitative and needs-based, the broader policy landscape has been moving to curtail total foreign worker intakes. Failure to secure the 60% blended approval rate we have assumed would be the key risk to our thesis.

- Attrition: We have assumed a net attrition rate of 10% which is in-line with the historic average. Manforce is naturally aligned to minimize attrition, since it increases costs both for Manforce and the client. In turn, Manforce is incentivized to keep workers happy and satisfied with working conditions.

- Marketing agents: Securing new customers and maintaining existing relationships, and any underperformance or termination of services by these agents could materially impair the group's ability to sustain and grow its customer base, as replacing them with equally effective representatives cannot be guaranteed.

- Foreign partners: The group relies heavily on its foreign partners to source and recruit workers from overseas and given that these partners operate within their respective source countries, any regulatory changes, economic instability or supply chain disruptions in those markets could compromise their ability to deliver a sufficient and consistent pipeline of workers to meet client demand.

IPO Summary

IPO Structure

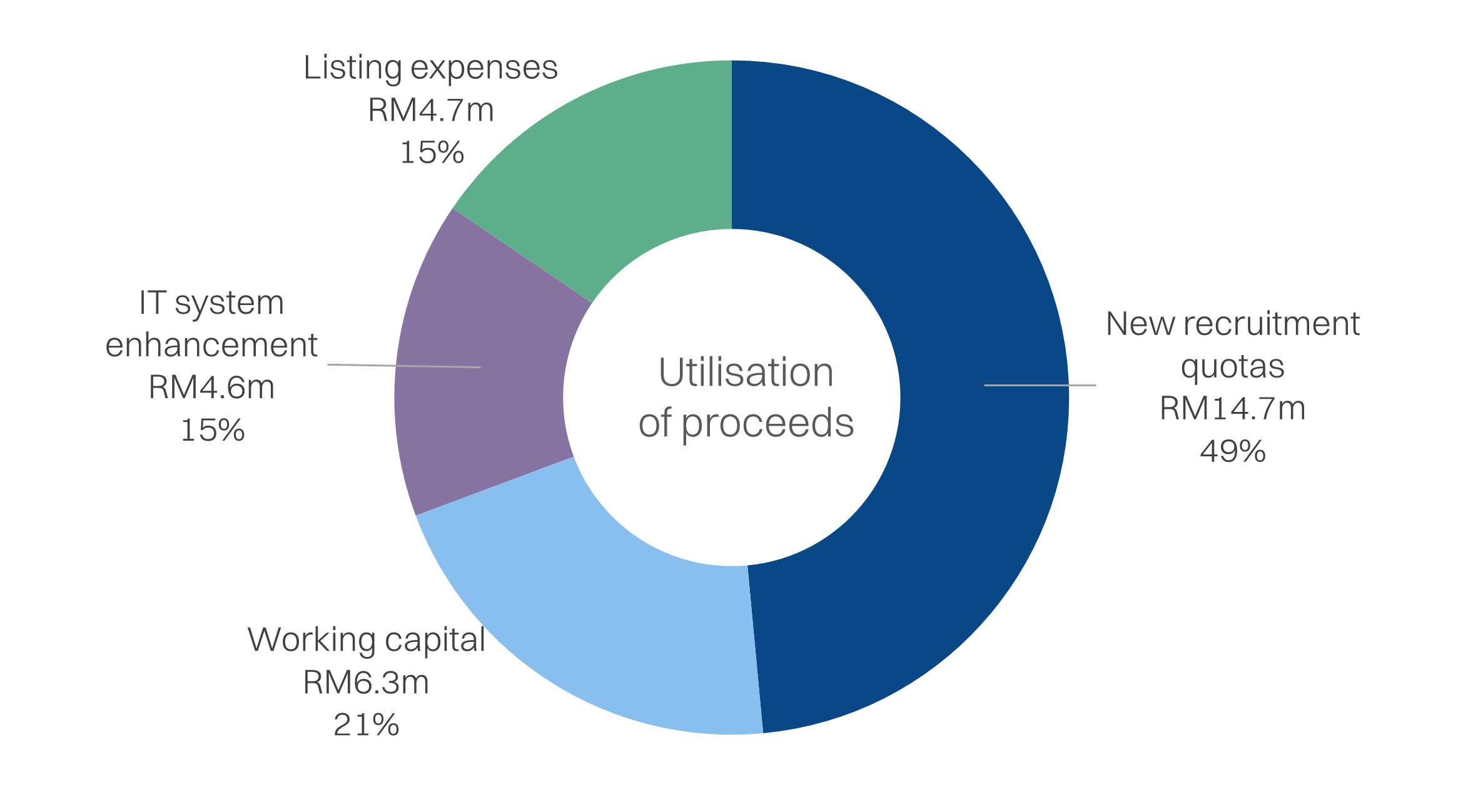

IPO: Utilisation of proceeds

MFGROUP will raise RM30.4m from the IPO for which close to 50% of this would go towards supporting earnings growth;

Business expansion through recruitment (48.5%): The bulk of Manforce's IPO proceeds is allocated towards business expansion through new recruitment quotas, targeting the addition of 5,000 workers under customer quotas and 1,000 workers under the group's own manual labour quota, with mandatory compliance costs covering FOMEMA, insurance and SKHPPA expenses for the combined 6,000 workers.

Working capital (20.8%): Manforce has allocated RM6.3m towards salaries and accommodation setup for the additional 1,000 foreign workers under the manual labour services segment. This will cover two months of salaries at the prevailing minimum wage of RM1,700 per worker as well as furnishing, utilities, renovation and waste management costs for worker accommodations to be arranged through lease agreements in either rented properties or CLQs depending on customer needs and proximity to work sites.

Enhancement of IT system (15.3%): Manforce has allocated RM4.64m for enhancing its IT and operational systems across three initiatives:

- The development of SmartApp, an integrated mobile platform consolidating worker tracking and payroll into a single application featuring AI powered assistance,

- E-wallet, remittance services and hostel management tools.

- The development of a proprietary CLQ management system to streamline worker administration and facility operations within CLQ facilities as government policy increasingly favours purpose-built accommodation, and the purchase of laptops and software licensing to improve operational efficiency.

Listing expenses (15.4%): Manforce has set aside RM4.70m to cover its listing expenses, with any shortfall to be funded from the working capital allocation.

Utilisation of proceeds

Pathway to double earnings by FY28E

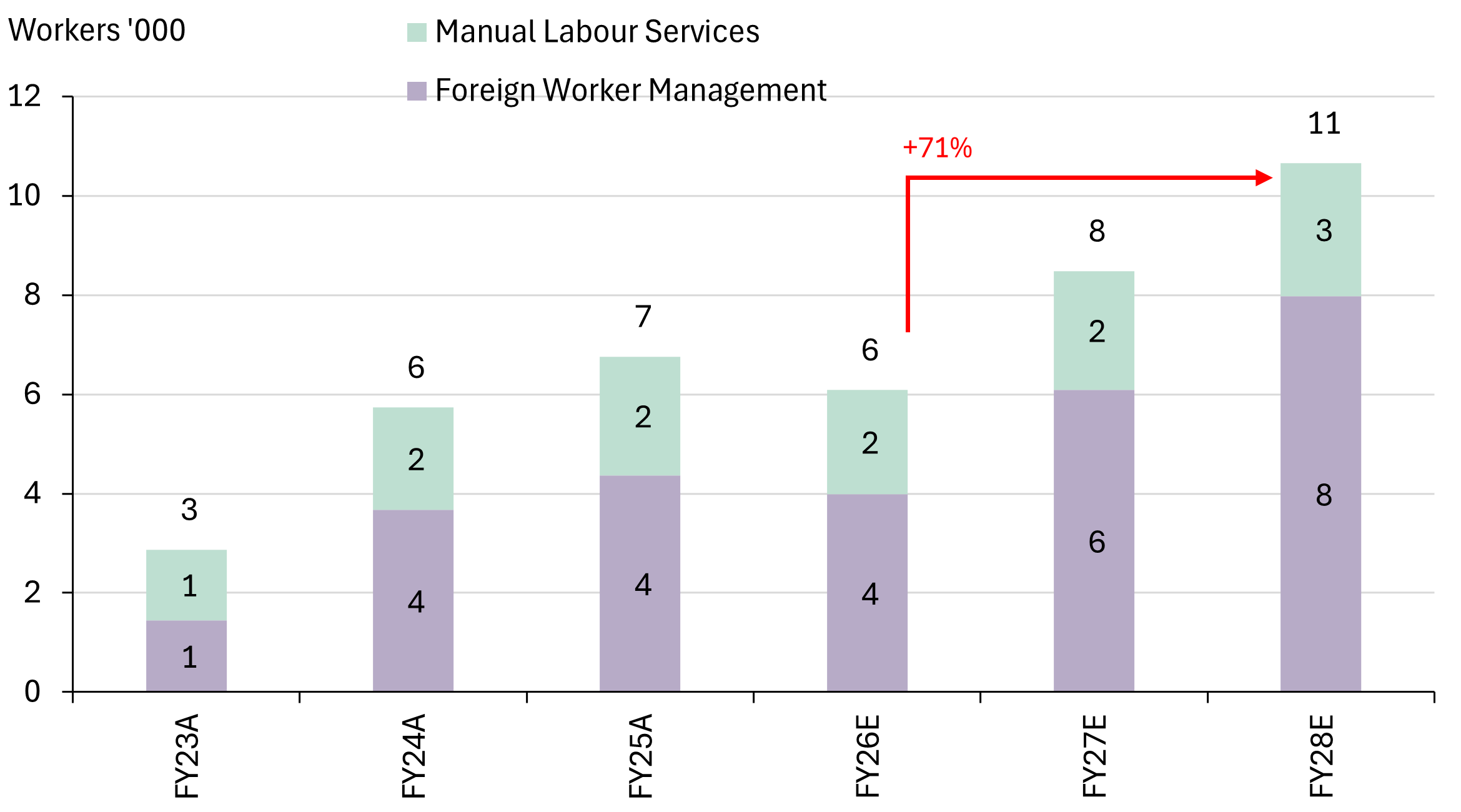

Manforce is aiming to increase headcount under management by +75% by FY28 (ended-Feb), which should drive a corresponding +23% NP CAGR (FY25-28). Against this backdrop, the IPO price of RM0.38 implies a valuation of only 11x FY27E PER.

The company is currently processing ~10k new applications as part of the current foreign worker quota window. Roughly 9k of the applications are for customers under the foreign worker management (FWM) segment as well as 1k for its in-house manual labour services (MLS) segment. Assuming a conservative conversion ratio of only 58% for the FWM segment and 80% for the MLS segment, Manforce would be able to expand its headcount under management from the FY26 average of 6.1k to >10k by FY28.

Note that the growth is driven by both an expansion of foreign worker requirements by existing customers, as well as the expansion of the customer base. Additionally, Manforce’s headcount should be supply-limited rather than demand-driven, given the broader shortage of foreign workers. Anecdotally, for applications that have already been approved, approval rates have been between 60-80%.

Recall, foreign worker applications have been frozen since 2023, which is why Manforce’s headcount growth stagnated in FY24-25. For context, MoHR indicated foreign worker numbers fell by -13% YoY as of Oct 2025 (link). The application window was reopened in January this year. Initially it was supposed to close by end-March, but it has since been extended.

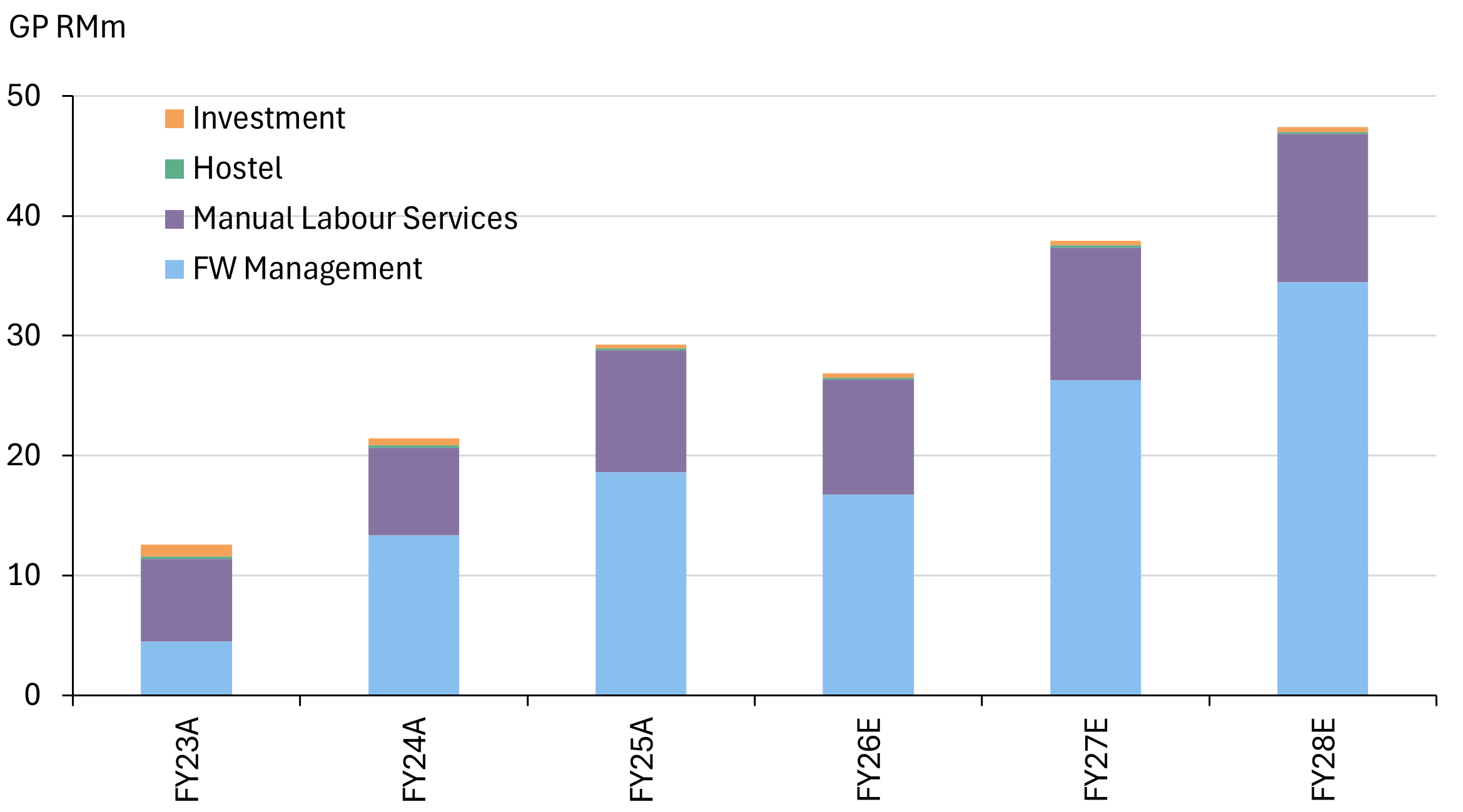

The business has fairly linear margins, since most costs are pass-through. Historically, Manforce has averaged RM300-400/headcount/month, across both the FWM and MLS segments. Thus, while headline GP margins look relatively thin at 15-16%, excluding payrolls, Manforce has an implied ex-payroll GP margin of 40-50%.

Furthermore, this is an asset-light business. Manforce has less than RM1m in fixed assets on its books, opting to lease most of its hostel requirements. In turn the group has booked a healthy double digit return on assets and ROE’s reaching 29% pre-IPO. We estimate post-IPO ROE’s will be >16% for FY27E.

Estimated headcount growth trajectory

Primary operating segment - foreign worker management services

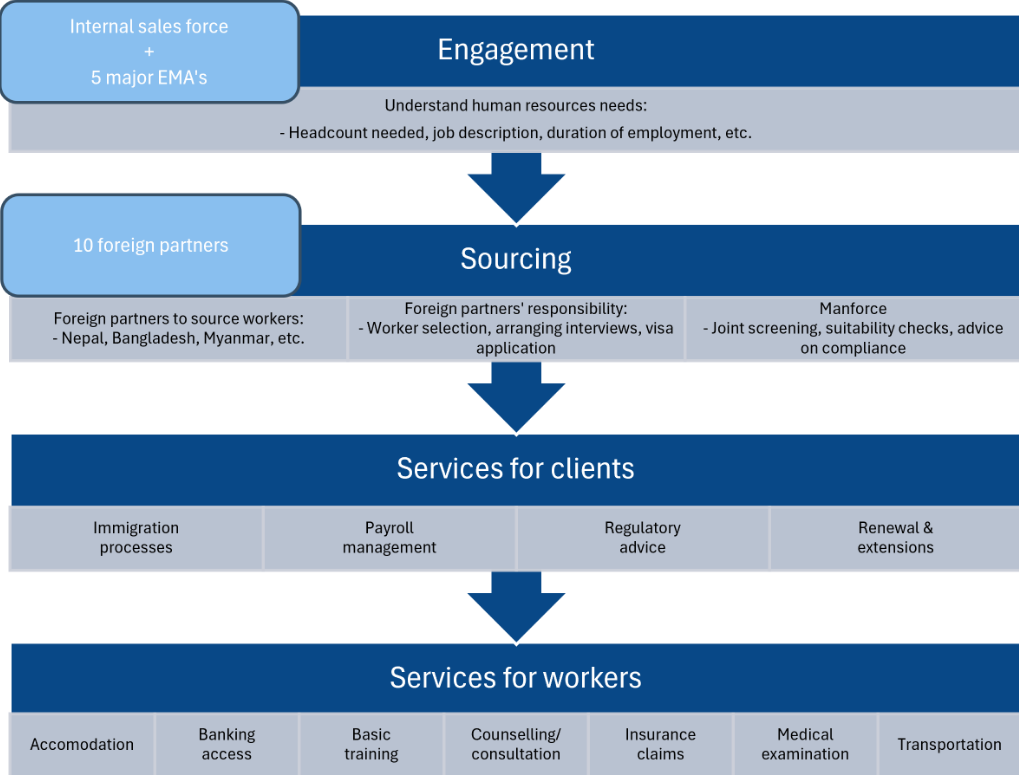

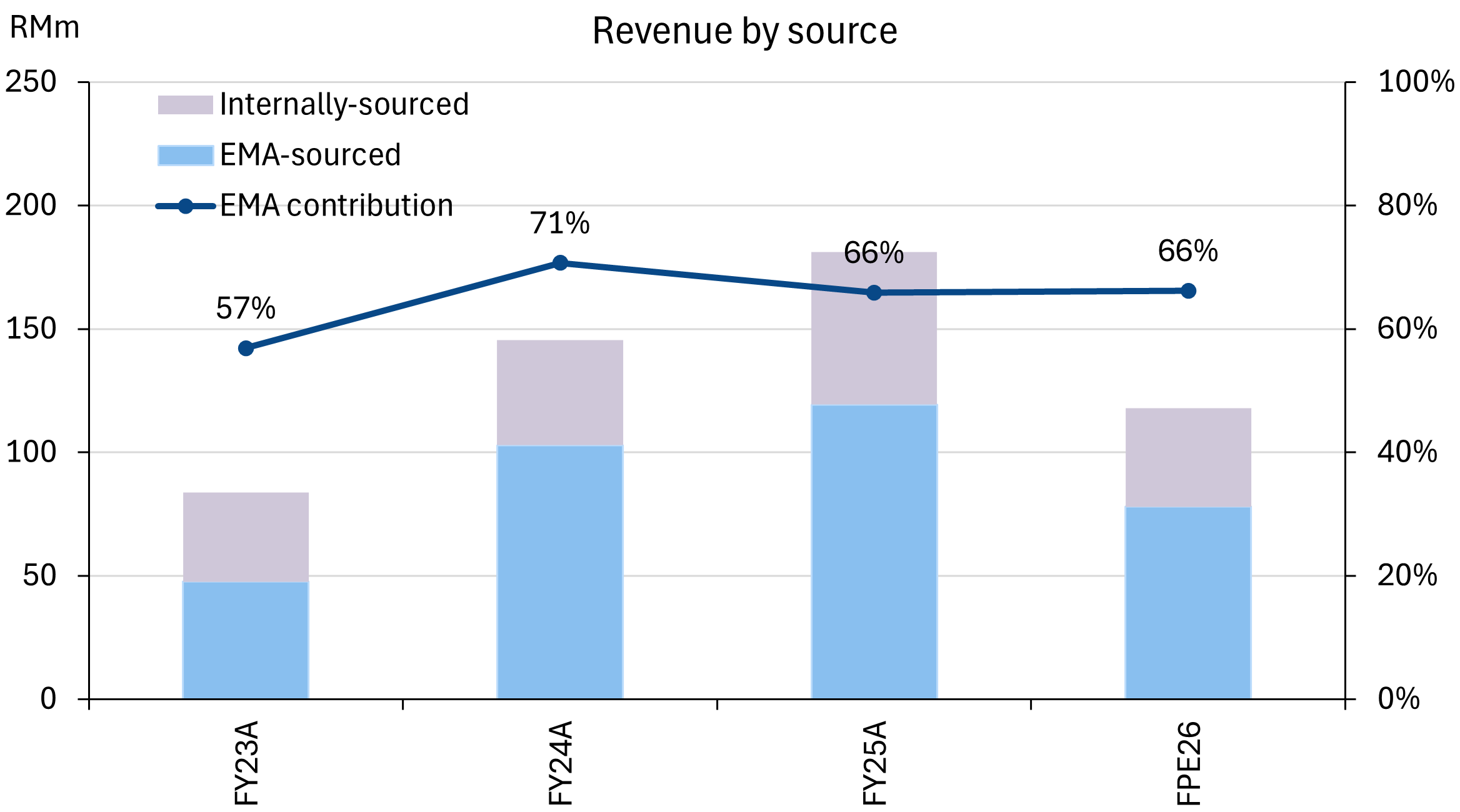

Manforce’s main segment is foreign worker management services, which contributes roughly 60% of gross profits. Manforce leverages 5 major exclusive marketing agents (EMAs) that have historically sourced >66% of revenues for the group. The balance comes from internal sales force.

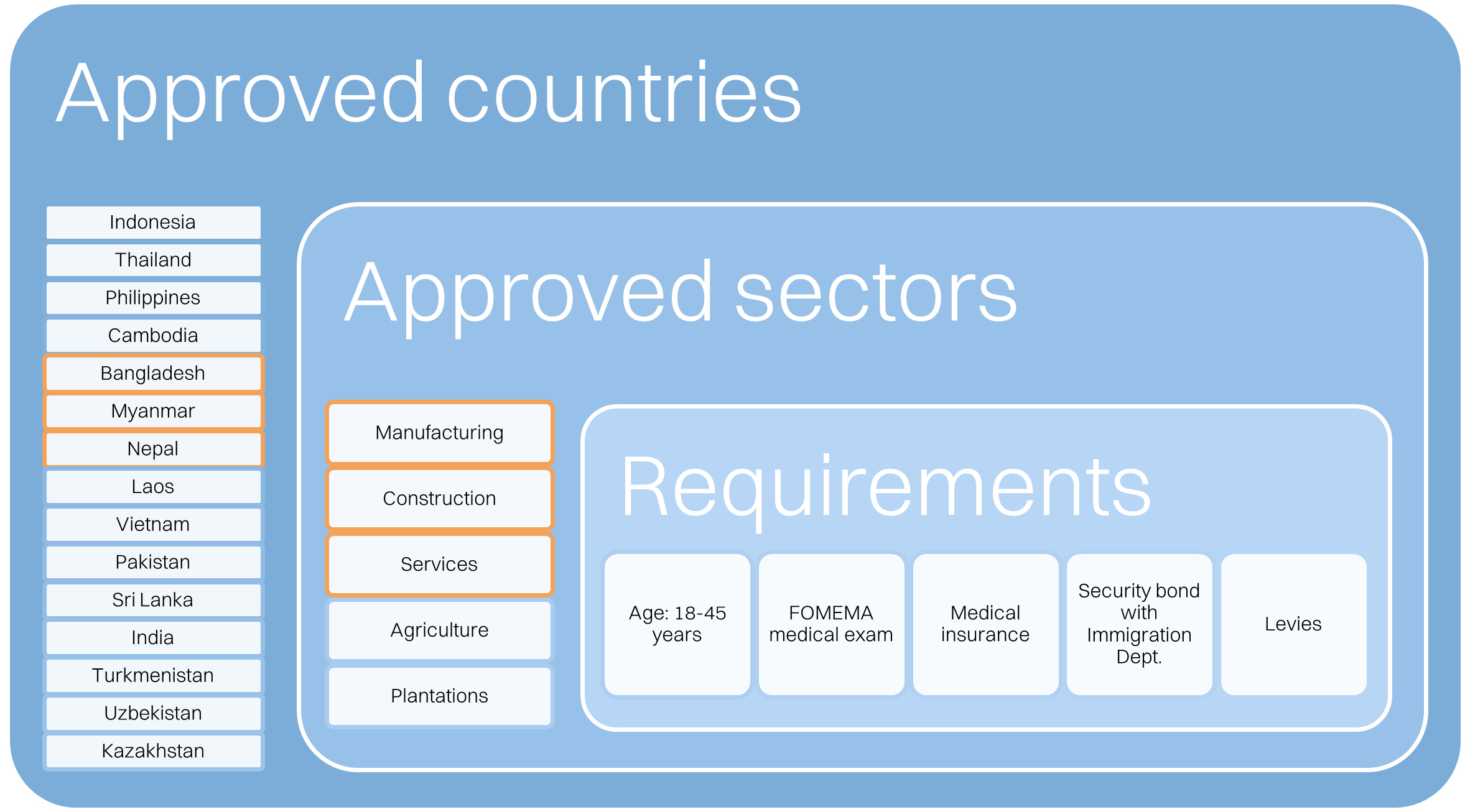

Critically, Manforce does not undertake recruitment directly, but connects clients with 10 foreign partners across Nepal, Bangladesh and Myanmar to source workers. Manforce does aid with screening and advise on immigration and regulatory matters. Another key distinction of the business model, is that the workers are directly employed by Manforce’s clients. Thus, the foreign worker quotas are held by the clients as well. This substantially minimises the potential liability in Manforce’s operating model.

The core recurring income however, comes from the provision of services - both for the foreign workers as well as the clients. This ranges from providing accommodation and transportation requirements for the workers, to processing insurance claims and managing workers’ welfare issues. In fact, Manforce provides an app for workers to use, to access basic services as well as seek help if there are any issues.

In turn, the key focus of the group is to minimise churn. Management indicated that attrition has historically been less than 20%. Over the past year, with the quota freeze, attrition was only ~10%. The key is an emphasis on ensuring good fit for the job as well as worker satisfaction and happiness. For the clients, this translates to lower costs and better productivity - particularly from reduced re-training associated with new workers as well as productivity losses.

Workers come in on an initial 2year contract and are subsequently allowed an extension of up to 10 years. Coupled with the three-year contract with clients, the earnings of Manforce should be seen as relatively sticky and recurring in nature. Revenue is not a good indicator for this segment, payroll may or may not be included. GP is a better indicator to track, and works out to RM300-360/work/month. We have assumed an additional 5,000 headcount by FY27E, with a 10% attrition rate.

Foreign worker management overview

Second core segment - Manual labour services

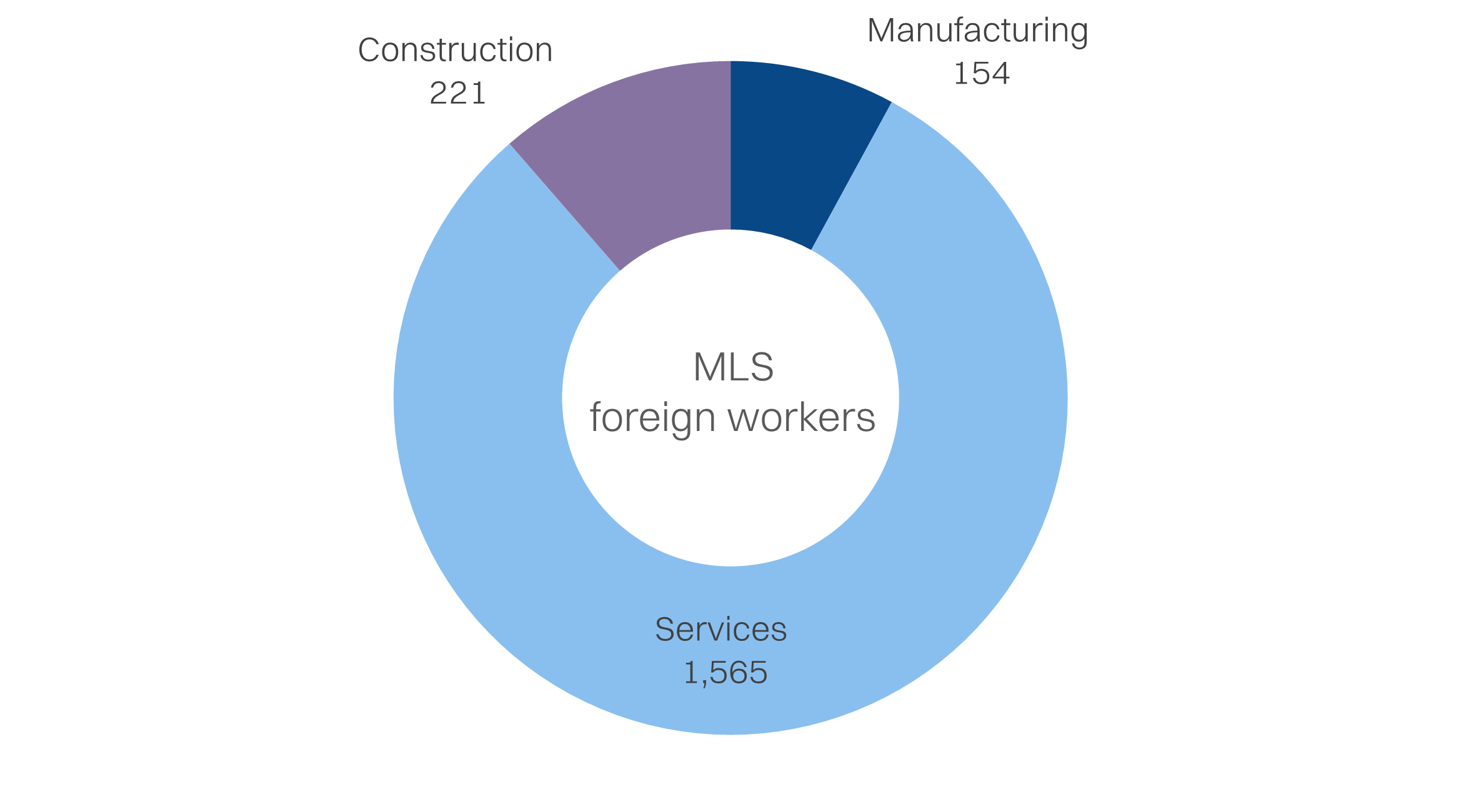

The second largest segment for the group is the manual labour services. Manforce directly employs both local and foreign workers (primarily foreign) to provide cleaning, sanitising, manufacturing and construction-related activities. The foreign workers are hired under the group’s own recruitment quota’s.

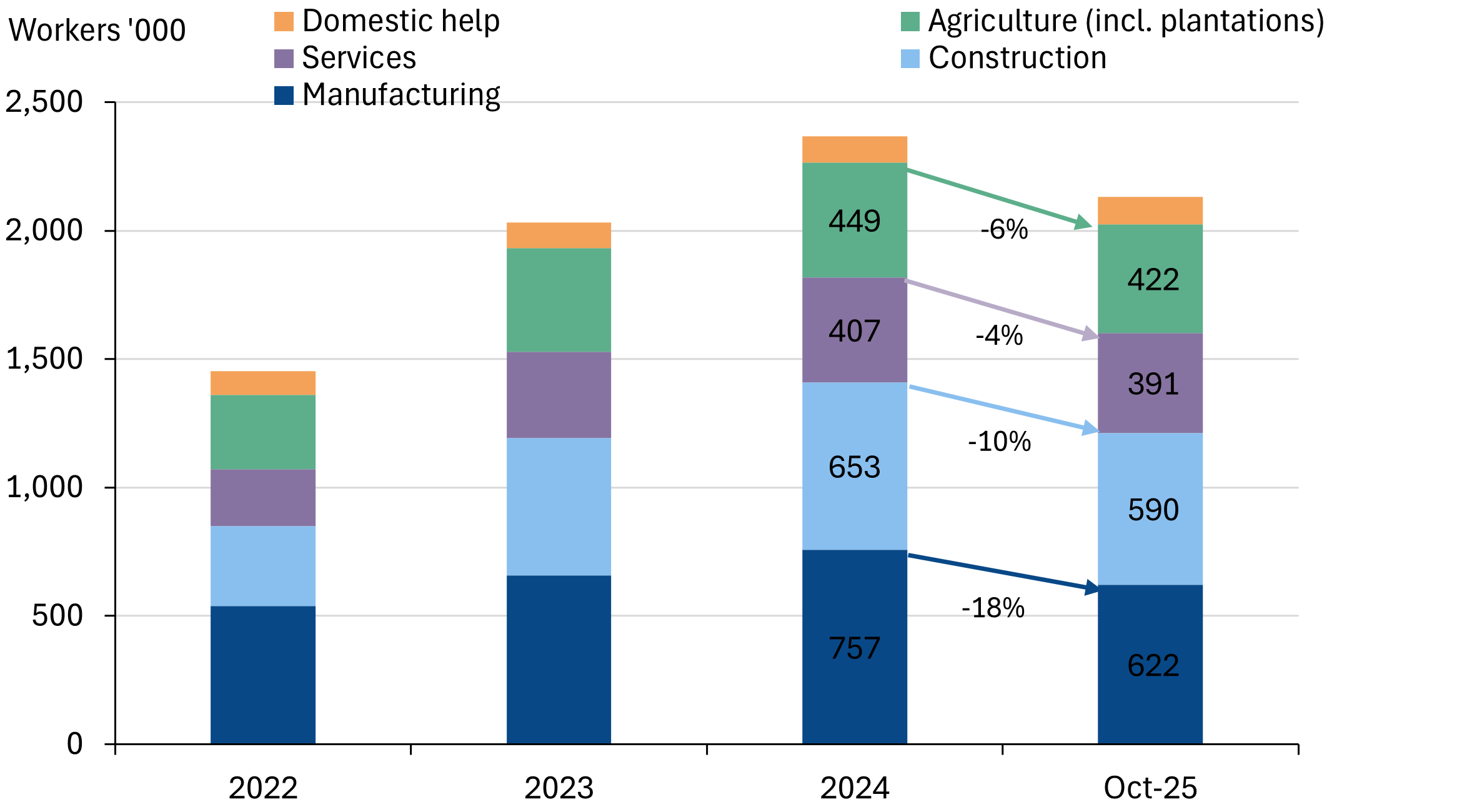

As of the prospectus, the group has fully utilized its quota and manages 1,940 foreign workers. The primary sector of focus is services - primarily cleaning and sanitisation. This includes high-rise facade and internal cleaning, initial cleaning and post-construction cleaning.

Contracts for this segment are at least 1-year in length. We do not see much risk of underutilisation in this segment, given the broader shortage of foreign workers. This segment also commands higher margins, with an average GP of RM350/worker/month, and is generally higher than the FWM segment.

However, growth for this segment is directly limited by the amount of quota that is approved by the Ministry of Home Affairs (MOHA). As part of the current application cycle, Manforce is applying for 1,000 headcount. For our modelling we have assumed an 80% approval rate, with a lower attrition rate of 5%.

MLS breakdown by sector

Segmental breakdown

Manforce has two more small segments that are relatively negligible for the group:

- Hostel management services: operating and managing hostels housing customers' foreign workers, providing maintenance, repair and security services. It accounted >0.2% of group revenue, but is consistently profitable. There are 77 units under management as of FY24.

- Investment holding/others: Other ancillary services including recruitment services, insurance product sales for foreign workers, and remittance services. Consistently loss-making, reflects a segment that captures unallocated holding company costs. It also houses a leasehold investment property with a negligible carrying amount of RM455k.

Revenue breakdown / Gross profit breakdown

Source: Company data, NewParadigm Research, May 2026

Valuation

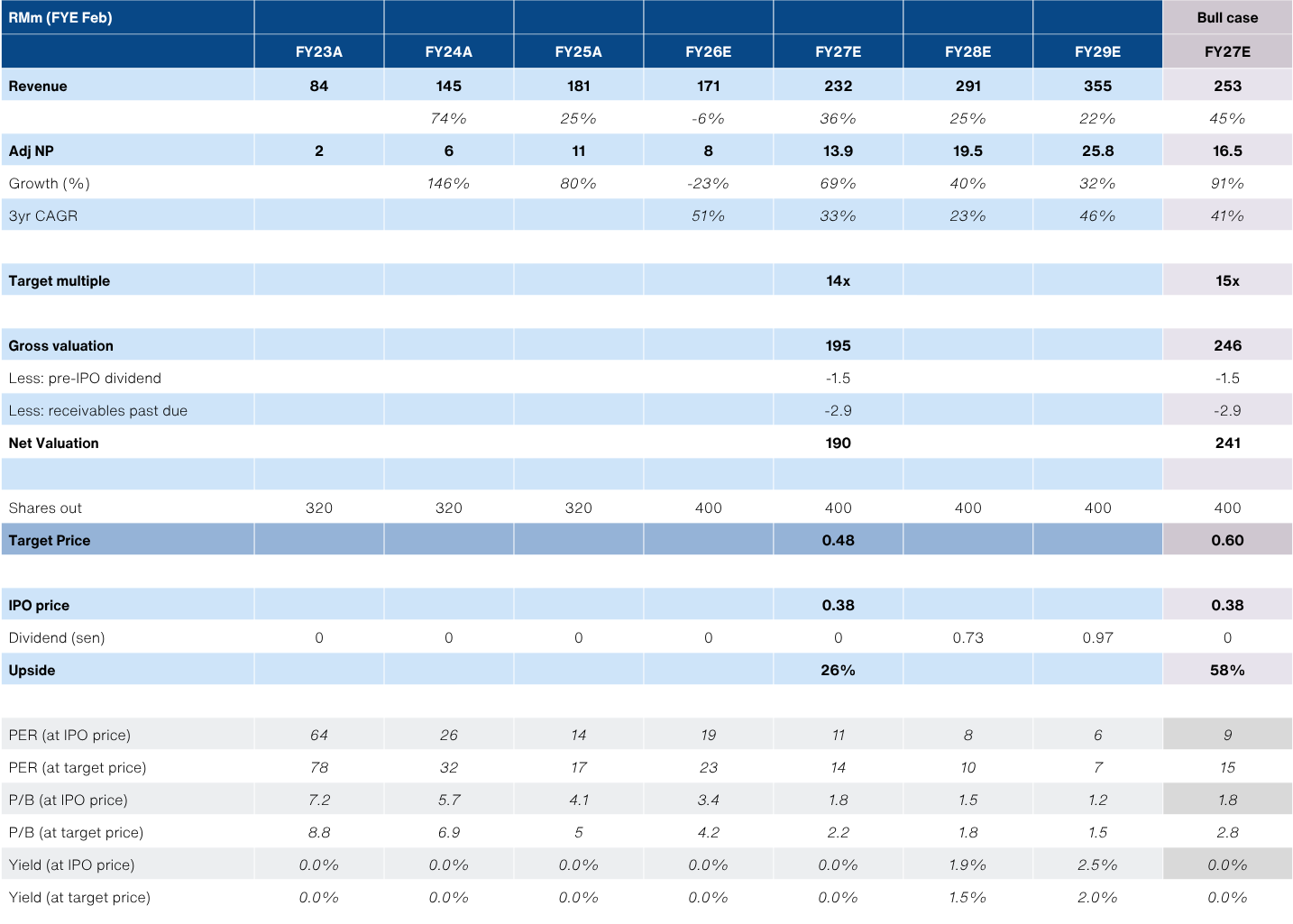

We ascribe a target price of RM0.48/share, based on 14x FY27E (ended-Feb) Adj NP of RM13.9m (+33% 3yr CAGR). This implies a 26% premium to the IPO price of RM0.38.

We have arrived at our Adj NP forecast based on the following key assumptions:

- 58% conversion rate of the 10,000 applications

- +5k headcount under FWM segment and 1k for MLS

- Progressive onboarding over FY27/28, with full recognition only in FY28.

- 10% attrition per year on existing headcount

- Strip out one-off IPO expenses (RM2m).

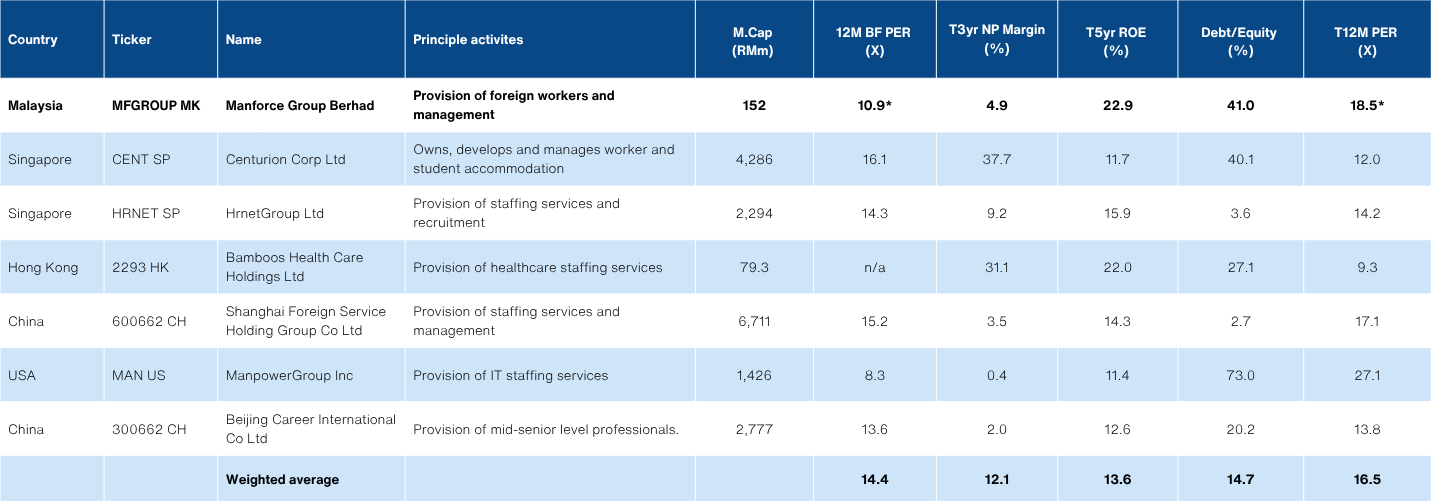

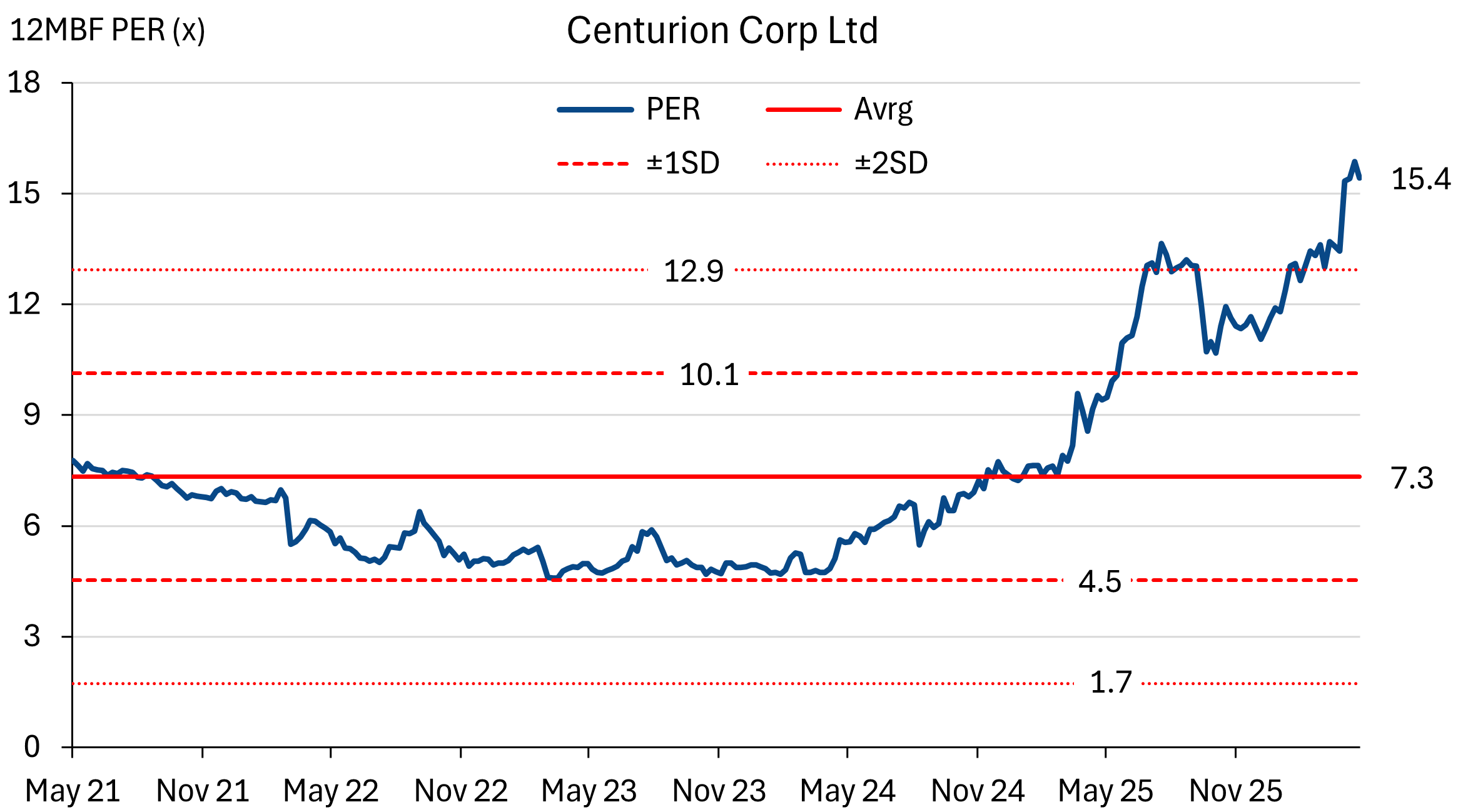

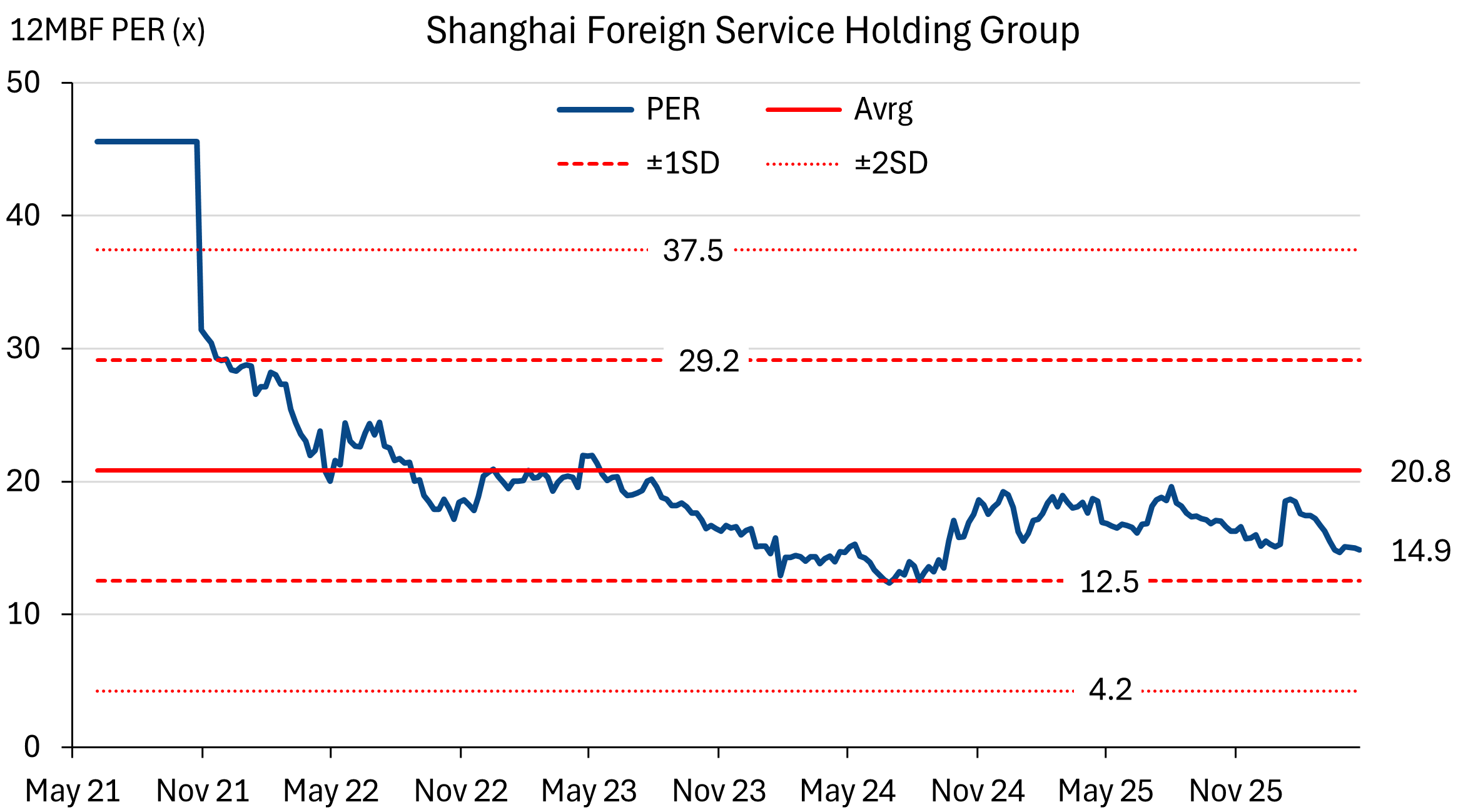

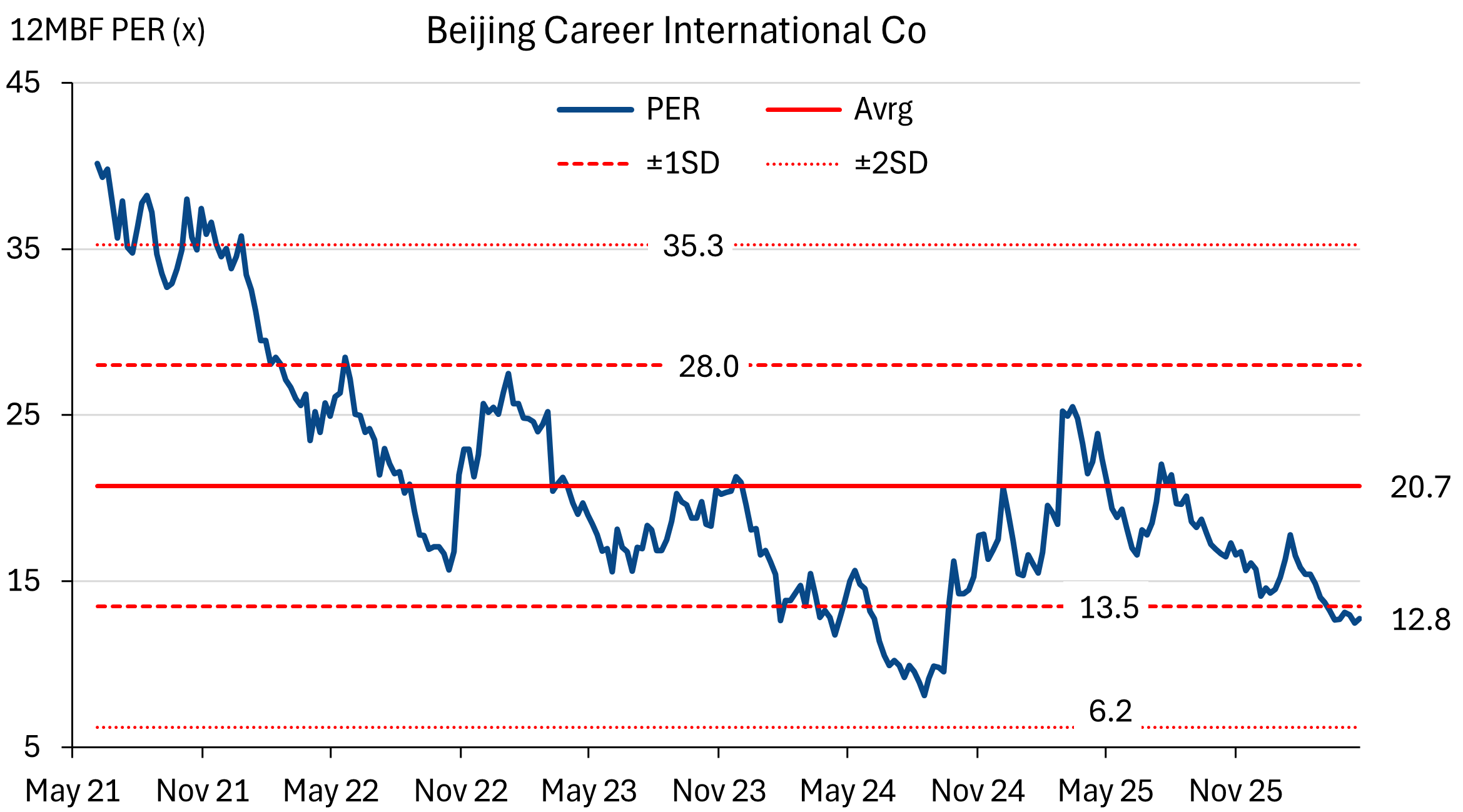

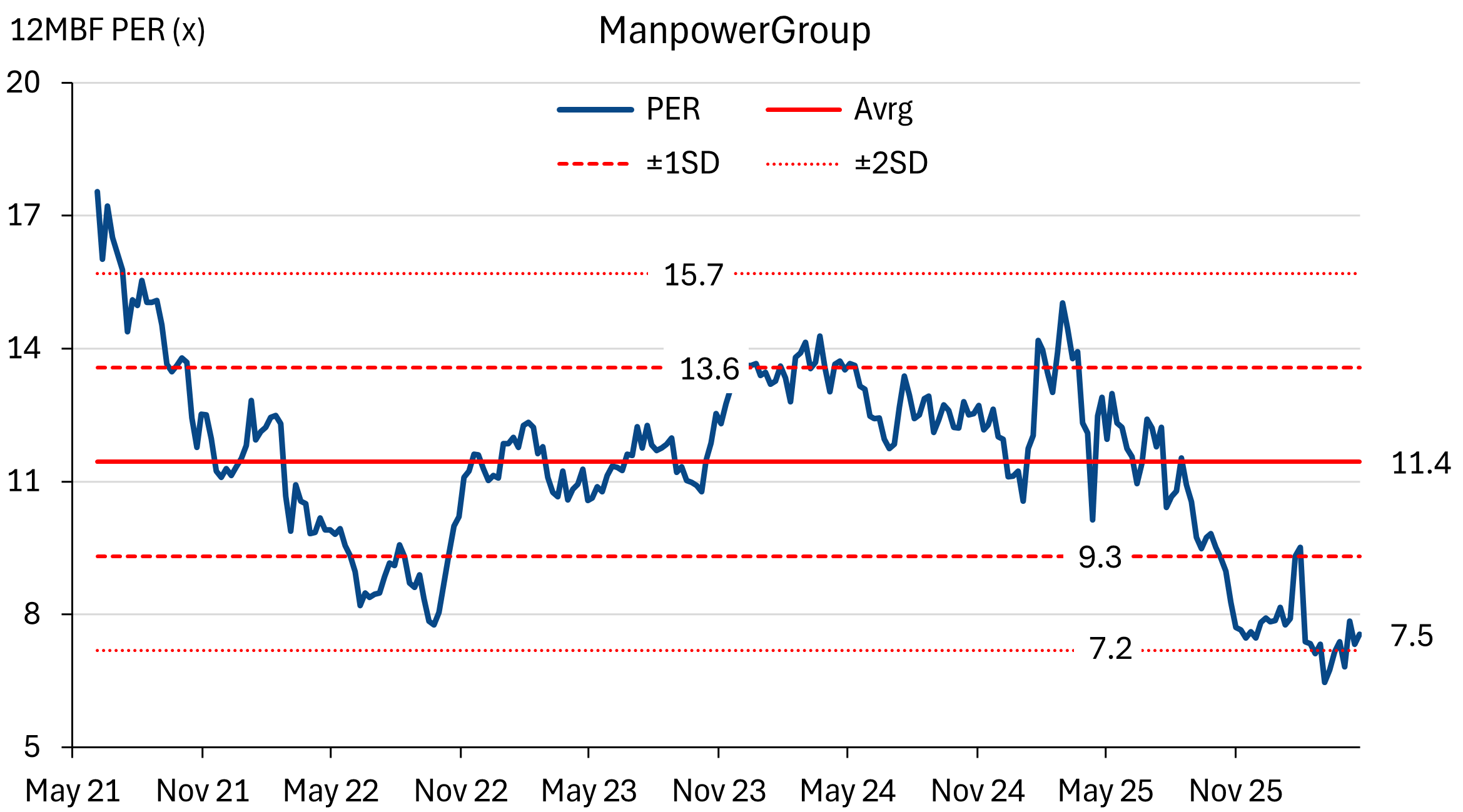

For our valuations, we flag a lack of direct domestic peers for comparison. There are several regional peers, that trade at an average valuation of 14.4x PER (12MBF). We opted for a target multiple of 14x on the basis that Manforce has a Leap Market track record and a reputable client base.

Additionally, our valuations also factor in an RM1.5m dividend payout (pre-IPO) that was paid out on 2 April. We also factored a potential non-cash impairment of RM2.9m for net outstanding receivables that is >90days past due, that is linked to a single construction sector client.

Our bull case valuation assumes an additional 1,500 headcount and a higher multiple of 15x.

Valuation table

Peers' comparison

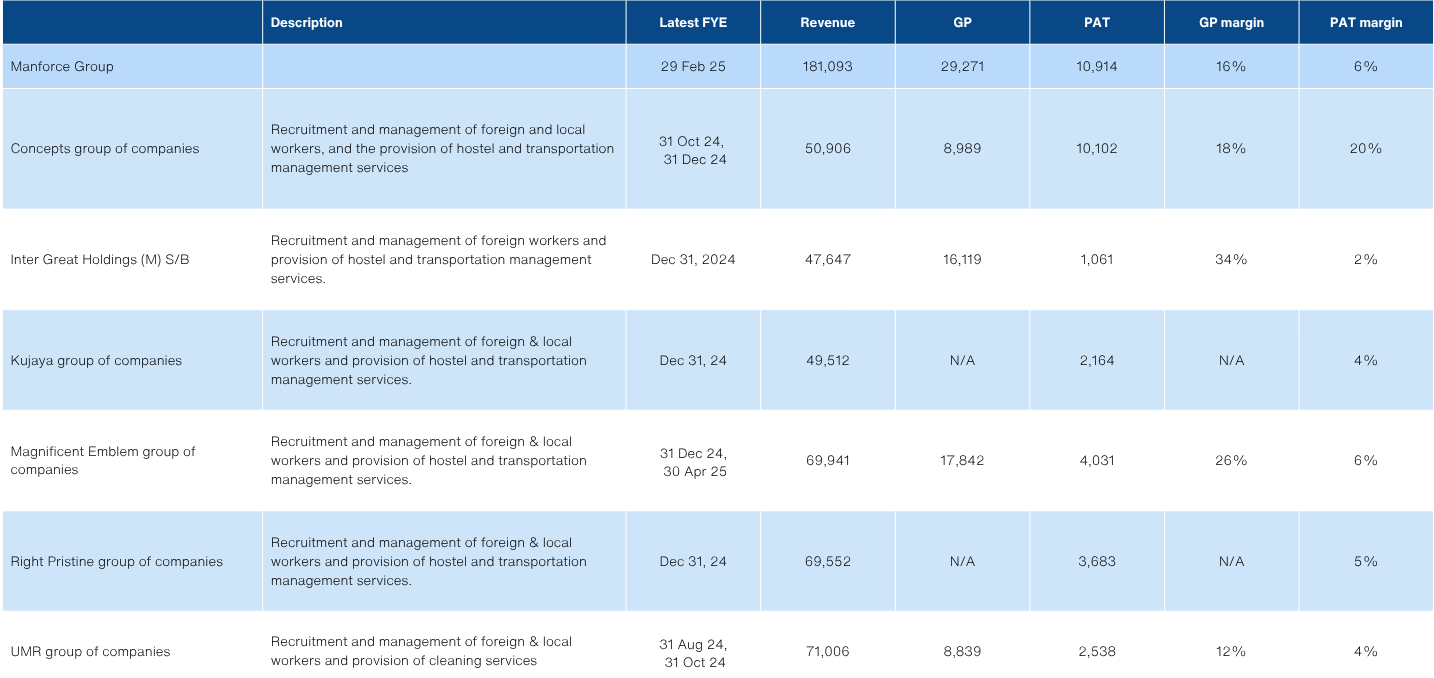

Manforce does not have any direct comparable peers listed in Malaysia, though the prospectus did include a number of non-listed peers. Generally, most had similar margins to Manforce, albeit at relatively smaller scale.

For valuation purposes, we turn instead to regional peers. The weighted average 12M BF PER is 14.4x. Manforce’s margins are below the peer weighted average of 13.6%. However, Manforce’s ROEs are higher at 22.9% vs the peer weighted average of 14.7%. Even the post-listing ROEs should remain above 15%, with the inflated capital base.

In turn, we think the 14x PER multiple we have assigned is reasonable when assessed against peer benchmarks.

Non-listed peers in Malaysia

Revenue dependence on EMA’s is high

PER bands

Source: Bloomberg, NewParadigm Research, May 2026

Foreign worker policy constraint

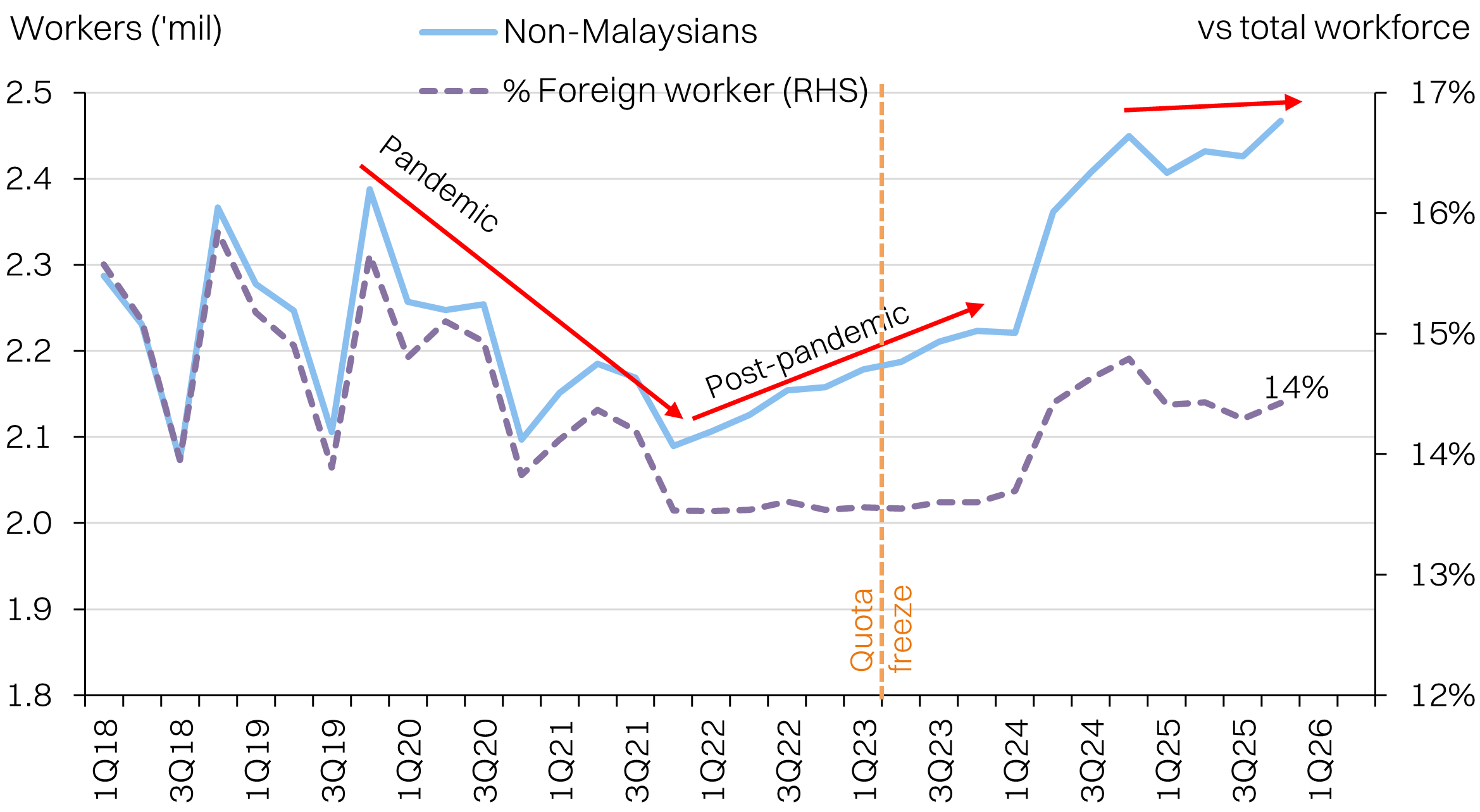

One of the LT growth considerations is the government’s stated policy to lower foreign workers’ ratio from 15% to 10% by 2030 and 5% by 2035.

We think that this policy will be challenging to fully enforce. It implies taking out ~300k foreign workers by 2030 or 1.1m foreign workers by 2035. We anticipate that most of the key sectors employing foreign workers will not be able to adapt quickly enough to replace the labour shortage, especially for manual jobs that are difficult to automate.

A more realistic scenario in our view is a steady increase in levies imposed on the respective industries to deter usage of foreign workers, but without over-tightening quotas, which can be disruptive to businesses.

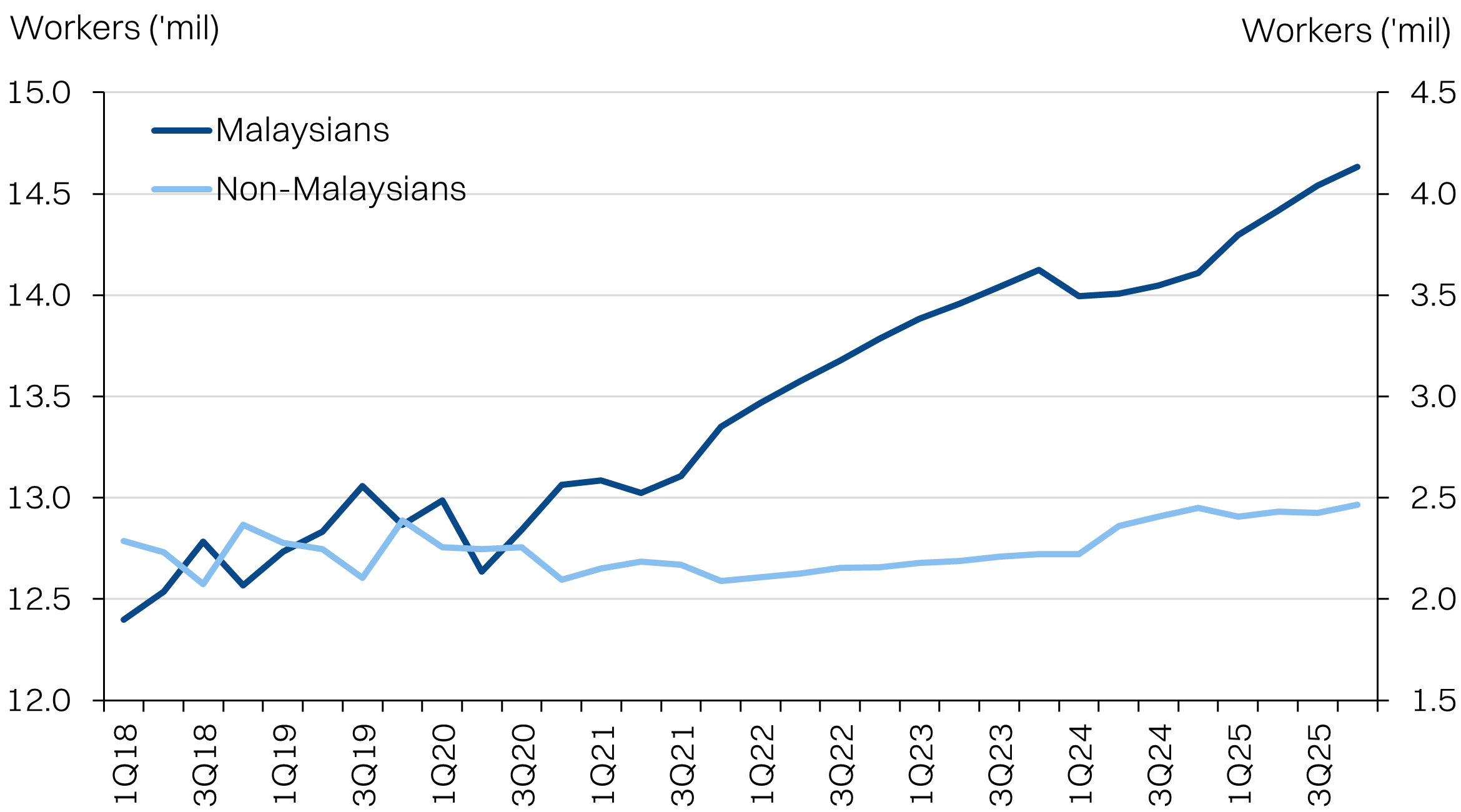

The following charts are based on DOSM’s labour survey, which may differ in numbers from the Ministry of Home Affairs’ figures.

In absolute terms, non-Malaysian worker numbers have trailed Malaysians

Non-Malaysians as share of workforce is down to 14%

Intrinsic mitigating factors

The aforementioned policy risks can be somewhat mitigated by Manforce’s business model:

- Manforce is focused on sectors that have enjoyed high historical requirements as well as countries with high historical approvals.

- Manforce can expand its headcount by serving new customers. It is not solely reliant on incremental headcount approval. In fact, Manforce’s selling point to prospective customers is the high retention rate of workers: >80%, which will be critical if there is going to be shortages.

- Manforce also focuses on high quality customers, that have the resources and the need that should allow for higher quota approvals. Manforce’s share of foreign workers is also very small.

Foreign workers by sector

Foreign worker regulations are comprehensive and stringent

Exclusive marketing agents risk

Manforce has a heavy reliance on 5 exclusive marketing agents (EMAs) to source revenue. Roughly two-thirds of revenue across FWM and MLS comes from these EMAs. Manforce also has an internal sales force team of 37 people, which drive the remaining one-third of revenue.

These agents operate exclusively with Manforce, but are independent entities. This creates some risk for Manforce, if there are any mistakes or misrepresentations by the agents in question.

The scope for the EMAs includes prospecting and solicitation of new clients, pre-arrival administration, post-arrival liaison, collections and ongoing relationship management. The commissions for the agents are classified under cost of sales, and ranges from 2.7% to 3.5% of agent revenues.

One of the EMAs stands out - MLS Resources. It is the sole proprietorship held by Tan Szu Chieh, who was previously a director with Manforce subsidiaries. The relationship was declassified as a related party transaction, following Tan’s resignation in July 2024. MLS Resources continues to operate as an EMA. The prospectus also flags that commission payable to MLS Resources was not conducted on an arm’s length basis, reflecting certain variations due to MLS Resources’ early involvement as an initial EMA.

Looking ahead, we’d like to see a larger proportion of revenue driven from in-house sales agents and a reduced reliance on EMAs. The ~3.5% commission is sizable, given the EBITDA margin is about 10-11%. This means the effective GP loss is about 30%. Decreased reliance on EMAs would help improve margins and profitability. That said, we have not factored in any reduction in said dependency.

Revenue dependence on EMA’s is high

Low customer concentration risk

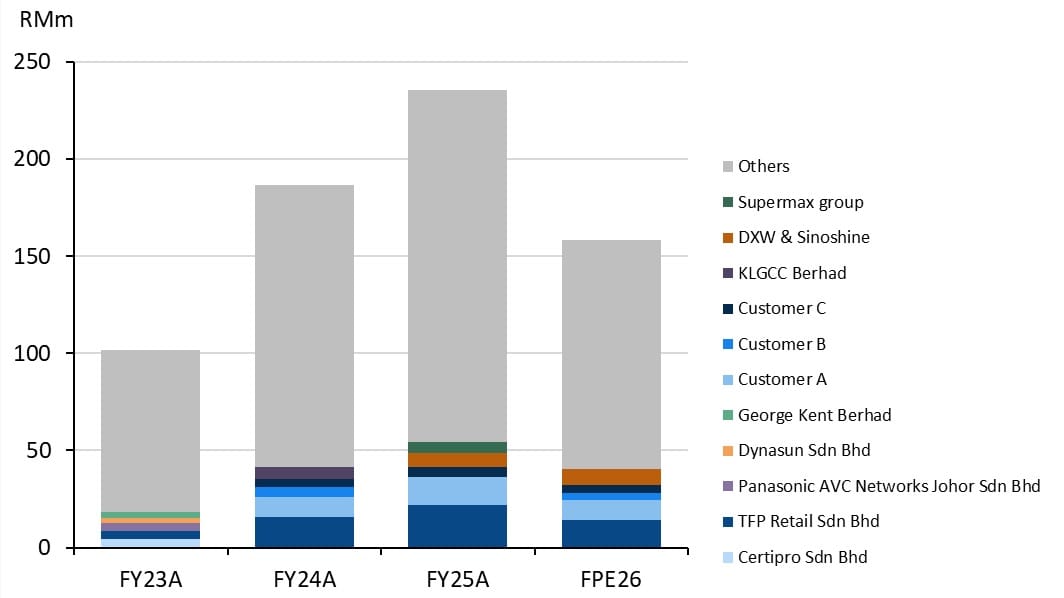

Manforce has a relatively diversified customer base. The group’s top 5 customers only contribute 34.5% of total revenue in FPE26. Overall Manforce has over 150 clients, which is well-diversified.

Some of Manforce’s notable customers includes TFP Retail Sdn Bhd, which operates Village Grocer, as well as listed companies such as Supermax, Panasonic and George Kent. Some of Manforce’s other larger customers includes hospitals, retail chains and pharmacies.

Looking ahead, management indicated plans to leverage its listing status to continue pursuing more high-profile customers that are also listed corporates. This will enable the group to grow beyond simply pursuing enlarged quotas/applications from existing customers. Key sub-sectors that are in focus includes F&B and retail.

Revenue breakdown by customer

Key management

Lim Ket Keong - Chief Operation Officer

Lim Ket Keong has over 25 years of experience in operations management, strategic planning, and business development. A graduate of Universiti Putra Malaysia with a Bachelor of Economics. His prior roles including General Manager and COO within the group and experience in foreign worker operations at IMI Supplies Sdn Bhd. He rejoined the group in 2020 as Chief Operation Officer, overseeing operational strategy, policy implementation, and overall performance. He is the sibling of Datin Lim and brother-in-law of Datuk Wong Boon Ming, and is the uncle of Wong Chen An and Wong Chew Li

Wong Chen An - Head of Sales & Marketing

Wong Chen An oversees sales strategy and customer acquisition, with over 15 years of experience in sales and marketing, including prior roles in insurance and HR outsourcing. He holds an MBA from the University of Gloucestershire and has been with the group since 2012. He is the son of Datuk Wong Boon Ming and Datin Lim, sibling of Wong Chew Li, and brother-in-law of Ng Chee Kiong

Ng Chee Kiong - Head of Recruitment & Administration

Ng Chee Kiong oversees foreign worker recruitment and manages relationships with overseas partners to match candidates with client requirements. He joined the group in 2015 and progressed from Overseas Operations Executive to Head of Overseas and Outsourcing in 2017, before being redesignated to his current role in 2025. He is the spouse of Wong Chew Li and son-in-law of Datuk Wong Boon Ming and Datin Lim, as well as brother-in-law of Wong Chen An.

Wong Chew Li - Head of Account

Wong Chew Li oversees accounting operations, financial reporting, and regulatory compliance, supporting the Finance Director in executing the group’s financial strategy. She holds a degree in Accounting and Finance from the University of Greenwich and has been with the group since 2011, progressing from Finance Executive to her current role in 2022, with over a decade of experience in financial reporting, audit, and treasury. She is the daughter of Datuk Wong Boon Ming and Datin Lim, spouse of Ng Chee Kiong, and sibling of Wong Chen An, indicating direct familial links across controlling shareholders and key management.

Low Siau Vun - Head of Human Resources

Loh Siau Vun is responsible for overseeing the group's human resource strategy encompassing payroll management, recruitment, compliance, employee engagement and professional development. With around 15 years of HR experience across the hospitality and healthcare sectors, she joined Manforce in 2019 as Assistant Manager of Human Resource and Administration, having previously managed payroll for over 800 employees at BP Healthcare Group, before being promoted to her current role in 2025.

Board of directors

Datuk Wong Boon Ming - Managing Director, Promoter, Substantial Shareholder

Datuk Wong Boon Ming holds approximately 65.3% effective ownership post-IPO (58.4% direct, 6.9% indirect) and has over 27 years of experience in foreign worker management, entering the sector in 1999. He acquired a 90% stake in MRSB, the group’s predecessor, in 2005 and has since led its strategic direction. The group’s ownership and management remain closely tied to the Wong–Lim family, with his spouse, Datin Lim, on the Board and several immediate family members in senior management.

Datin Lim Gun Kiau - Non-Independent Non-Executive Director, Promoter, Substantial Shareholder

Datin Lim holds approximately 65.3% effective ownership post-IPO (6.8% direct, 58.5% indirect) and has been involved with the group since its early formation. She began her career in the family poultry wholesale business before supporting the operations of MRSB in 2005, and acquired a 10% stake in 2007, serving as Non-Executive Director since. She is the spouse of Datuk Wong Boon Ming, with broader family representation across senior management.

Tengku Faizwa Binti Tengku Razif - Independent Non-Executive Chairperson

Tengku Faizwa has experience in human capital development and strategic consulting, having founded The Switch Sdn Bhd and Ideaspark Sdn Bhd. Since 2018, she has been involved in management services and charter flight businesses. She currently serves as Independent Non-Executive Chairperson of KGW Group Berhad, ASM Automation Group Berhad, and Kee Ming Group Berhad, with no disclosed relationships with other board members or substantial shareholders.

Chin Kok Weng - Finance Director

Chin Kok Weng has approximately 28 years of experience in accounting and finance, beginning in audit before moving into corporate finance roles overseeing treasury and accounting functions. He joined the group in 2012 and progressed to Chief Financial Officer in 2016, Executive Director in 2018, and was redesignated as Finance Director in 2025.

Tan Yiing Fung - Independent Non-Executive Director

Tan Yiing Fung has over a decade of experience in corporate and commercial law, specialising in mergers and acquisitions, corporate restructuring, and capital markets. She is a Partner at Messrs. CY Poon & CM Lim, focusing on equity and debt capital markets and venture capital advisory. She currently serves as Independent Non-Executive Director of West River Berhad, Aldrich Resources Berhad, Malaysian Genomics Resource Centre Berhad, and Camaroe Berhad, with no disclosed relationships with other board members or substantial shareholders.

Koh Eng Siong - Independent Non-Executive Director

Koh Eng Siong has over four decades of experience in manufacturing operations and business leadership, progressing from a Process Engineer role into senior management positions, included General Manager and Chief Executive Officer. He had a long tenure at Superlon Worldwide Sdn Bhd, contributing to operational growth, and later moved into advisory roles, including ISO auditing and business coaching.

Lim Chai Har - Independent Non-Executive Director

Lim Chai Har has over 20 years of experience in audit, accounting, and corporate services, beginning her career at Ernst & Young where she progressed to Senior Manager. She later founded and co-founded several firms focusing on outsourced accounting, corporate secretarial, and advisory services. She currently serves as Independent Non-Executive Director of Kamdar Group (M) Berhad.

Selected financials

Source: Company Data, Bloomberg, NewParadigm Research, May 2026