Just charts: Banks 1Q26 preview

There is high risk of a negative surprise in banks' earnings.

Key takeaways:

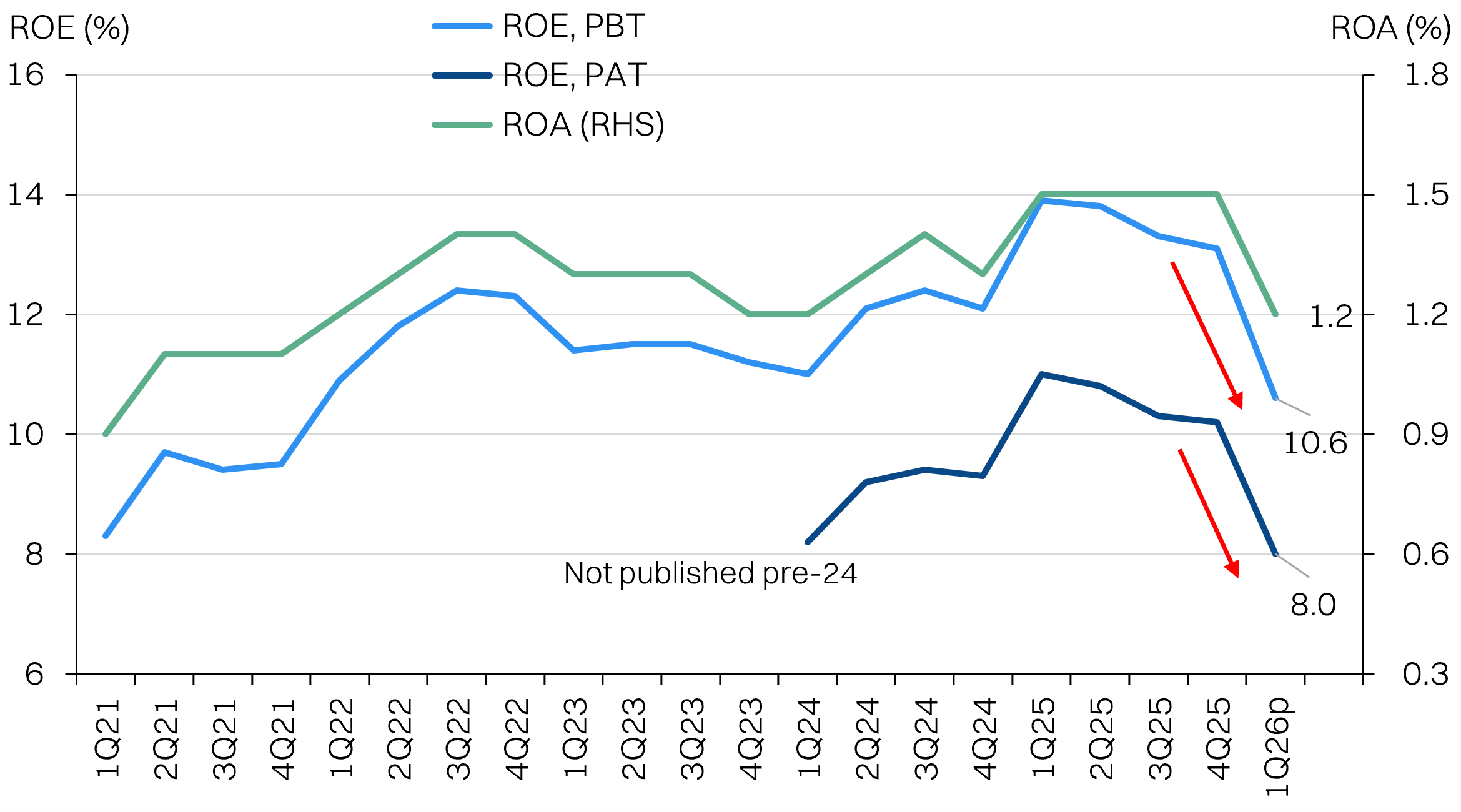

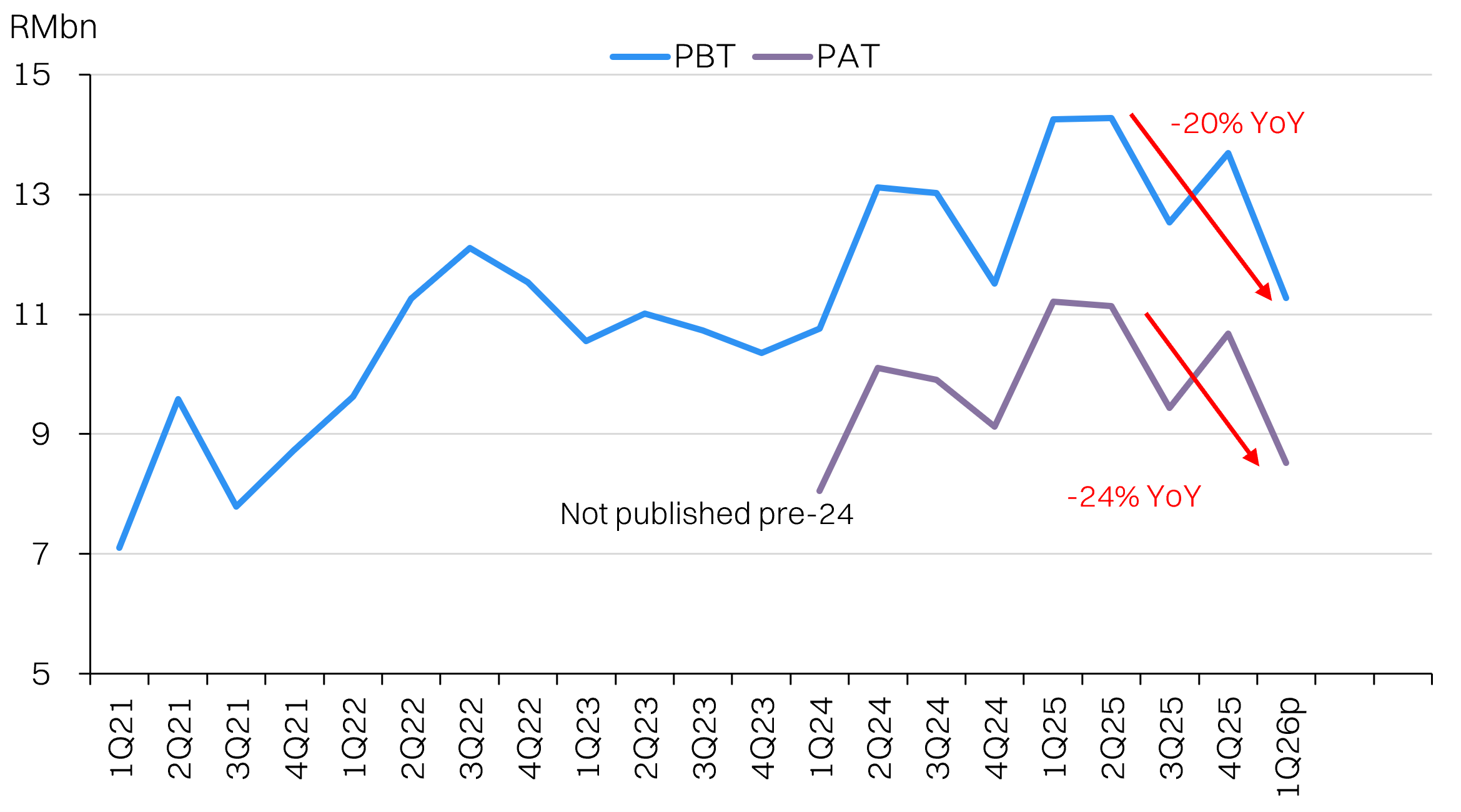

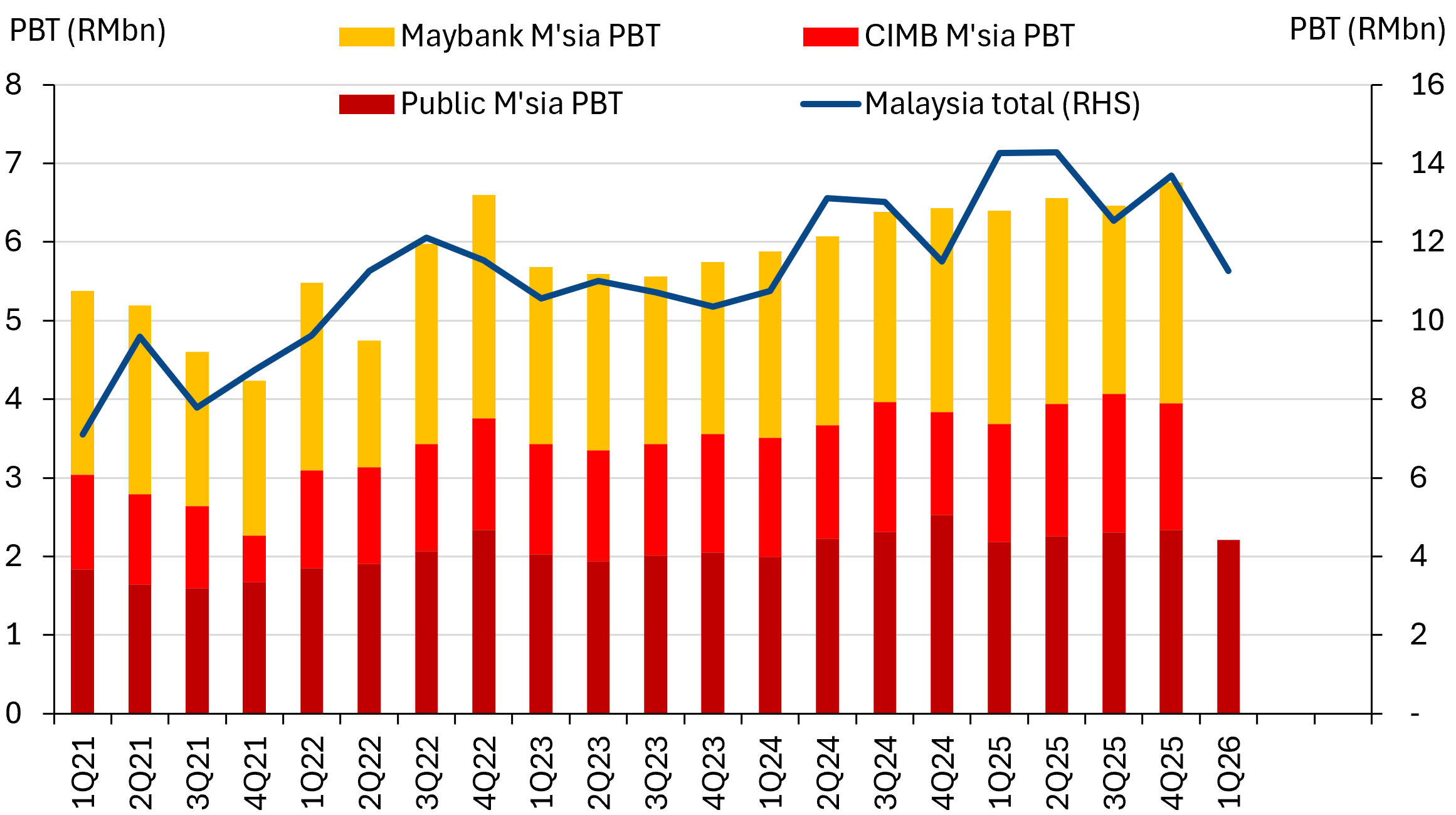

- BNM's prelim earnings for banks' profitability shows a sharp contraction in 1Q26; -20% YoY.

- Public Bank already reported a fairly stable 1Q26 PBT (+0.1% YoY); raises possibility one of the other big banks disappoints.

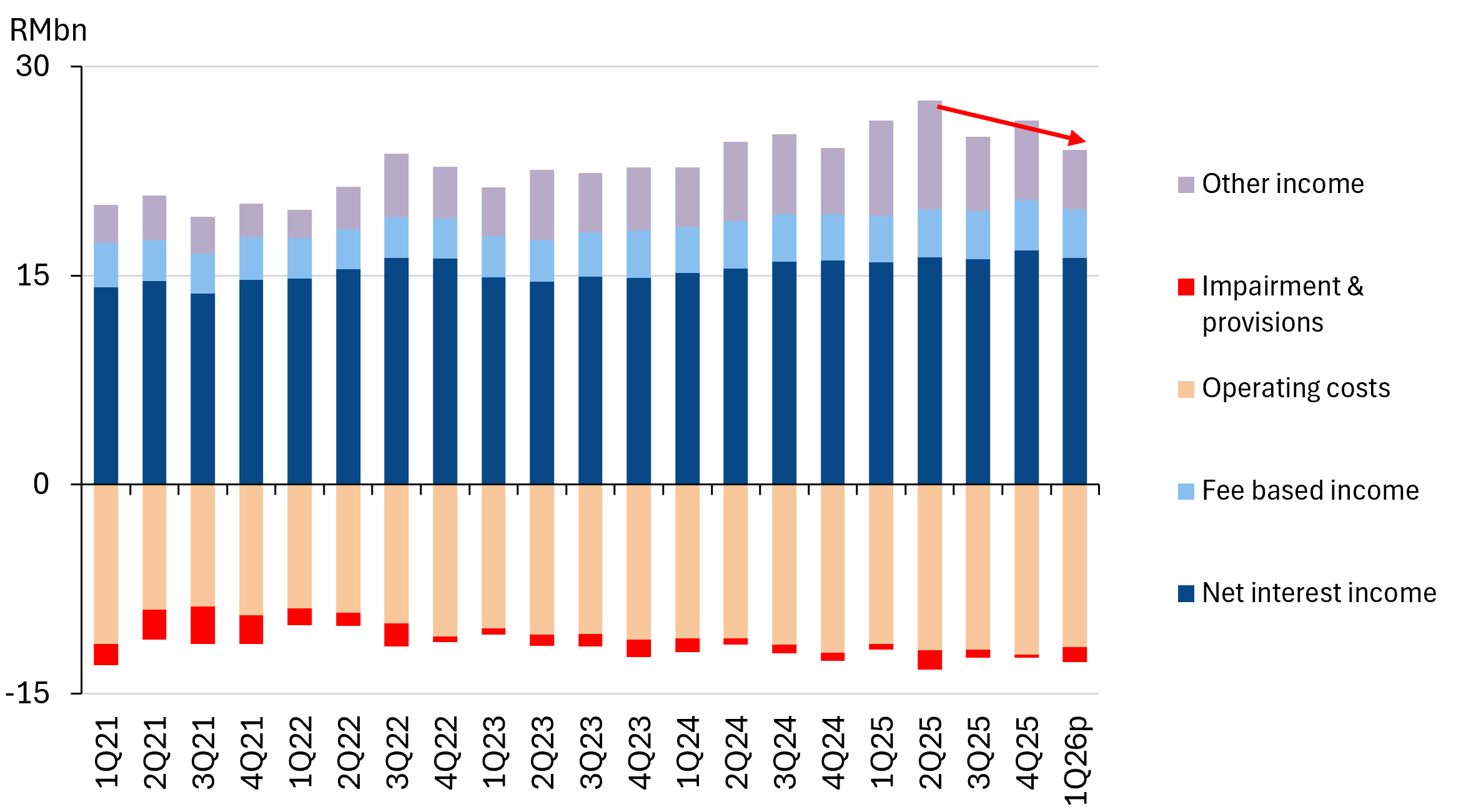

- Soft topline growth hurt by NIM compression, despite loans growth.

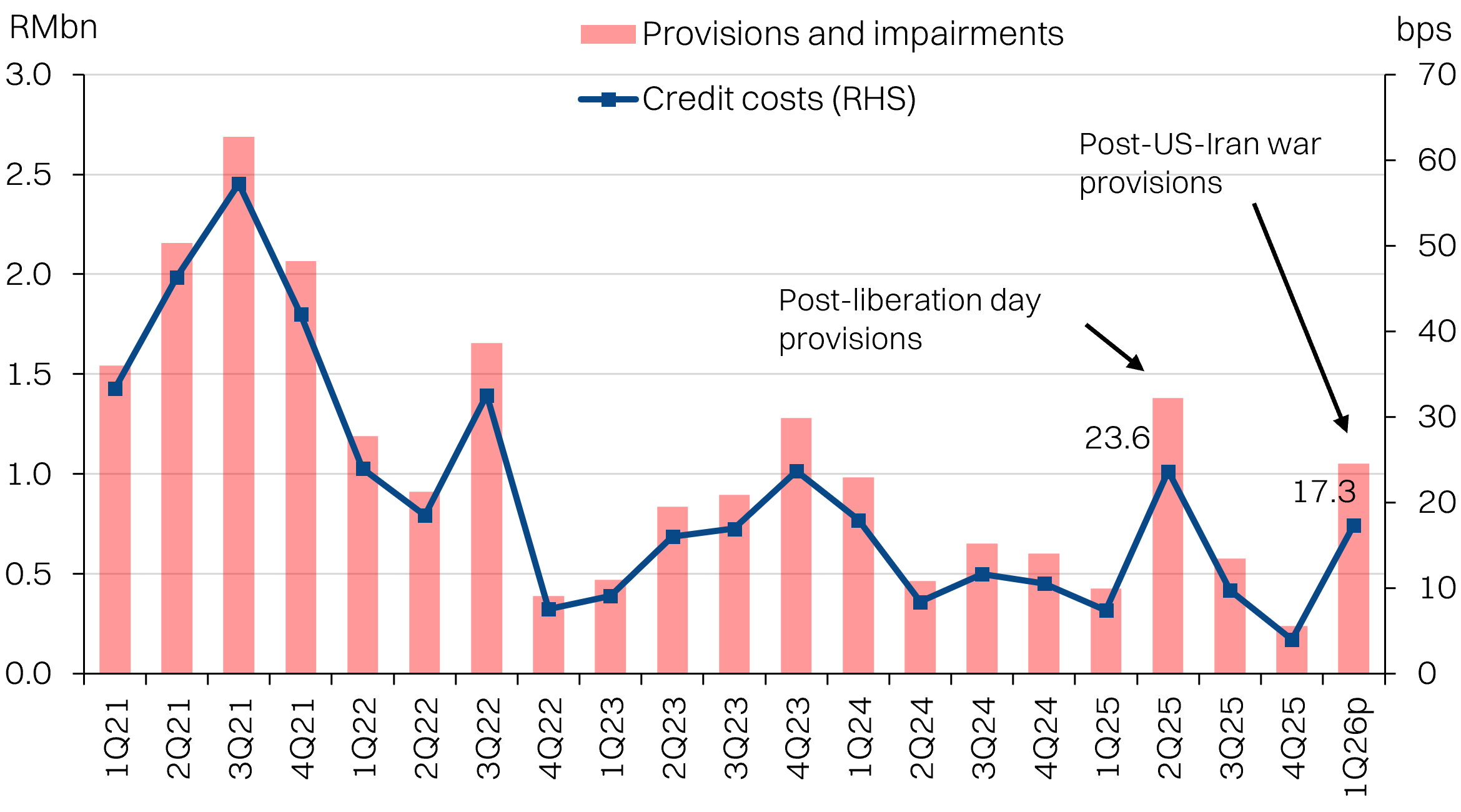

- Credit costs jumped to ~17bps, compared with 11bps FY25 average, likely on preemptive provisions due to the US-Iran war with room to normalize going forward.

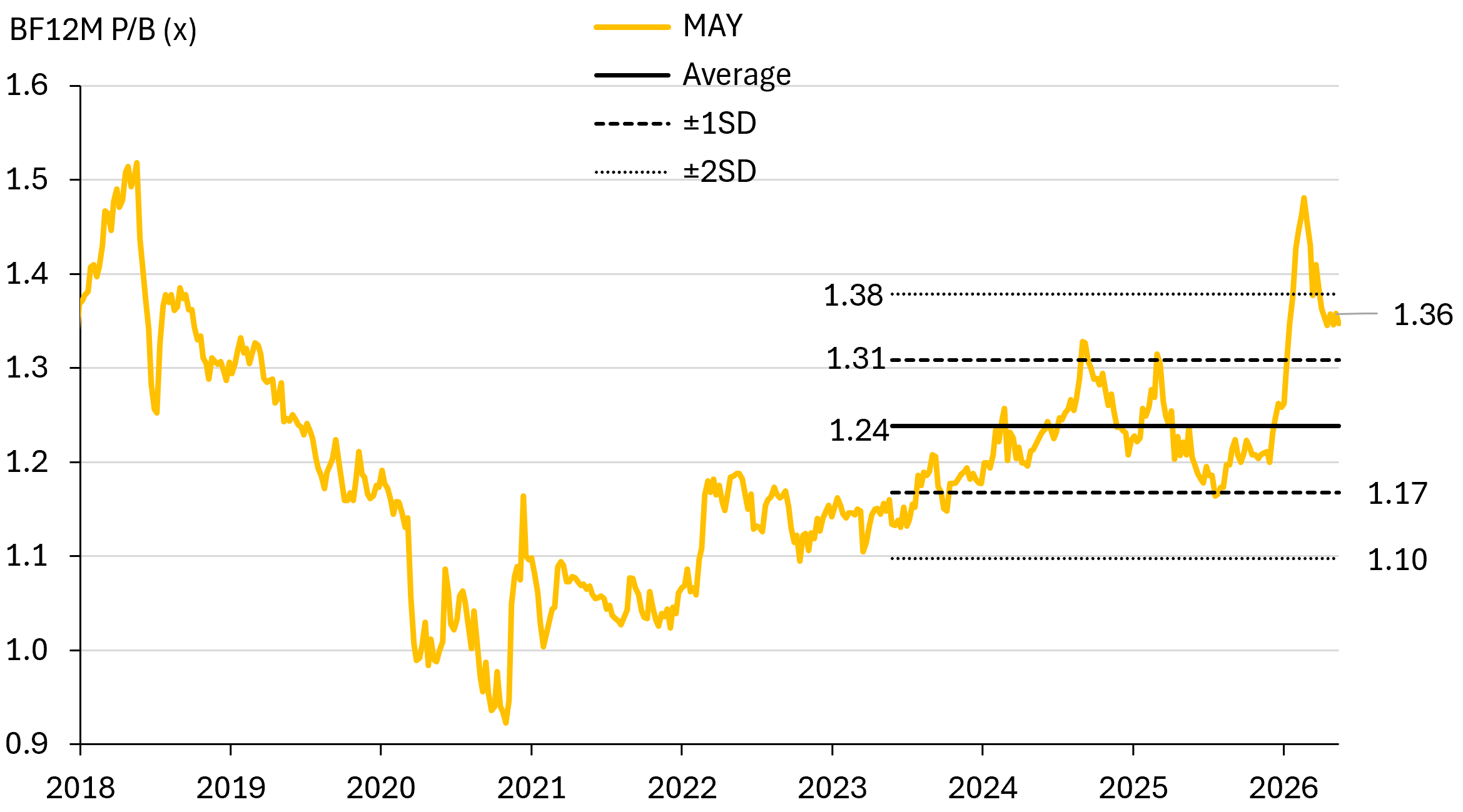

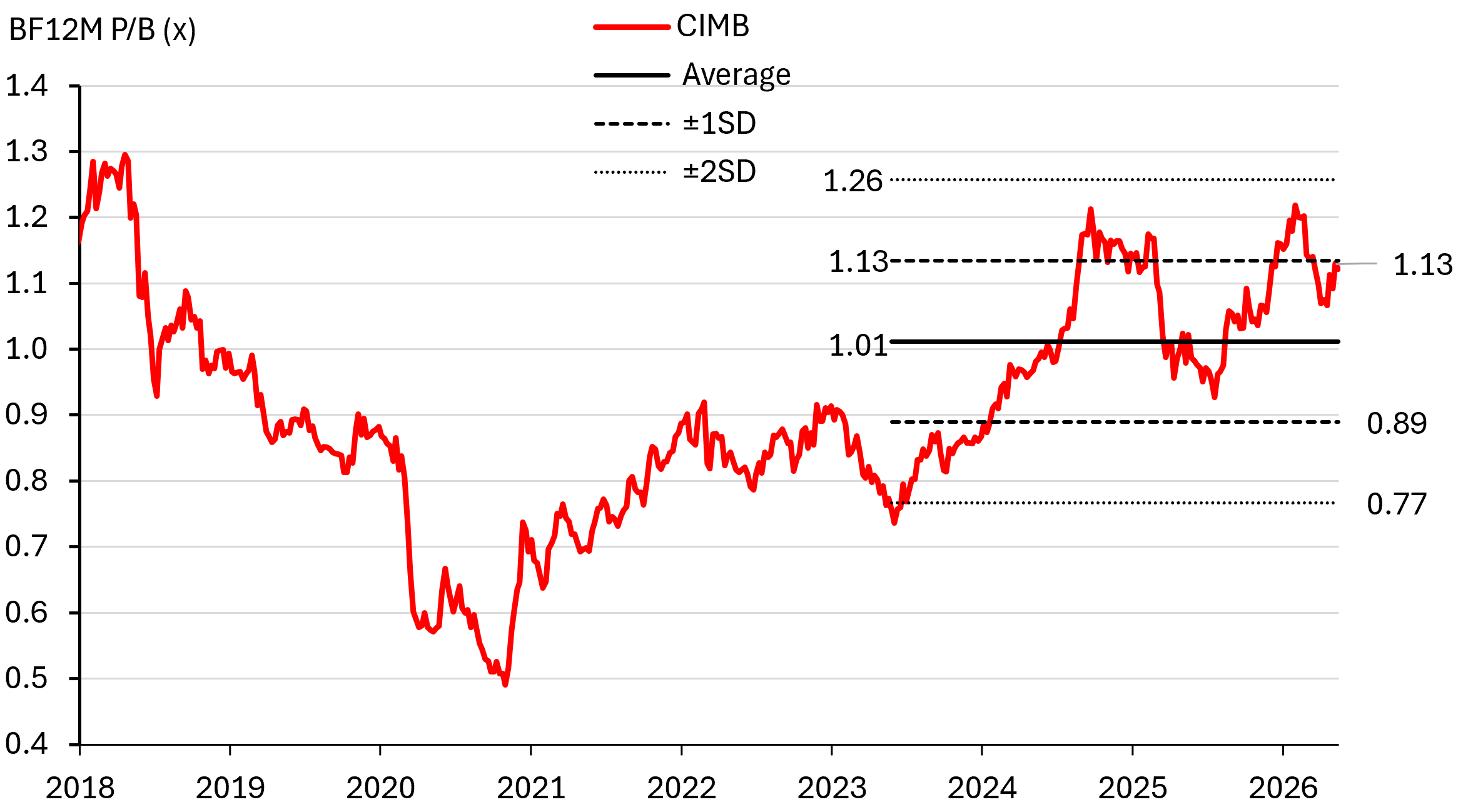

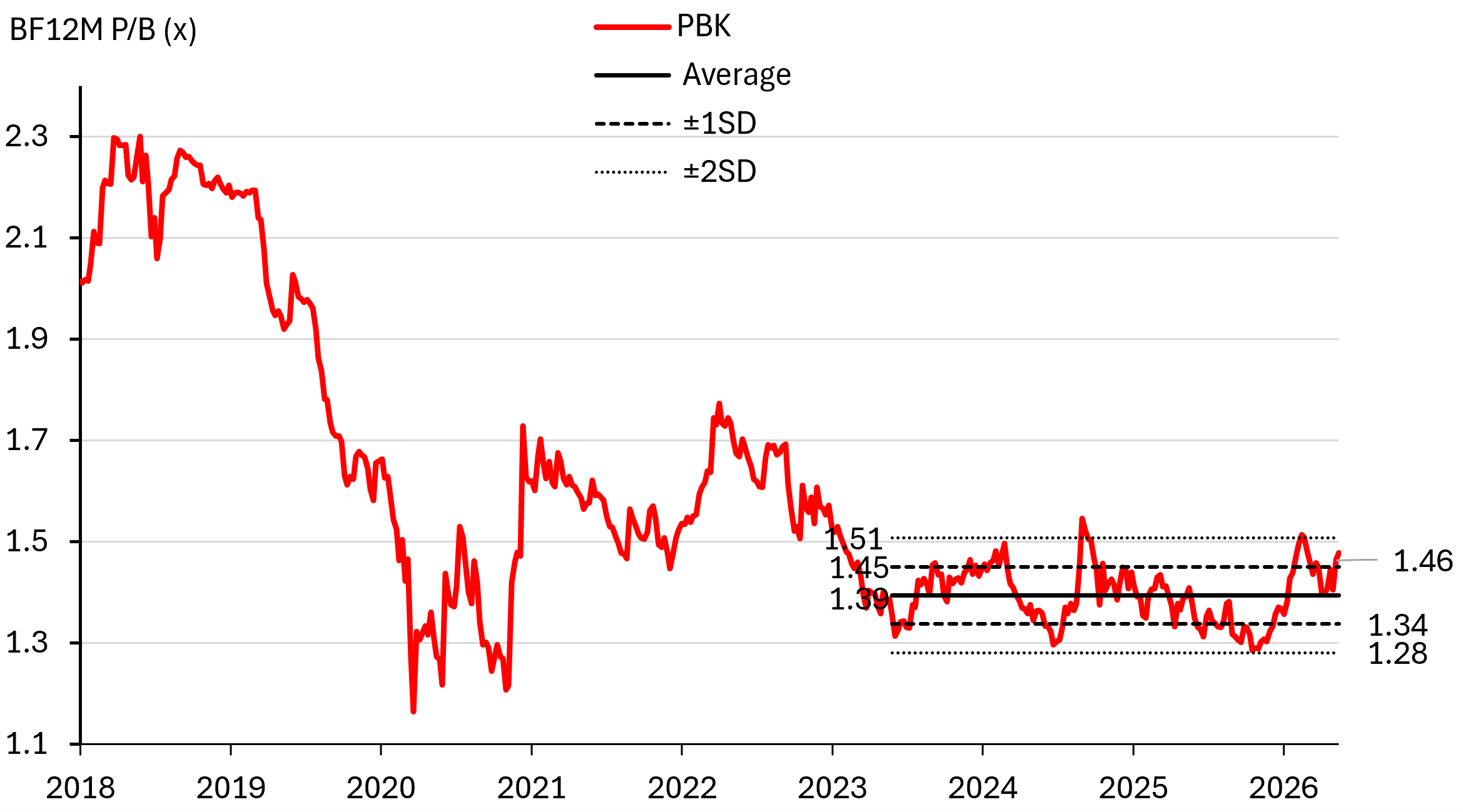

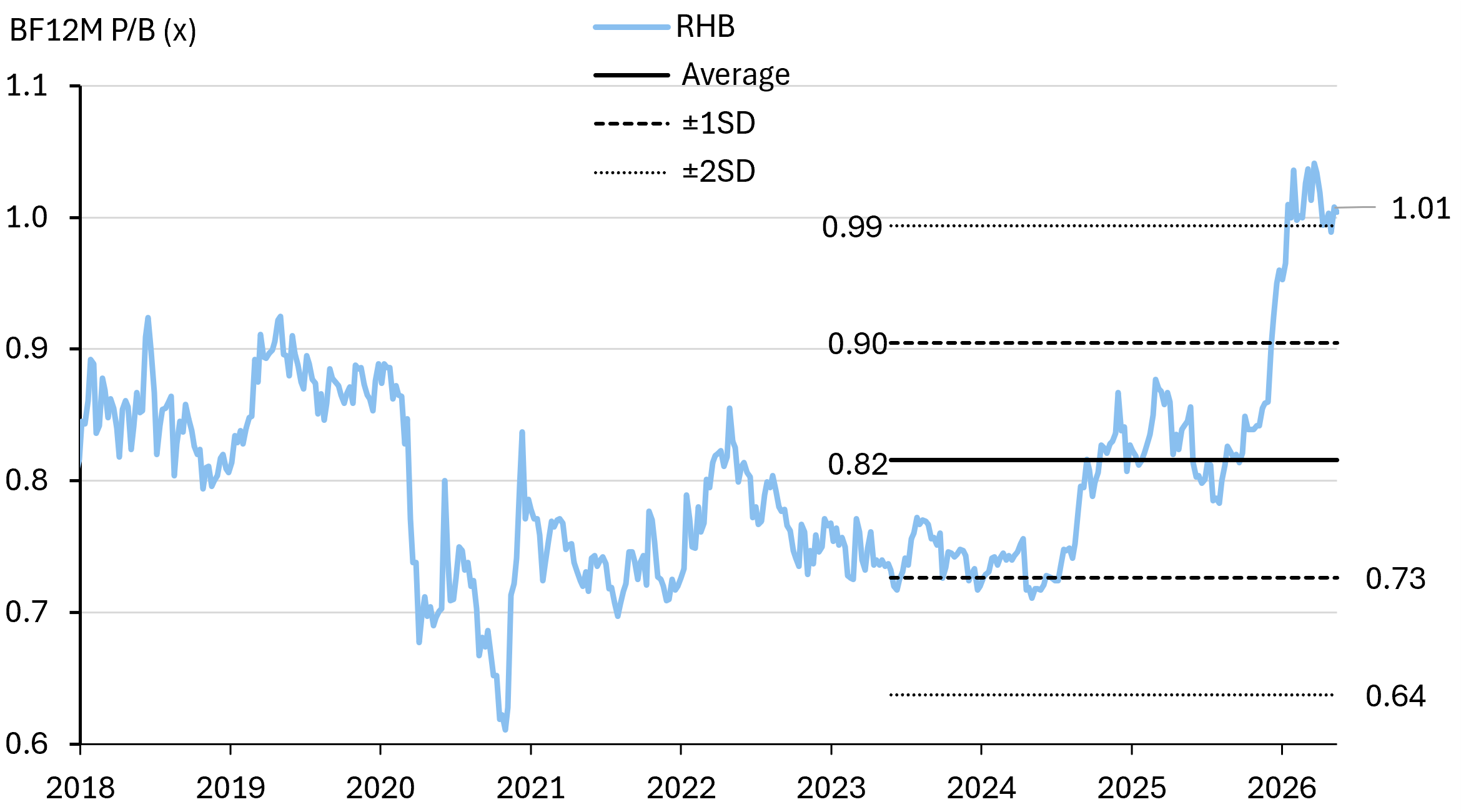

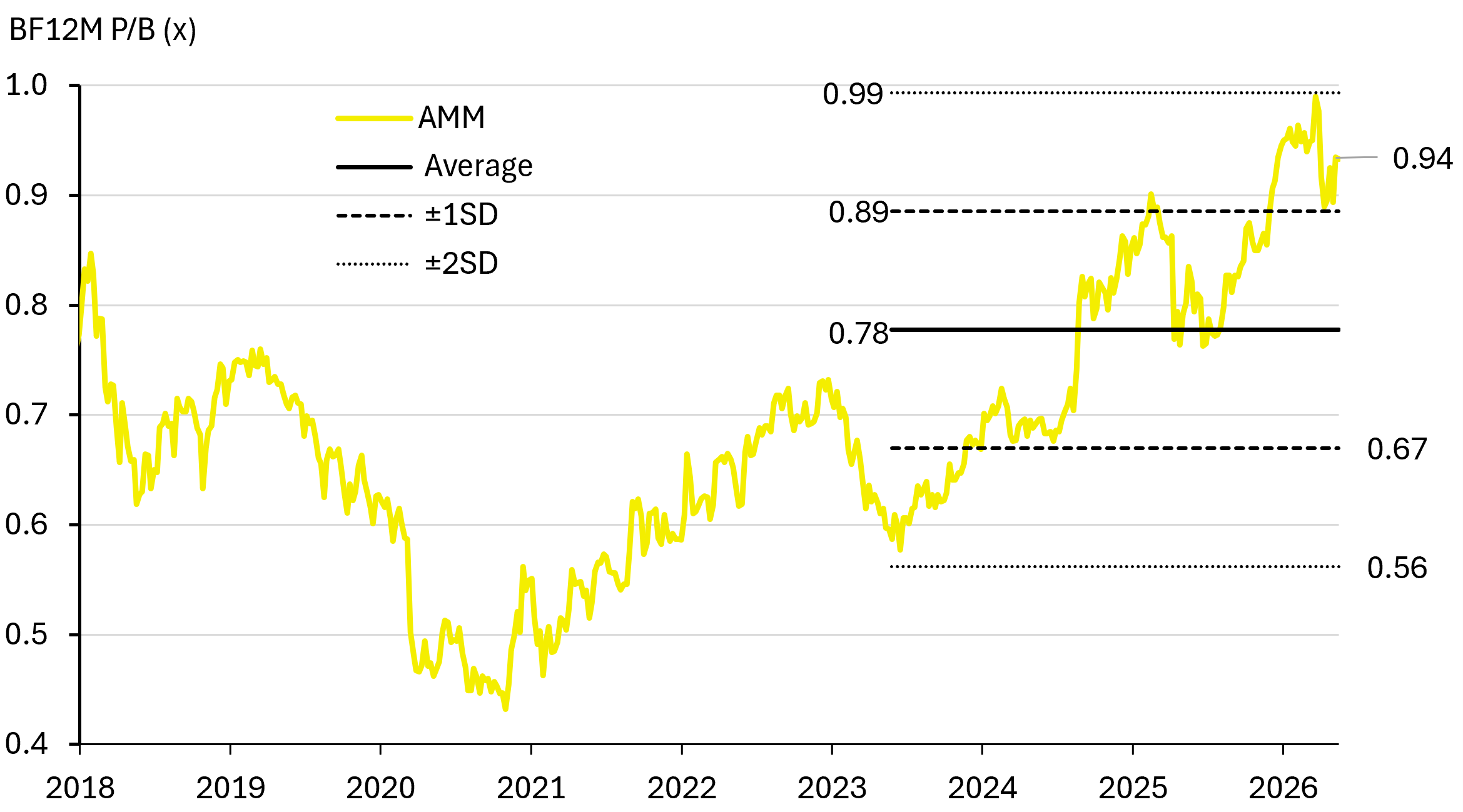

- Meanwhile, bank sector valuations remain elevated (as high as+1.5SD to +2.1SD) as a perceived defensive sector.

About BNM's prelim domestic bank data

BNM publishes the domestic banking sector preliminary profitability roughly 2 weeks before the banks report earnings. Numbers are subject to revisions and reflects only the domestic banking operations of banks. It excludes overseas operations and includes domestic operations of foreign banks. Historically, the big 3 make up about 50% of the prelim PBT numbers.

Additional qualification of the figures: Banking system profits are aggregated at the entity level. The aggregated results for 2019 onwards are subsequently adjusted for dividend income received from domestic banking subsidiaries (previously added at both the parent and subsidiary levels). The adjustment is reflected under 'Other income'. Differences in comparative pre-tax figures reported in previous Quarterly Bulletins are estimated to range between 5.5% and 10.7%.

Domestic sector prelim profitability: Sharp compression

Domestic banking prelim earnings: Sharp compression

Domestic banking prelim earnings vs big 3 banks

Domestic banking prelim P&L: Revenue pressure

Domestic banking prelim credit costs - spiked following the war

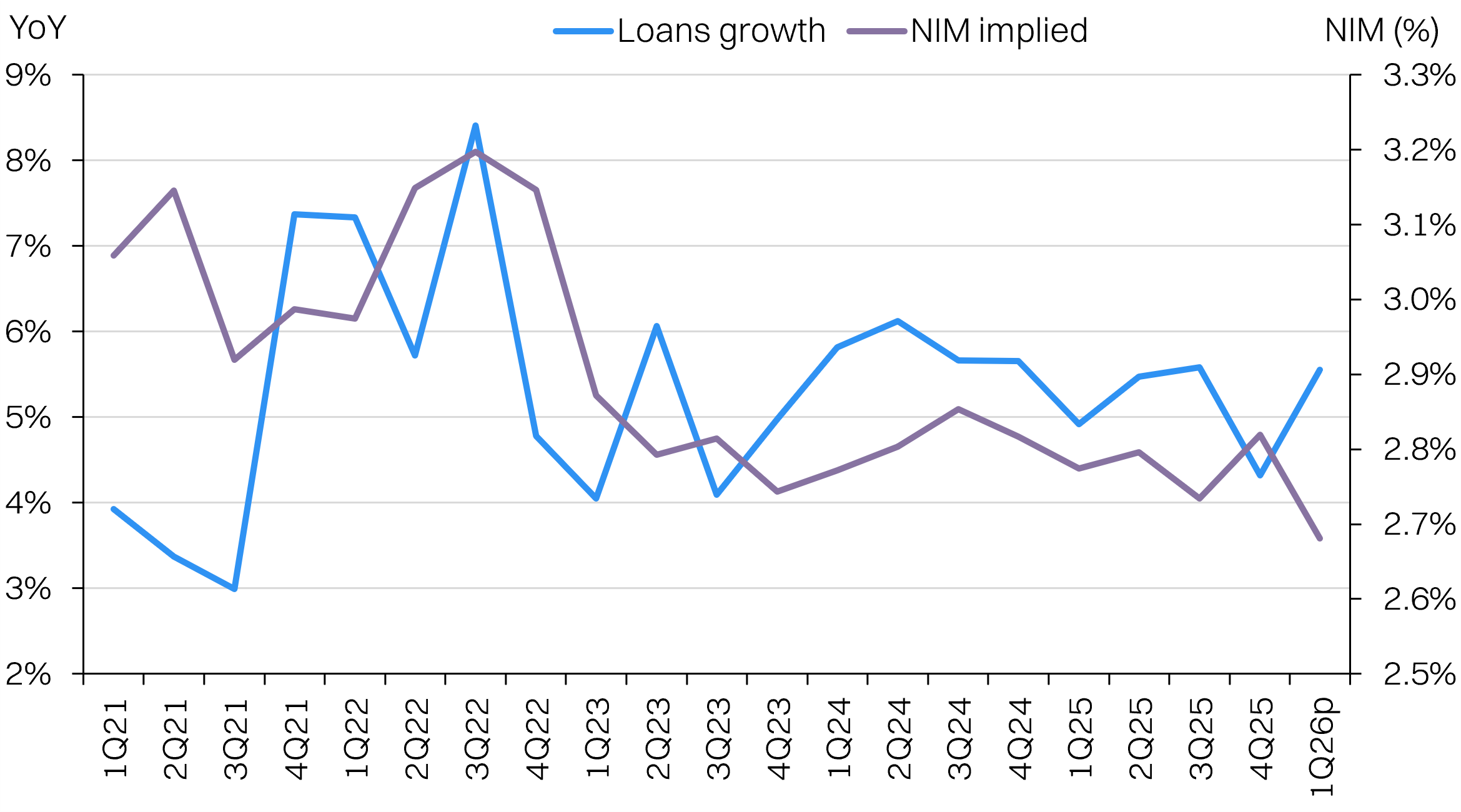

Domestic banking prelim NIM & loans growth - volume over margins

Banks' valuations & profitability

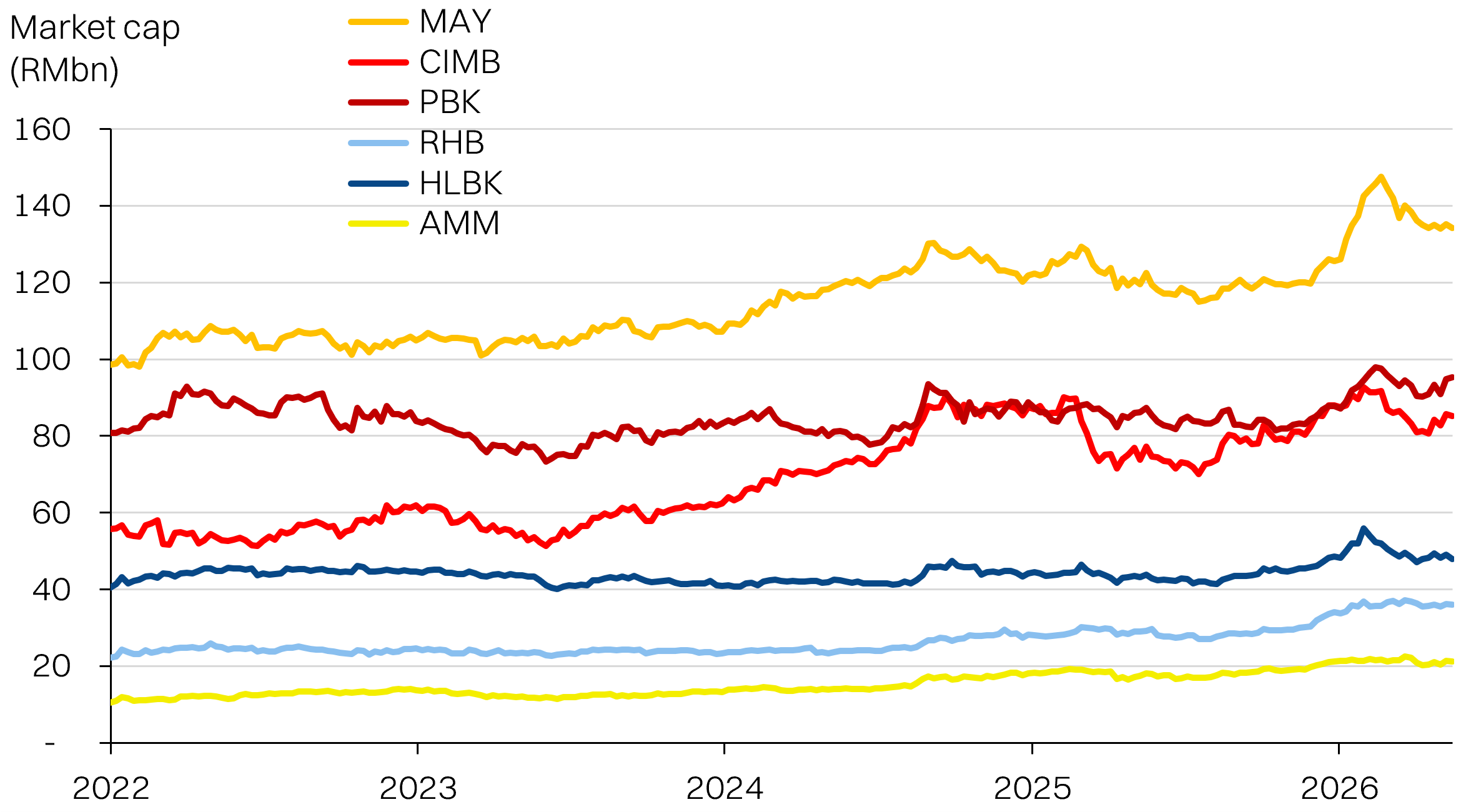

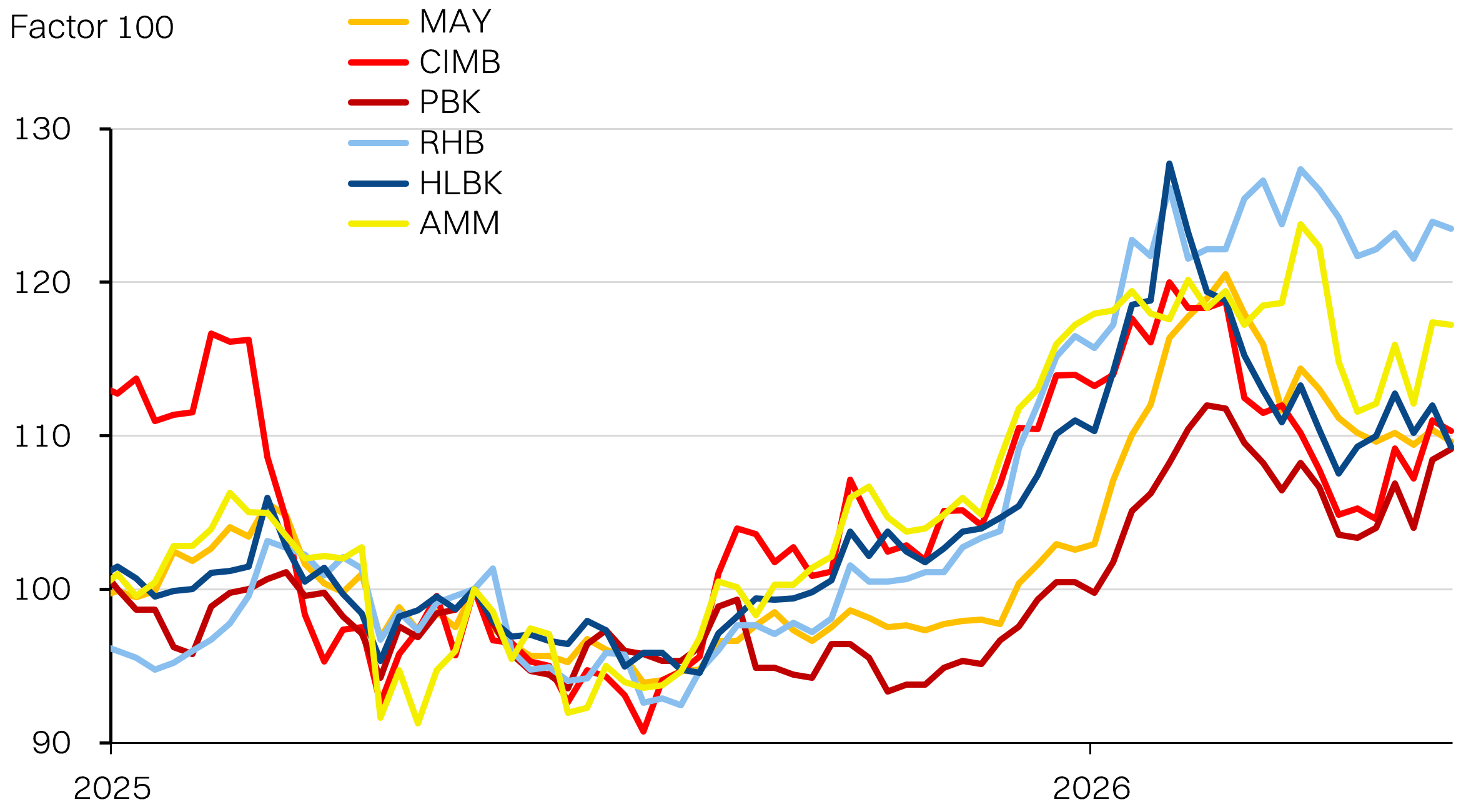

Market cap | 1yr performance

Source: Bloomberg, NewParadigm Research, May 2026

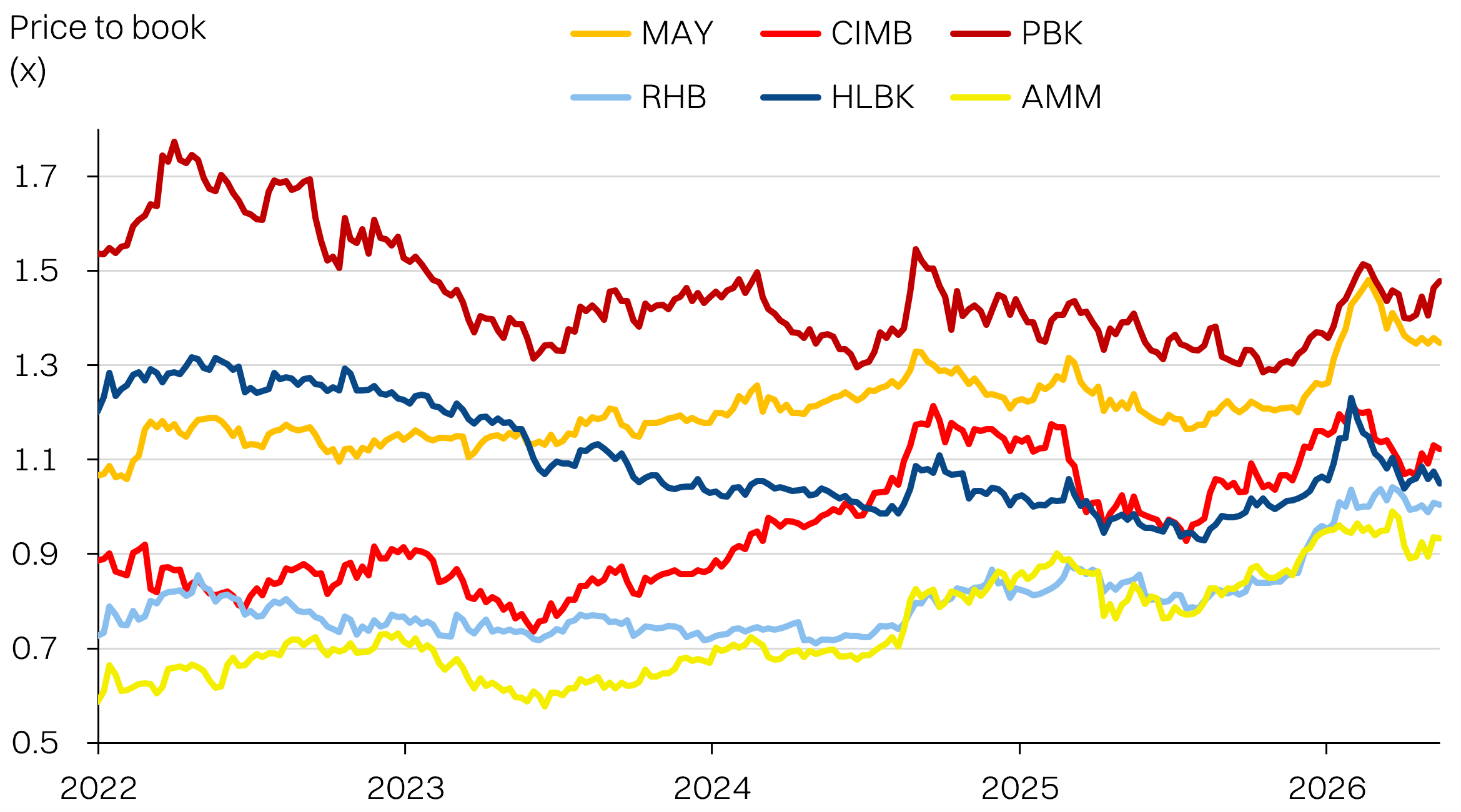

Price-to-book ratio for the banks

P/B bands for the banks

Source: Bloomberg, NewParadigm Research, May 2026

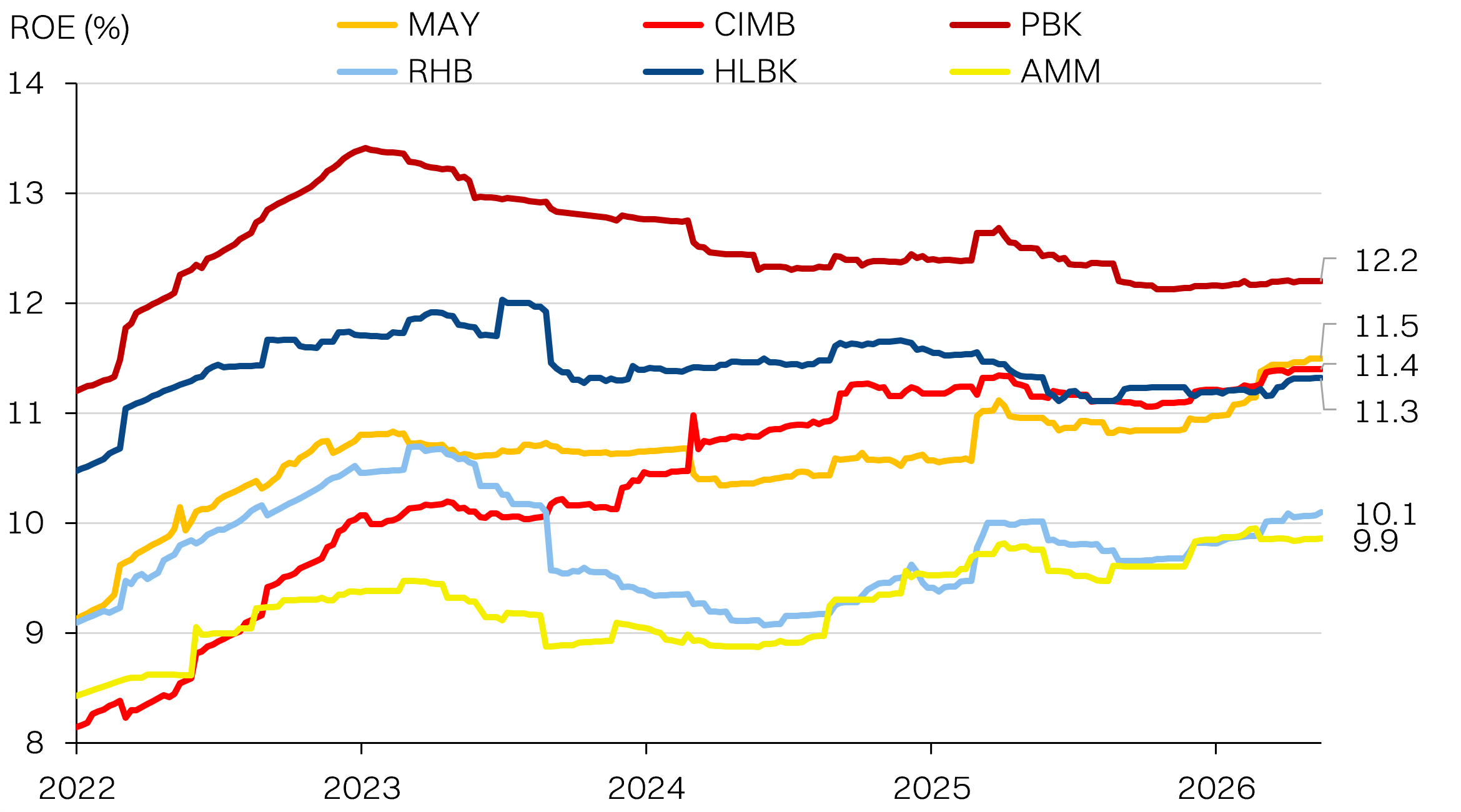

ROEs - Incremental convergence

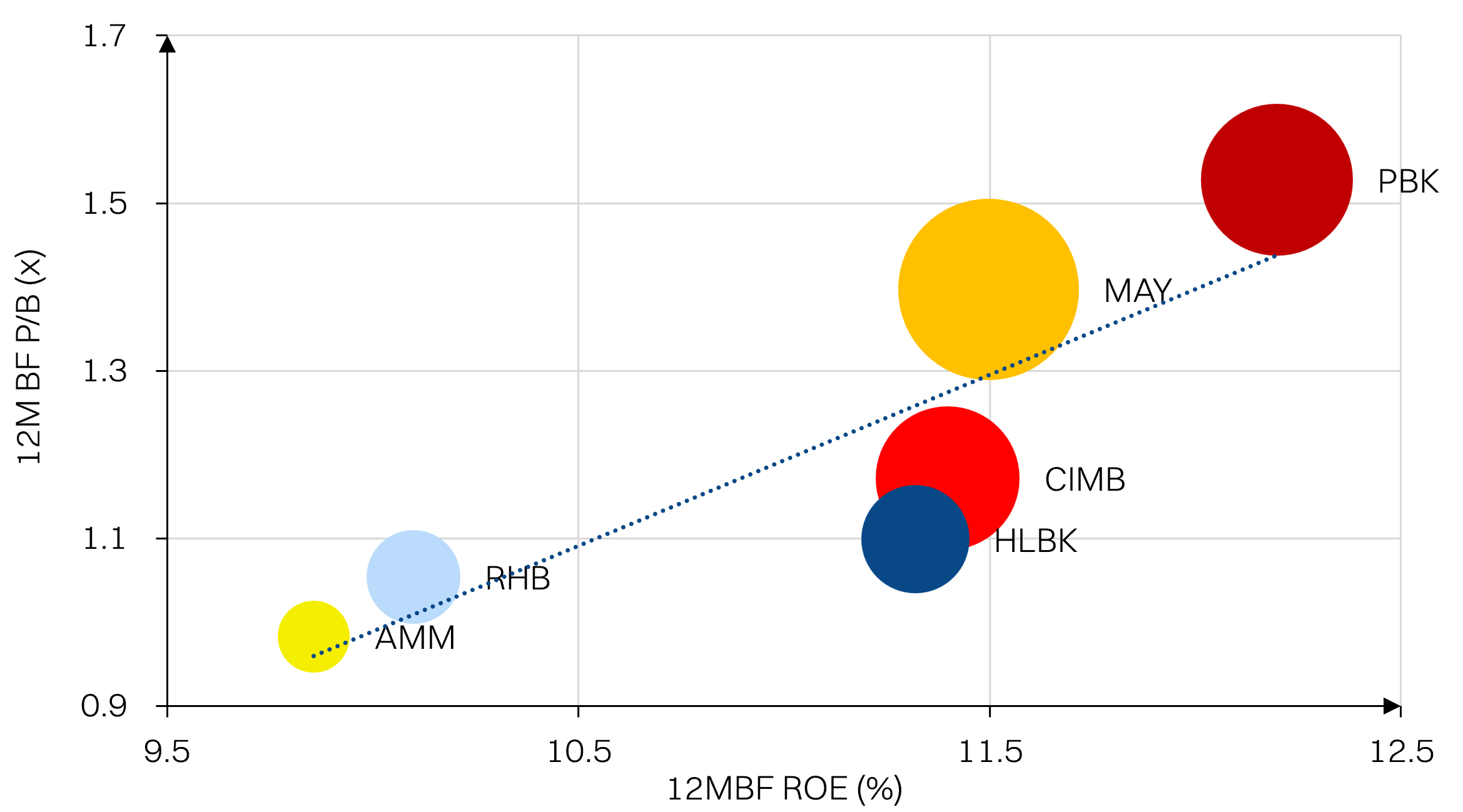

P/B vs ROE - CIMB & HLBK relatively cheap

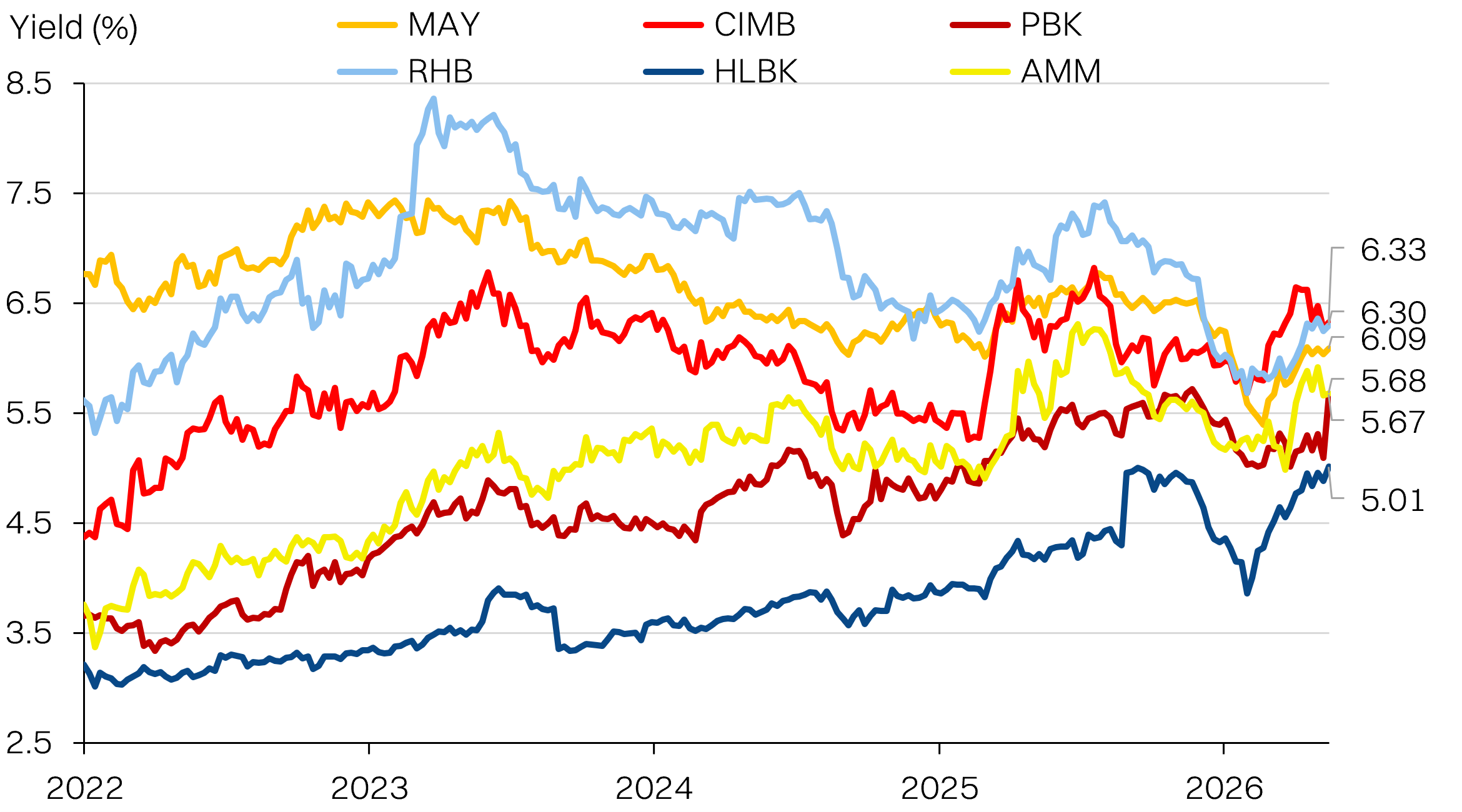

Yield - Convergence

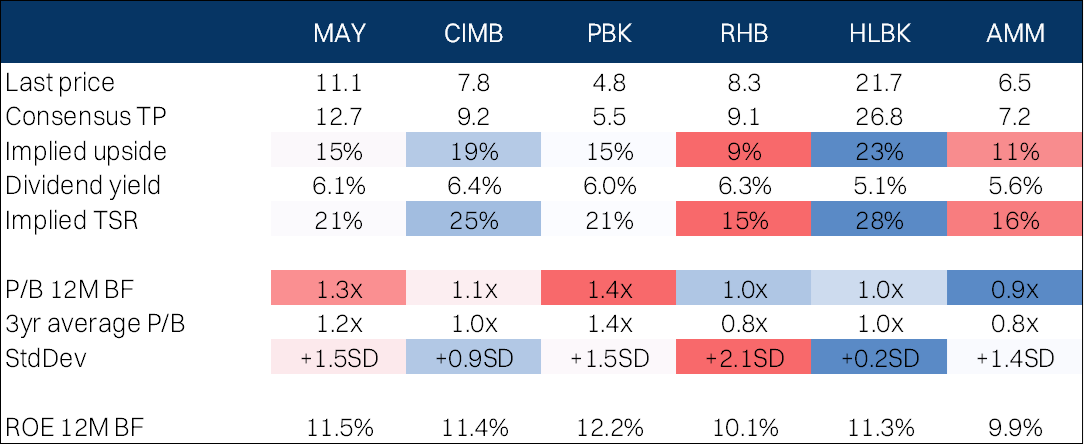

Comp table