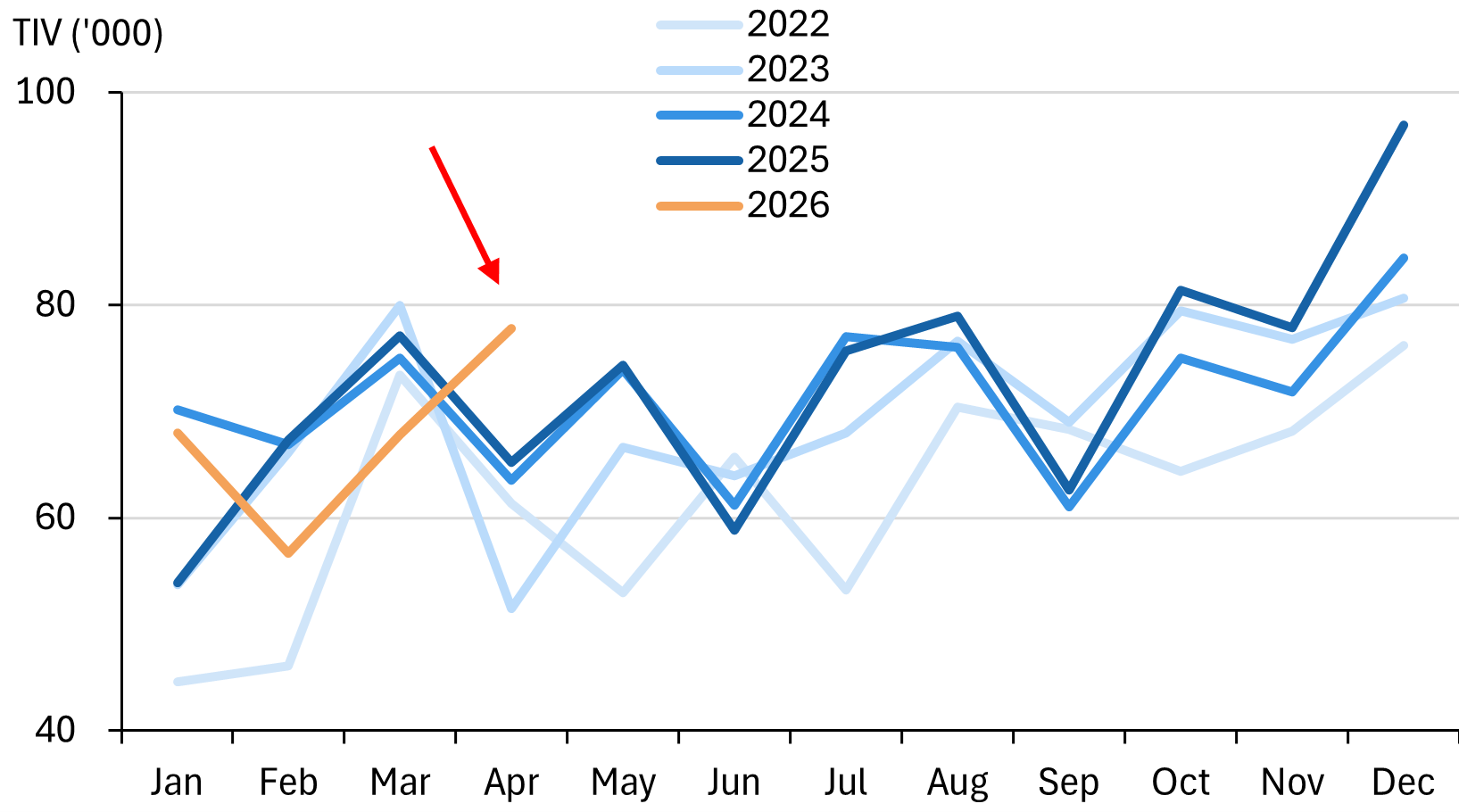

Steep post-festive rebound in April

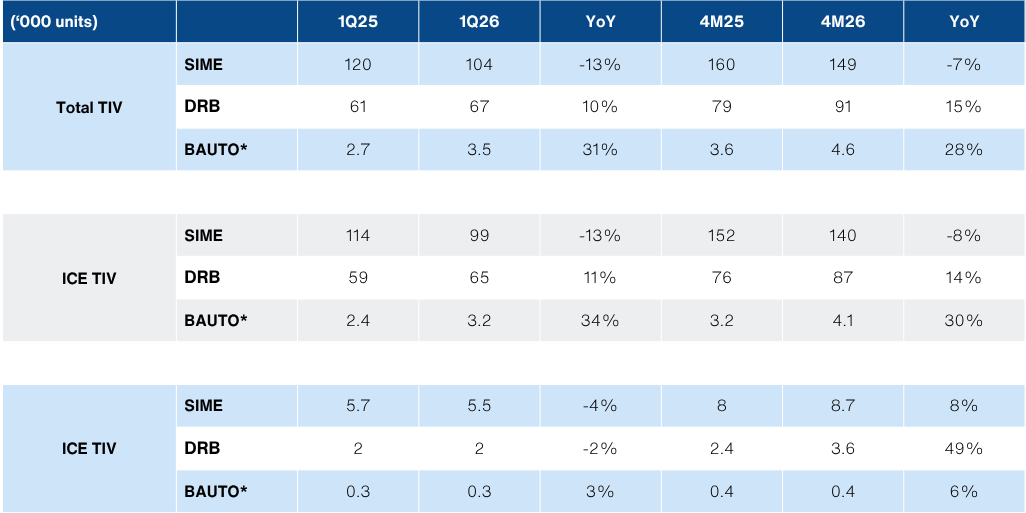

Automotive sales were soft in 1Q26, with SIME hurt the most.

Malaysia Automotive

Disclaimer: By using this information, you acknowledge that you are solely responsible for evaluating the merits and risks of any investment decision and agree not to hold NewParadigm Research liable for any damages arising from such decisions.

Key takeaways

- 1Q26 preview - big divergence, with SIME’s sales dragged down by Perodua & Toyota. EV sales a major driver for DRB. Bermaz rebounding from low-base 2025.

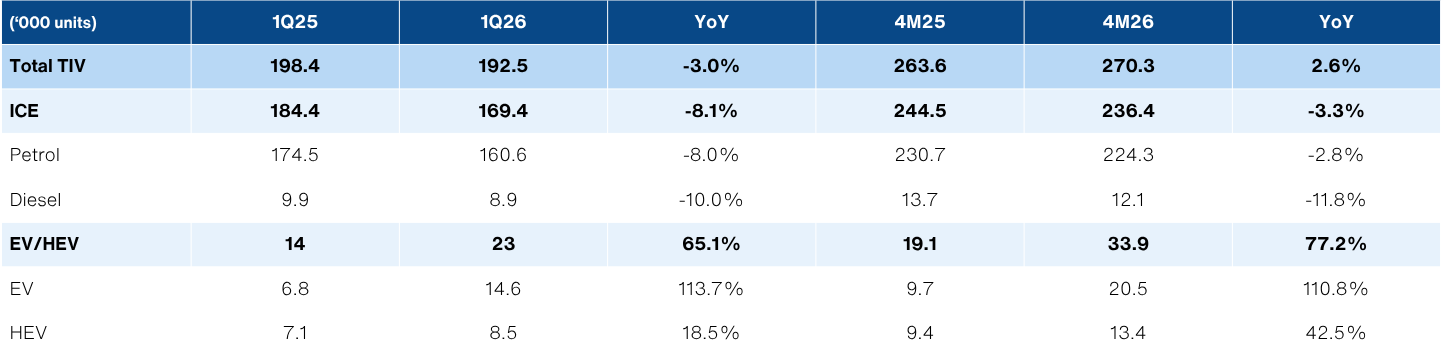

- Post-festive season drag in 1Q26, April sales surged, despite the war. 4M26 TIV +3% YoY, with EVs +111% YoY offsetting ICE’s -3% YoY.

- Positive but nuanced read-thru on consumer sentiment. Mass-market ICE models underperforming but EVs doing well on e.MAS 5 launch.

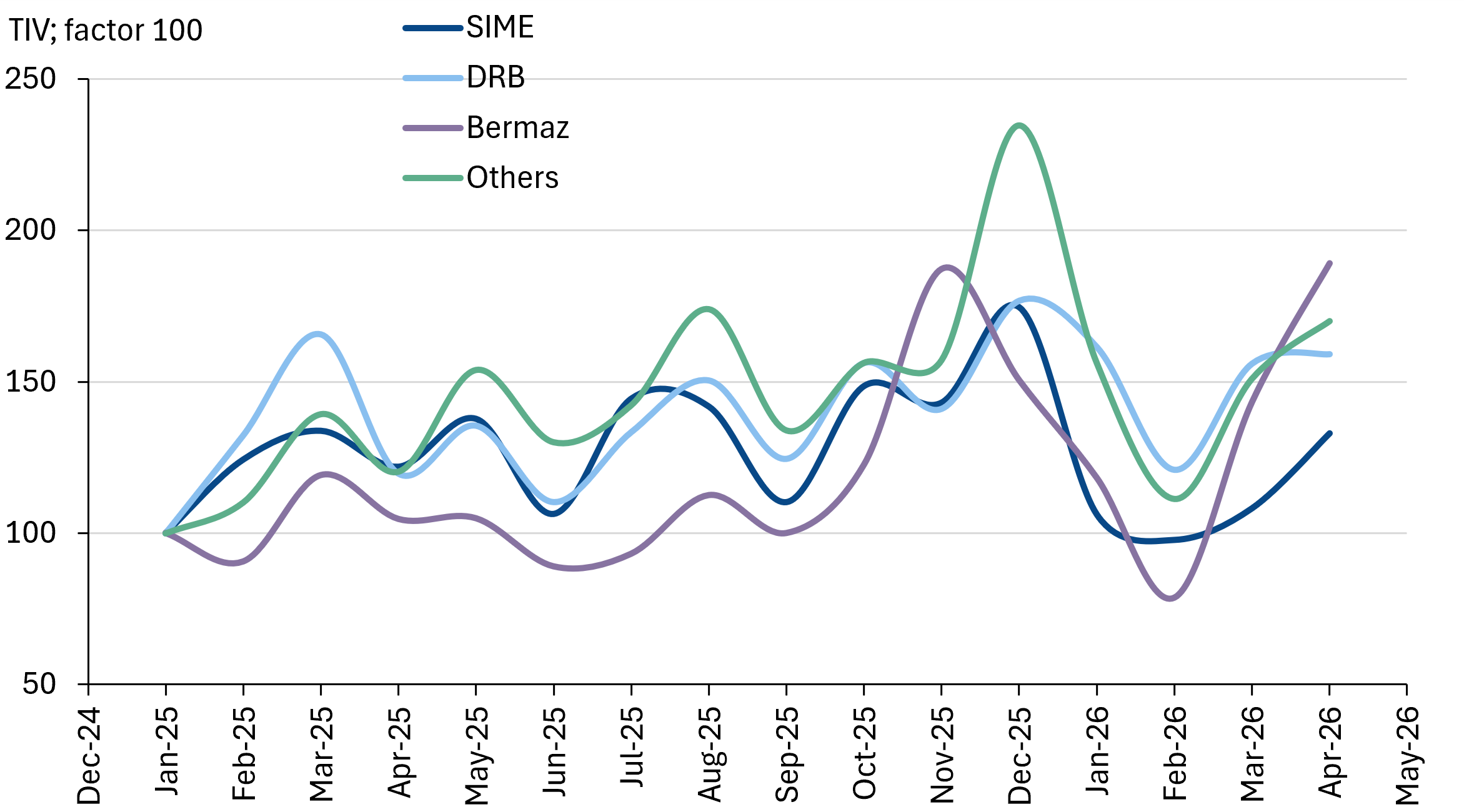

SIME hit in 1Q26 | April sales rebounded | DRB has outperformed

Source: DOSM, JPJ, NewParadigm Research, May 2026

TIV figures paint a complicated picture

- Headline 1Q26 auto sales was weak, dragged down by double festive seasons, aggressive 4Q25 discounting pulling demand forward, as well as a lack of new model launches.

- ICE: Proton’s mass-market line up appears to be taking market share from Perodua as well as resisting cannibalisation from EVs. Most notable is the -20% YoY hit to MyVi sales against the +41% YoY jump in Saga sales. Mid-market staples like the Toyota Vios and the Honda City also struggled, down -50% YoY and -29% YoY with limited recovery in April.

- EV: The strong sales of the e.MAS 5 should not be a surprise, bringing total EV sales to +114% YoY in 1Q26. But most EV models actually saw sales decelerate. Excluding the e.MAS 5, EV sales would have only grown by +16% YoY only.

- April did see a sharp rebound, but this is seasonal and typical after a festive season. It was also substantially driven by EVs (+111% YoY for 4M26). ICE sales remained in contraction at -3% YoY for the period.

Company read-thru

- SIME - We think SIME is the worst positioned from the TIV data, with sales down-13% YoY. Both its key marques, Perodua and Toyota, appear to be losing market share. Furthermore, its key EV proposition, BYD, also lost ground with the launch of Proton’s e.MAS 5 and is likely to see further pressure once the new CIF floor is imposed in July (link). We anticipate downside risk to earnings (reporting 3QFY26 ended March on 25 May), as well as forward earnings expectations, unless current market share loss can be reversed. We estimate downside risk of ~10% for the stock.

- DRB-Hicom - Sales trajectory paint the most positive picture relative to peers. Proton market share gains across ICE and EV drove sales +15% YoY (4M26), and not from a low base. In the ST, a rush to purchase competing outgoing EV models before the CIF floor is imposed could be a speed bump, but we see moderate upside (10-15%) for the stock. If not for the dilution by non-automotive segments (especially Pos Malaysia), we’d be more bullish.

- BAUTO - After the slump in 2025, the 4M26 sales recovery is encouraging. However, it is being driven by discounting and lower priced models (Mazda 3). We think this is already in the share price and are neutral on the stock’s outlook with some downside risk.

1Q26 sales were soft

Automotive sales in the first quarter of 2026 was soft, falling -3% YoY. However, it is worth noting that a sharp recovery in April has brought YTD sales back up to +3% YoY albeit driven by EVs.

Broadly, we see this as a function of the record 4Q25 year-end sales sapping demand from the seasonally weak start of the year, coupled with the seasonal festive season drag.

Looking more closely by fuel mix, internal combustion engine (ICE) sales saw a steep -8.1% YoY drop in 1Q26, but April’s recovery trimmed the drop to -3.3% YoY. In contrast, EV sales continued to surge +114% YoY in 1Q26, despite the expiry of the excise duty exemptions on CBU’s at the end of 2025. This was largely thanks to the launch of Proton’s eMAS5, which is dominating EV sales.

With the US-Iran war driving unsubsidized fuel prices through the roof, it was not a surprise to see diesel vehicle sales in particular remain depressed at -11.8% for 4M26 period.

Automotive sales by fuel type

1Q26 sales were especially weak after a record 4Q25

ICE trends - Perodua slumps, Proton surges

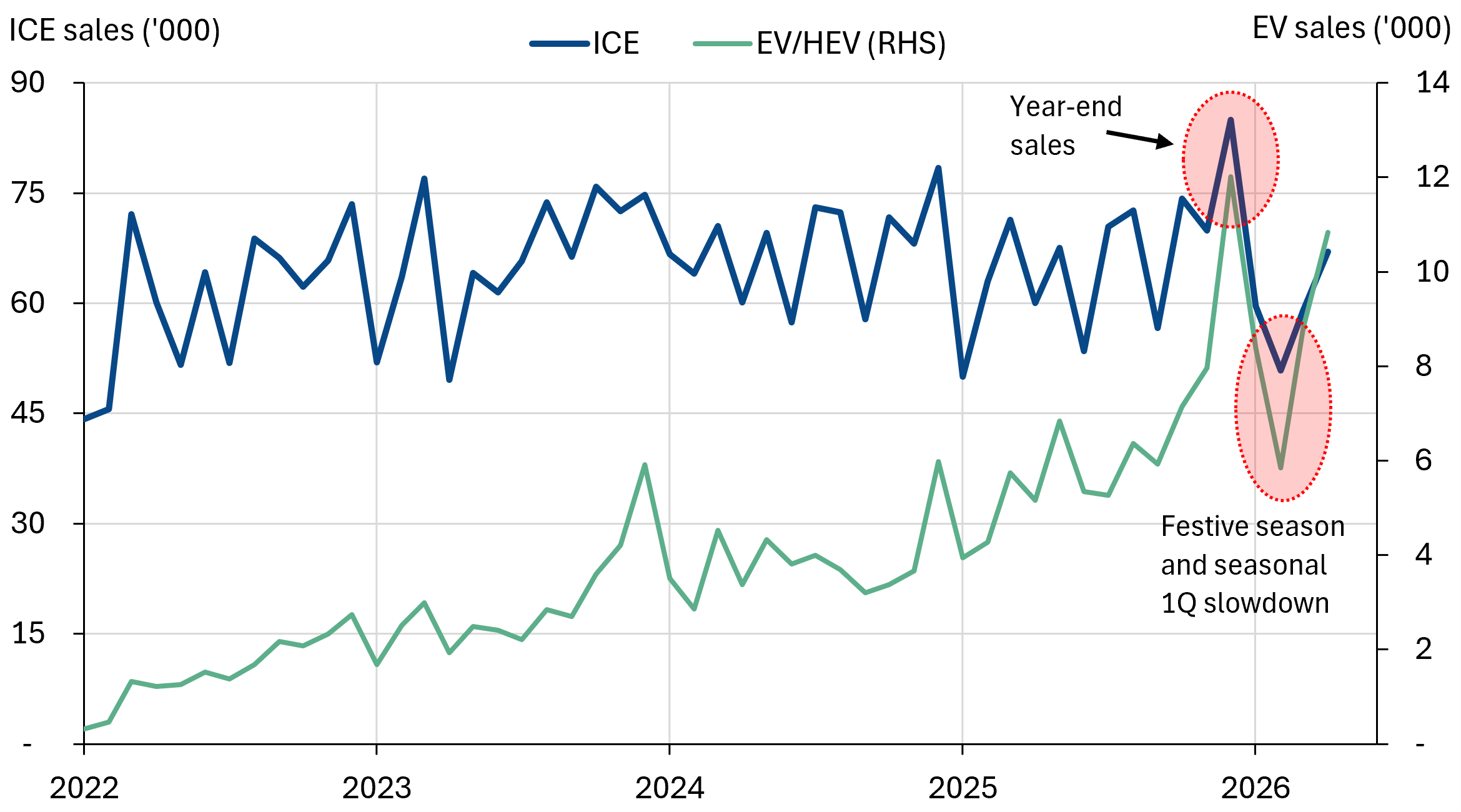

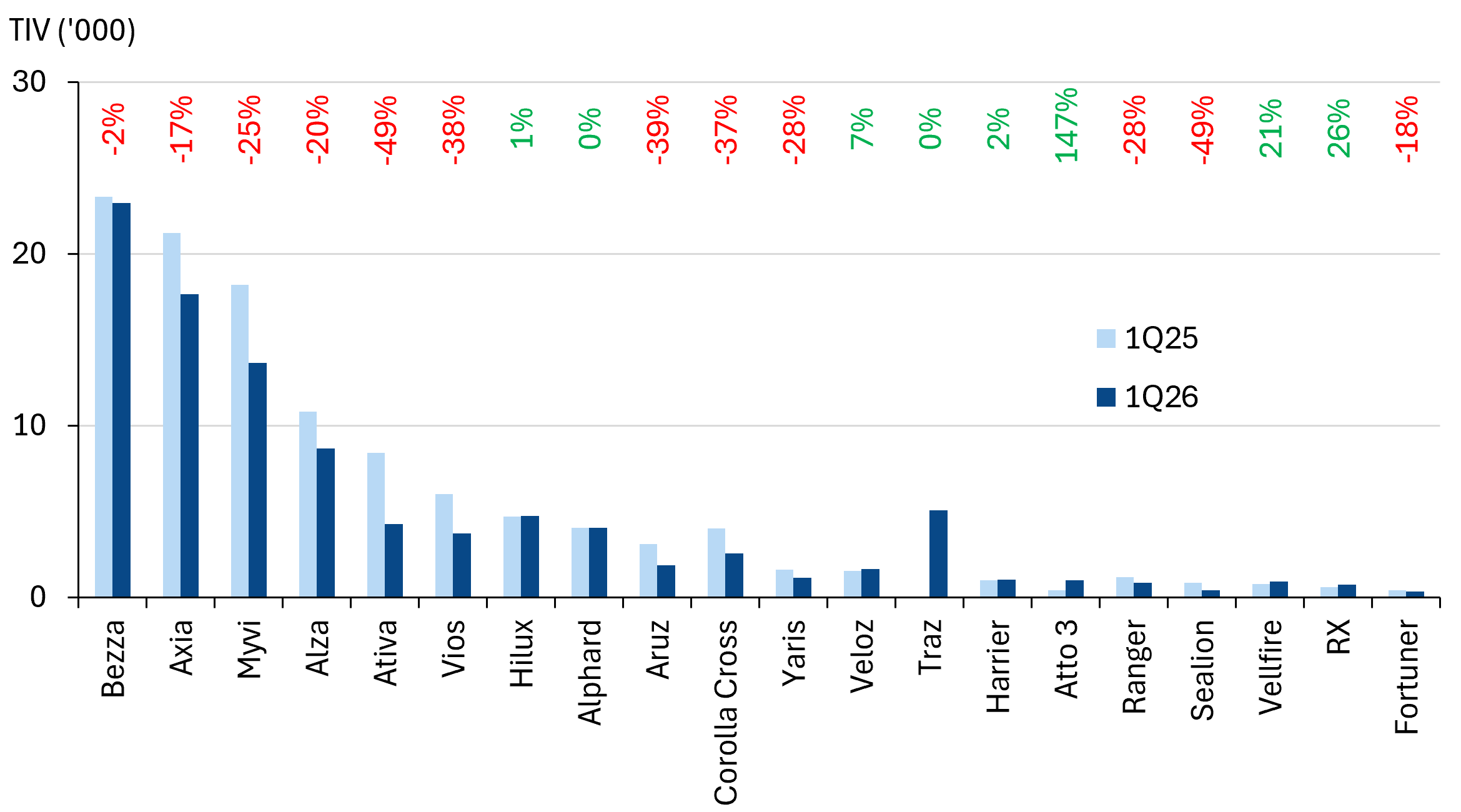

For 1Q26, we can see a very weak performance from Perodua, with key models like the Axia (-17% YoY), MyVi (-25% YoY) and the Alza (-20% YoY) substantially underperforming the broader sector.

In contrast, Proton was a clear outperformer. The Saga refresh supported a +41% YoY jump in sales, with the X50 up +41% YoY and the S70 up +31% YoY.

Another notable trend has been the stark weakness in the usual mid-market staples. The Toyota Vios and the Honda City are down-50% YoY and -29% YoY respectively. Even the top Chinese model in this segment (albeit at a higher price point of ~RM138k), the Jaecoo J7, saw sales tumble -37% YoY.

The following charts show the top 20 ICE models, which account for about 80% of total ICE sales. It is dominated by the mass market models as well as the Japanese marques.

ICE TIV (1Q26 vs 1Q25) - Perodua models underperformed; Proton shone

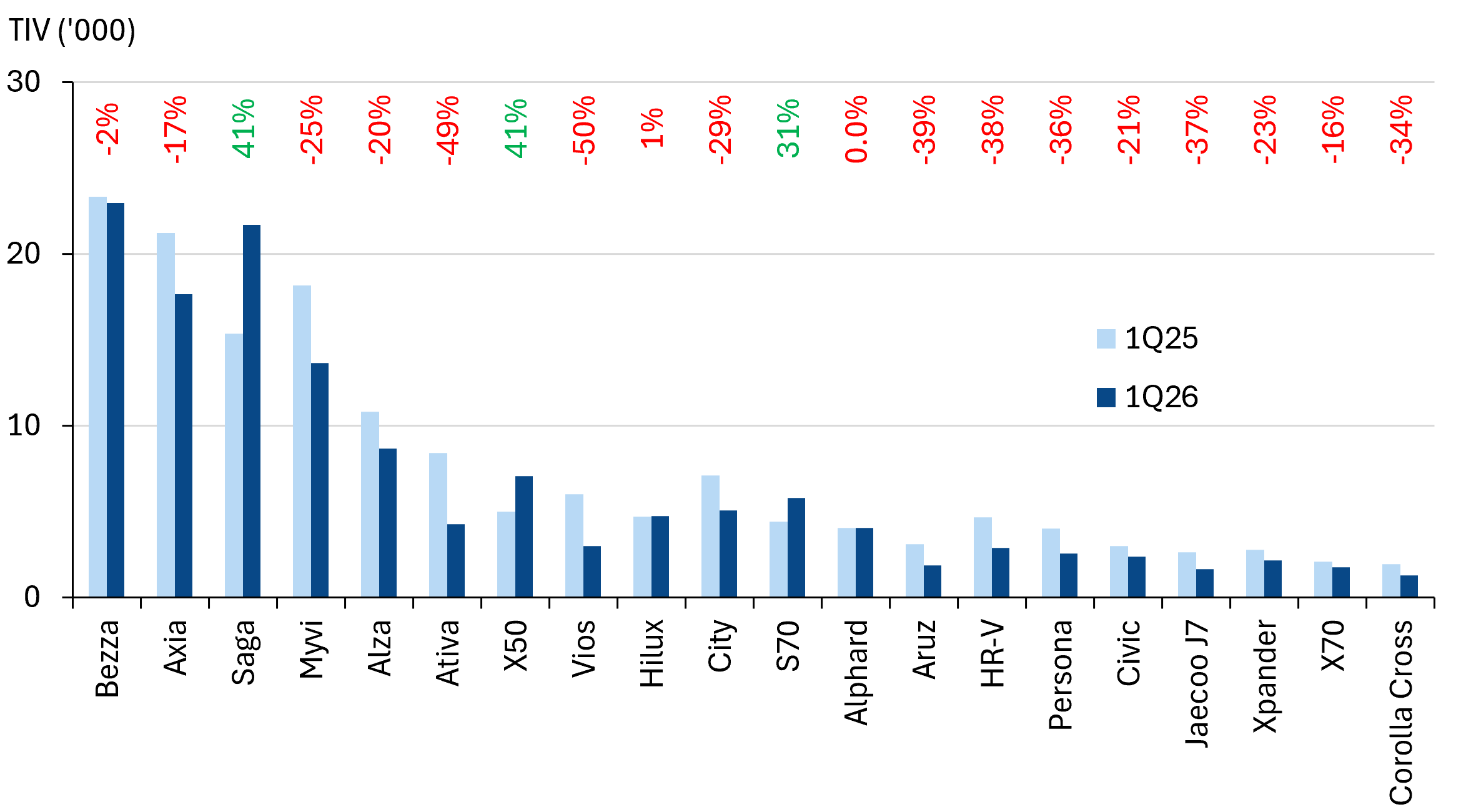

ICE TIV (4M26 vs 4M25) - Perodua recovered, mid-segment models remain weak

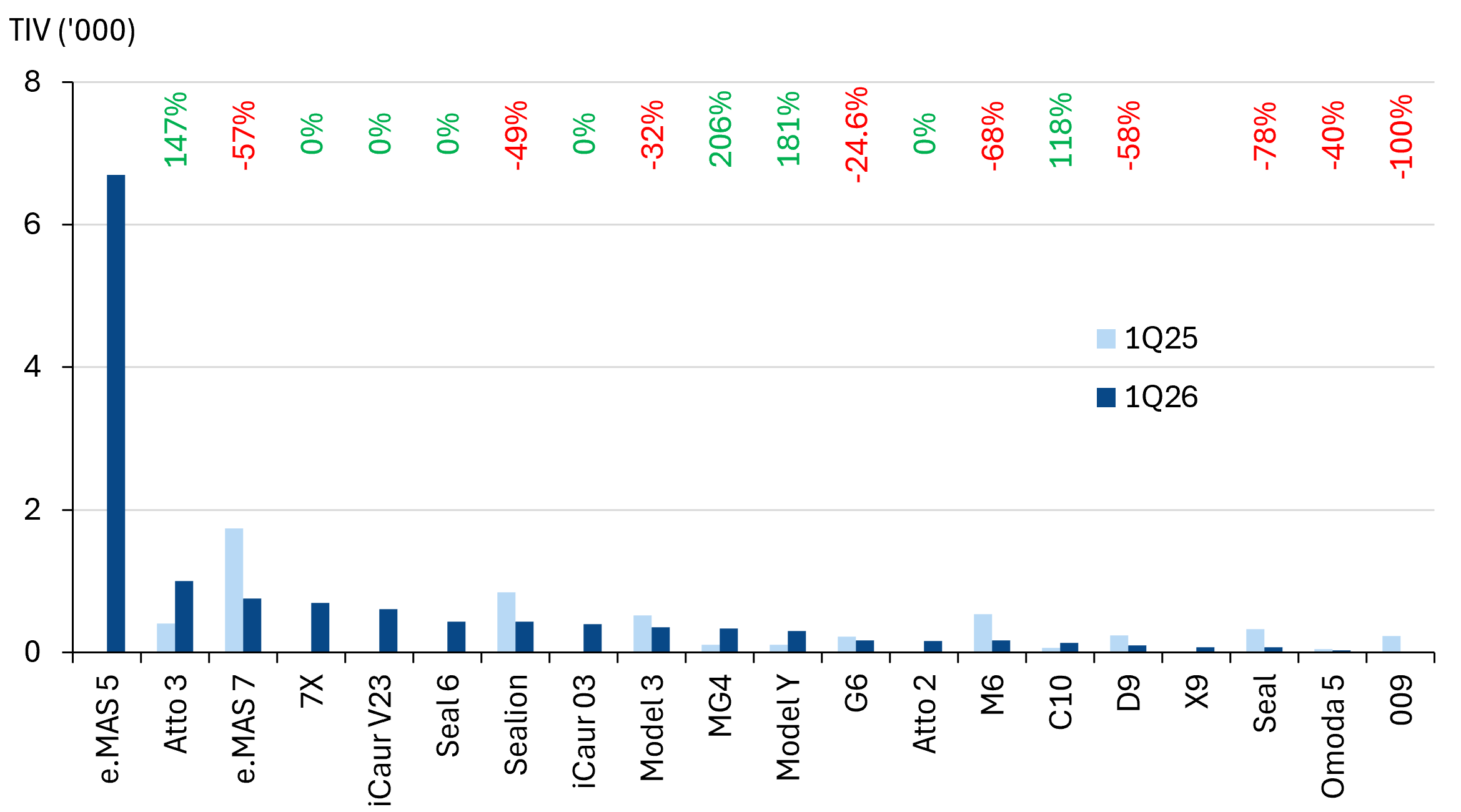

EV trends - e.MAS 5 storms in

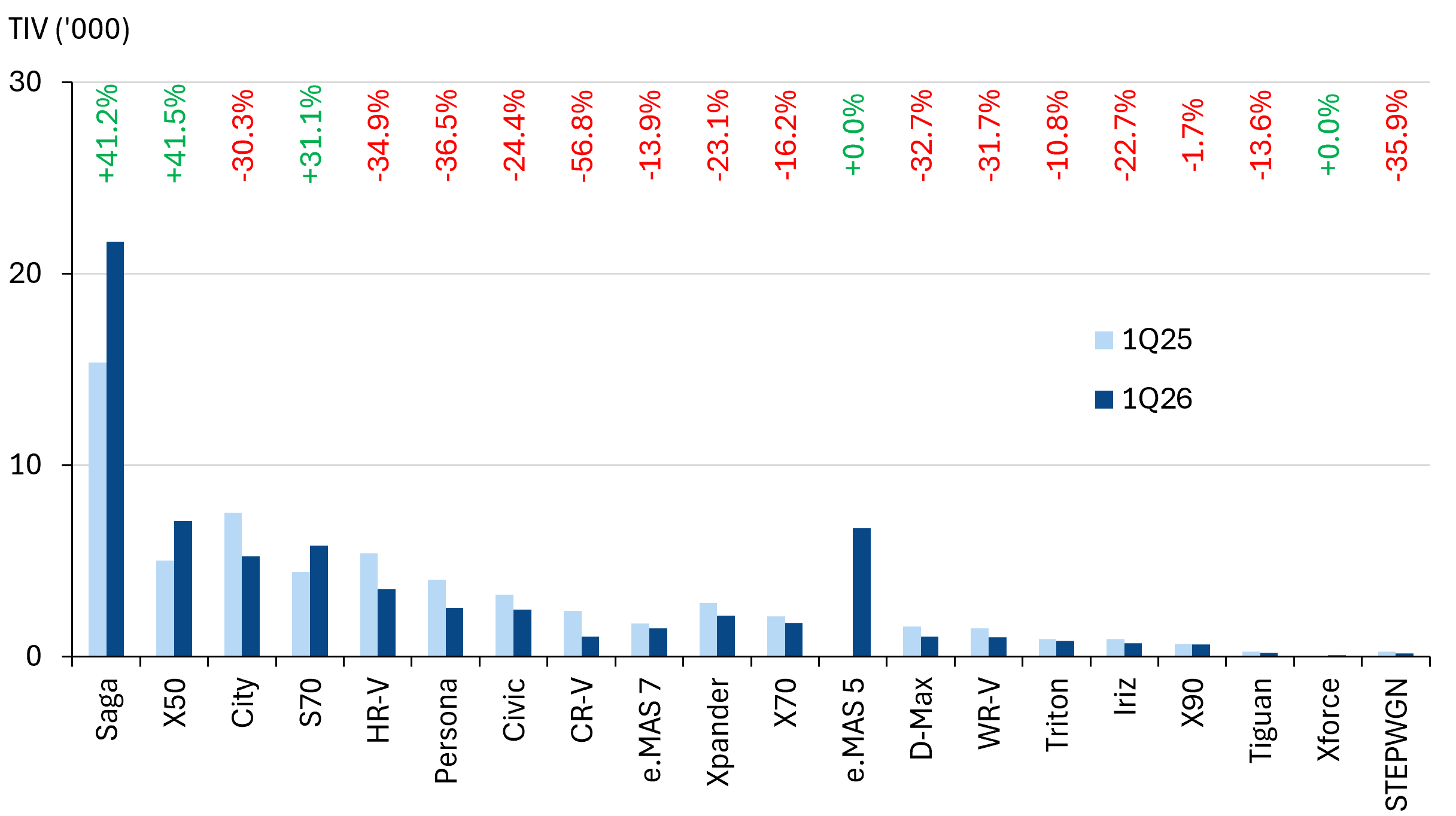

2026 is being defined by the introduction of Proton’s e.MAS 5 - the first mass-market EV. With pricing starting at RM56.8k for the basic model, the e.MAS 5's sales in the first four months of the year, the e.MAS 5 racked up 8,473 units sold. In the same period last year, the total TIV for EVs was only 9,719.

For the four months-to-date, e.MAS 5 sales now have a 41% market share. For contrast, the e.MAS 7 had a market share of 19% in 2025.

We anticipate that this has led to substantial cannibalisation of ICE sales in the same segment, likely at the expense of Perodua’s MyVi in particular. It also appears to have tempered sales for most other EVs, especially that are closer in price point - the Atto 2 (-77% YoY), Seal 6 (-48% YoY) and even the e.MAS 7 (-52% YoY).

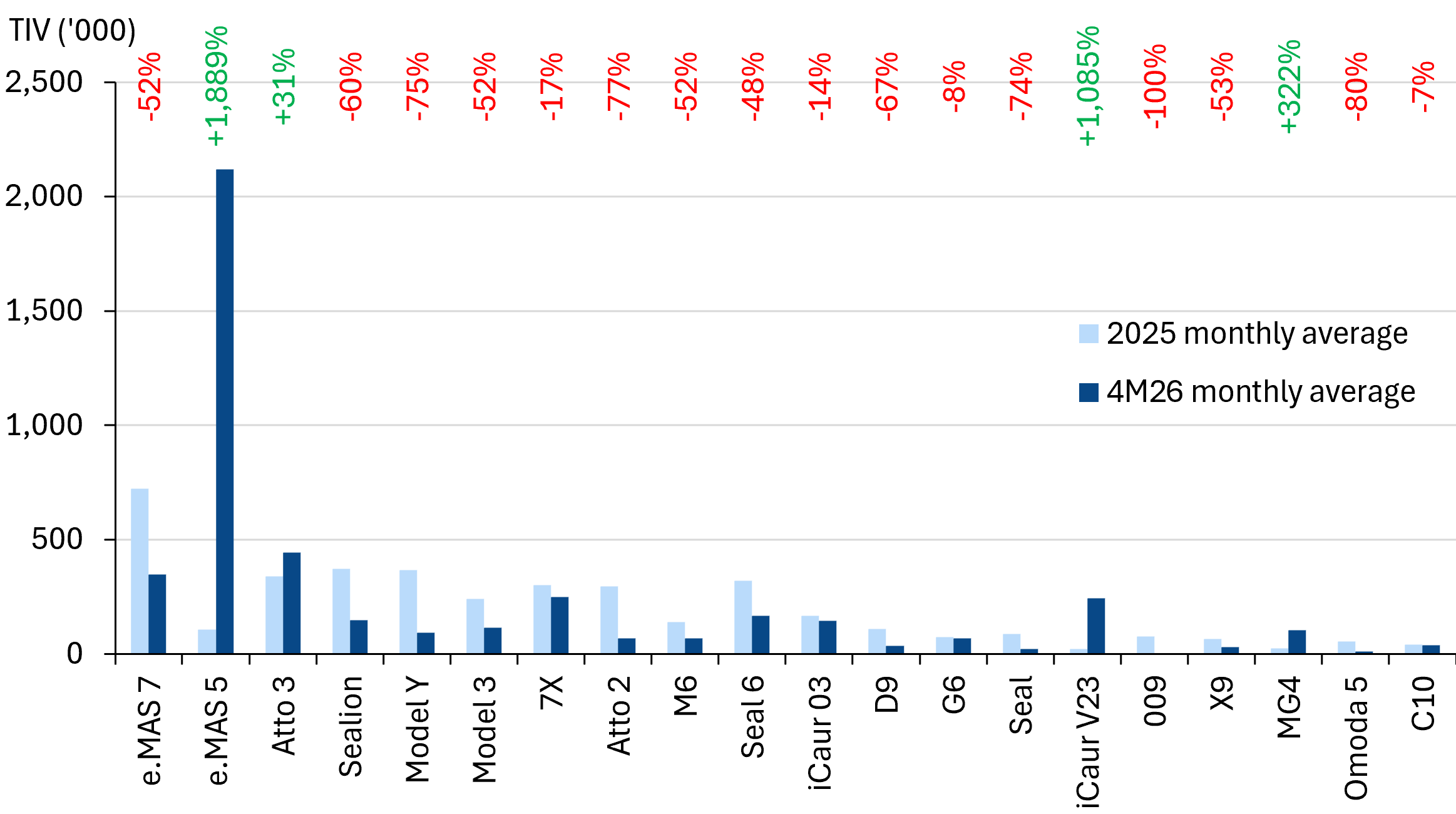

The top 20 EVs make up >86% of total TIV. Due to relatively recent launches of models, we used the monthly average sales for 2025 to compare with the monthly average sales in 2026 for a better benchmark of growth.

EV TIV (1Q26 vs 1Q25) - e.MAS 5 grabbing market share

EV TIV (Monthly average YoY) - Most EV models saw a fall in sales

Earnings preview

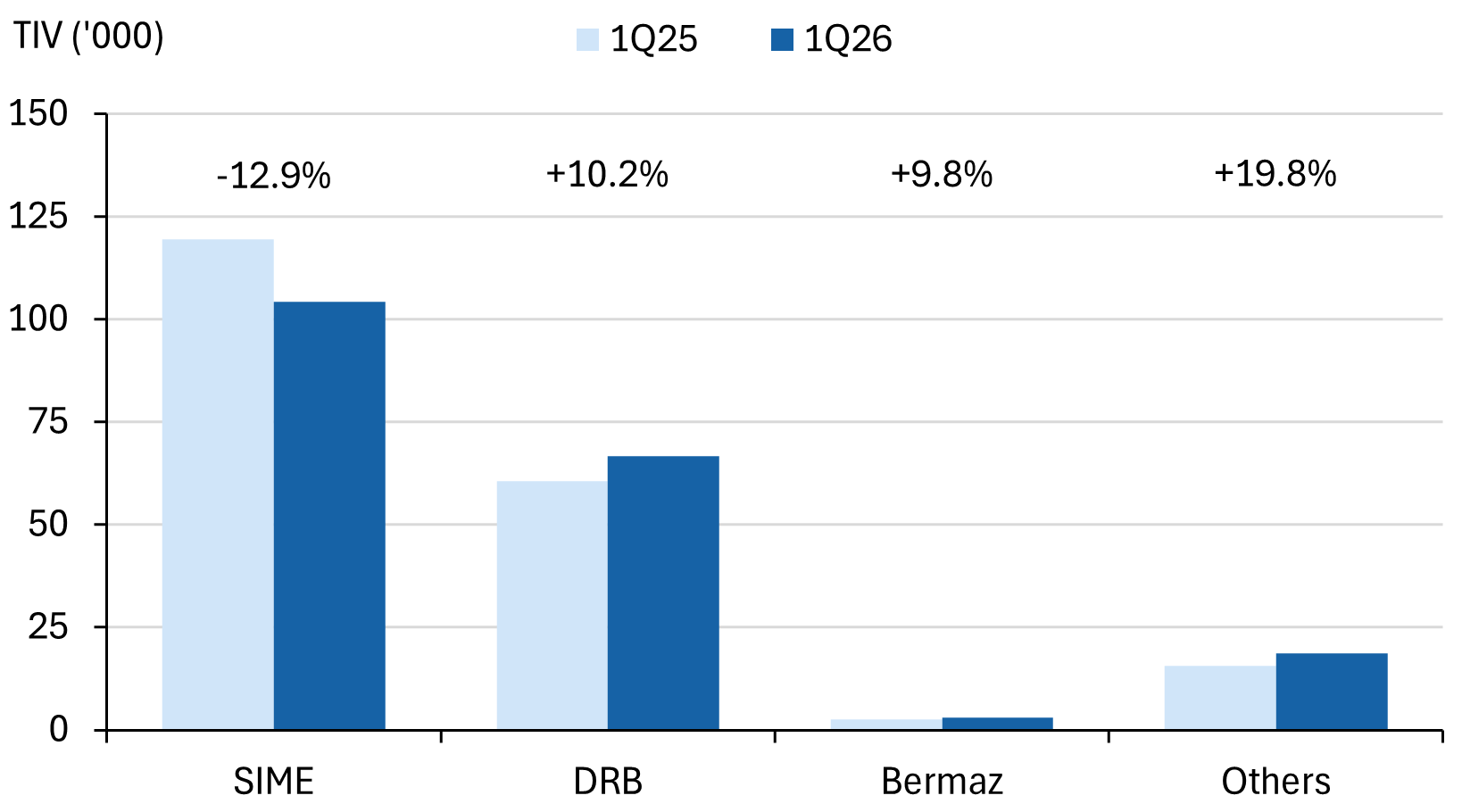

For the coming 1Q26 reporting, we see a clear divergence between Sime Darby Bhd (-7% YoY) against DRB-Hicom Bhd (+15% YoY) and Bermaz Auto Bhd (+28% YoY; April-ended).

SIME saw sales fall 7% by volume, primarily dragged down by soft Perodua and Toyota sales. The impact will be blunted by the smaller effective equity share of said brands (38% and 51% respectively).

DRB in turn, saw strong sales for in Proton - both on the ICE (+14% YoY) and EV (+49% YoY) fronts driving total TIV.

BAUTO is benefitting from a low-base effect, following weak 2025 sales. However, volumes are still about 30% lower compared with corresponding 2024 levels.

Note: We aggregated sales by company, for SIME, DRB and BAUTO based on the makes under each group. A minor shortfall to this approach, is that the aggregate sales figures will include sales by other distributors, for example Approved Permit (AP) sales. Nonetheless, we think the broad volume should reflect the underlying sales trends for each of these companies domestic sales.

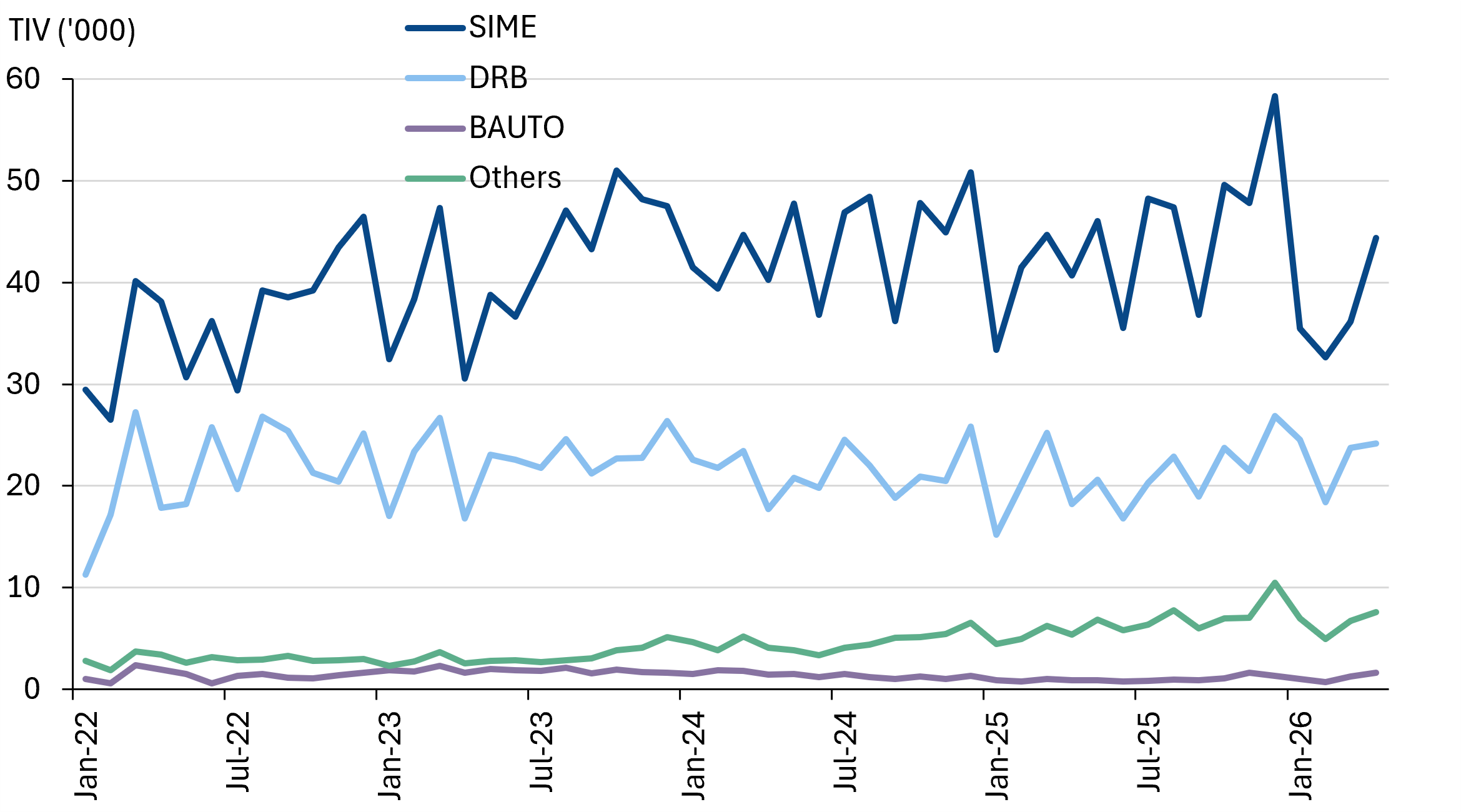

Sales by the automotive group

TIV by company

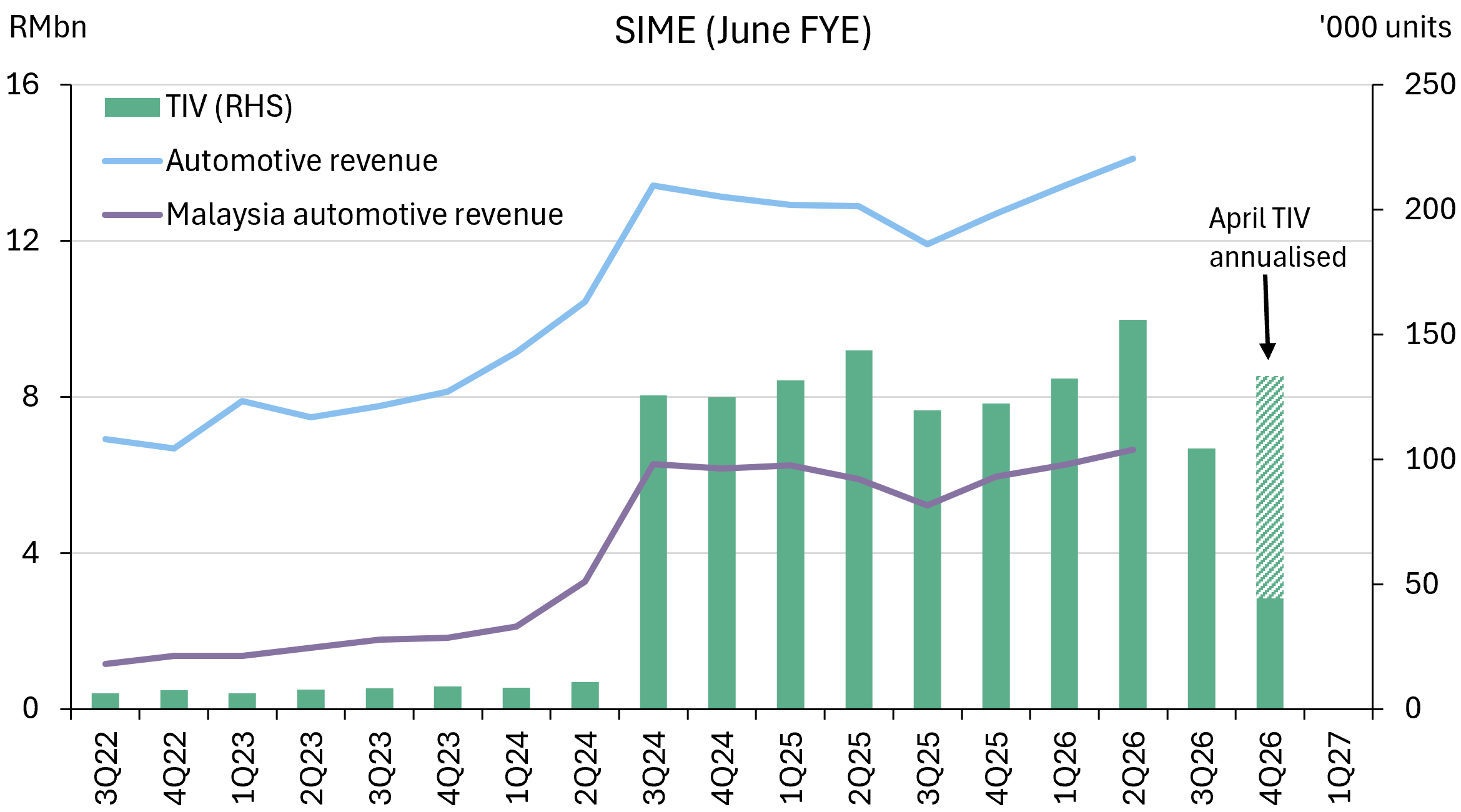

SIME - weak 3QFY26 outlook

Earnings outlook for SIME is weak for 3QFY26 (ended-March) with domestic automotive TIV falling by -13% YoY and -33% QoQ. While seasonality played a role (as well as a high-base 4Q25 on demand brought forward by aggressive discounting), weakness across key makes like Perodua and Toyota were steep, pointing to the weakest quarterly sales post-pandemic.

While Perodua did stage a rebound in April, sales for Toyota remain worrying - reflecting broader competitive pressure from affordable Chinese ICE models as well as cannibalisation from EVs. Looking ahead, the government’s move to limit CBU EVs CIF at RM200k is likely to create a rush to purchase BYD’s before the end-June cutoff, but overall negative for the full-year outlook.

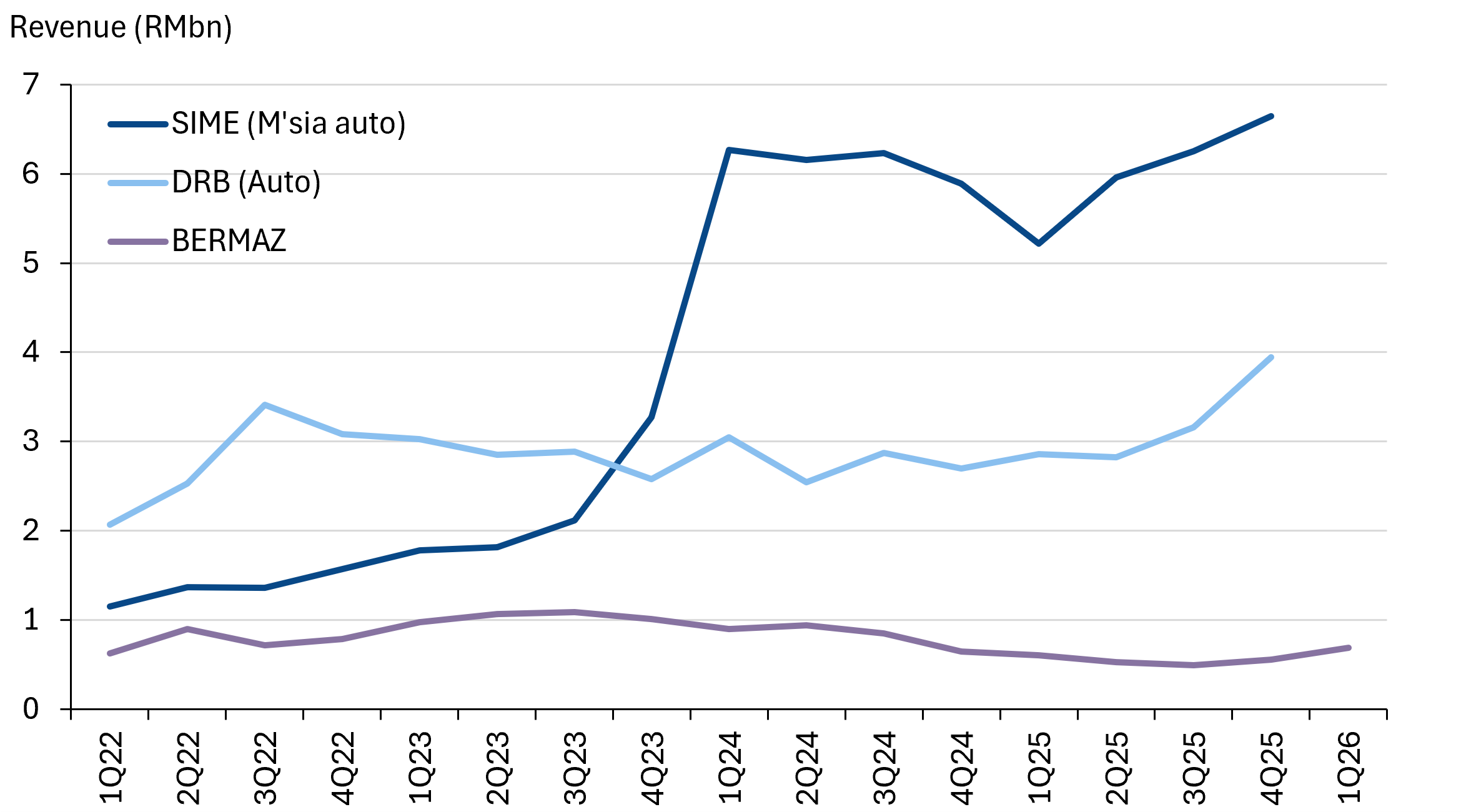

Note: SIME’s automotive revenue makes up 74% of total revenue. The Malaysian automotive revenue, in turn makes up 35% of total revenue. This report only covers the domestic sales. Also, Perodua’s contributions are captured as an associate and not reflected in the revenue. In the following chart, we have omitted the total revenue (excluded the non-automotive revenue) to streamline the presentation.

SIME revenue vs TIV

SIME top 20 models

Earnings & valuations implications

We anticipate downside risk to consensus expectations for SIME for FY26. The April rebound in sales is not likely to persist and the pressure on key Perodua and Toyota models remains a key concern.

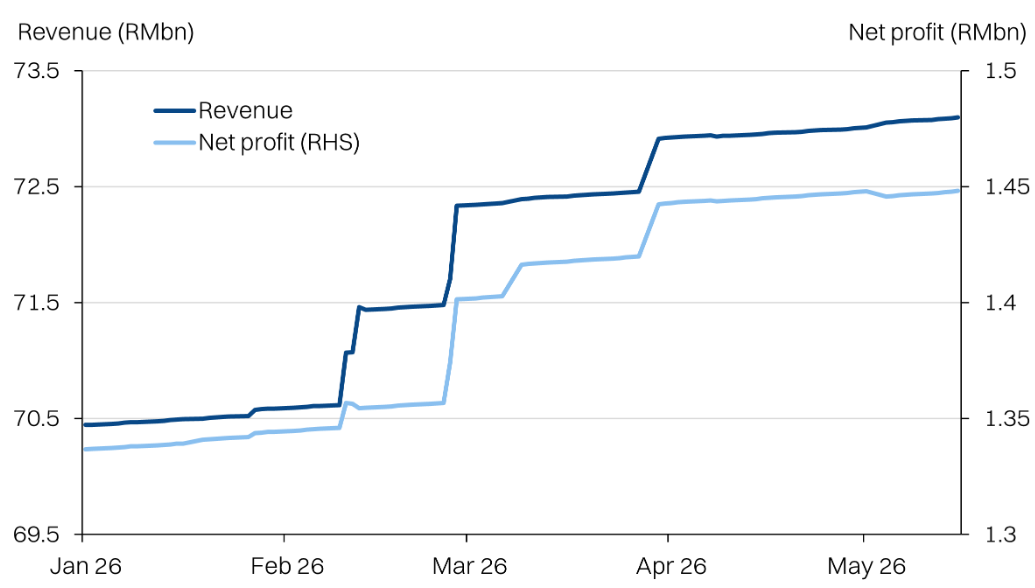

Consensus is pointing to RM72bn revenue against RM1.4bn NP for FY26, and we anticipate ~3%/5% downside risk respectively. This could be somewhat alleviated by the rush for BYD purchases before the CIF floor is imposed, but with the e.MAS 5 as competition, the sales might have to be supported by heavy discounting.

New models that could move the needle includes the Yaris Cross (starts at RM100k) that was launched in May as well as the Perodua Traz (RM76k B-segment SUV) that was launched in December.

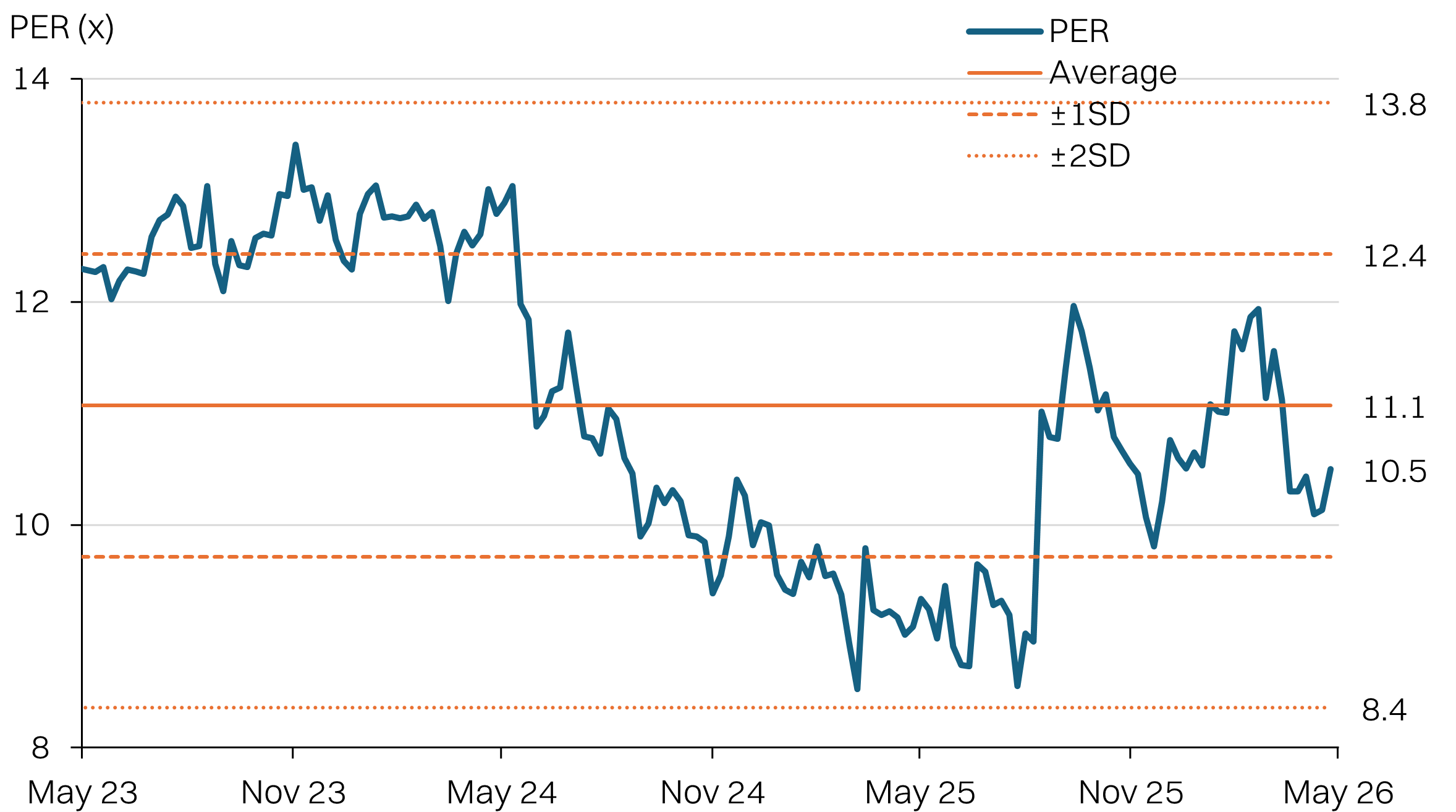

Against this backdrop, SIME is trading at 10.5x fwd PER, which is marginally below the 11.1x historic average. Against the earnings downside risk, we anticipate some room for valuations could ease round the 10x level. Overall, this translates to a downside risk of ~10% from the current levels, especially if Toyota/Perodua sales remain under pressure. We see balance of risk tilted to the downside for SIME.

SIME BF12M revenue and NP

SIME 12MBF PER bands

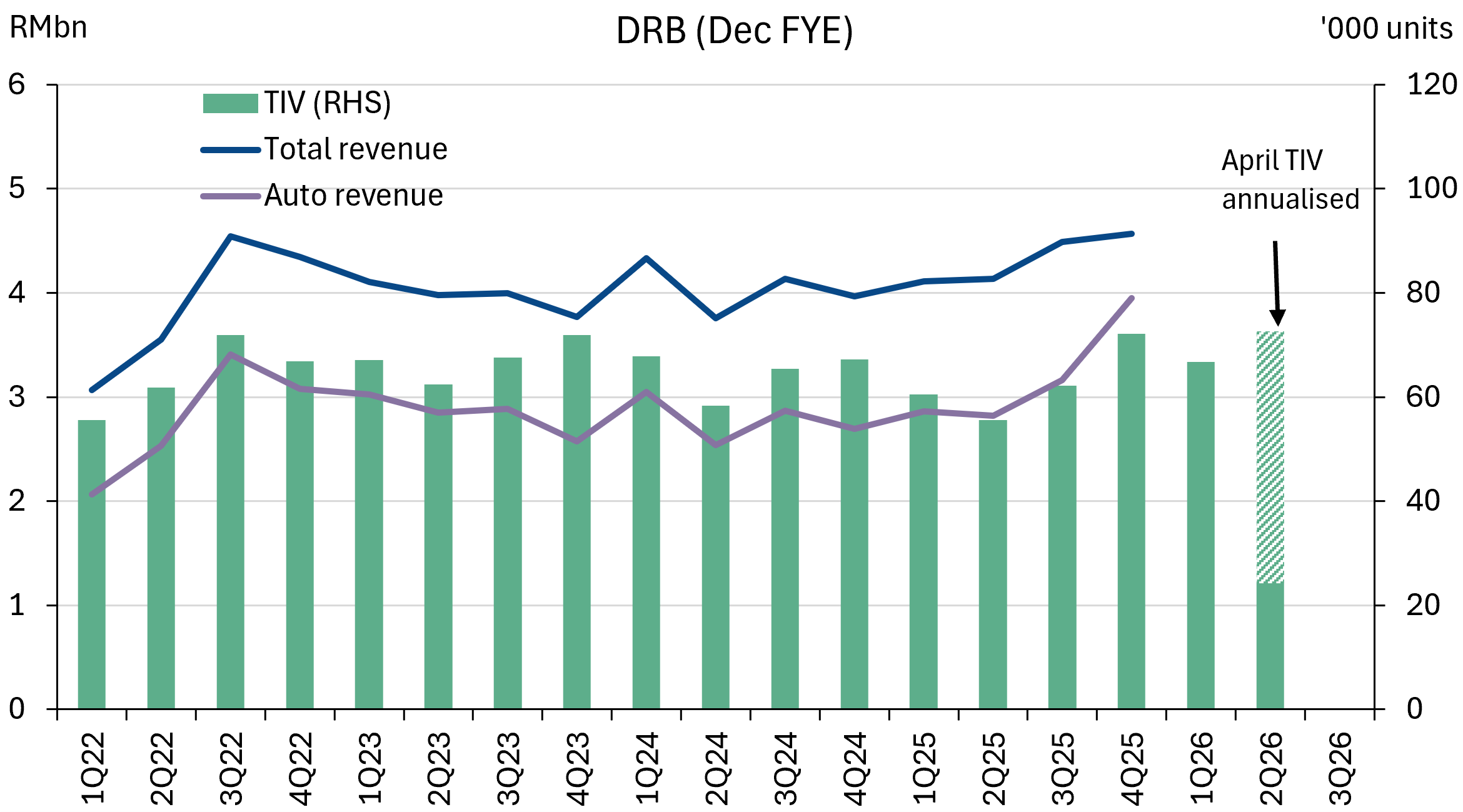

DRB-Hicom - e.MAS 5 unrivalled

Sales in 1Q26 were robust, rising by +10% YoY driven by a strong showing in Proton Saga (+41% YoY), X50 (+41% YoY) and S70 (+31%). Of course, the e.MAS 5 was also a big swing factor, delivering +6.7k units. Without the e.MAS 5 numbers, DRB’s growth would have been flat, dragged down by the weaker Honda performance: City (-30% YoY), HR-V (-35% YoY), CRV (-57% YoY).

In April, DRB’s momentum continue to improve, with 24.2k units sold. This brings 4M26 sales to +15% YoY (low-base 2025), driven by the Saga, X50, S70 and the e.MAS 5, which is now DRB’s 3rd most popular model.

Looking ahead, we anticipate the e.MAS 5 will continue to deliver strong sales given the lack of competition in this price bracket for EVs. However, we note e.MAS 7 sales could falter further in the short term, due to canibalisation by the cheaper e.MAS 5 as well as the aforementioned rush by buyers to pick up a BYD before the CIF floor is imposed (end-June).

DRB revenue vs TIV

DRB top 20 models - e.MAS 5 debut

Earnings & valuations implications

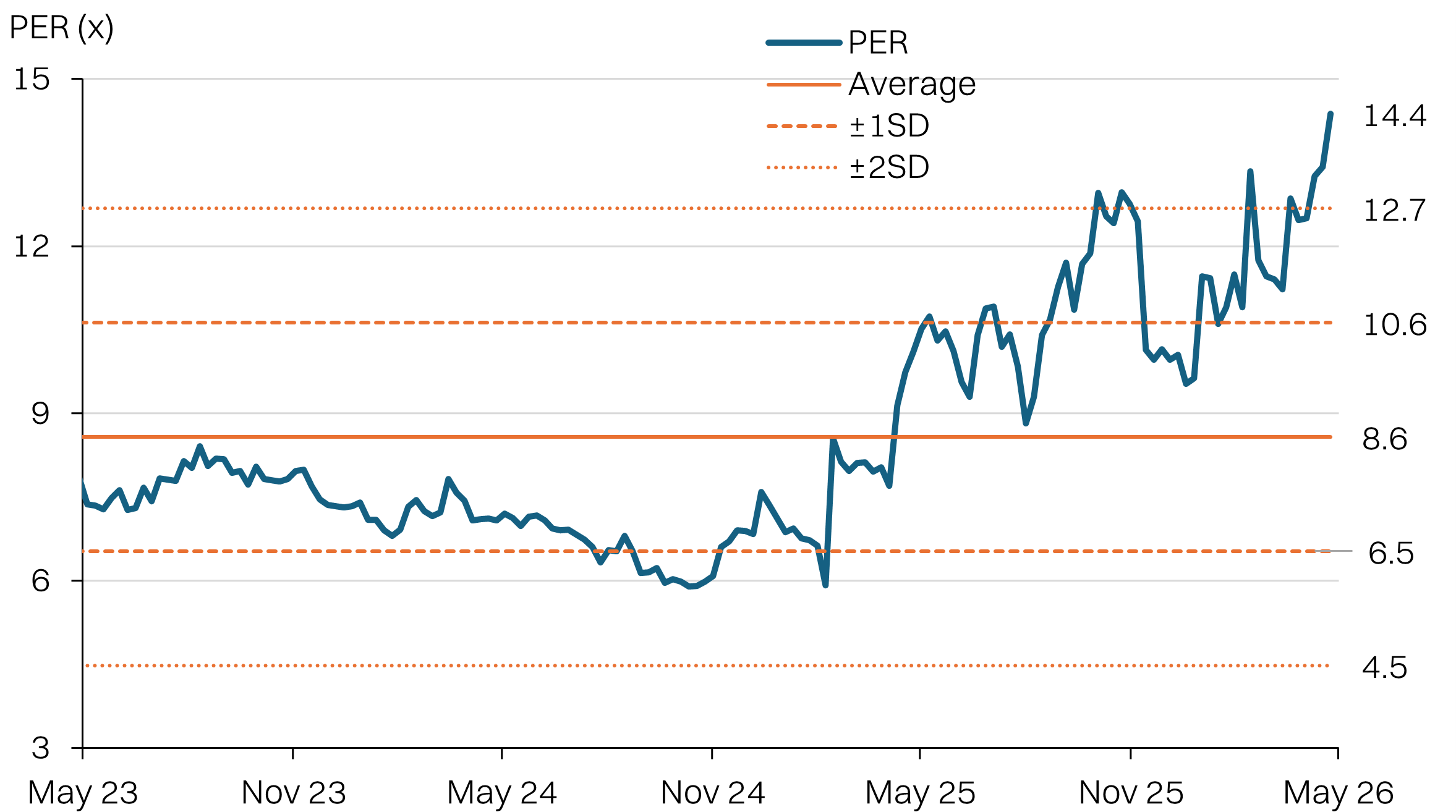

DRB has enjoyed a decent re-rating over the past 12 months, with the PER multiple rising to 14.4x 12MBF earnings. However, we do note that the consensus figures for the stock are relatively thin due to limited analyst coverage.

Furthermore, DRB’s earnings is substantially diluted by its non-automotive holdings, including loss-making Pos Malaysia (53%) and Bank Muamalat (70%). This means even if we are positive on the automotive segment performance, it could be unwound by the non-automotive performance.

That said, given that the stock is already trading at >2SD above the historic average, we, we anticipate that most of the upside from the stronger automotive sales could already be priced-in.

We’d need to see more persistent market share gain from Perodua as well as more market share gain for the e.MAS 5 to justify further re-rating of the stock. We see moderate upside risk for DRB going forward.

DRB BF12M revenue and NP

DRB PER bands

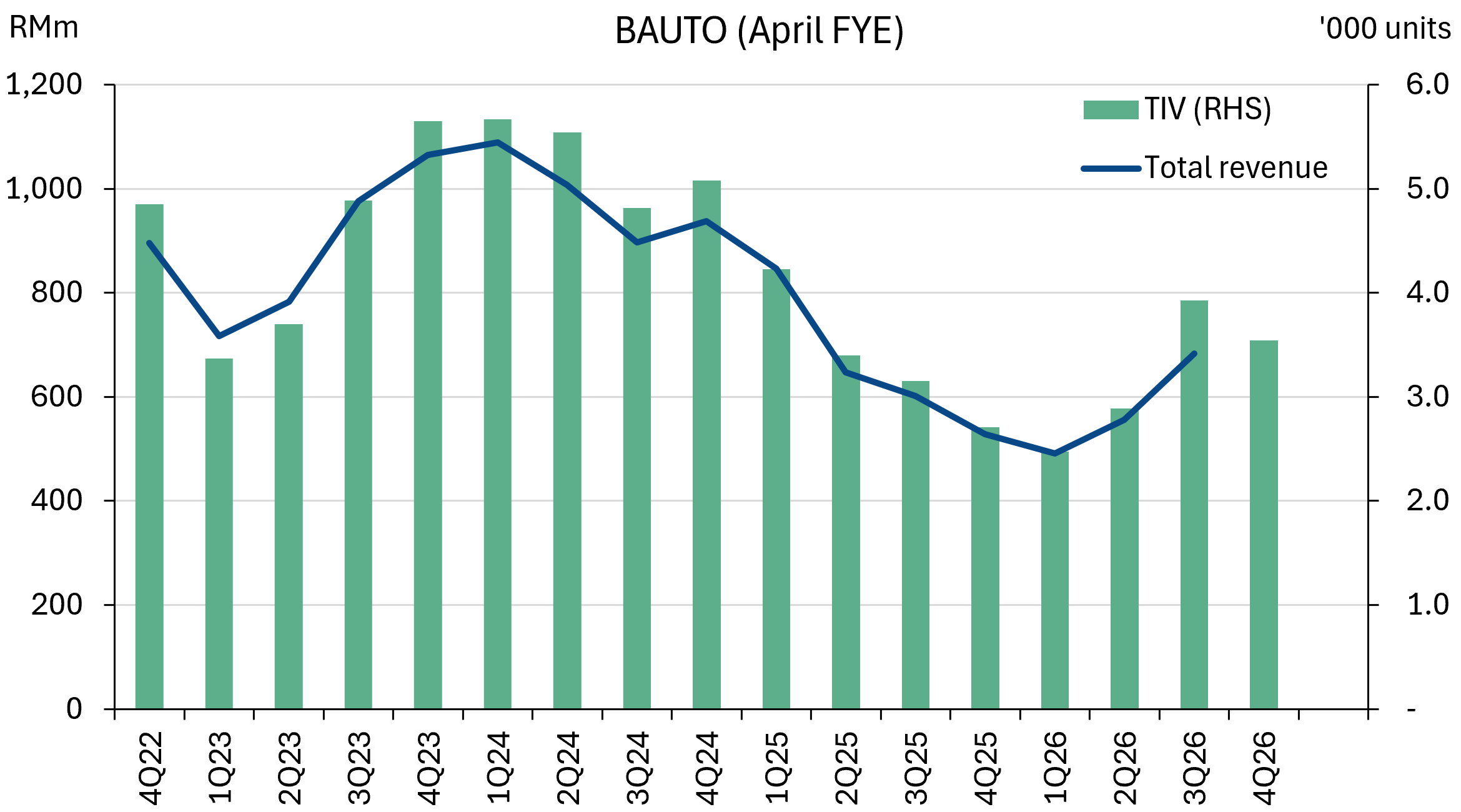

BAUTO - MAZDA 3 supporting recovery from low-base

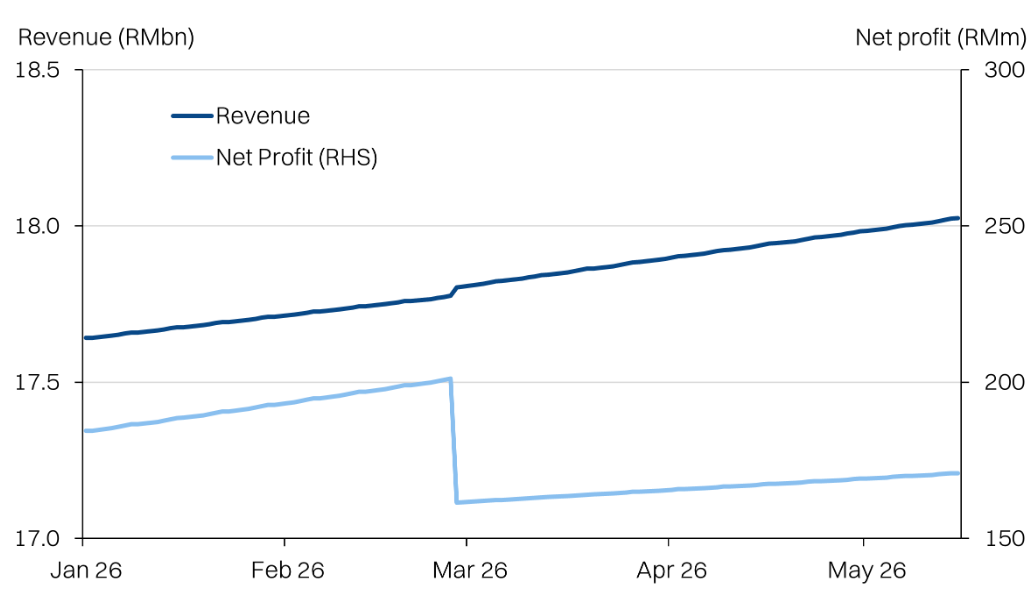

After a disappointing 2025, BAUTO’s sales showed strong +25% recovery in 3QFY26 (ended-Jan), matching the broader industry’s record year-end sales.

Come 4QFY26 (ended-April), BAUTO’s sales remained above the low-base 2025, growing by +31% YoY. Note that 4QFY25 and 1QFY26 marked the low-point of BAUTO’s sales in that period.

The bright spot for BAUTO appears to be the Mazda 3, which saw sales hit 676 units in April, solidifying itself as the top selling model at 41% of total sales. Note that the 1.5l variant was launched in November 2025 with pricing starting at RM119.6k - roughly RM30k cheaper than the previous variant, despite various spec bumps.

In turn, we anticipate that BAUTO’s revenue growth will be more muted due to falling ASPs. Margins should also be suppressed due to the broader price cuts.

BAUTO revenue vs TIV

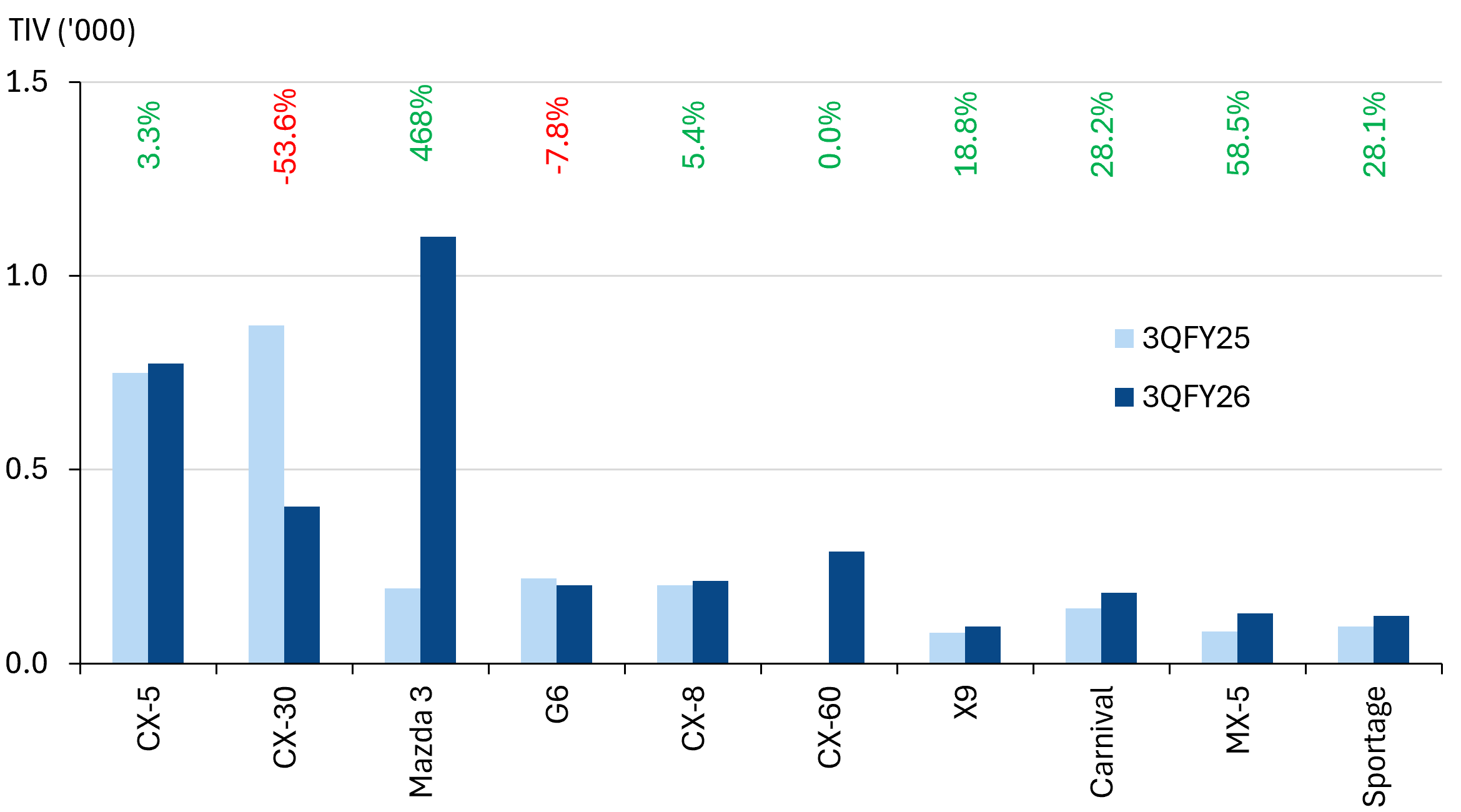

BAUTO top model sales

Earnings and valuations implications

BAUTO Should be able to meet consensus expectations, given the implied 4QFY26 (ended-April) consensus expectation is very low - only RM509m. The TIV figures suggest ~10-15% upside to that number. However, when looking at FY27E outlook, we flag downside risk from the CIF floor implementation for EVs, that could hurt some of BAUTO’s portfolio - most notable is the XPENG G6 (priced at RM158k). Similar to SIME, there could be a small rush to secure purchases ahead of the cutoff.

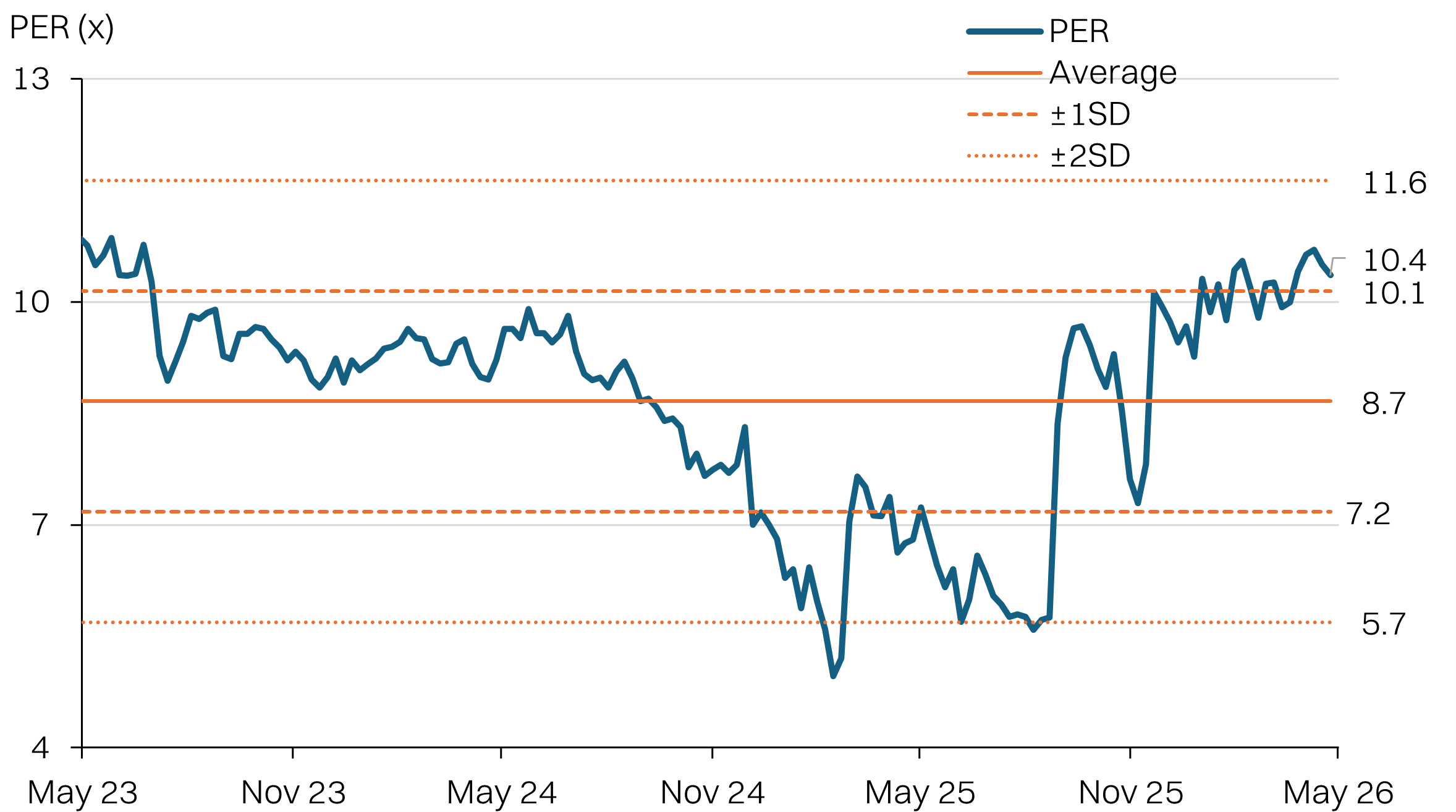

However, when we look at valuations, it looks like the earnings recovery by BAUTO is fully priced-in. BAUTO’s PER multiple is already recovered to 10.4x 12MBF PER, which is >1SD vs the historic average.

Positive optics from headline growth (thanks to the low-base effect from 2025), could continue to support the valuations. However, we anticipate risk is tilted to the downside for consensus FY27E earnings, given the sales volume is shifting to more affordable models (Mazda 3) coupled with the downside to the XPENG EV sales.

In short, we see balance of risk to the downside for BAUTO.

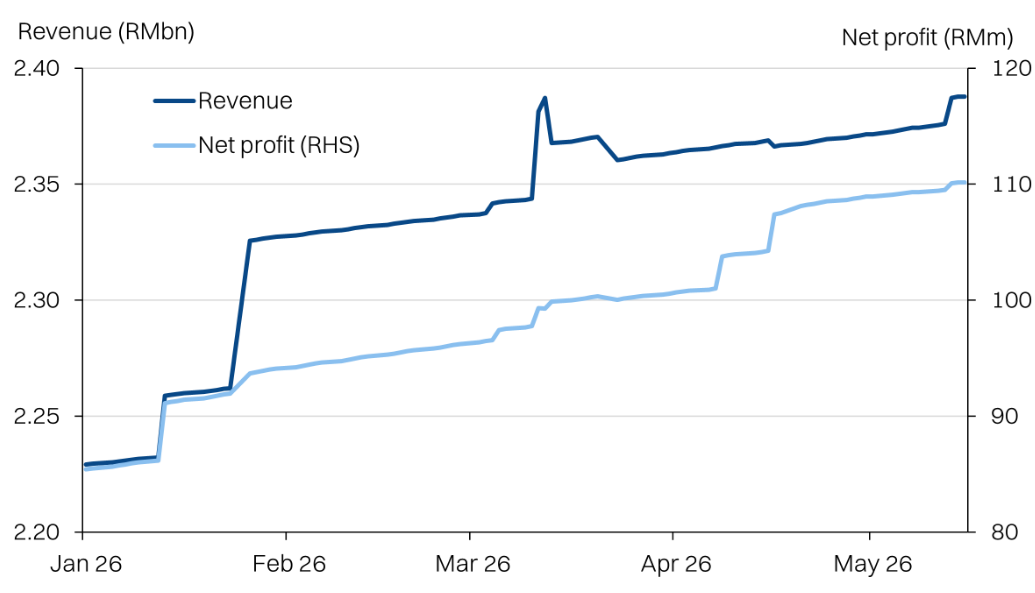

BAUTO BF12M revenue and NP

BAUTO

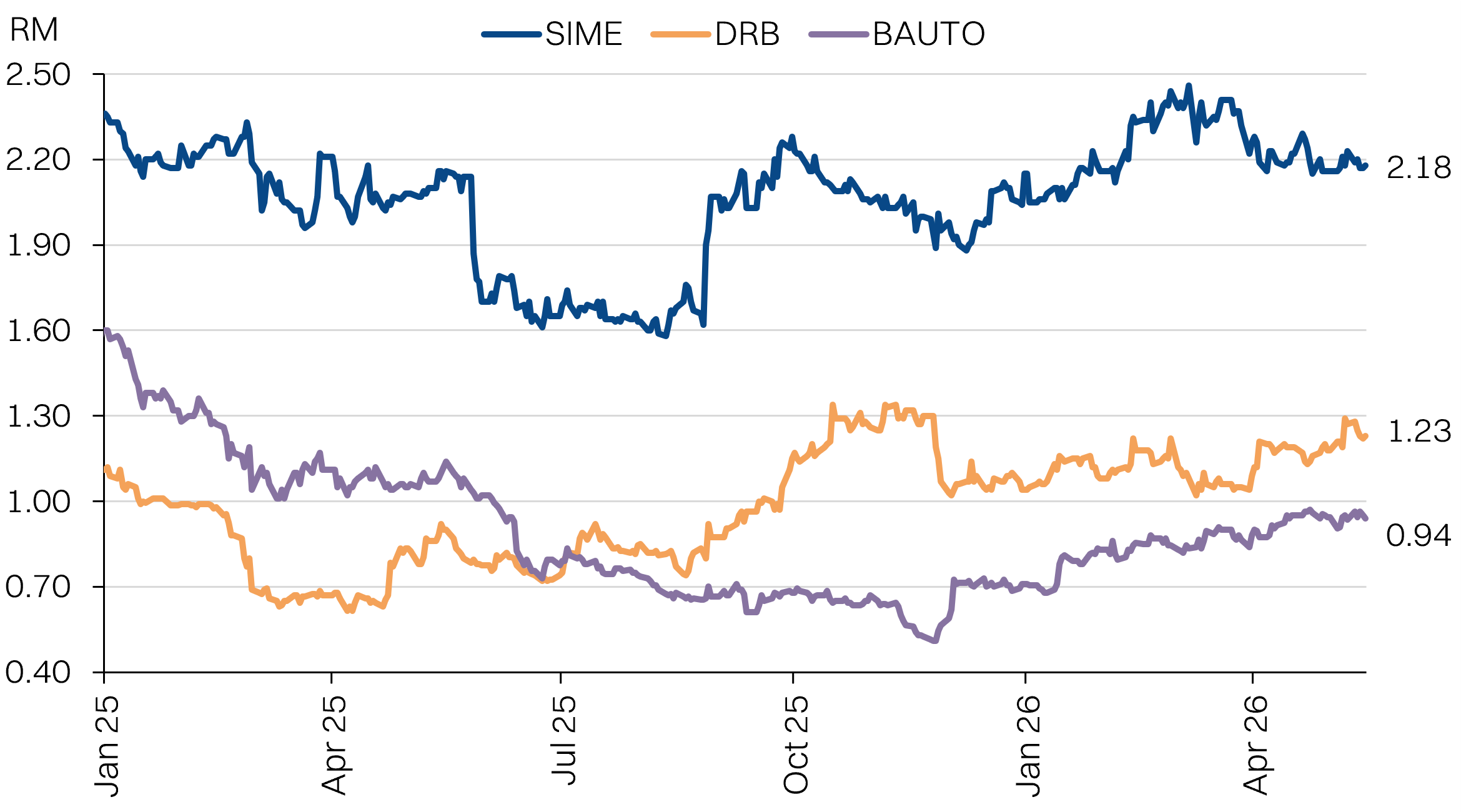

Share price performance

Reported revenue