Demand curtailment presents buying opportunity

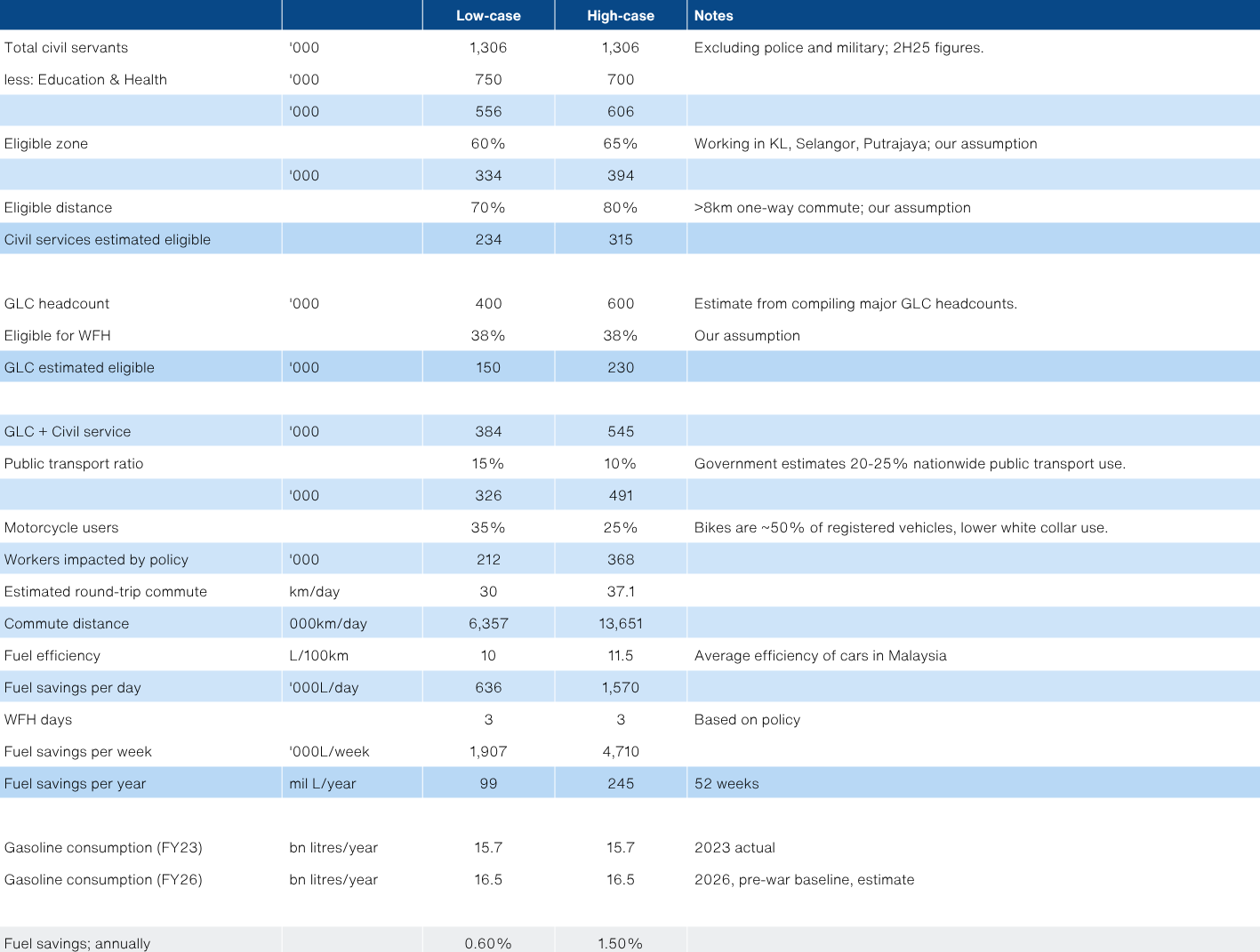

The government's WFH policy might only trim fuel demand by ~1.5% at best.

PETRONAS DAGANGAN

PETD | 5681.KL

Not Rated

Fair value: RM20.90

Last price: RM21.22

Market cap (RMm): RM21,081m

Shares out: 993m

52-week range: RM16.84 / RM23.58

3M ADV: RM17.7m

T12M returns: 20%

Disclaimer: By using this information, you acknowledge that you are solely responsible for evaluating the merits and risks of any investment decision and agree not to hold NewParadigm Research liable for any damages arising from such decisions.

Key takeaways

- Retail fuel demand management implemented for public sector is small. We estimate 0.6-1.5% annual fuel savings only.

- We estimate up to 25% demand curtailment might be needed if the war is prolonged, suggesting private sector companies could be nudged to increase WFH at a later stage.

- But even with the hard lockdowns of the pandemic, PETD was still profitable. We estimate ~25% earnings downside from demand curtailment, at worst, with a corresponding FV floor of RM19.00.

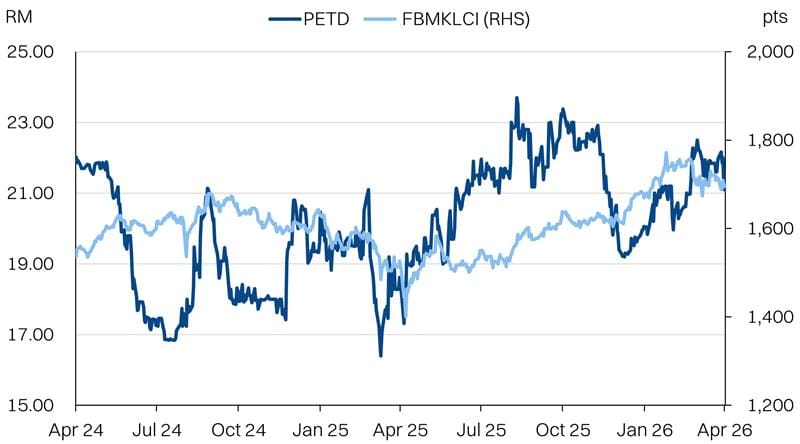

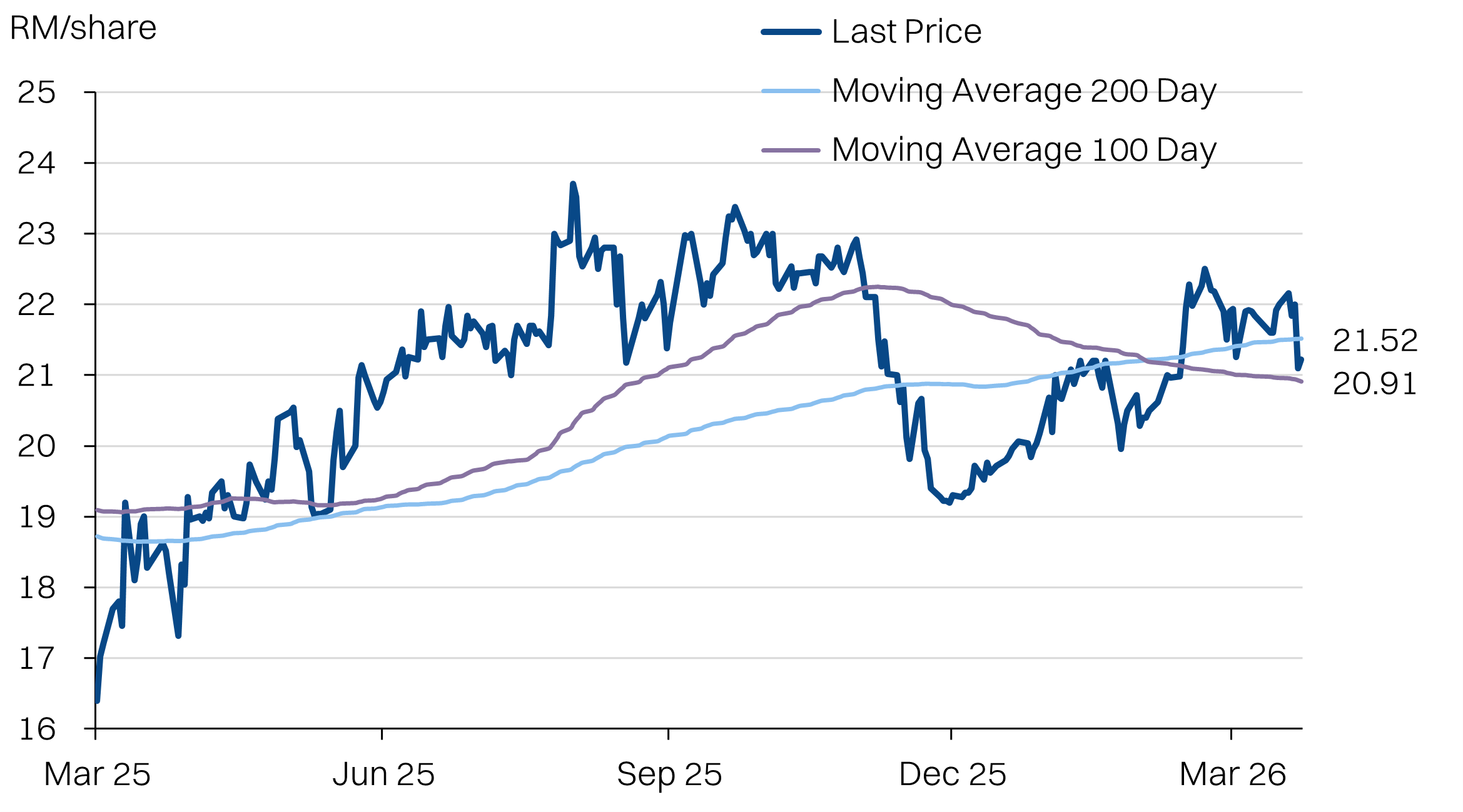

Share price performance

Investment fundamentals

| RMbn (FYE Dec) | FY23A | FY24A | FY25A | FY26E |

|---|---|---|---|---|

| Revenue | 37.5 | 38 | 38.3 | 42.1 |

| Growth YoY | 2% | 1% | 1% | 5% |

| EBITDA | 1.8 | 2.0 | 2.0 | 1.5 |

| EBITDA margin | 4.83% | 5.33% | 5.28% | 4.00% |

| Adj NP | 0.9 | 1.1 | 1.1 | 0.83 |

| Adj NP margin | 2.51% | 2.86% | 2.90% | 2.00% |

| ROA | 8% | 10% | 10% | 7% |

| PER (x) | 23.01 | 17.66 | 18.05 | 25.6 |

| Yield | 3.80 | 5.00 | 5.30 | 4.00 |

Source: Company data, NewParadigm Research, April 2026

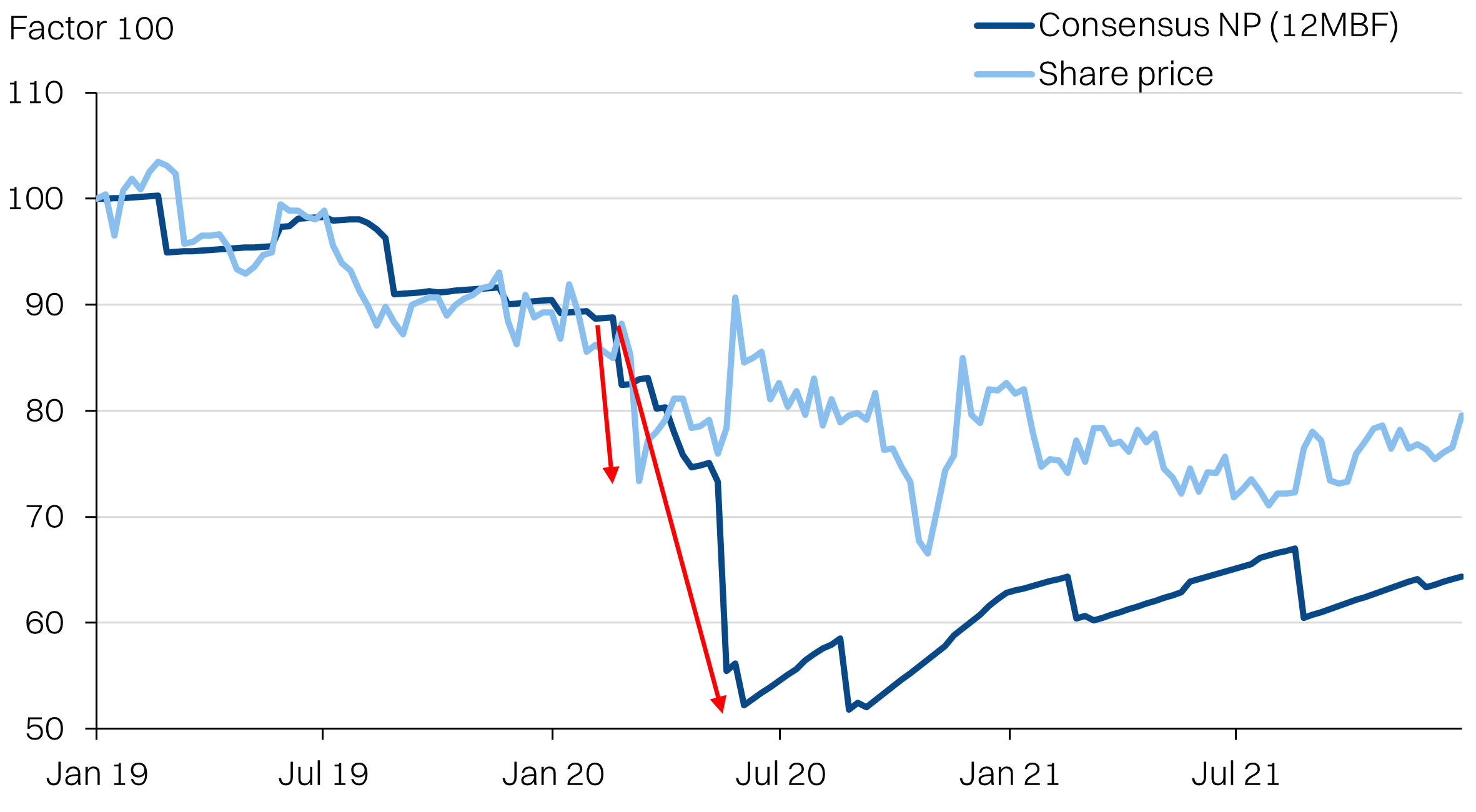

Lessons from Covid-19

- PETD is highly resilient to transient demand shocks. Even at the peak of pandemic-induced lockdowns, PETD remained profitable for the full year with RM285m NP (-65% YoY) in FY20. At the same time, the share price fell -28% peak-to-trough.

- We estimate the fuel savings from the work-from-home (WFH) policy is only 0.6% to 1.5% on an annualised basis. This is very small, implying at most an additional week of fuel reserves. However, this excludes potential compliance from the private sector as well as the impact of demand destruction from the higher prices on unsubsidized consumers (RON97 and diesel), the reduction of the Budi95 quota to 200L, and the hit to commercial demand.

- Critically, we anticipate more demand curtailment will be needed if the war prolongs. This means more policies to encourage/compel/expand WFH is likely to be announced the longer the war drags on. This could weigh on the sentiment of PETD.

- Malaysia’s gasoline exposure to the Middle East is about 40% (including domestic refining with feedstock dependencies). We estimate demand curtailment of ~25% might be needed to ensure sufficient inventory buffers.

Buying opportunity on negative newsflow

- We anticipate earnings downside of about 25% for PETD arising from demand curtailment policies in 2026. Critically, the negative newsflow of demand curtailment policies will continue to trickle in over coming weeks and weigh on sentiment.

- With PETD breaking below the 200D moving average, the negative newsflow, and the lack of clarity on earnings impact, we foresee the stock could at least test the next support level of RM20.90. The floor for PETD, even in the maximum demand destruction scenario of -20%, we think floor for PETD would be RM19.00 (~20x 12MBF PER).

- We think there is a window to wait on further negative newsflow and look to accumulate PETD around RM20.90 on the basis that the shocks will be transient. On normalized earnings, we estimate this implies a healthy yield of 5.7%.

- In the worst case scenario, PETD at RM19.00 implies a yield of 5.9%, once the earnings normalize.

About the Company

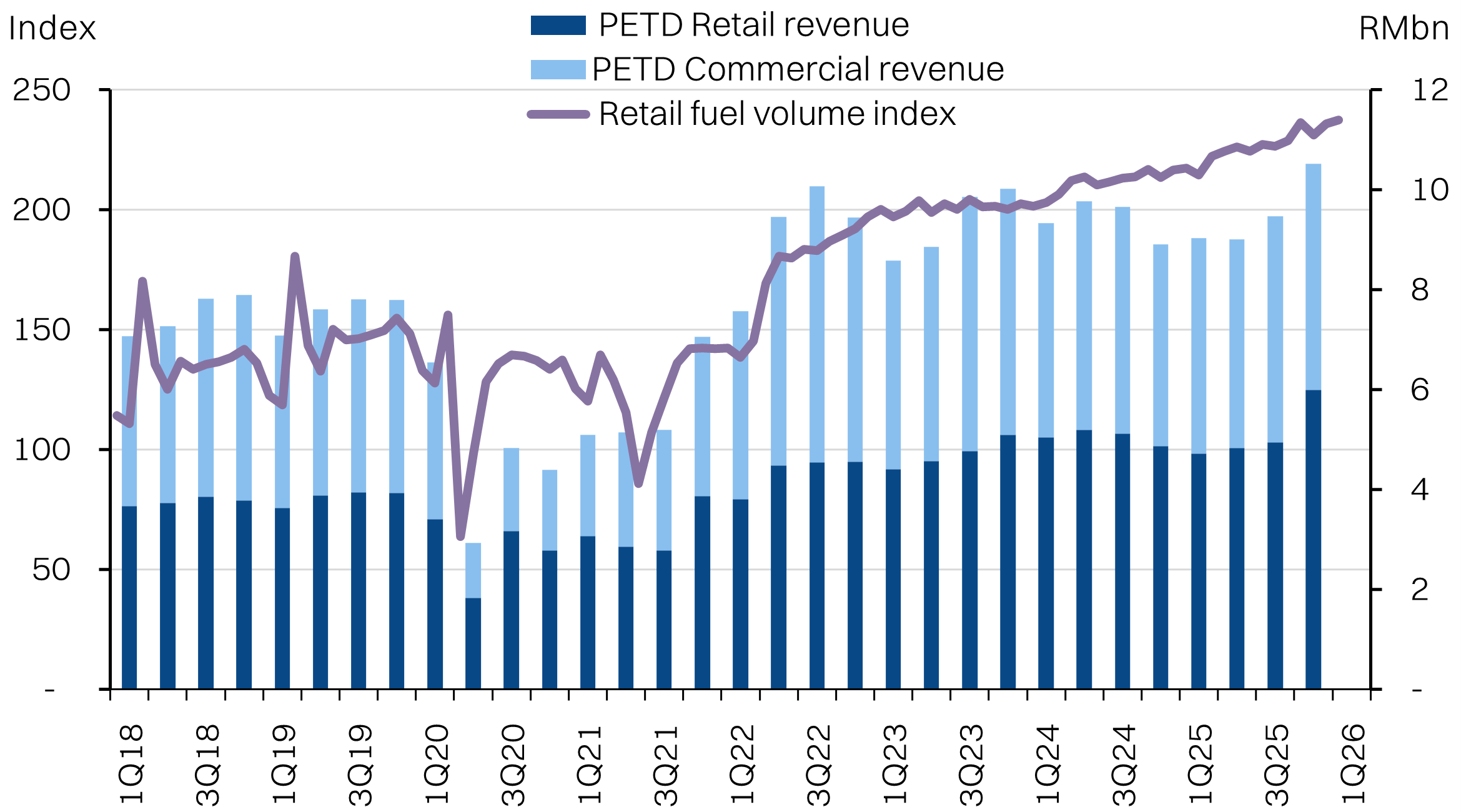

Petronas Dagangan runs the largest retail fuel network in Malaysia with over 1,000 stations and 800 Mesra convenience stores. The group derives 60% of sales from the retail business and another 40% from commercial. Within commercial, roughly 40-50% stems from jet fuel.

PETD also has the Setel digital wallet app that collects loyalty rewards for users as well as facilitating redemption of the Budi95 fuel subsidy quotas.

About the Stock

PETD is part of the Petronas stable of listed companies and is 63.9% owned by the latter. The next largest shareholder is EPF with a 13.19% stake. PETD is a syariah compliant stock that is also a constituent of the FBMKLCI Index.

A key characteristic of PETD, is that many ESG-minded funds may opt to avoid holding the stock due to its high exposure to fossil fuels and challenge in pivoting to electric vehicles.

Coupled with the policy risk from subsidy rationalization, PETD’s valuations have been under pressure in recent years.

Investment Idea

PETD has broken below the 200D moving average. We anticpiate more selling pressure on the negative newsflow, as well as the expectation of more demand curtailment policies.

We anticipate further negative newsflow could see PETD test lower support levels of ~RM19 on the back of earnings downgrades and increased emphasis on EV adoption. However, we argue this event is transient and investors can take advantage of weakness arising from the negative newsflow to take a position.

Key Risks:

EV adoption accelerates: This is a long-term risk to PETD’s earnings. But faster than expected adoption is likely to weigh heavy on sentiment of the stock as investors price in a more rapid adoption of EVs. Elevated pump prices for a prolonged period would present a catalyst for more EV adoption. While subsidies are shielding the mass market from the worst of the oil price surge, mid to upper middle segments have a more compelling case for EV adoption after the Budi95 quota was cut to 200L/month.

Policy impact is muted, for now

We estimate the demand curtailment for nationwide retail gasoline is only going to be 0.6-1.5%, compared with pre-war estimates. The primary reason is that it will only affect an estimated ~210k to 370k commuters. For context, an estimated 3 million vehicles enter KL each day on average.

However, the government’s primary intention is to curtail non-essential fuel demand to mitigate the pressure on limited reserves. The government has indicated reserves of ~2 months. Considering roughly 40% of Malaysia’s gasoline requirements are tied to Middle East imports, the 2 months of reserves could be stretched to roughly 5 months at most, assuming no adjustment to consumption.

In turn, we estimate that policy-driven demand curtailment is likely to expand if the war is prolonged and oil prices rise further. This would include increasing the WFH days or extending this to the private sector on a progressive basis.

Estimated impact of the WFH policy for civil servants and GLCs

Watch for overreaction

PETD is currently trading near record-low valuations, at 17.6x 12MBF PER. However, earnings expectations do not currently factor in retail fuel demand curtailment from government policy and the higher pump prices.

We estimate that the aforementioned demand curtailment from a protracted war could de-rate earnings by up to 25% (FY26E) on a corresponding ~20% fall in total volumes - retail and commercial. In turn, this implies a PETD is trading at 25x FY26E PER.

However, we make the case that this shock is transient in nature - policies can be rapidly reversed once the war ends. In turn, investors should price through the earnings cuts. However, with PETD breaking below the 200-day moving average, the stock could be vulnerable to more selling pressure in light of the negative newsflow.

We think the immediate support level should be around RM20.90 (the 100-day moving average) on the recent newsflow. What keeps PETD interesting is the potential for more demand curtailment policies from the government in the coming weeks if a ceasefire in the Middle East remains uncertain. If this is the case and the -25% earnings downside we anticipate materializes, we foresee RM19.00 could be the next support level.

PETD is trading at historically low valuations, even compared with Covid-19

Covid-19: PETD share price did not fall as steeply as earnings expectations.

PETD has broken below the 200D moving average

BUDI95 implementation lifted headline sales numbers in 4Q25