Trade on the bumper margins

Glovemakers should enjoy margin expansion as higher ASPs offset the nitrile costs.

Malaysia Gloves

Disclaimer: By using this information, you acknowledge that you are solely responsible for evaluating the merits and risks of any investment decision and agree not to hold NewParadigm Research liable for any damages arising from such decisions.

Key takeaways

- Glovemakers could enjoy further earnings and valuation rerating on bumper margins in 2Q/3Q.

- Trade into the optimism, but be mindful of potential headwinds towards the end of the year.

- Our top pick in the sector is HART for quality and high nitrile exposure, but flag Kossan as a higher beta play.

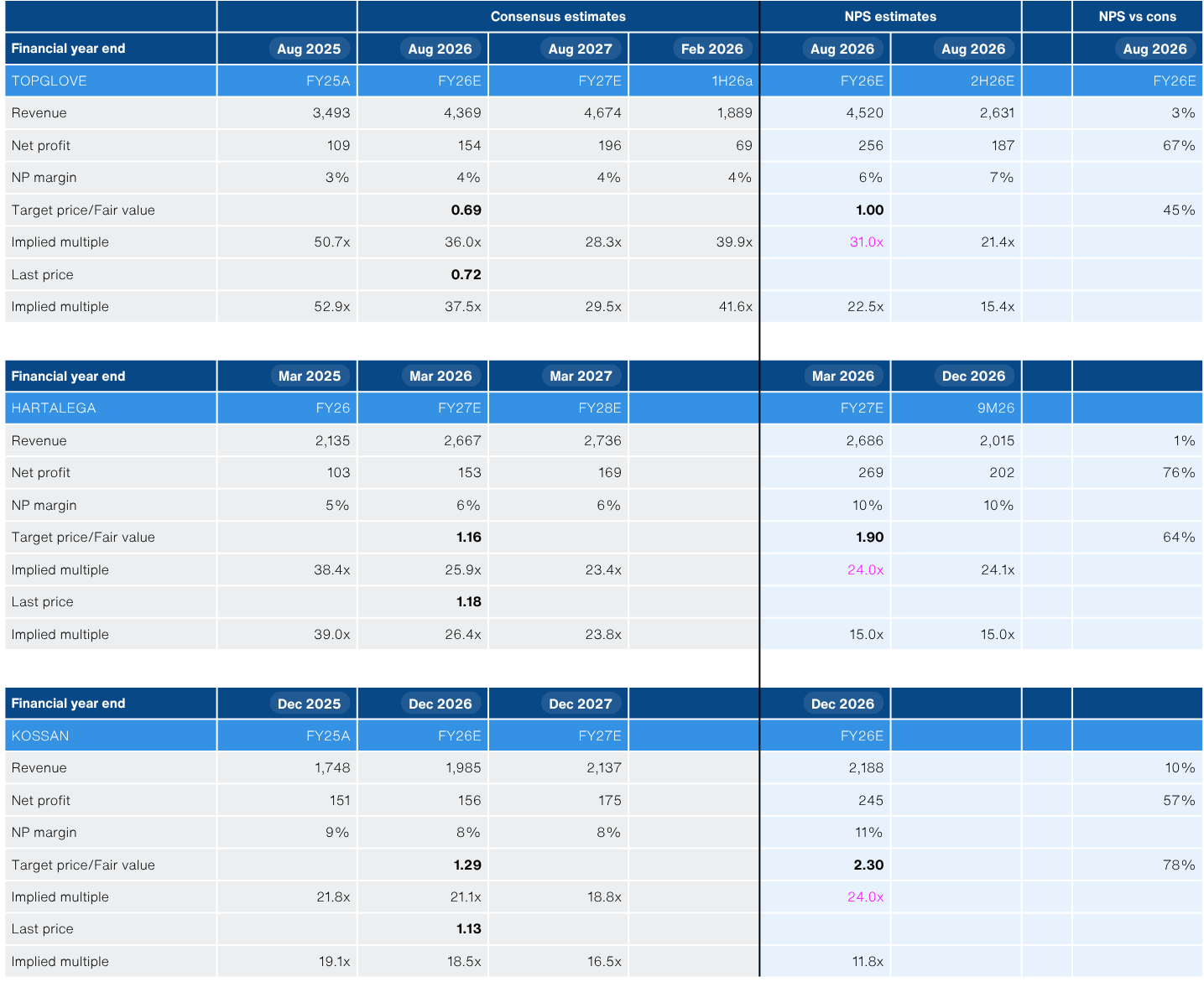

Market is not pricing-in bumper ASPs | ASP data points lag, creating uncertainty | Glovemakers’ fair value

Source: Bloomberg, DOSM, NewParadigm Research, May 2026

Trading opportunity

- Market appears too focused on the uncertainty around glovemakers’ ability to pass on the higher nitrile prices to end-customers. We disagree. We estimate that glovemakers have a unique opportunity to raise prices above and beyond the direct cost impacts, for now.

- We foresee the next 1-2 quarters, where ASP hikes can outpace the higher nitrile costs, supported by industry-wide repricing, US tariffs preventing Chinese imports, and lagging gas price hike to glovemakers.

- Our earnings estimates are 60-80% above consensus, but we flag both ASP and nitrile prices are currently exposed to a high degree of volatility. Note, that we have factored in a 5% hit to volumes on potential demand destruction.

- We think consensus’ assumptions are volume-led rather than ASP-led, and yet to factor in meaningful margin expansion. On earnings expectations upgrades over the next 2 quarters, we anticipate valuations will re-rate as well.

- Key risk: ST inventory destocking by end-buyers to avoid high ASP’s. Will delay our thesis but not unwind it.

When to swap

- We foresee headwinds emerging towards the end of the year, that could dampen optimism for the sector.

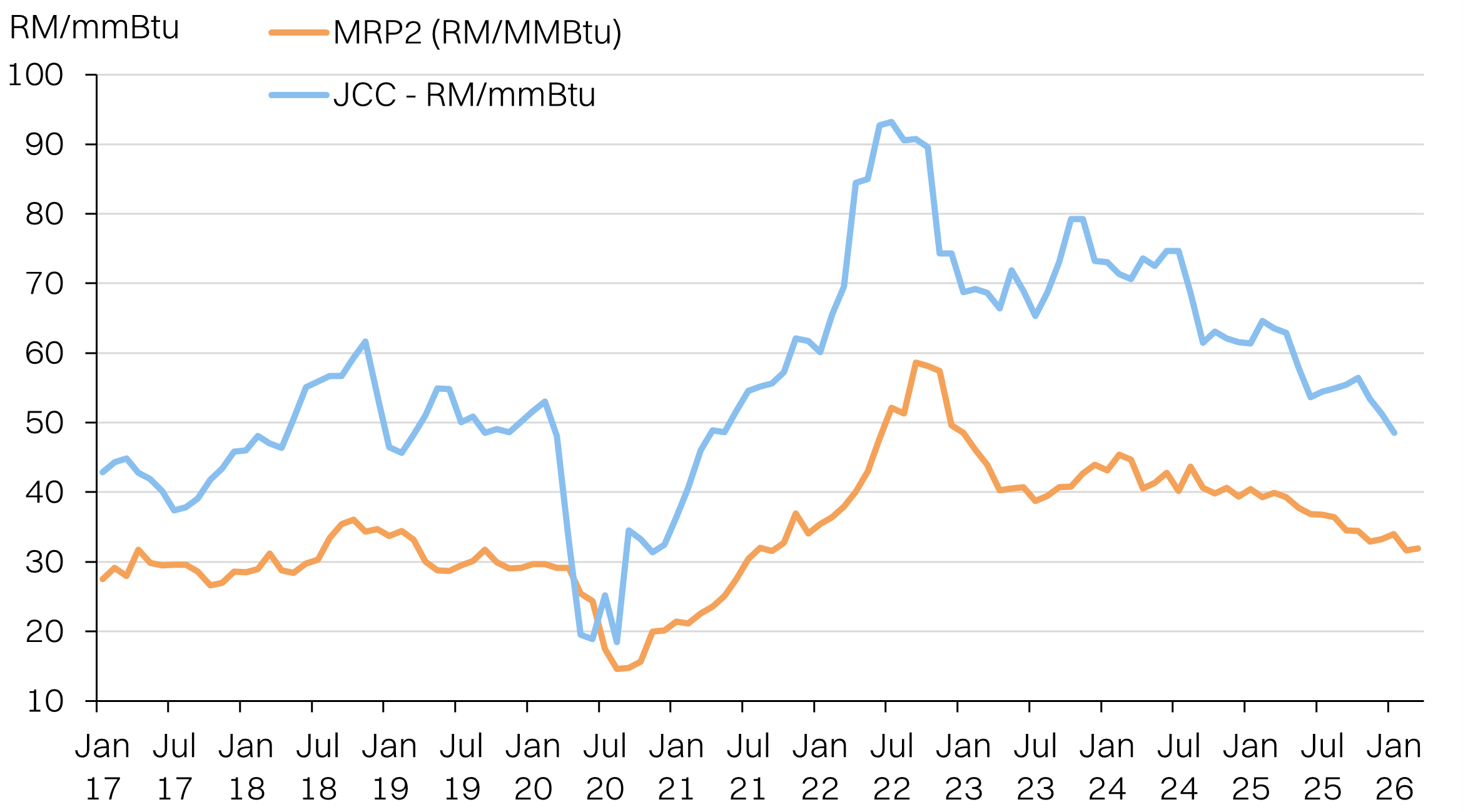

- Energy price inflation (natural gas) will only show up in 4Q26, due to Malaysian Reference Price (MRP) lag of 6 months. We estimate 20-25% increase in gas costs, which make up 15% of COGS.

- Chinese glovemakers could have a structural advantage if the war runs long, from access to Russian naphtha. Malaysian glove makers rely on nitrile from South Korea which is heavily reliant on Middle East imports.

- Finally, Chinese glovemakers are building capacity in Vietnam to circumvent US tariffs, with volumes scaling up through the year.

Fair value upside

- Hartalega has the highest earnings leverage, potentially doubling earnings sequentially. However, we anticipate Kossan could have higher beta from a sector-wide re-rating.

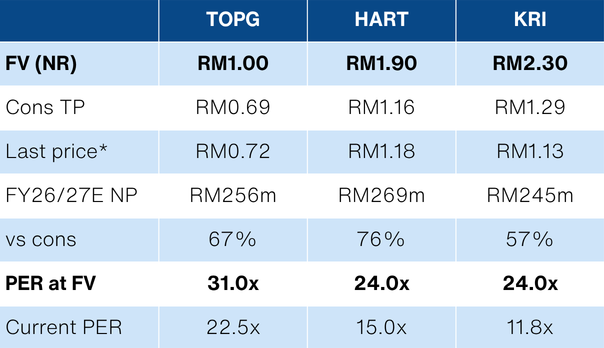

- Our FV for TopGlove is RM1.00 on 31x FY26E PER (NR).

- Our FV for Hartalega is RM1.90 on 24x FY27E PER (NR).

- Our FV for Kossan is RM2.30 on 24x FY27E PER (NR).

Cost-push driving margin expansion

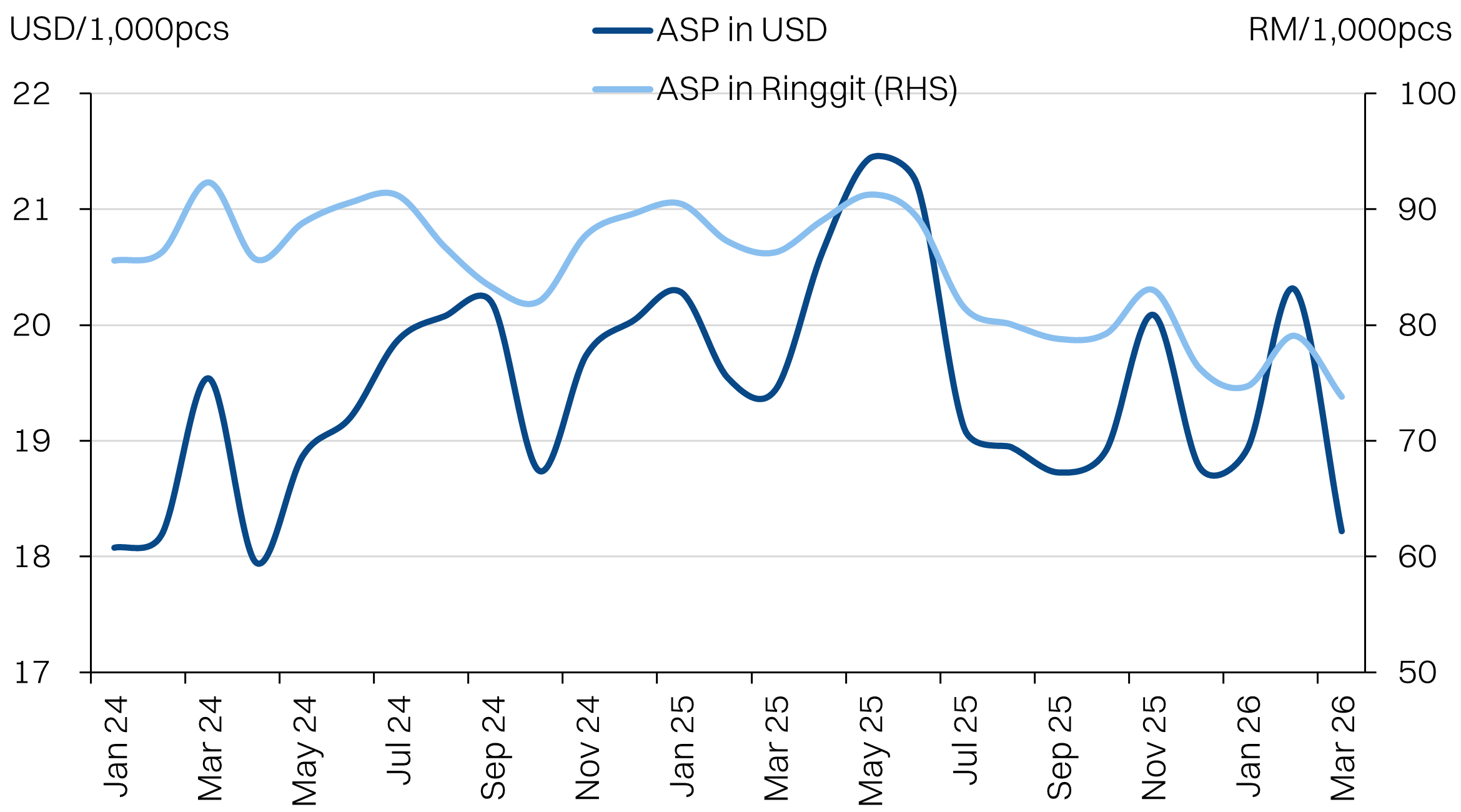

Glovemakers have started to signal higher ASP’s, but the market does not appear to be pricing it in just yet. One of the main reasons, is that the ASP’s have not yet shown up in the numbers and expectations on glovemakers has had a conservative bias.

What has been said:

- Hartalega indicating ASP increase in April of +US$3/1,000pcs, and +US$7/1,000pcs in May.

- TopGlove indicating ~60% MoM increase in nitrile ASPs to ~US$27/1,000pcs, for the last week of April.

Market is probably being conservative, given that the ASP upside is not yet showing up in high-frequency indicators. As of March, the implied blended ASP for gloves actually fell by -7%/-10% in Ringgit and Dollar terms respectively. In contrast, the surge in nitrile prices has been much more visible.

DOSM export data have not yet shown the ASP impact

In turn, earnings expectations for the glovemakers as well as the sector valuations have not yet begun to price this in.

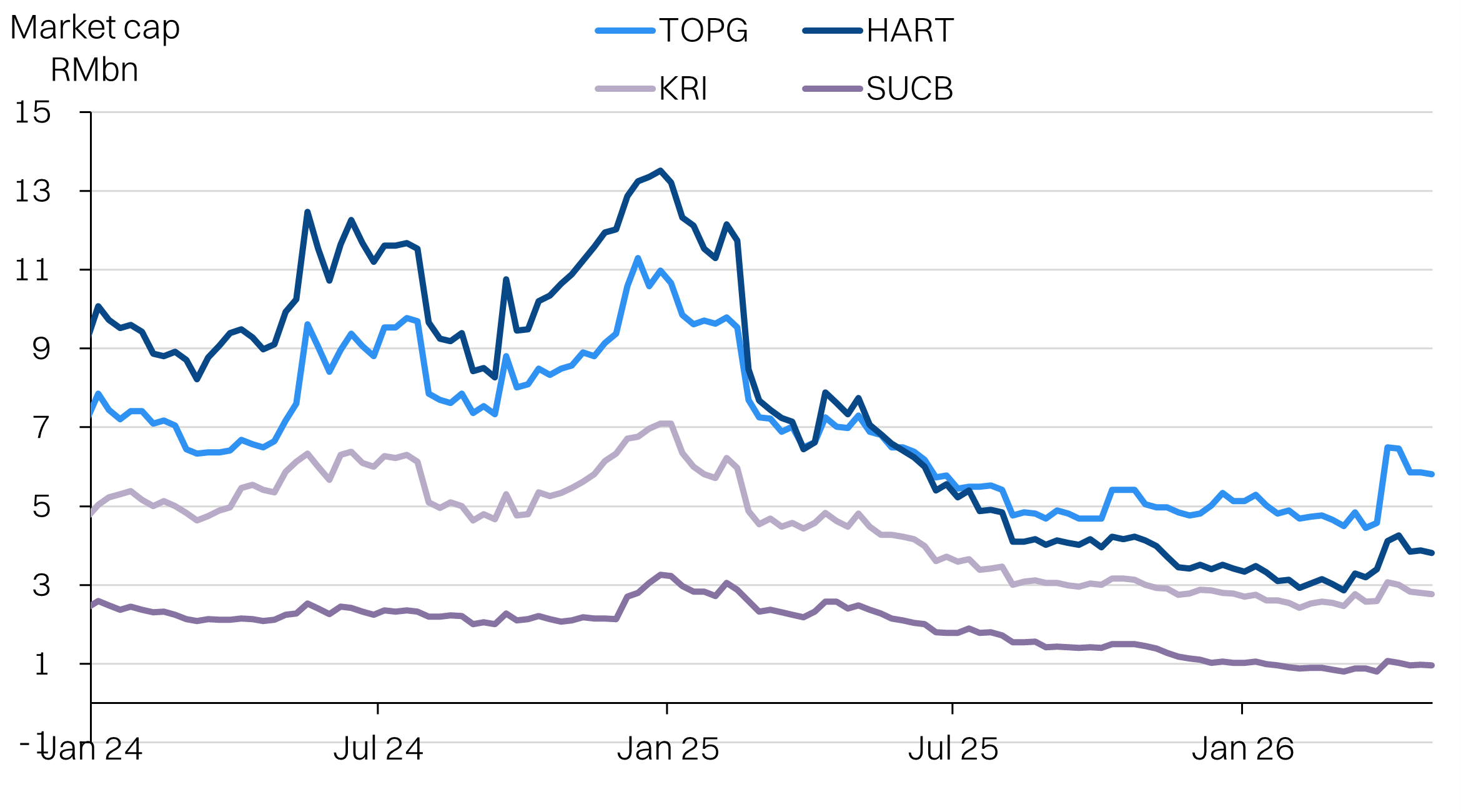

Malaysian glove stocks have been muted since the war

Nitrile cost concerns overshadowing ASP outlook

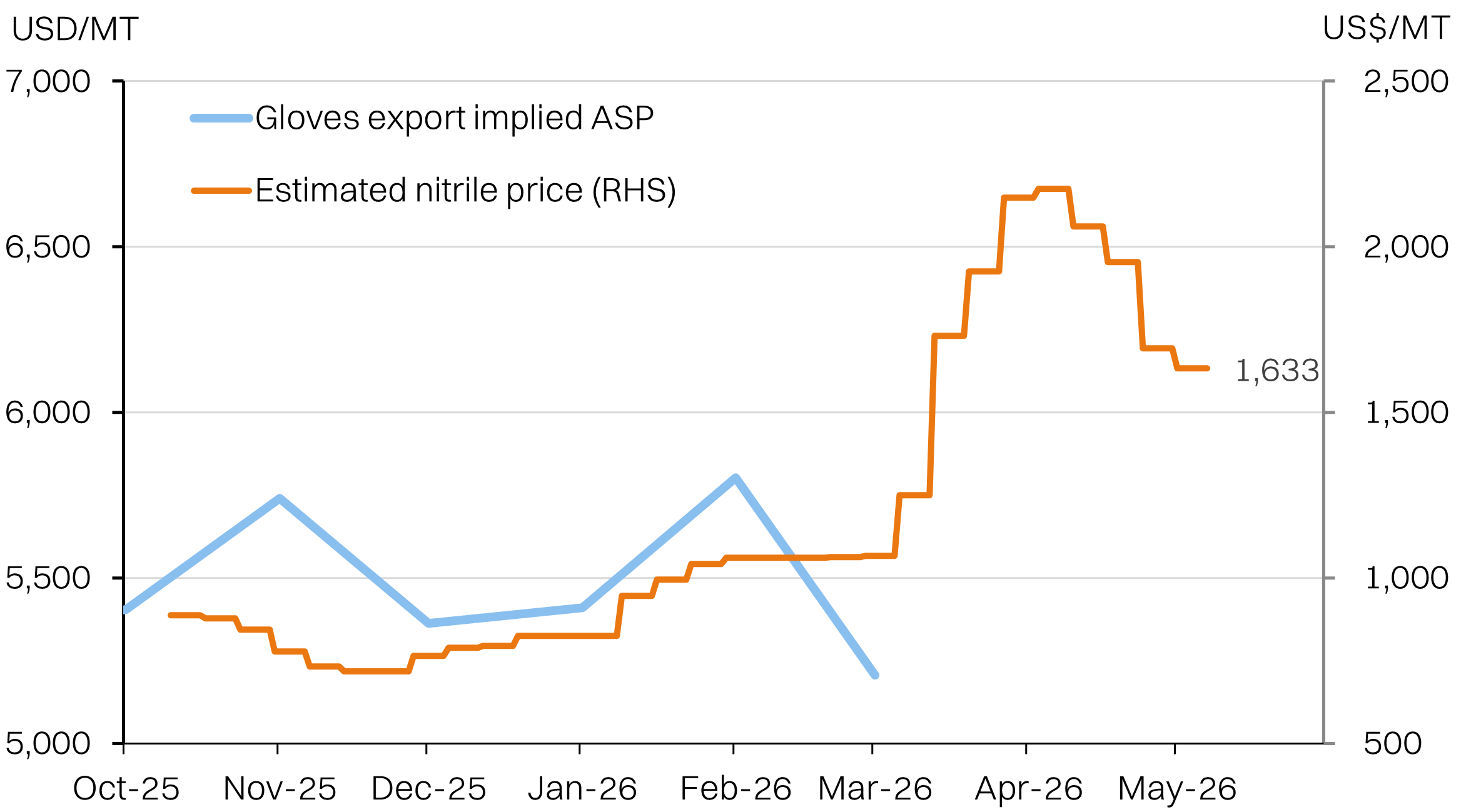

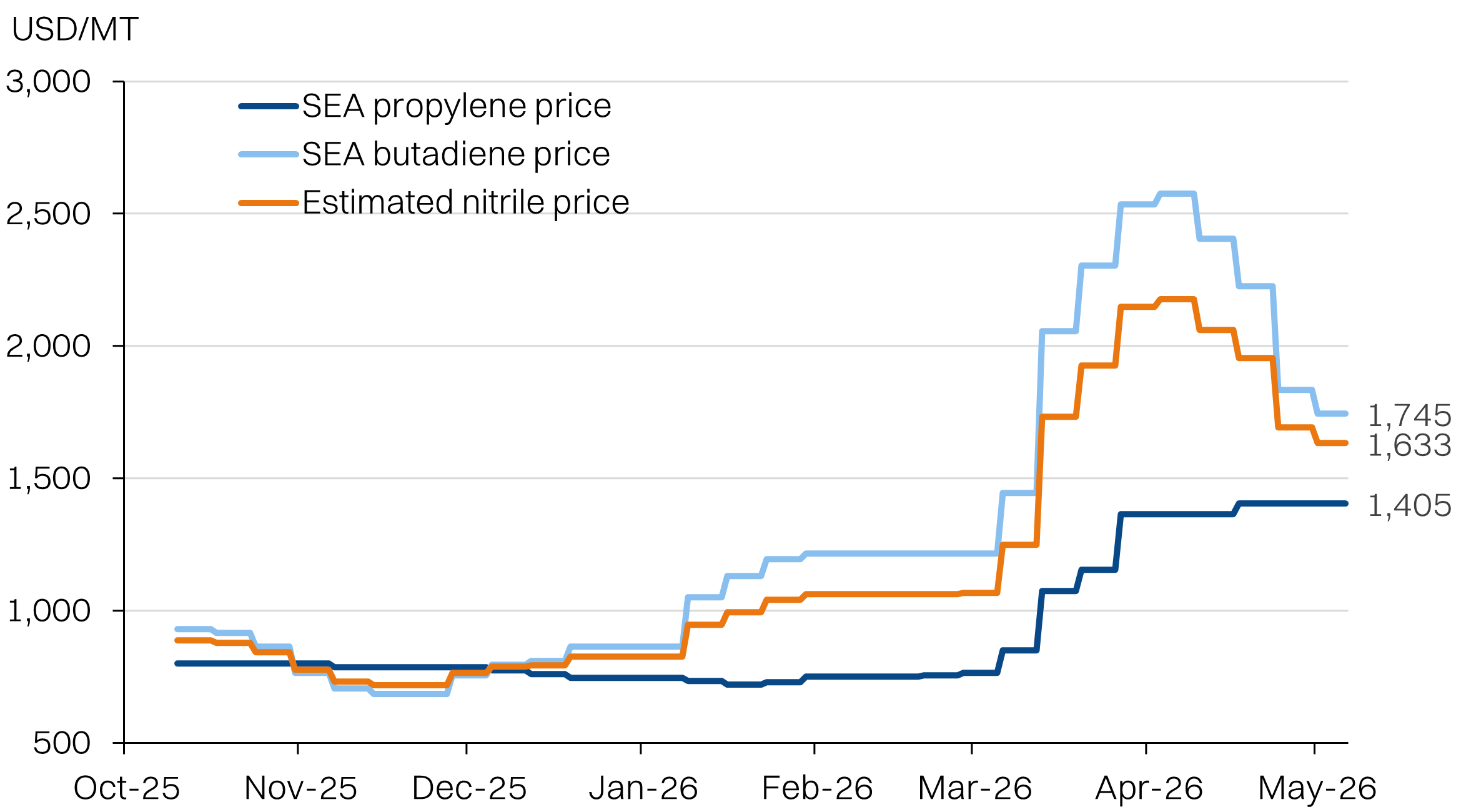

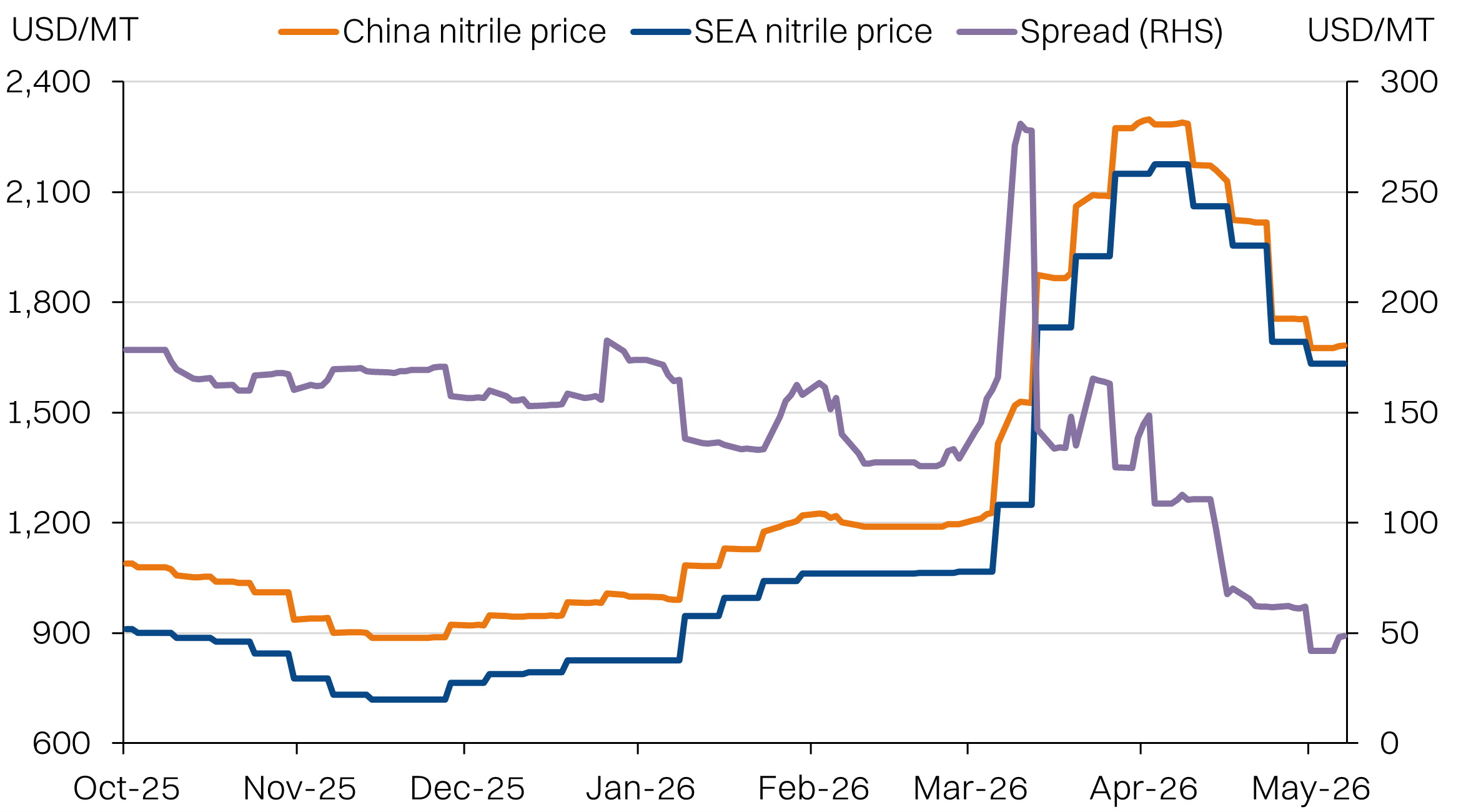

Nitrile, or nitrile butadiene rubber, is derived from naphtha. The US-Iran war that has shut the Strait of Hormuz, has also choked supply of naphtha to Asia. We estimated that nitrile prices are about 60% more expensive due to the shortages of naphtha.

Malaysian glovemakers source ~65% of their nitrile requirements from South Korea, which in turn has a ~50% dependency on Middle Eastern naphtha imports.

There are no published benchmarks for nitrile prices. However, it is made up of roughly 33% propylene and 67% butadiene. We’ve used Southeast Asian pricing benchmarks for these two precursor inputs to estimate nitrile prices. Since the war began, nitrile prices peaked at around US$2,200/MT before settling at around US$1,630/MT. On average, nitrile prices post-war are up about 60%.

For gloves, nitrile constitutes about 40% of total cost. Hence the market is rightfully concerned about the impact. However, it is also worth noting that all the glovemakers, including the key competitors in China, are facing the same cost-push pressures. In turn, the broader industry has been passing on the higher costs to end-customers. This is possible because demand for medical disposable gloves are non-discretionary in nature.

It is also worth noting that substitution to latex is not viable are bulk scale due to allergy risks. Natural rubber gloves also tend to be less durable and not suitable for all applications.

Estimated nitrile prices are up +60% on average

US tariffs on China helps with pricing power

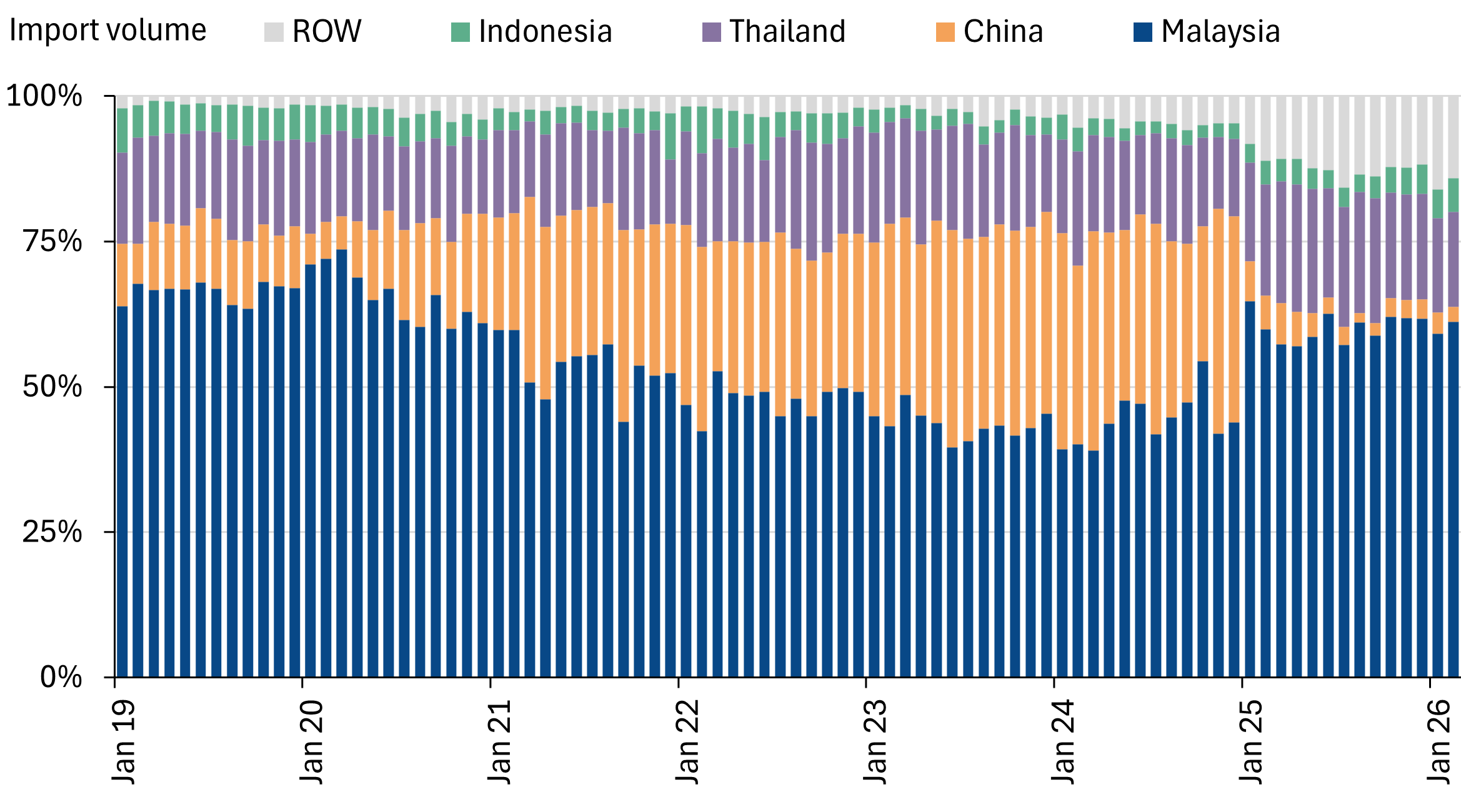

Pricing power for Malaysian glove makers is also boosted by the Section 301 tariffs that have been imposed on Chinese gloves since 2025. The 100% tariff has made the import of low-margin gloves from China completely impractical.

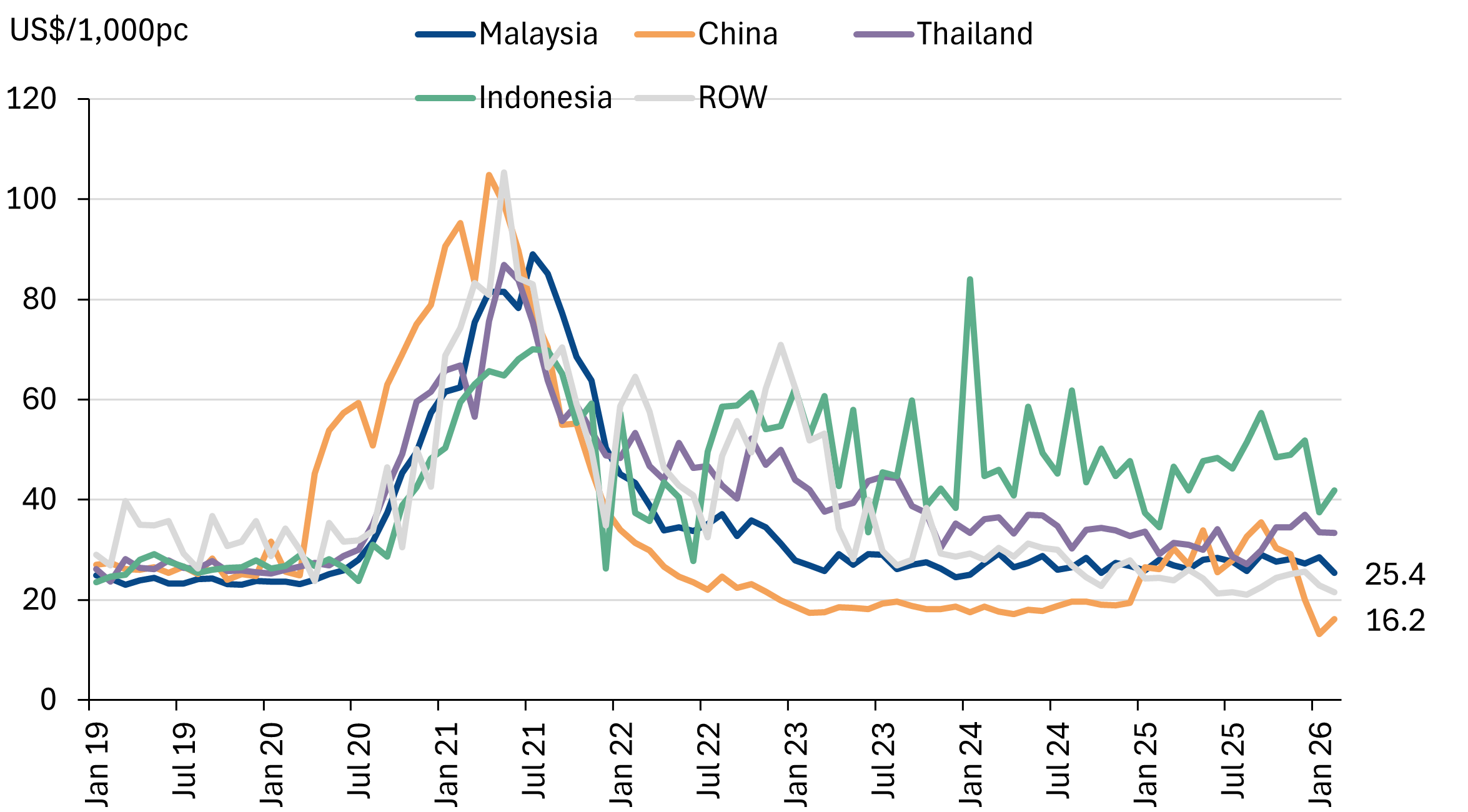

Malaysian gloves now make up >60% of imports by volume, with Thailand in second place with 16%. China’s once dominant >30% market share has since fallen to less than 10%. The exclusion of Chinese glovemakers proved to be less of a tailwind over the past year, simply because it pushed the same volumes to other markets and limited ASP upside for the Malaysian glovemakers. Though it did help a little bit with volumes.

US tariffs have pushed Chinese nitrile glove imports out of the market

This is evident in the implied ASP for glove imports (import value vs import volumes), which show fairly stable pricing for the non-Chinese imports. This reflects the broader overcapacity challenge with the industry as a whole.

It is worth considering that the Section 301 tariff on Chinese medical nitrile gloves is structurally isolated from the US-China diplomatic tariff truce framework. It is part of a distinct trade action, that is separate from the IEEPA tariffs that were struck down by the supreme court in February. We do not anticipate this tariff will be lifted in a hurry.

Estimated nitrile prices are up +60% on average

Consensus still not yet convinced

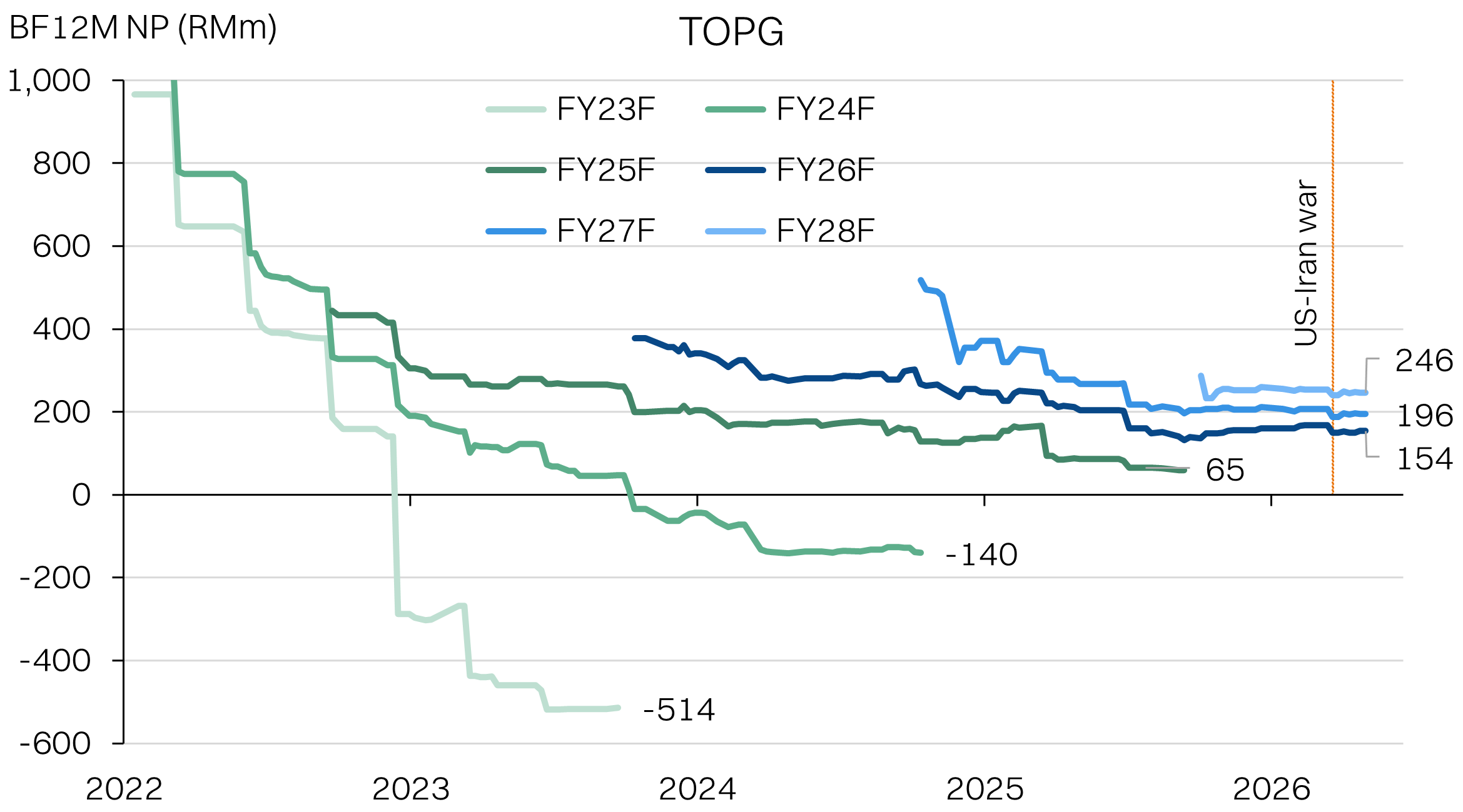

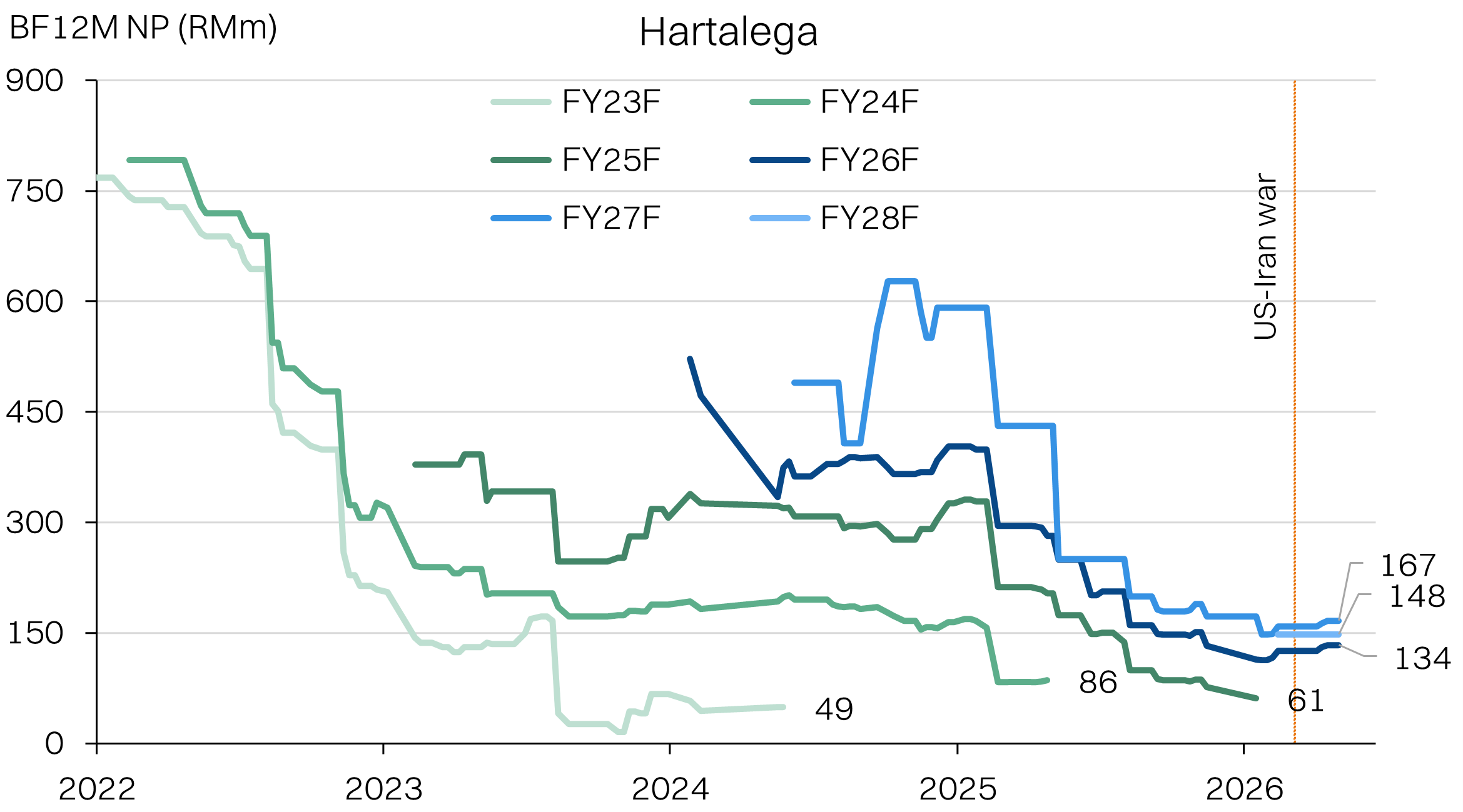

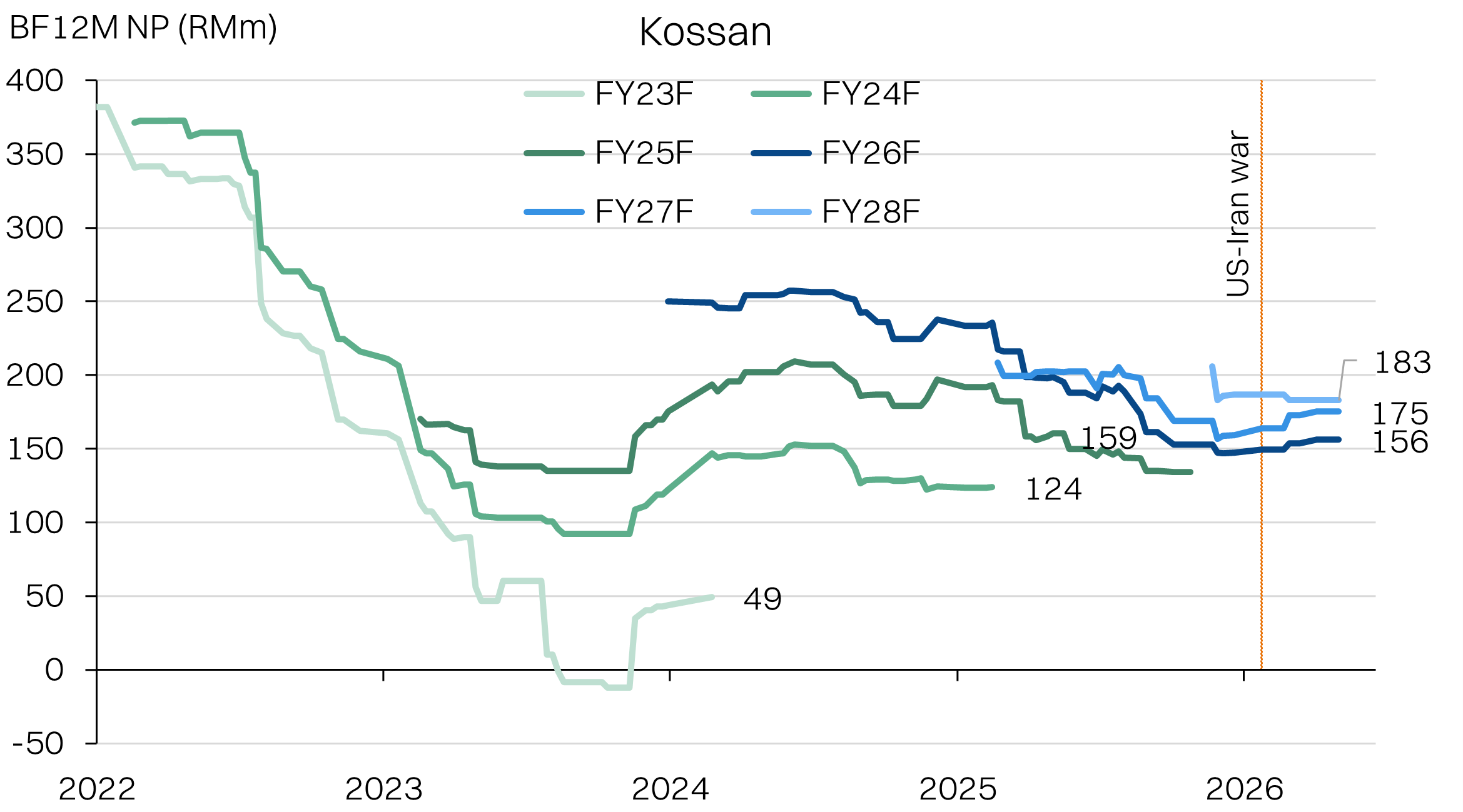

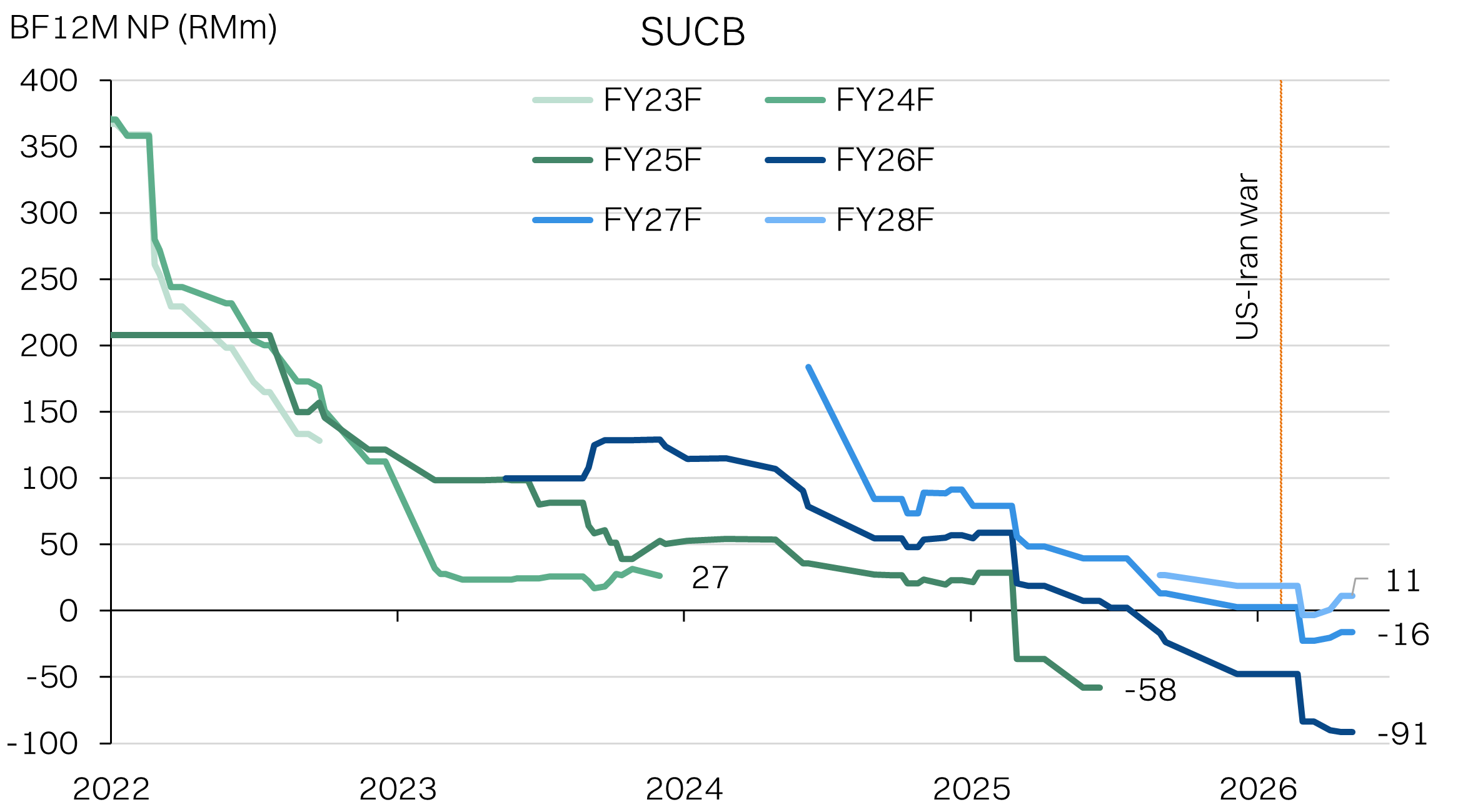

When we look at market expectations, we see that consensus has generally held back on more substantive upgrades to glovemakers’ earnings. Since the start of the year, the blended forward 12M NP estimates have only be lifted by 7%. It is hard to say why this is the case, but we suspect it could be due to concern around the nitrile prices and the glovemakers inability to command pricing power in recent years due to the oversupply of gloves.

The bias for conservatism and the “wait and see” approach presents an opportunity - once the earnings delivery trickles in, the upgrades to expectations could spur a more substantive rerating for valuations as well.

It is also worth noting that there has not been a meaningful upgrade to consensus earnings expectations, mid-year, since the Covid-19 windfall years.

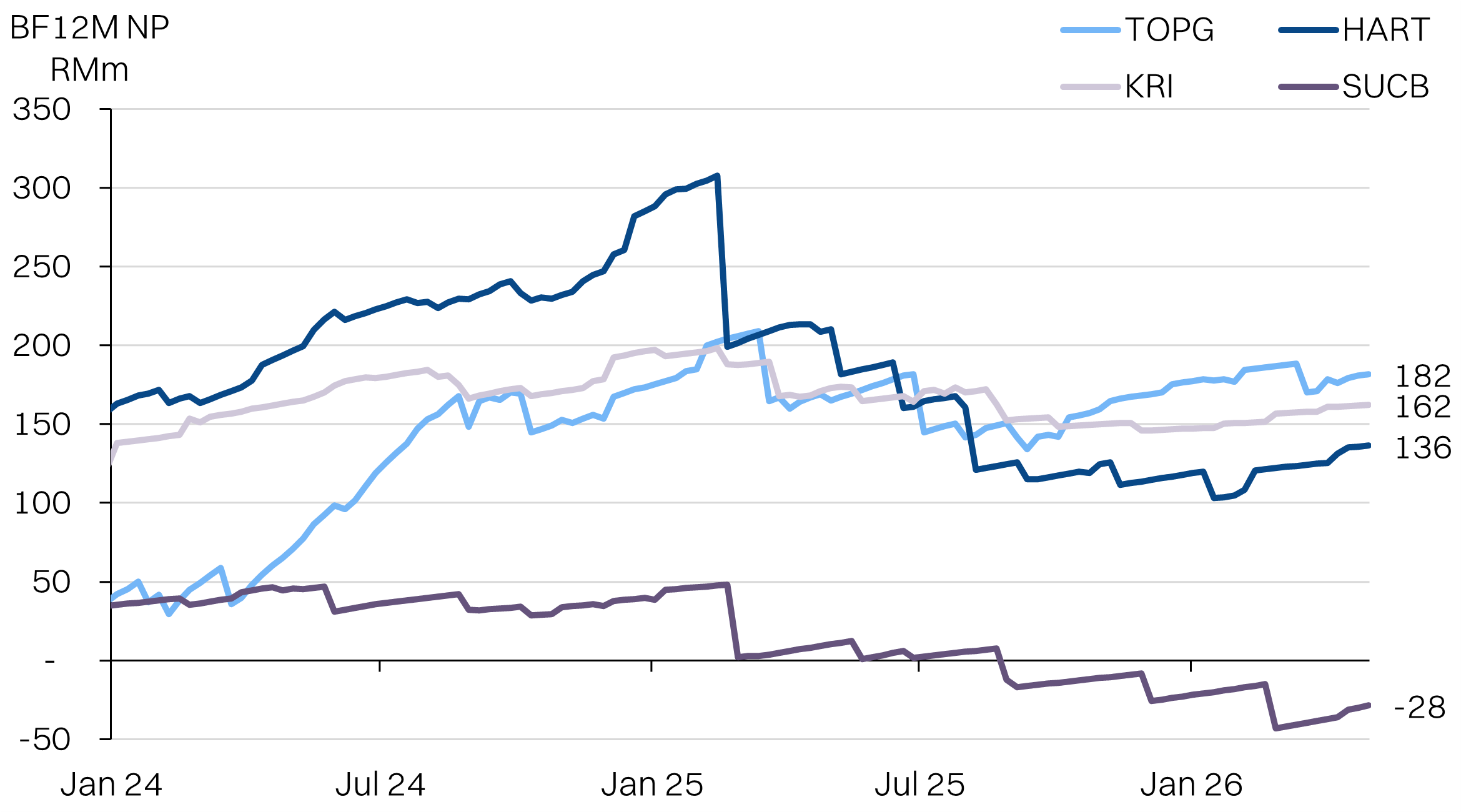

Blended forward 12M NP expectations for the glovemakers

NP expectations by financial year

Source: Bloomberg, NewParadigm Research, May 2026

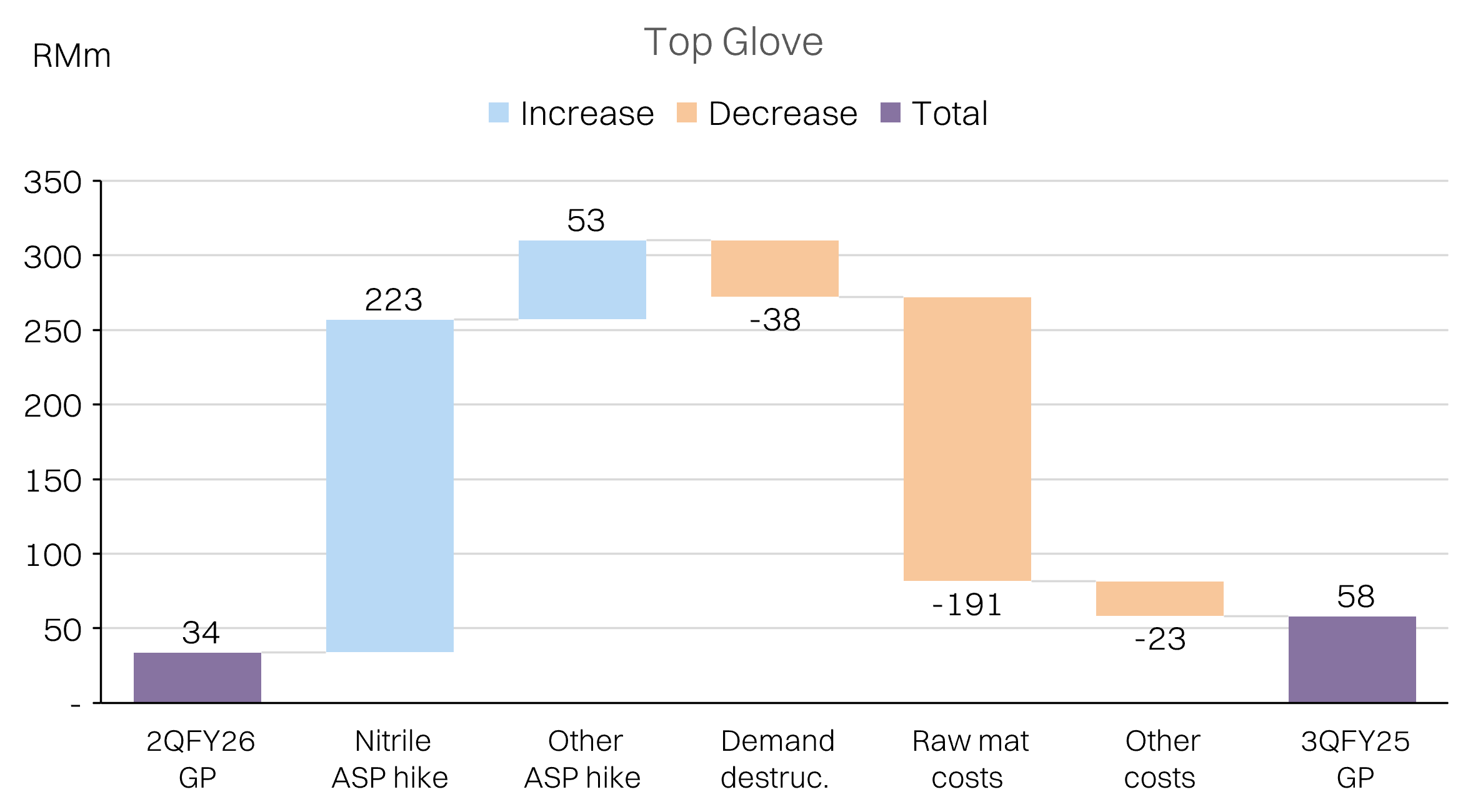

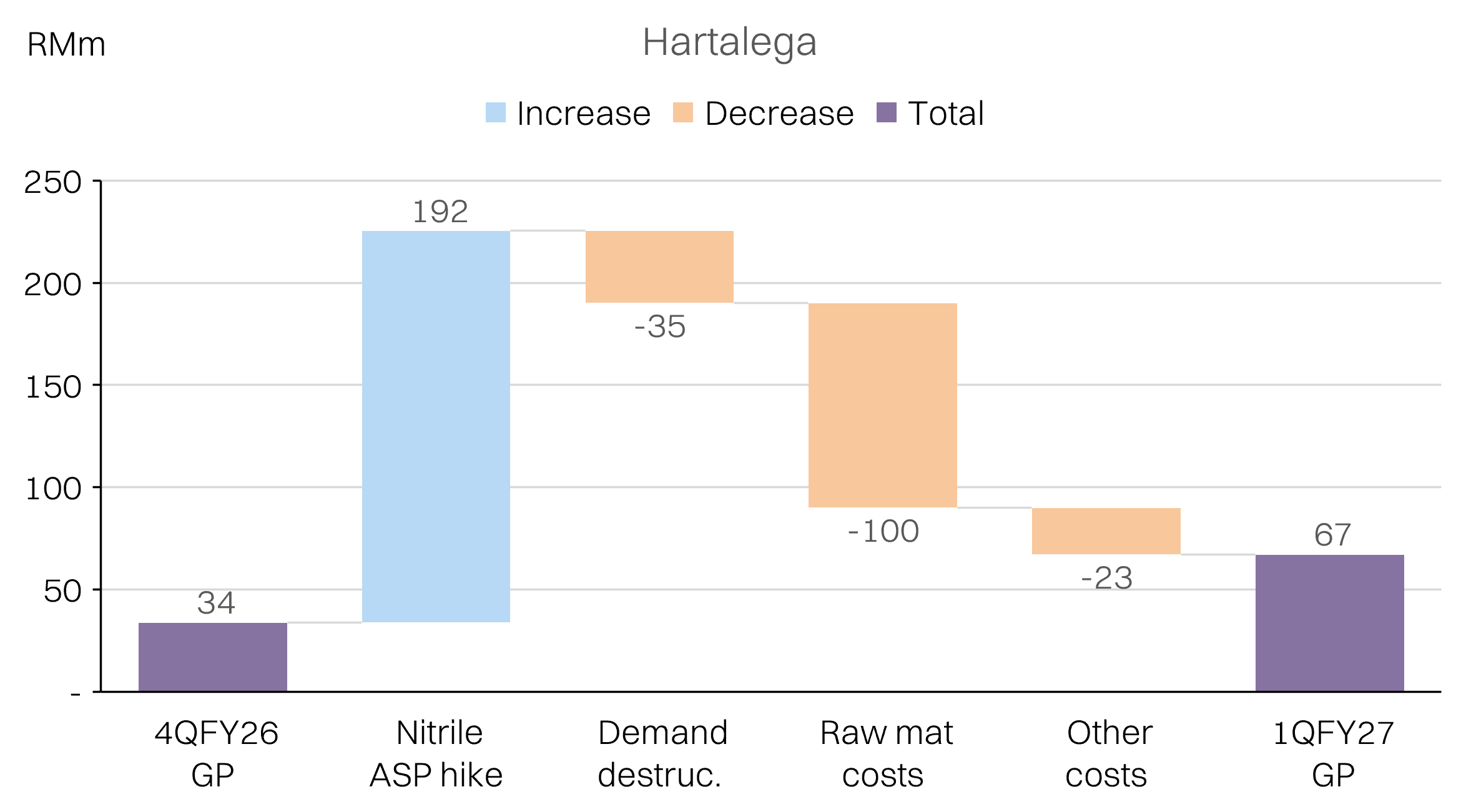

Earnings could double within the next 1-2 quarters

We ran an earnings simulation on both TOPG and HART (operating stats were more transparent than KRI and SUCB) and found that the indicative ASP hikes should comfortably outpace the higher nitrile costs, since the latter is only ~40% of pre-war operating costs.

We even baked in some volume destruction and broader cost inflation of 15% to account for hikes in electricity, labour, fuel and packaging.

Given HART’s production capacity is almost entirely nitrile, it had much higher leverage to the ASP expansion than Topglove. The latter would see net profits almost double sequentially, while the former would have ~60% sequential growth.

Note that TopGlove has an offset August financial year-end, compared with Hartalega’s March financial year-end.

TopGlove & Hartalega GP waterfall from ASP hikes vs higher nitrile prices

Source: Bloomberg, Company data, NewParadigm Securities, May 2026

Earnings sensitivity and valuations

Our earnings estimates are 60-80% above consensus among the big 3 glovemakers on the following assumptions:

- Realised USDMYR remains stable 4.0.

- -5% volumes on demand destruction.

- ASP’s for nitrile gloves increase to US$25-27/1,000pcs.

- Cost of nitrile increase by +60%.

Our fair value for TopGlove is RM1.00 (NR). We assign a target multiple of 31x FY26E (ended-Aug), noting that the period also captures 6M of earnings (ended-Feb) that did not enjoy the margin expansion.

Our fair value for Hartalega is RM1.90 (NR): We assign a target multiple of 24x FY27E (ended-March). HART’s financial year is not diluted by the pre-war margins.

Our fair value for Kossan is RM2.30 (NR): We assigned a target multiple of 24x FY27E (ended Dec). Note that Kossan’s financial year includes one quarter of pre-war margins

Hartalega GP waterfall from ASP hikes vs higher nitrile prices

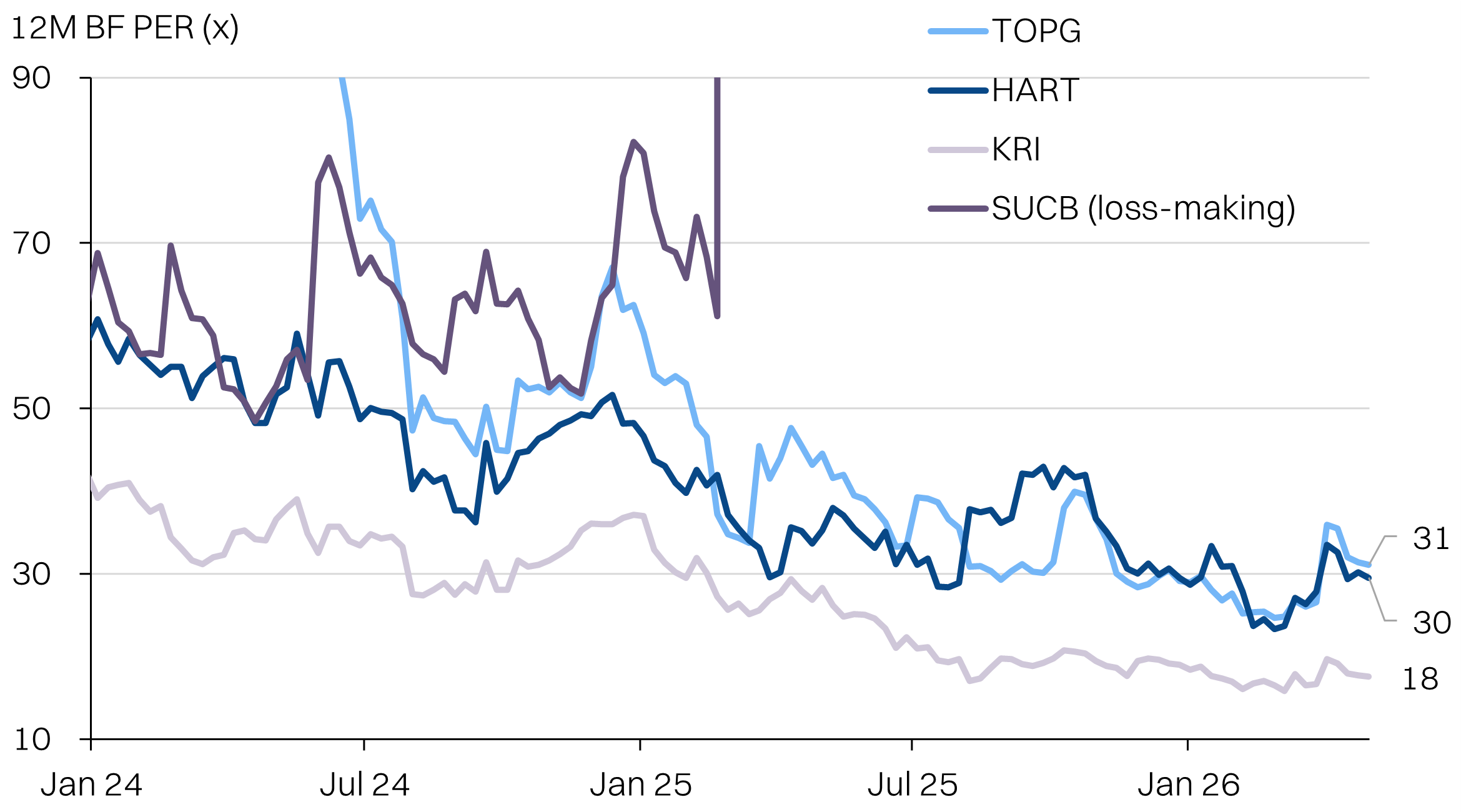

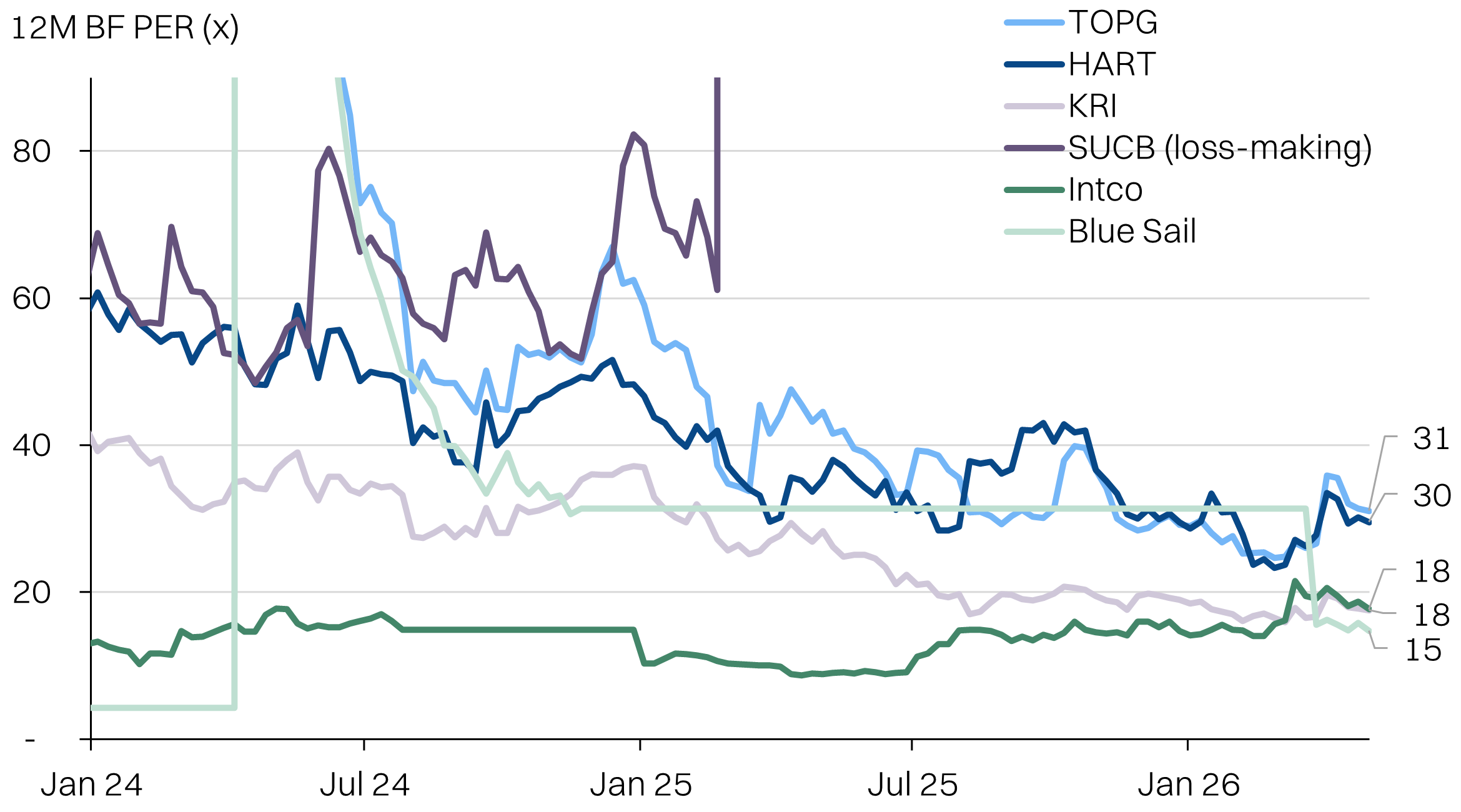

Valuations - PER considerations

One of the challenges with valuing the glovemakers is that PER is difficult to benchmark against historic averages. The collapse in profitability post-pandemic inflates the historic average PER, making it unsuitable as a reference. Top Glove’s average PER since mid-2024 is 42x.

The pre-pandemic benchmark would also be inapplicable since the stocks then did not have to contend with the current structural oversupply that has emerged from the pandemic, particularly from Chinese capacity.

That said, it is worth noting that the top Chinese glovemakers - Intco Medical Technology Co Ltd (300677 CH) and Blue Sail Medical Co Ltd (002382 CH) - trade on average PER multiples in the mid-teens. However, note that coverage on Blue Sail is thin, so the historic PER range is choppy.

Our target multiples incorporate the ST recent PER average, but adjusted to account for the different financial year-ends, that include pre-war margins (lower).

Thin post-pandemic profitability makes historic PER unhelpful as valuation benchmarks

But relative valuations against Chinese peers are worth considering

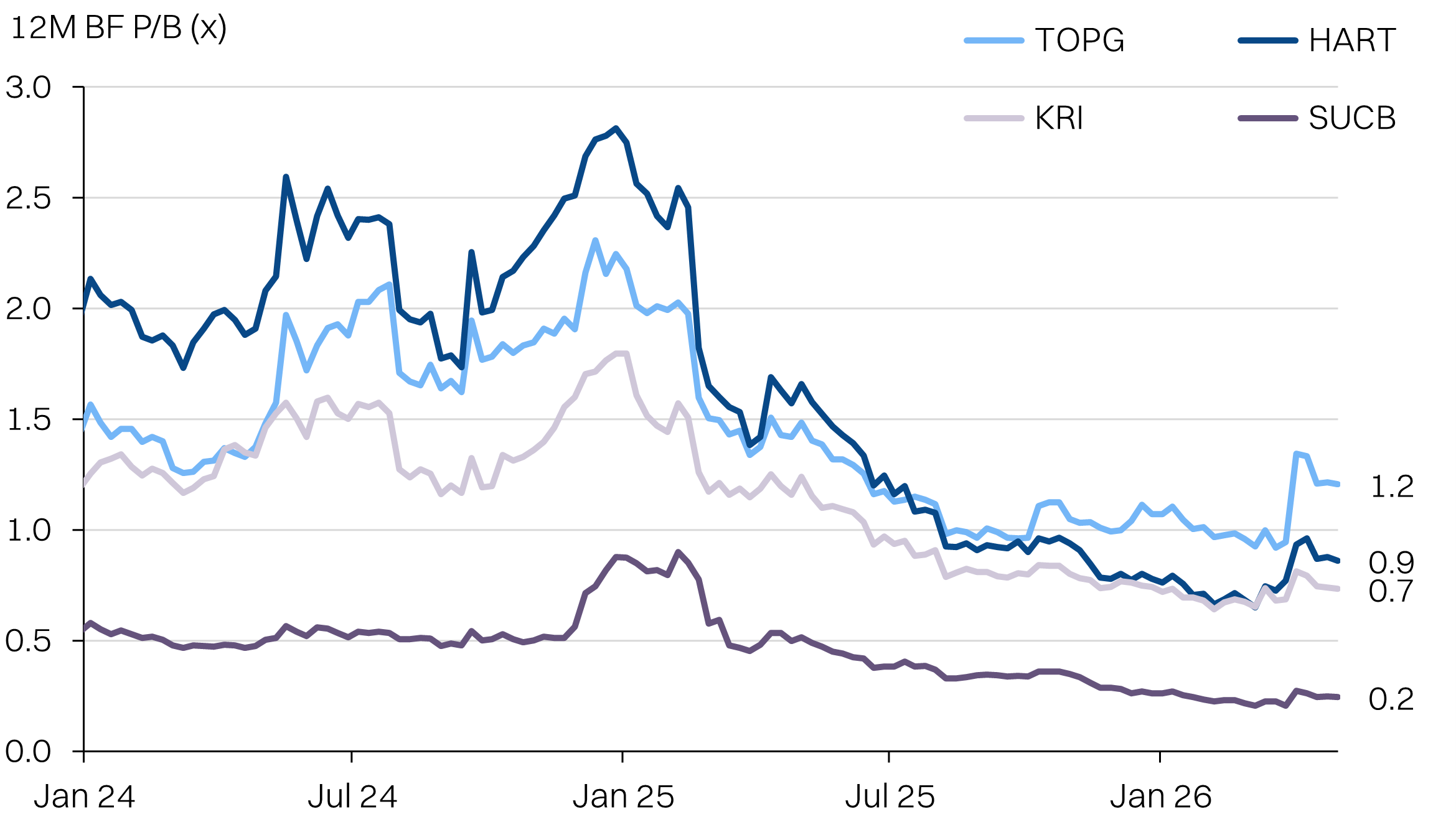

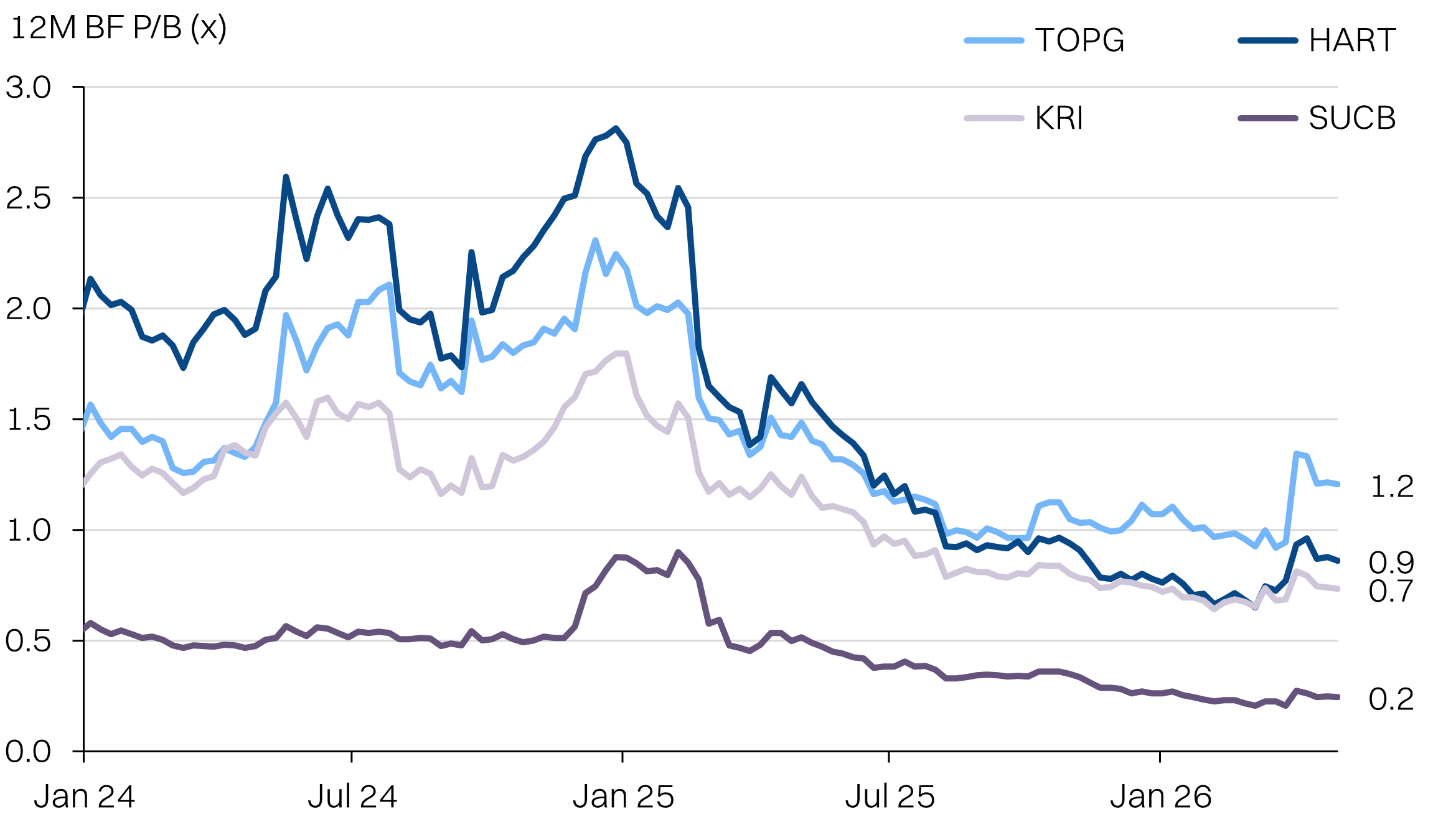

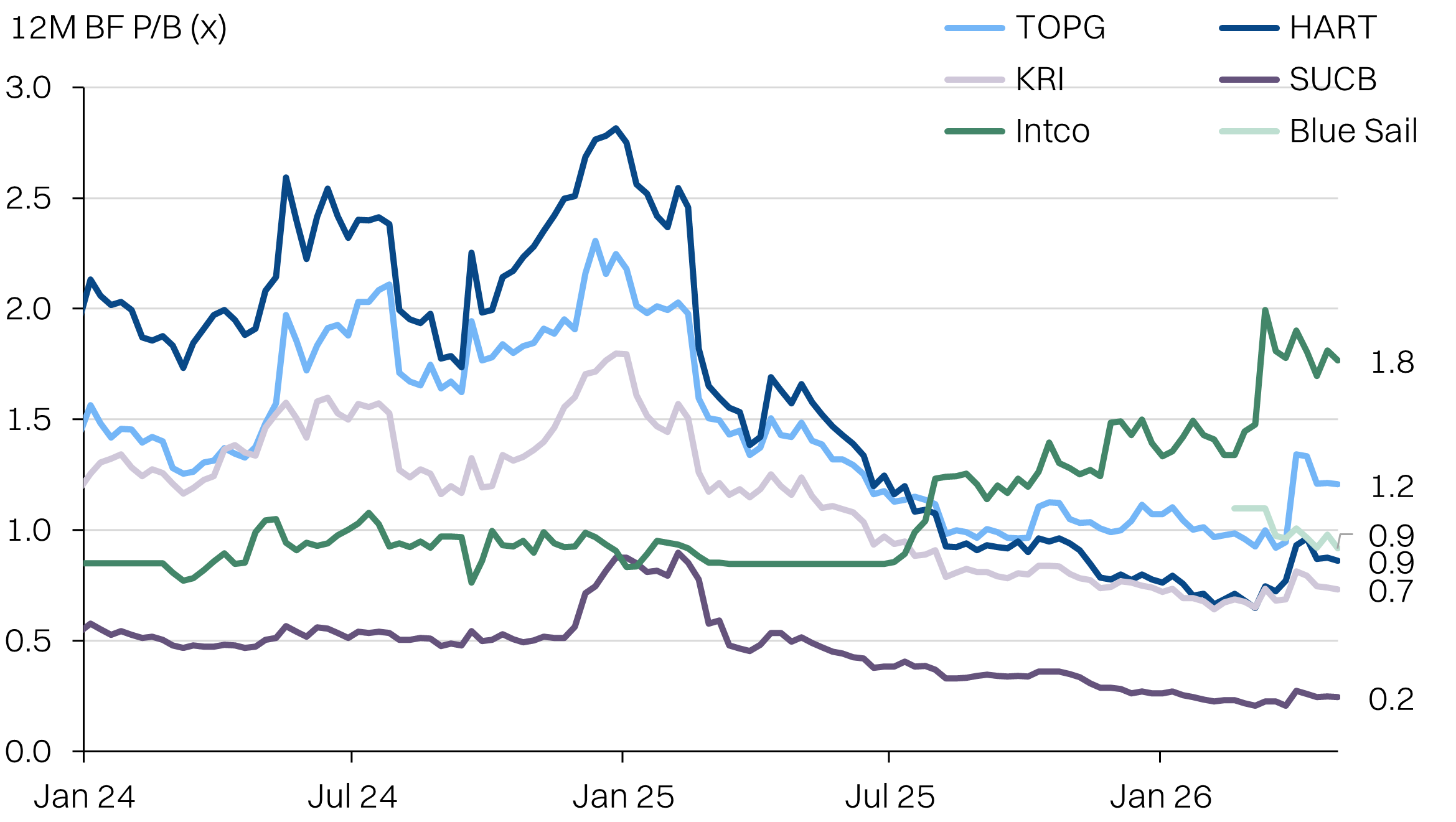

Valuations - P/B as a sanity check

Price to book valuations are less than ideal, especially for stocks that are highly sensitive to earnings delivery. However, it does provide a more useful reference point for how the market is valuing the glovemakers over time.

TOPG and HART have average post-pandemic P/B ratios of 1.4x and 1.5x respectively. Kossan and Supermax have lower averages of 1.1x and 0.5x respectively. We think these are useful reference points for the potential trading range.

The Chinese glovemakers have a wide divergence in P/B as well, with INTCO currently at 1.8x P/B and Blue Sail at 0.9x P/B.

P/B for glove makers have receeded as the sector derated.

Chinese glovemakers have P/B between 0.9-1.8x

ST risks - temporary destocking

The biggest risk to our thesis in the ST is that end-customers hold off on orders and draw down inventories for the time being. This wait-and-see approach would be underpinned by high volatility in glove ASPs as well as hope that a rapid conclusion to the war would quickly bring naphtha prices down and in turn glove prices.

This is potentially evident in the slower volume sales in March, at the beginning of the war as purchasers defer some orders on the initial price increase.

Our house view is for energy commodity prices to remain elevated till year end, even if the war were to end quickly. Using Brent as a reference, we estimate the benchmark price of oil will remain above US$80/bbl till year end.

What this means for glovemakers - order lead times will remain short through 2Q26. But similar to the cliff facing other energy commodities, we anticipate that the glovemakers will have the most upside when inventories become tight and drives re-stocking by end-users.

All said, we think this dynamic only delays our thesis, but does not negate it. It helps that naphtha prices have already stabilised and cooled since the start of the war. Furthermore, we have imputed a 5% volume hit from demand destruction in our ST earnings assumptions.

The coming headwinds

While we are bullish on glovemakers potential for bumper 2Q/3Q ASPs and earnings, we are mindful of some headwinds that could emerge towards the end of the year. Thus, we flag to investors that to take a 3-6month view on the gloves trade.

The key headwinds we foresee are:

- China’s relative naphtha sourcing advantage

- Intco’s return to the US via Vietnam

- Delayed gas price impact to Malaysian glovemakers.

China has access to Russian naphtha

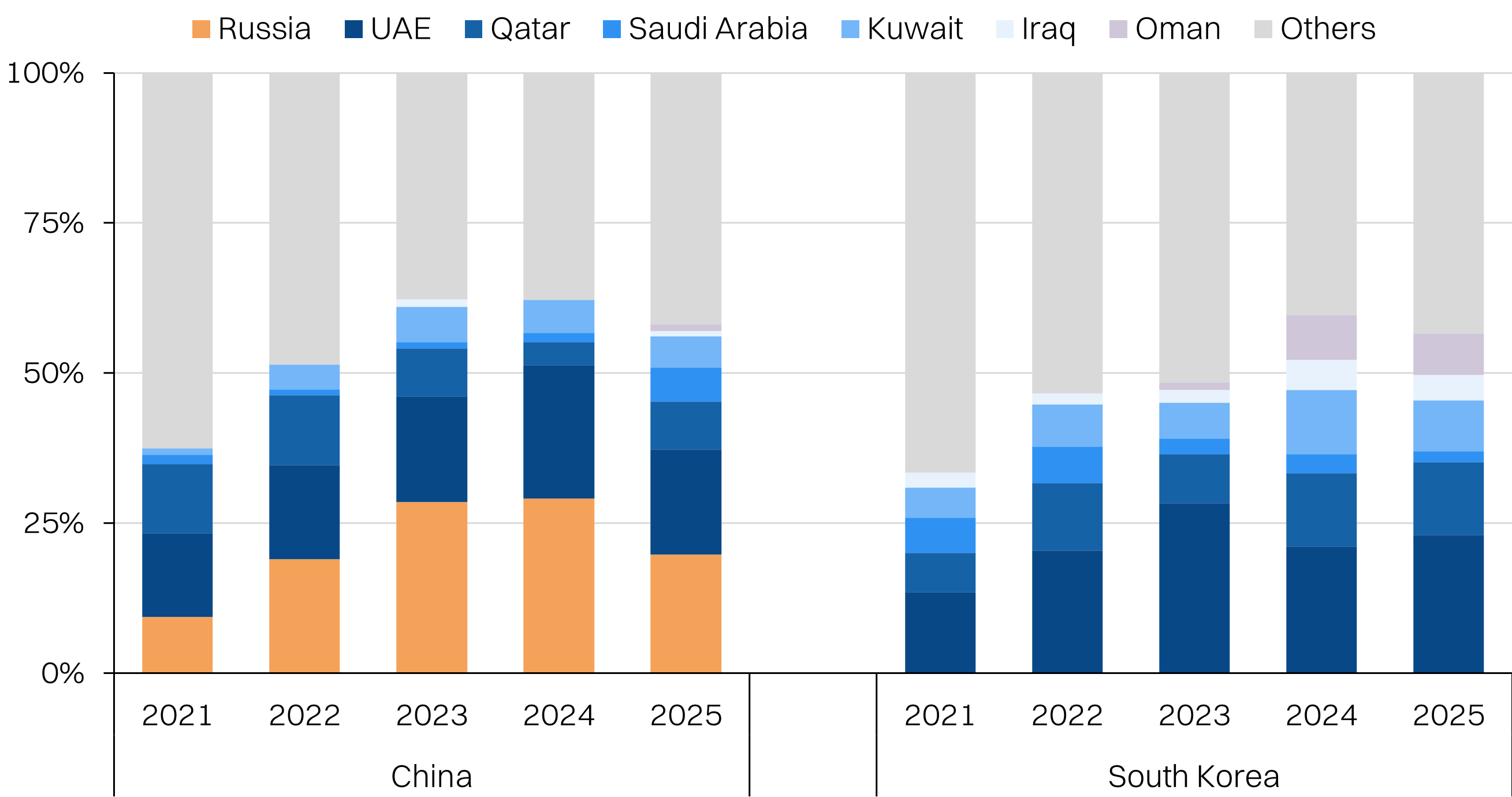

For now, the fluid ceasefire in the Middle East presents substantial uncertainty for nitrile prices and we expect that to translate to the ASPs in the immediate future. However, if the war runs long, we foresee that China could present a structural cost advantage against Malaysian glove makers. This is because China, unlike South Korea, has been sourcing naphtha from Russia.

Data is patchy, but Russia is potentially the top supplier of naphtha to China. This reduces China’s dependency on the Middle East-sourced naphtha that is currently being choked by the war. For context, China has historically faced higher naphtha prices due to structural limitations with its crackers for reasons that are somewhat technical that we will not get into.

Looking ahead, Chinese glovemakers’ historic disadvantage on nitrile costs could narrow going forward, depending on how the Strait closure plays out. This is on top of supply security. In turn, this would put incremental pressure on Malaysian glovemakers’ ASPs.

Two mitigating factors to consider. Firstly, Ukrainian drone attacks have been increasingly successful at damaging Russian energy export infrastructure, which could tighten supplies. Secondly, Russia does export naphtha into Southeast Asia as well, including Malaysia. Malaysian glovemakers could switch up nitrile sourcing towards a Russian feedstock source.

Keep in mind that Chinese glovemakers appear to have an advantage with production costs due to better automation as well as energy costs, using coal-fired cogeneration instead of natural gas.

China-SEA implied nitrile price spreads are narrowing

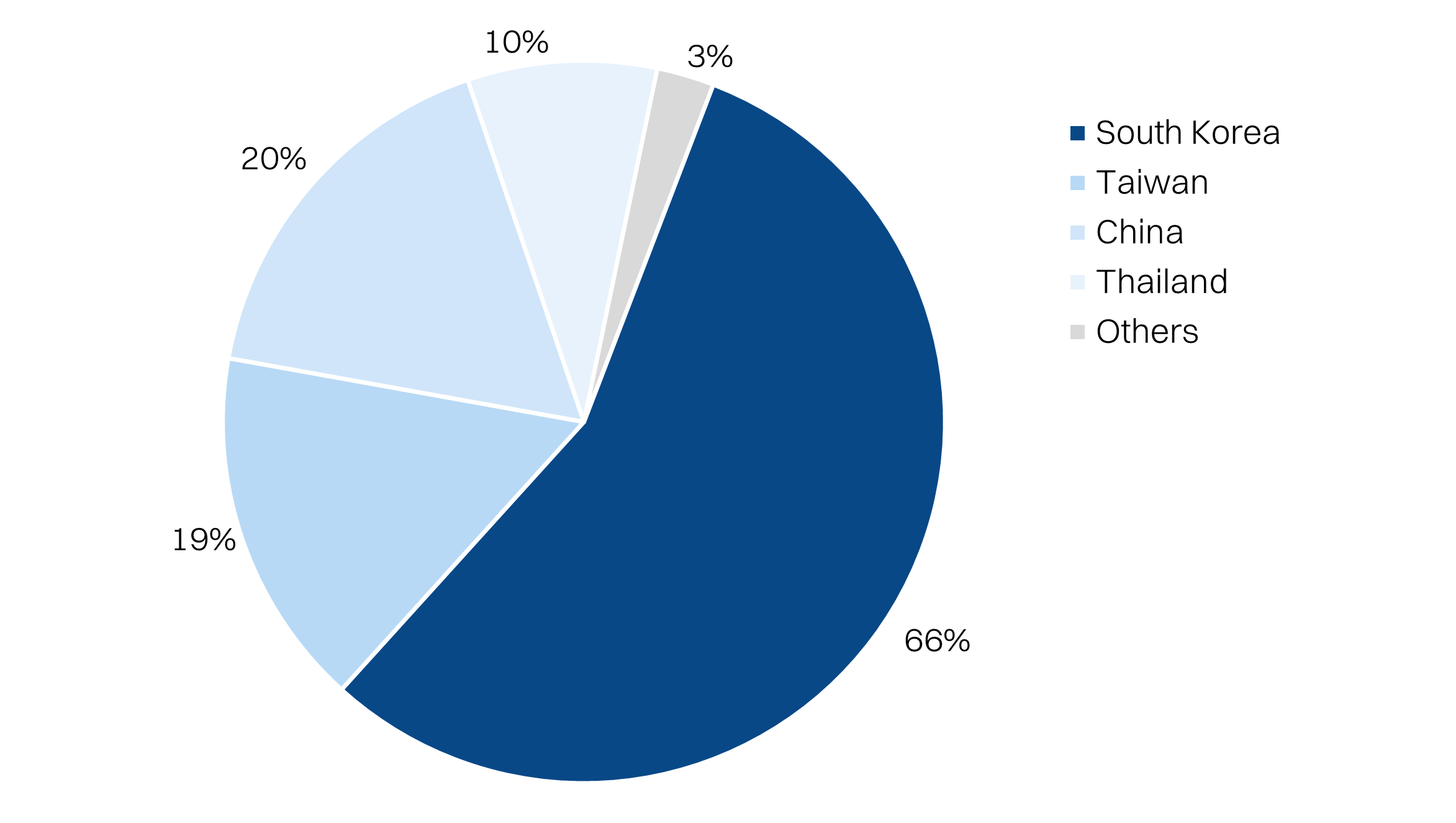

2024 Malaysia's NBL import

China vs South Korea light oils imports (includes Naphtha)

Chinese moving to circumvent US tariffs

Chinese glovemakers are proactively acting to circumvent the 100% tariffs imposed by the US under Section 301. The most visible of these has been INTCO’s investment of capacity in Vietnam. Based on the company’s annual report and other filings, the new Vietnamese-based capacity should have started to come online in late-2025. We have limited visibility on the scale and timing of this additional capacity.

However, INTCO did indicate that total capacity growth will be about +16bn pcs/year (from 87bn pcs to 103bn pcs) over 6 months. Assuming a substantial portion of that capacity is coming from Vietnam with the express intention to target the US market, we anticipate the incremental dilution to Malaysian glovemakers’ share would start to peak towards late-2026.

Rising gas prices

We estimate natural gas prices will rise by 20-25% by 4Q26. Currently, Malaysian gas consumers are fully insulated from the war price shock to gas thanks to the 6-month lag in the transmission of the MRP (Malaysia Reference Price, for LNG) to the effective tariffs. Note that Malaysia’s imported LNG is almost entirely sourced from Australia.

In turn, Malaysian glovemakers are actually enjoying substantial albeit temporary energy cost advantage compared with the Chinese competition. Fuel costs typically make up 15% of total costs and is the second largest cost item after raw materials.

We estimate that a 25% jump in fuel prices that is not passed on will translate to a -50% to -60% PATAMI impact, against our existing baseline assumptions. We do not expect a full hit, since glovemakers would try to pass on some of the costs. However, we expect ASPs will still have to respect the benchmark set by the Chinese competitors in most markets, resulting in some potential margin compression.

JCC & MRP - not yet reflecting the US-Iran War