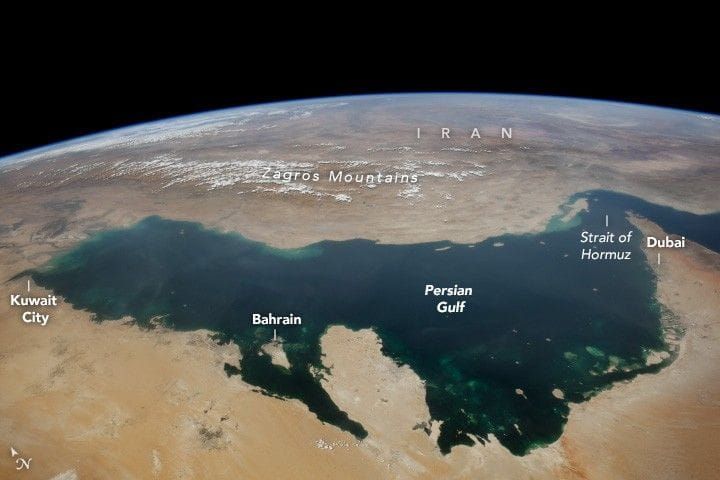

War in the Middle East

Shipping through the Strait of Hormuz has been frozen due to the war.

Malaysia Strategy

Disclaimer: By using this information, you acknowledge that you are solely responsible for evaluating the merits and risks of any investment decision and agree not to hold NewParadigm Research liable for any damages arising from such decisions.

Key takeaways

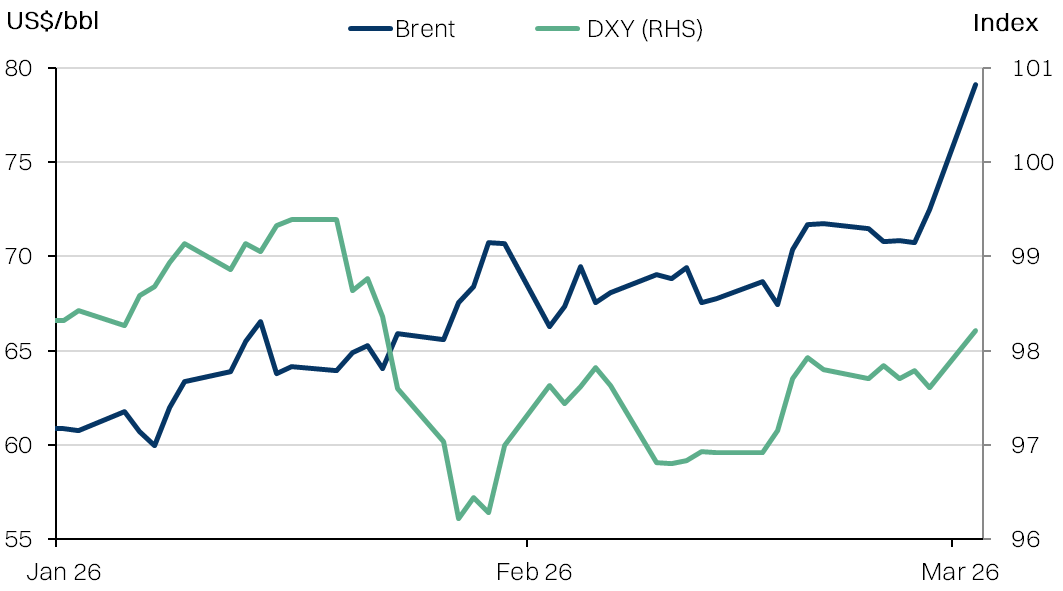

- Oil - Brent is up +9% to ~US$79/bbl following the effective closure of the Strait of Hormuz. OPEC+ production boost is tempering fears but cannot compensate for prolonged closure.

- Dollars: DXY up +0.6% but may yet overshoot if there is a short squeeze. As a top outperformer pre-conflict, the ringgit will be vulnerable. We see risk of depreciation back towards 4.10.

- Inflation: Central banks may face the stagflation dilemma, not unlike Ukraine-Russia 2022. Taking the 2H Fed rate cut off the table will not help risk-off pressure on equities.

Brent and US$ on the rise / Key indices at onset of Russia-Ukraine war

Source: Bloomberg, NewParadigm Research, March 2026

Catalyst for rotation

- With the killing of Iran’s supreme leader, Ayatollah Ali Khamenei, the US and Israel have climbed the escalation ladder almost to its topmost rung.

- The four horsemen of this conflict will be oil, dollars, inflation, and regional contagion. The big question is - how long will this war last? Or more critically - how long will the Strait of Hormuz remain closed?

- We simplify the complex and fluidly developing event into two scenarios on opposing ends of the barbell: a protracted war of attrition or a relatively rapid deescalation.

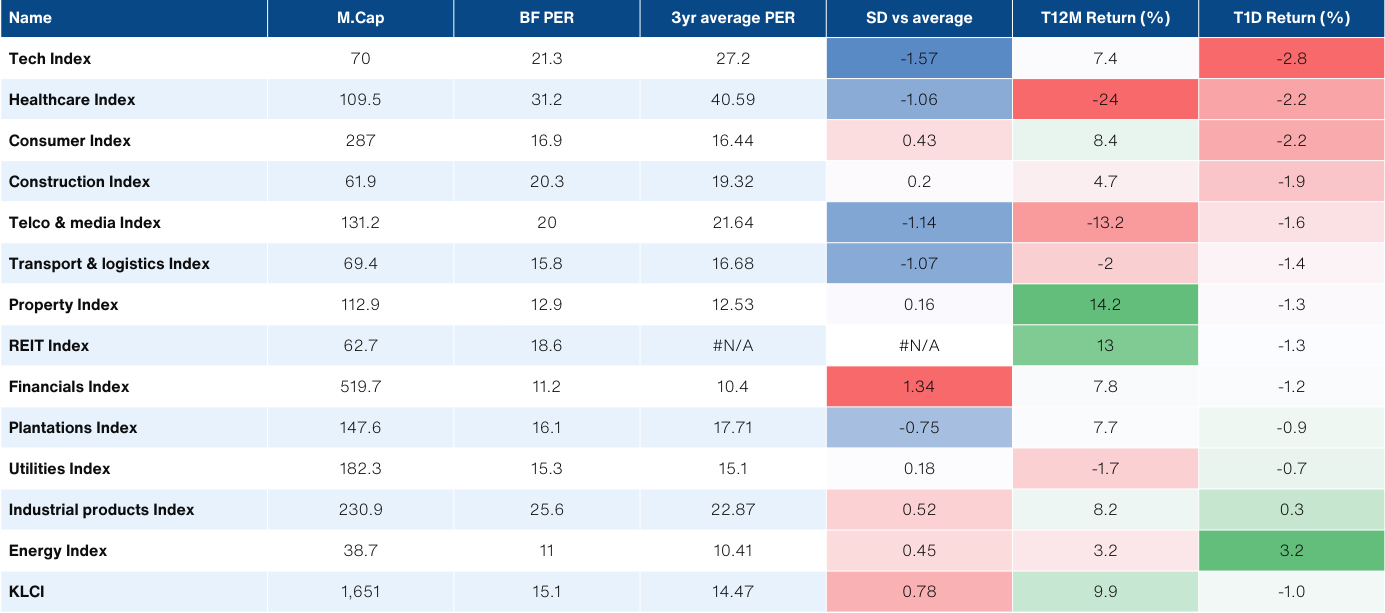

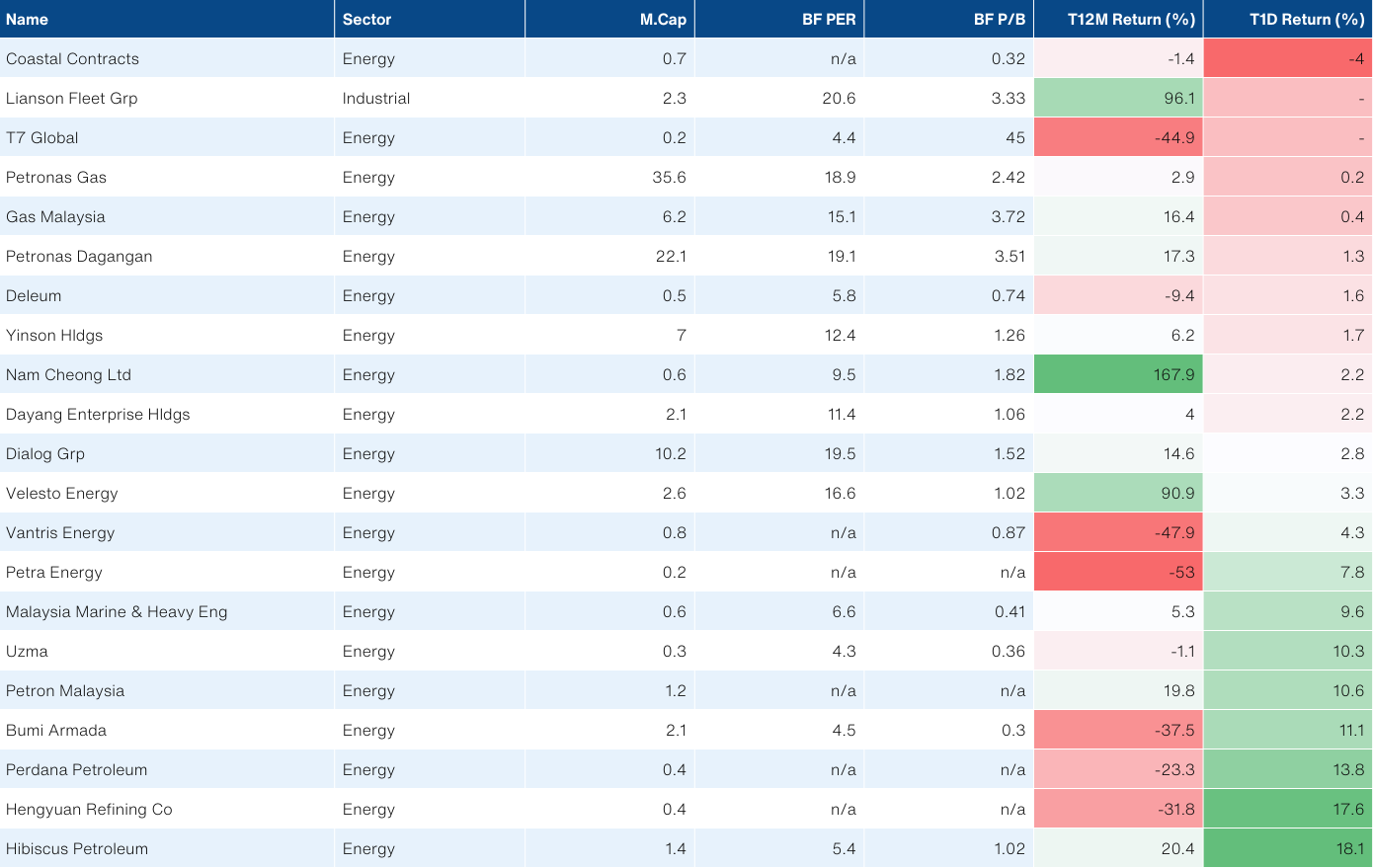

- In the first scenario, we see deeper and broader downside risk to the market, particularly from over-valued sectors. We flag financials, consumer and property for this risk. At the same time, O&G names that directly benefit from higher oil prices (e.g. DLG, HIBI) would be key beneficiaries.

- Rotation could also put laggard sectors in the spotlight, and we like the tech sector for this, as it would benefit from the stronger dollar. That said, we’d be wary of manufacturers of discretionary products that get hit by the stagflation double whammy - higher input costs and weaker demand.

- In the second scenario, we’d expect to see a rebound in the market, as future risks are priced out. From the current market levels however, the upside would be fairly limited. This scenario would mostly see the oil price beneficiary trade unwind.

What to do

- We think the risk remains tilted to the downside. While some of the risk has been priced in ahead of the event, the post-event correction has been relatively moderate. We think some of the tail risks are not being factored in.

- Within our coverage FRCB is the top beneficiary on ringgit weakness, as the bulk of earnings is denominated in TWD.

- Within our non-rated research, the top loser from higher oil prices and stronger dollar would be AAX, with high sensitivity to both. We also flag that SPZ and LWSABAH as potential losers if resin costs (USD costed and petroleum-derived) were to spike.

Scenario A: prolonged attrition

- Why this is possible: This is less likely to be a repeat of the previous 12-day war with Israel. Initial reports suggest Iran’s strategy and posture is different. Attacks have not been telegraphed, and it has been broader in scope - even hitting other countries in the region. Critically, it appears that the low-value drones are being deployed first in an attempt to exhaust air-defense batteries. In short, Iran appears to be positioned for a longer war of attrition rather than a relatively short show of force as a deterrent.

- Another notable change is the reports of attacks on commercial vessels in the Strait of Hormuz, with 3 reported so far. With relatively few resources, it would be possible for Iran to make transit too risky for insurers to cover, which would effectively shut the passage.

- The big question is around capability to sustain the pressure. Iran has access to the relatively affordable Shahed drones that have an estimated cost of US$20k-US$50k to produce, which it has been supplying to Russia. That said, US/Israeli strikes have been targeting production facilities.

- So what: In this scenario, oil prices in particular could surge to over US$100/barrel, as the Strait of Hormuz accounts for 20% of global crude flows. While oil production could be boosted (and OPEC+ has shown a willingness to do so), it would not be able to compensate for the logistical disruption. In turn, this could recreate similar global macroeconomic headwinds from the Russia-Ukraine war in 2022 - a spike in global inflation that also puts pressure on growth.

Scenario B: Rapid deescalation

- Why this is possible: Iran’s internal politics are very fluid at the moment with reports of over 40 key leaders having been killed in strikes. Prior to the attacks, Iran had already had to violently put down protests in the streets due to worsening economic conditions in the country. This is among the reasons the US is hoping to see rapid regime change and a de-escalation.

- A more pragmatic consideration is simply Iran’s capability to sustain the conflict. US/Israel have demonstrated the capability to strike targets with impunity and are targeting Iran’s launchers under a “kill the archer” strategy. This puts somewhat of a clock on munitions as commanders face “use it or lose it” dilemma.

- Circling back to the economy, Iran is heavily dependent on its oil exports. Shutting the strait would be self-defeating and severely cripple Iran’s already limited economic resources. Unlike Russia, Iran’s domestic economy is not as self-sufficient.

- In this scenario, risk of escalation declines, but intermittent disruption to the strait remains likely. Still, it should help curb concerns around contagion risks and settle market volatility on both oil and the USD.

Key event to watch for:

Iran previously made a strategic “bargain” - that it would focus its attacks on Israel and leave the strait mostly undisrupted on the basis that its adversaries would also leave its oil production facilities intact. If Iran reverts to this strategic posture, it would quickly drive a scenario B outcome. Conversely, attacks on Iran’s oil production facilities and/or its tankers would remove any remaining self-interest to keep the strait open to facilitate the export of its own crude that is crucial for its economy.

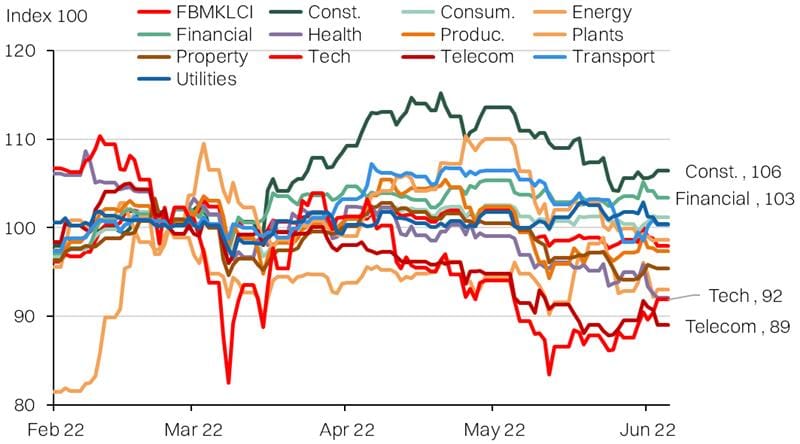

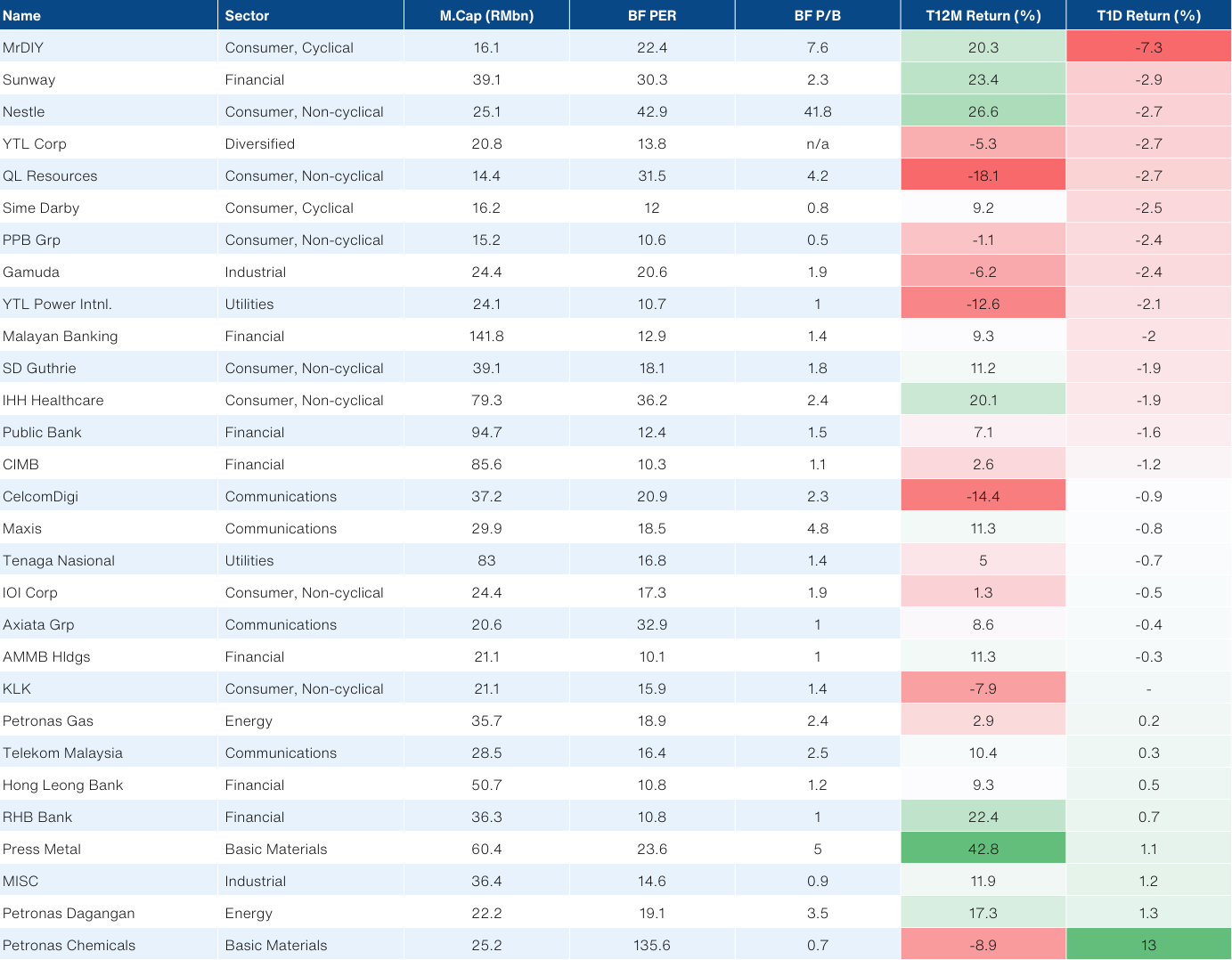

Performance of key sectoral indices | Performance of KLCI component stocks

Source: Bloomberg, NewParadigm Research, March 2026

Performance of selected O&G stocks | Performance of selected Tech stocks

Source: Bloomberg, NewParadigm Research, March 2026